Housing Continues to Seemingly Defy Gravity

- Housing defied expectations and displayed surprising resilience in the first half of 2023.

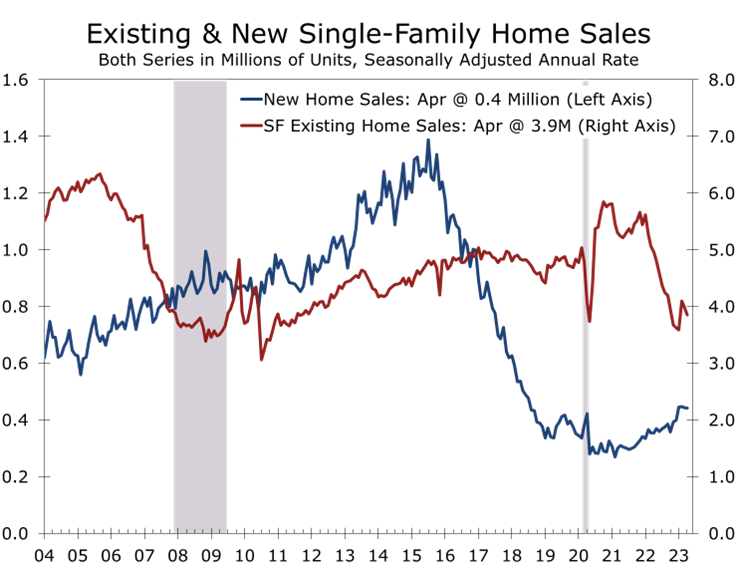

- Sales of new and existing homes rebounded, as mortgage rates briefly fell back to 6% at the start of the year.

- Most homeowners hold mortgages at rates well below the prevailing mortgage rate, which has made them reluctant to sell.

- With existing inventories exceptionally low, the revival in sales rekindled bidding wars for those homes on the market and pushed many buyers toward new homes.

- After falling in the second half of last year, home prices rebounded modestly this spring.

- Bottom line: New and existing home sales outperformed reduced expectations during the first half of this year. Housing is undersupplied and the revival in demand is real. Unfortunately, affordability is stretched, and interest rates are likely to rise further.

This marks our first installment of our quarterly Housing Chartbook, which will track key trends driving the market, including recent trends in sales and construction, mortgage rates, inventory levels, housing affordability, buyer attitudes and regional conditions. We will also include a detailed forecast for single- and multi-family starts, new and existing home sales, home prices and interest rates. Look for a link at the end of the html version of this report.

New and existing home sales rebounded earlier this year, as mortgage rates reversed much of the spike that occurred last fall. Buyers who had canceled purchase contracts or put buying plans on hold, returned to the market in January and February.

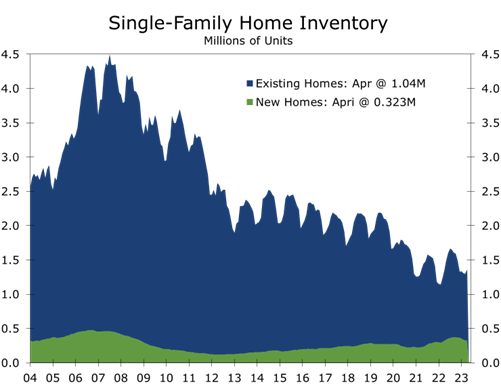

The turnaround in home sales occurred when inventories were unusually low. Eighty percent of outstanding first-lien mortgages have rates below 5% and 60% have rates below 4%. With such low rates, fewer homeowners are looking to sell. The scarcity of new listings set off intense competition for what homes were on the market. Home prices, which had been falling since the middle of last year, did an abrupt about face. The lack of existing homes for sale has also pushed more buyers toward new construction.

The paucity of existing homes for sale has pushed more buyers toward new construction.

Following a spike in cancellations last fall, home builders shifted some of their production to rentals earlier this year. The influx of higher-margin traditional buyers has greatly boosted builder confidence. After slumping to 31 in December, the NAHB/Wells Fargo Housing Market Index has rebounded to 55.

Following a pullback resulting from last fall’s mortgage rate spike, single-family starts have rebounded somewhat. We expect single-family starts to maintain their recent pace for a few months but slow later this summer amidst higher interest rates and slower economic growth. Builders still have a substantial backlog of projects underway, and many are looking to clear backlogs as supply chain disruptions diminish further.

Demand for homes revived most significantly in the South, benefiting from strong in-migration and greater relative affordability compared to the West Coast and Northeast. The West experienced the most significant price declines last year, while prices held up best in the South. Florida is currently seeing some of the strongest home price appreciation, which has greatly diminished affordability for native buyers.

Robust job growth continues to drive demand for apartments, particularly in the South. The limited availability of homes for sale has bolstered lease renewals for apartments, helping contributed to a 6% year-to-year increase in rents. There is an enormous supply of apartments due to be completed in the South this year and next, however, which will push vacancy rates up a couple of percentage points or more and weaken rents. Credit underwriting for new apartment projects is expected to tighten further, bringing about an overdue correction in apartment development.

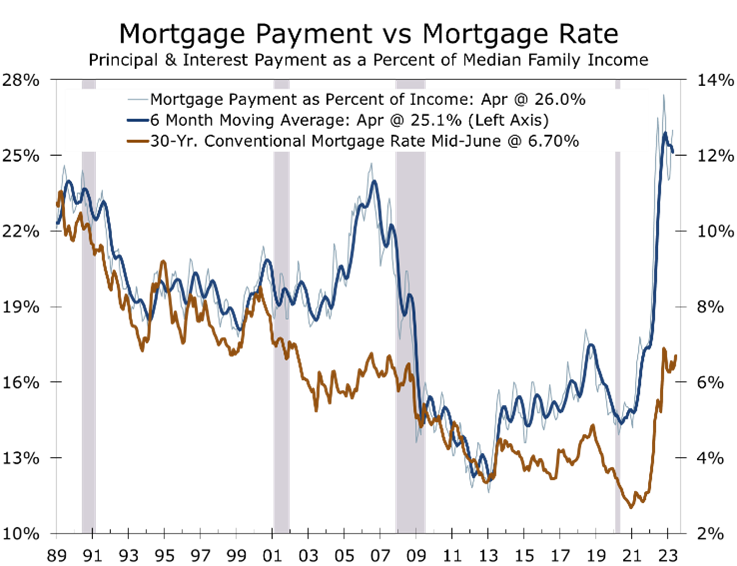

Affordability hurdles currently exceed levels hit at the height of 2005-2007 housing bubble. The monthly principal and interest payment on a median priced home has soared to $1,972, which equates to 26% of median household income. Property insurance and taxes have also risen across much of the country, creating an even greater hurdle.

With housing affordability so stretched a correction in home sales seems likely. The migration of well-heeled buyers from Northeast and West, where median household income is $103,337 and $99,543, respectively, to the South, where median family income is $83,537, has masked the extent to which affordability has deteriorated. Migration will likely taper off as job growth slows, more clearly exposing the lack of affordability for native buyers.

With the Fed expected to raise rates at least one more time and then hold rates at that level until next spring, mortgage rates will provide little near-term relief. There is room for mortgage rates to fall, however, as the spread between the 10-Year Treasury Note yield and 30-Year fixed rate mortgages is unusually wide. That spread should narrow as economic activity cools and interest rate volatility subsides.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.