Uncertainty Keeps Fed in Wait-and-See Mode

- The Fed held its federal funds rate target steady at 4.25%-4.5%, maintaining the pause that began in January following 100 bps of cuts from September to December 2024.

- The Fed notes that economic growth remains solid despite volatility in net exports, which pulled down first quarter real GDP growth.

- The policy statement also noted that uncertainty about the economic outlook had increased further since the last meeting.

- The Fed also noted that the risks of higher unemployment and higher inflation had have risen, which has amplified talk of stagflation.

- Powell noted that it is too early to know how tariff policy will ultimately settle out and what that would mean for inflation and labor market conditions. With both in a relatively good place, now is not a bad time to wait and see where trade policy evolves.

- We continue to believe the Fed is underestimating labor market risks and anticipate weaker job numbers in the coming months, which may prompt the Fed to begin to cut rates as early as July.

The Federal Reserve left its federal funds rate target unchanged at 4.25% to 4.50% at its May 6–7 meeting, extending a pause that began in January following 100 basis points of cuts between September and December 2024. The decision was widely anticipated, but the accompanying policy statement reflected a more cautious tone, with the Fed highlighting increased uncertainty about – rather than around previously – the economic outlook, persistent inflation pressures, and growing risks to the labor market. The slight switch implies an acknowledgement that the risk of recession have increased.

Chair Jerome Powell reiterated the Fed’s data-dependent stance, emphasizing that more time is needed to assess whether recent soft data foreshadow a meaningful slowdown or simply reflect noise. Powell also underscored the lack of clarity on tariff policy, noting it is too early to determine where trade measures will ultimately land—and how they will impact inflation and employment

Fed Chair Jerome Powell feels that monetary policy is in a pretty good place to wait and see.

The FOMC noted the economy continues to expand at a solid pace, supported by resilient consumer demand and a labor market that remains historically tight. Private final domestic demand grew at a 3% annualized rate in Q1. However, volatility in net exports pulled first-quarter GDP growth down at a 0.3% pace.

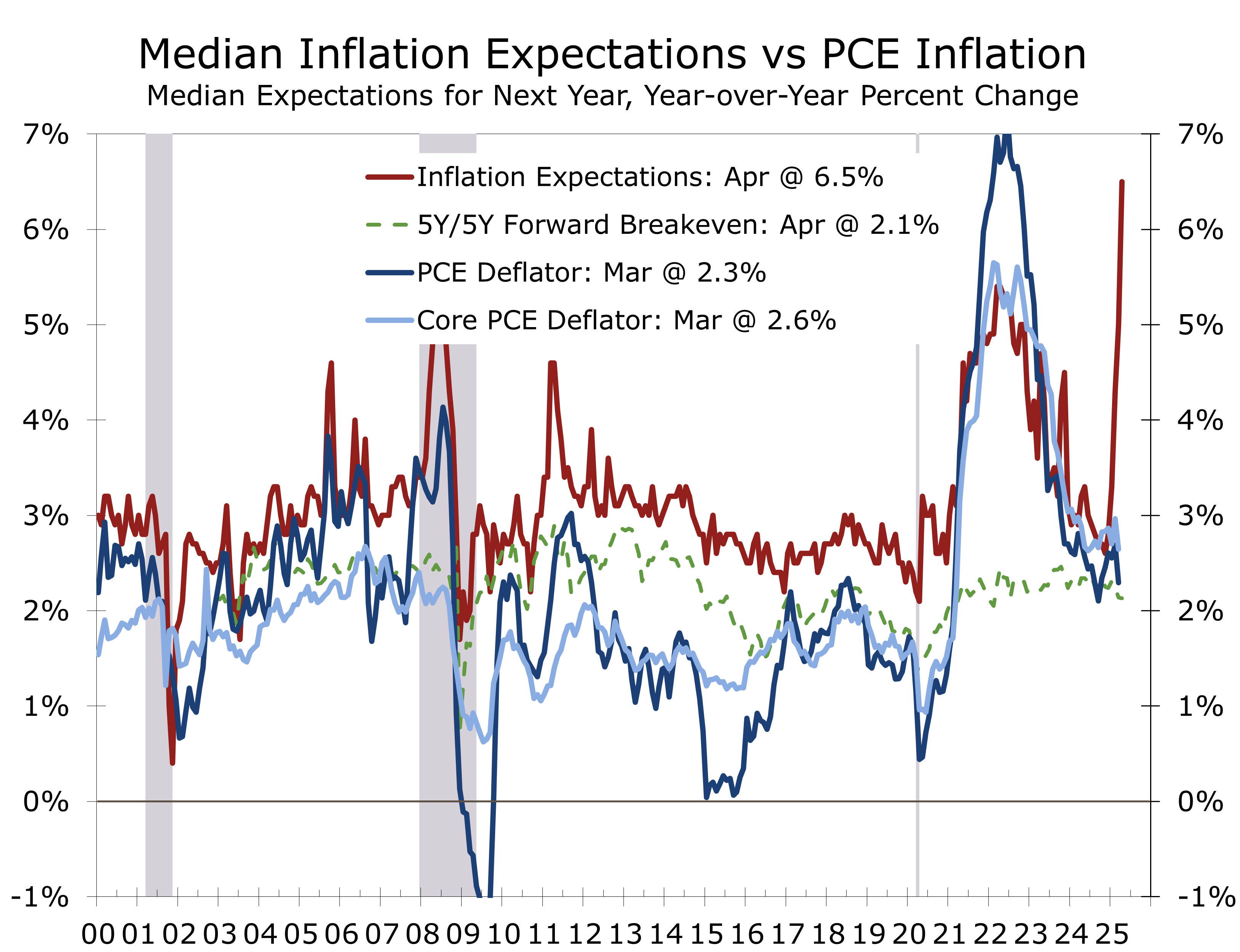

The most recent inflation data show prices pressures have moderated, with core PCE up 2.6% year-over-year in March—still above target but moving in the right direction. The impact of tariffs, however, will take time to work its way into the data. The rise in consumer expectations for inflation could become self-fulfilling if consumers rush to purchase goods ahead of tariffs or shortages. Used car prices have already risen sharply.

Surging inflation expectations may feed into actual inflation, becoming self-fulfilling.

More time is needed to fully assess risks. While hiring remains solid overall, surveys suggest momentum is weakening. Job openings have declined, and anecdotal reports indicate job seekers are having a harder time finding work. The share of consumers expecting hiring to slow has also jumped. Powell acknowledged that labor market conditions remain healthy but emphasized the need to monitor for further softening.

The May meeting did not include updated projections, but the March Summary of Economic Projections downgraded 2025 GDP growth to 1.7% and raised core inflation expectations to 2.8%, reviving concerns about stagflation. The May statement noted that risks of both higher inflation and rising unemployment have increased, suggesting that internal growth forecasts have likely been revised down further

Powell emphasized that holding rates steady gives the Fed time to assess the inflation and employment effects of shifting trade policy. The Fed also continues its balance sheet runoff, reinforcing its broader commitment to normalization.

Powell signaled no urgency to move policy in either direction, citing a balanced economic backdrop. However, he acknowledged that tariff-driven inflation could be persistent and hard to isolate. While some measures of inflation expectations have ticked up, market-based gauges remain stable. The 5-year, 5-year forward inflation expectation rate—derived from inflation-indexed Treasuries—continues to reflect well-anchored long-term inflation expectations.

We expect quarter points cuts in both July and September, based on a weaker labor market than the headline data suggests. We estimate true job growth is closer to 100K per month—about one-third slower than reported—just enough to keep unemployment flat. We expect the jobless rate to rise another 50 basis points by year-end, as hiring slows and employers grow more cautious. The economy is approaching the edge of recession, with a roughly 45% probability and the Fed will move more aggressively if conditions worsen.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 7, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000