The Manufacturing Revival Stalls

- The ISM Manufacturing Purchasing Managers Index (PMI) fell 1.1 points in April to 49.2.

- Despite the drop, manufacturing shows signs of strengthening, with normalized customer inventories and fewer supply chain issue.

- The underlying details were soft, with new orders and production both weakening. The employment index rose but remained in contractionary territory.

- Supplier deliveries improved, indicating faster delivery times and fewer supply disruptions.

- The inventory index remained steady at 48.2, which means more manufacturers reported inventories declining rather than rising.

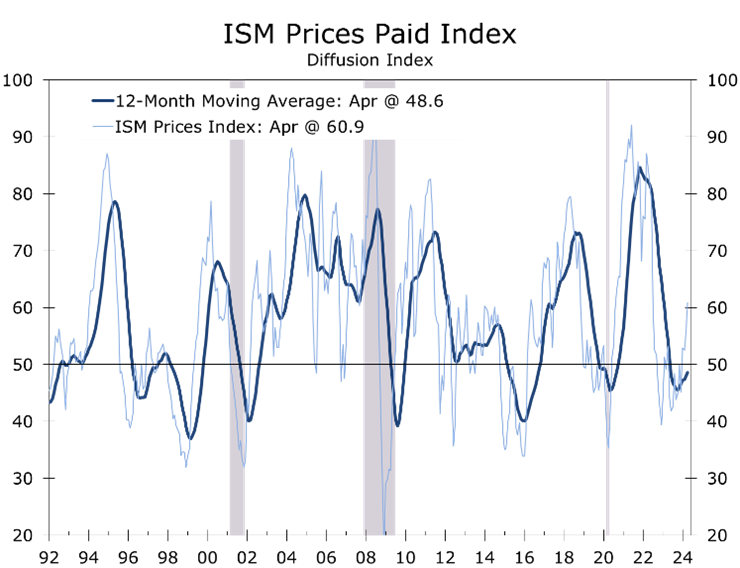

- The Prices Paid index jumped 5.1 points to 60.9, reaching its highest level since June 2022 and adding to fears of stagflation.

- April’s weaker than expected ISM report adds year another piece of evidence to the growing chorus of forecasters project a return of stagflation. We do not expect to see a return of 1970s-style stagflation. Manufacturing activity will likely improve modestly this year, while a stronger recovery overseas pulls commodity prices higher and squeezes manufacturers profit margins.

The ISM manufacturing index slipped back into contractionary territory, with the headline index falling 1.1 points to 49.2. A reading below 50 means more manufacturers report conditions are weakening than report they are strengthening. The overall ISM manufacturing index has been below 50 for 17 of the past 18 months, with the lone expansionary reading coming in March.

Even with April’s drop, manufacturing activity is showing some tentative times of strengthening. Customer inventories have largely normalized, and supply disruptions have largely dissipated. Output is improving slightly faster overseas, however, than it is improving at home, with the stronger dollar lowering the price of imports and making US exports more expensive to overseas buyers.

Manufacturing activity softened a touch in April, while prices paid by manufacturers increased.

April’s 1.1-point drop was worse than had been expected. New orders and production both weakened, while there was a slight uptick in the employment component. The new orders series fell by 2.3 points to 49.1, while the production index fell 3.3 points to 51.3. The employment component edged 1.2 points higher but remained in contractionary territory at 48.6.

Supplier deliveries declined 1.0 point to 48.9, indicating faster delivery times for a larger proportion of respondents. There are far fewer supply disruptions today and supply chains have largely normalized. The lead time for production materials increased 1 day to an average of 79 days, compared to an average of 67 days in 2019 (prior to the pandemic) and a peak of 100 days in July 2022. The inventory index was unchanged at 48.2, meaning more manufacturers reported inventories declining than rising.

Prices paid by manufacturers jumped 5.1 points in April to 60.9 on a non-seasonally adjusted basis. The increase is yet another data point hinting at the return of some sort of stagflation. We believe there is more to the story, however, and see the recent uptick in the prices paid series reflecting rising manufacturing output overseas, particularly in China.

A global manufacturing rebound is pulling industrial commodity prices higher.

In April, 31% of companies said they paid higher prices (up from 24% in March), with only 9% reporting paying lower prices (down from 12%). Several key commodity prices have increased, including crude oil, aluminum, steel, and plastics. The recent spike in crude oil has eased somewhat, as Iran/Israel tensions have subsided. The rise in industrial commodity prices aligns with the recent strengthening in output overseas.

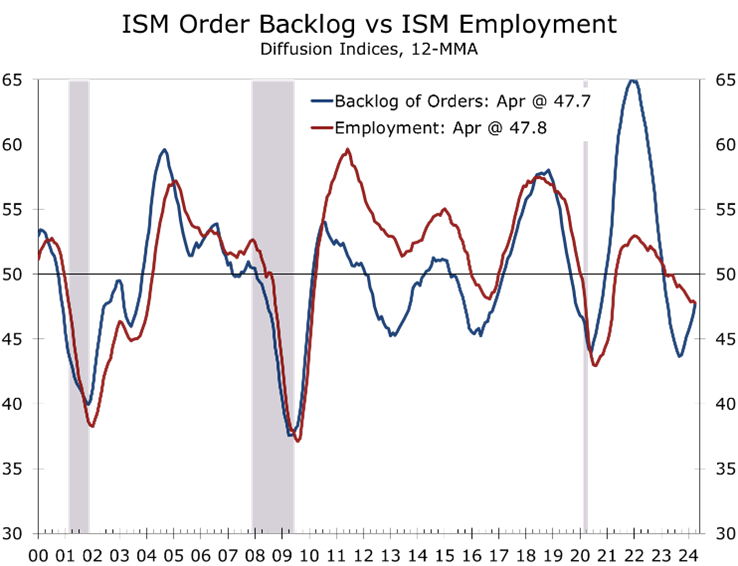

The ISM employment index rose 1.2 points to 48.6 in April, indicating a slight narrowing of the contraction in manufacturing payrolls. April marks the 7th consecutive month of contraction, however, meaning more reductions in manufacturing employment than new hires. An Employment Index above 50.3 percent typically corresponds to a rise in the BLS monthly payroll manufacturing measure.

Separately, the BLS reported job openings declined in March, falling from 8.8 million openings to just under 8.5 million. Job openings in manufacturing also declined, falling from 587,000 to 570,000 openings. Only 4 of 18 industries in the ISM survey — transportation equipment, computers and electronic equipment, textiles, and nonmetallic mineral products – added jobs in April, while 7 cut staff and 7 others reported no change.

We continue to expect the manufacturing sector to modestly strengthen this year, with orders rising amidst solid final demand and normal/low inventories. Manufacturing employment will take longer to recover, however. Manufacturers tend to hold off adding staff until order backlogs rise and that still appears to be a few months off.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 1, 2024

mark.vitner@piedmontcrescentcapital.com

Chief Economist (704) 458-4000