Key Takeaways from December’s ISM Report

-

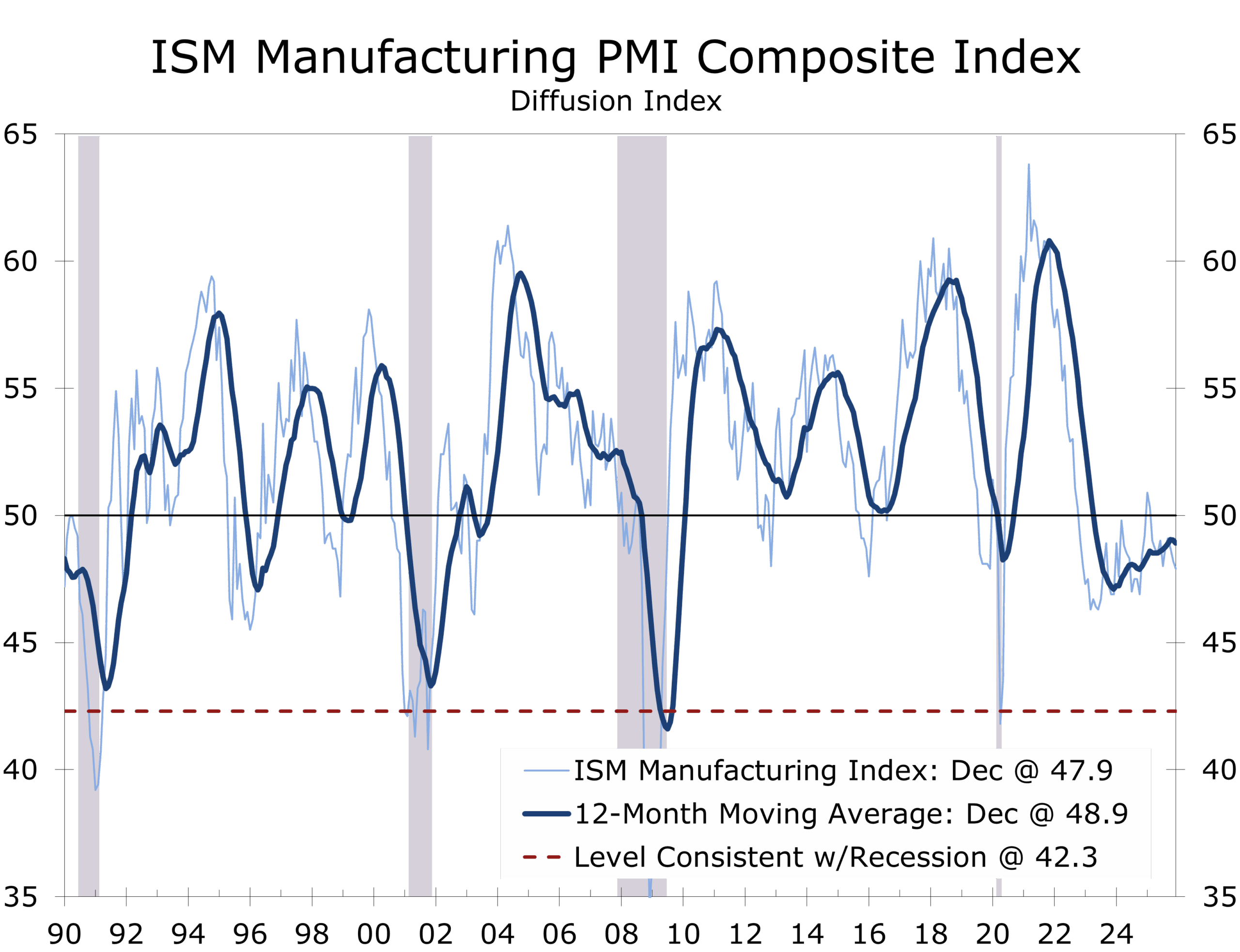

- Manufacturing PMI®: 47.9 (–0.3 pts) — lowest reading of 2025; 10th straight month in contraction.

- New Orders: 47.7 (+0.3 pts) — still contracting, but marginally firmer; early stabilization, not a turn.

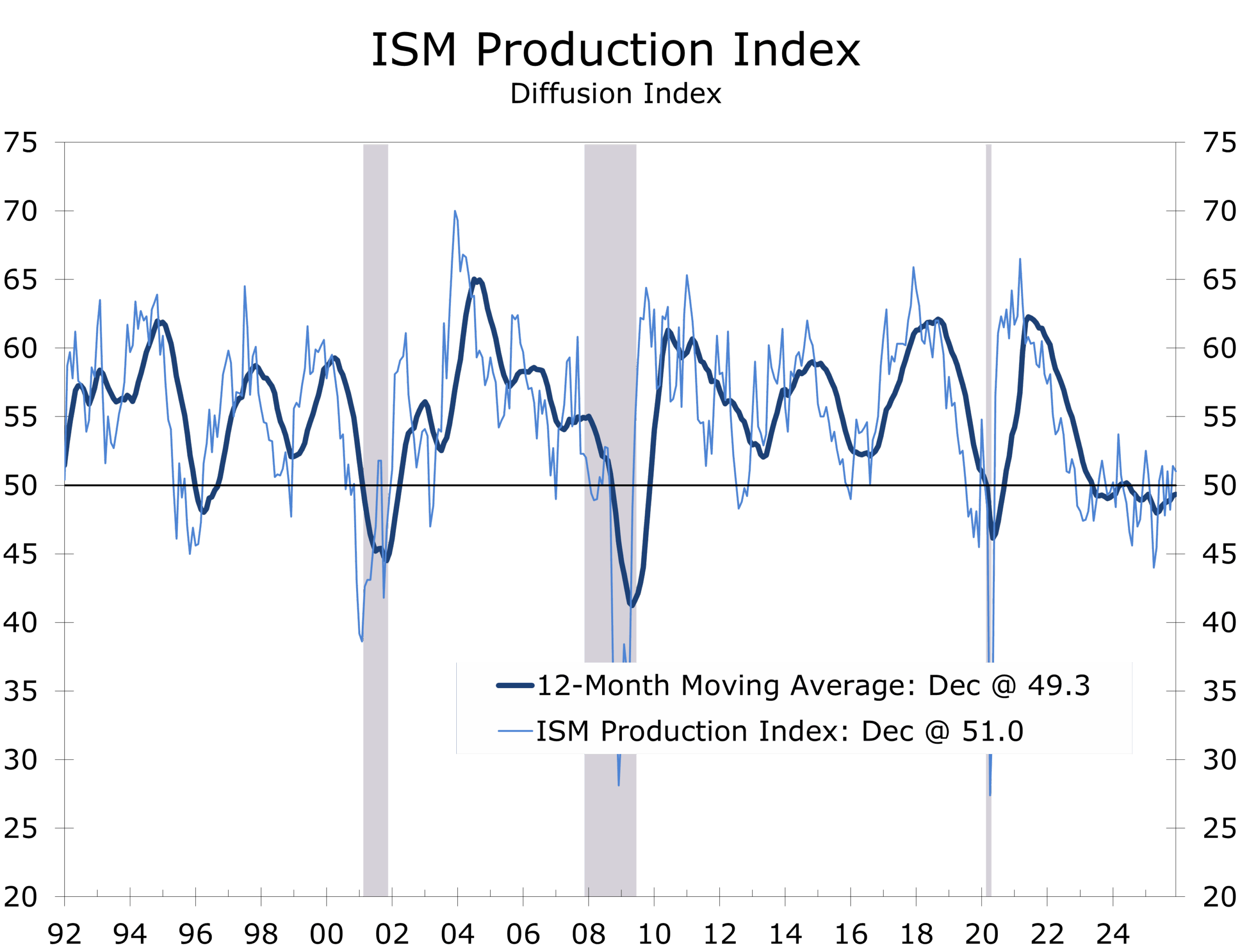

- Production: 51.0 (–0.4 pts) — still expanding, but losing momentum as demand remains soft.

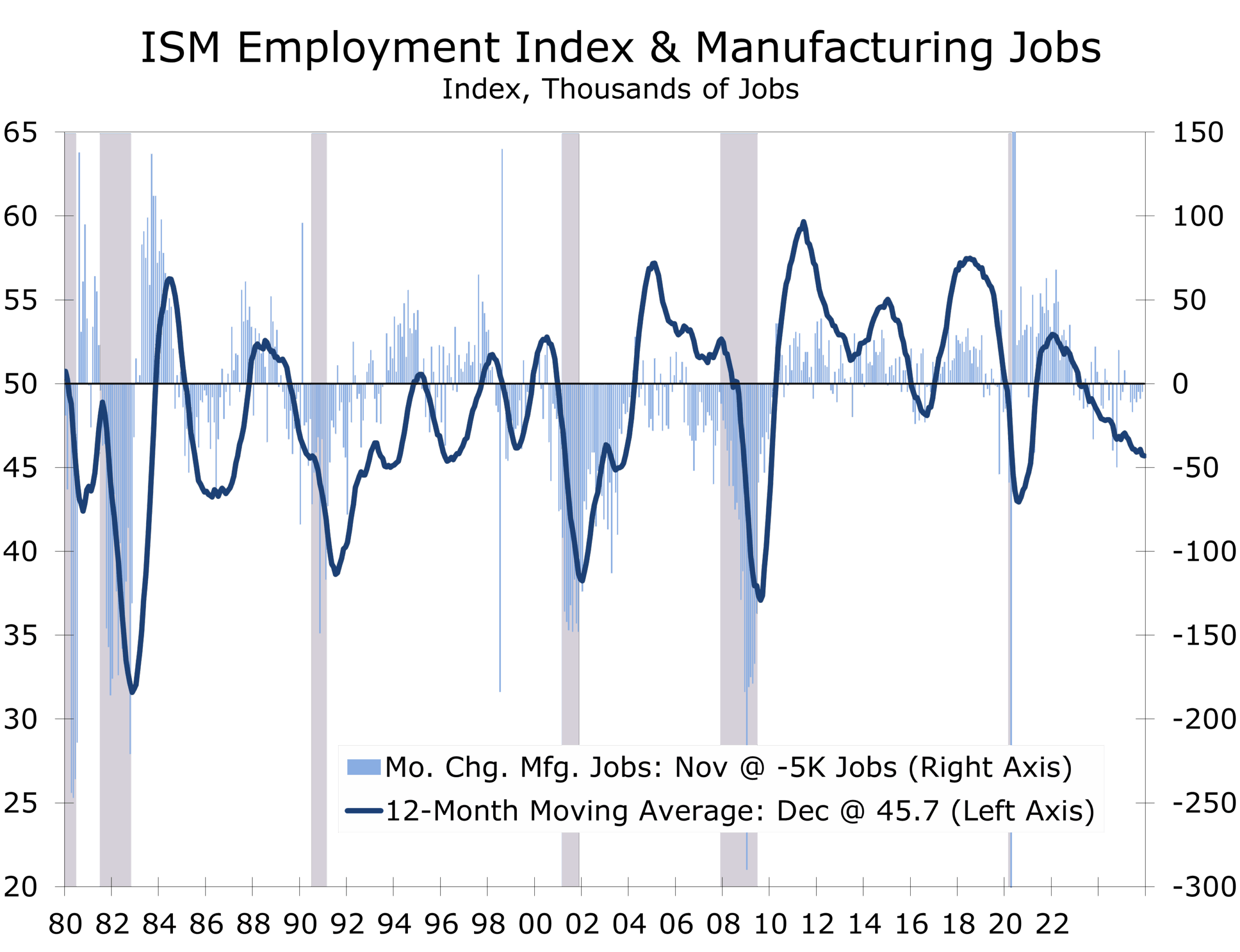

- Employment: 44.9 (+0.9 pts) — contracting at a slower pace; firms still managing headcount.

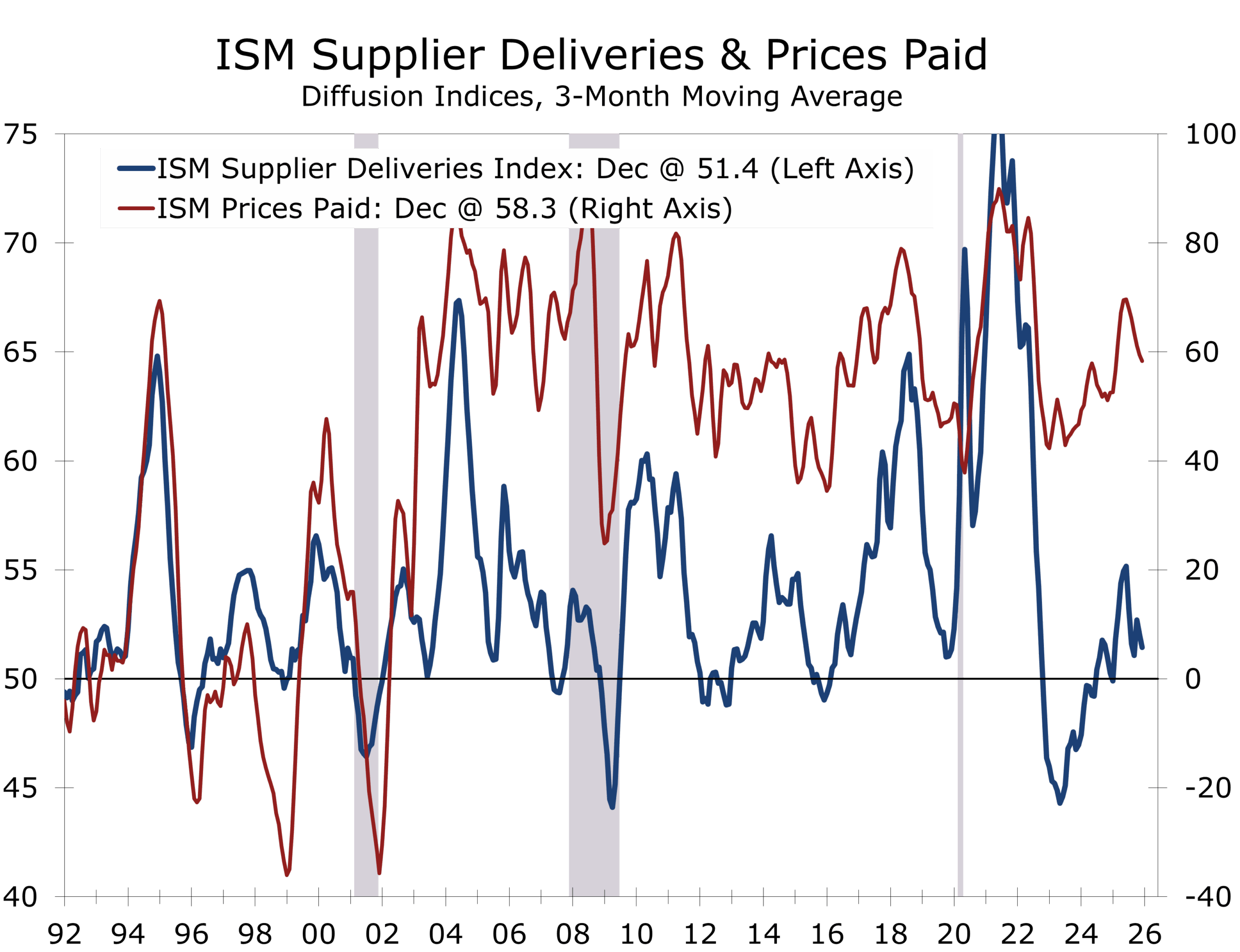

- Supplier Deliveries: 50.8 (+1.5 pts) — back to slower deliveries after one month “faster”; pockets of constraint persist.

- Inventories: 45.2 (–3.7 pts) — sharp drop; restocking is not happening yet.

- Customers’ Inventories: 43.3 (–1.4 pts) — “too low” and more acute; a future tailwind if confidence returns.

- Prices: 58.5 (unch.) — sticky cost pressure, still dominated by metals and tariff-affected inputs.

- Backlog of Orders: 45.8 (+1.8 pts) — improved, but still contracting; pipelines remain thin.

- New Export Orders: 46.8 (+0.6 pts) — slightly less weak; still sub-50.

- Imports: 44.6 (–4.3 pts) — notably weaker; suggests demand restraint and/or tariff-driven sourcing shifts.

- GDP signal: ISM equates 47.9 to roughly +1.6% annualized real GDP, consistent with continued overall expansion. Core GDP is running about a percentage point higher, helped by continued strong capital spending.

Lean Inventories Persist as Confidence Limits Growth

The ISM Manufacturing PMI® slipped to 47.9 in December, the lowest reading of 2025 and the sector’s tenth consecutive month in contraction. As with prior months, the sub-50 reading reflects the breadth of softness, not a collapse in activity. Manufacturing remains a drag on overall growth, but the level of the PMI is still consistent with continued overall economic expansion, reinforcing our view that the U.S. economy is moving through a long adjustment phase, or policy reset, rather than a cyclical downturn.

What stands out in December’s report is not deterioration, but hesitation. Capacity is adequate, supply chains have largely normalized, and production continues to expand modestly. Yet firms remain reluctant to take risk, particularly when it comes to inventories, hiring, and forward purchasing. This posture closely mirrors the themes laid out in our 2026 outlook, where policy uncertainty and cost visibility matter as much as demand itself.

Demand is not collapsing, but it is not strong enough to restore confidence.

Demand indicators remain in contraction, but the pace of decline moderated. New Orders (47.7), Backlog of Orders (45.8), and New Export Orders (46.8) all improved modestly from November, suggesting that demand is stabilizing at low levels rather than continuing to weaken. At the same time, Imports fell sharply to 44.6, signaling a deliberate pullback in purchasing and a continued preference for flexibility over volume. This is consistent with an environment where firms are choosing to wait for clearer signals on trade policy, tariffs, and global growth before fully reorienting supply chains and committing capital.

Despite soft orders, Production remained in expansion at 51.0, though momentum eased. Output continues to be supported by execution on existing programs and selective capital spending, particularly in electronics and electrical equipment. This dynamic aligns with our outlook that the current cycle is capital-led rather than demand-led, with growth concentrated in productivity, automation, and targeted investment rather than broad restocking or consumer-driven expansion.

Labor conditions reinforce that interpretation. The Employment Index rose to 44.9, indicating that contraction slowed but hiring did not resume. Firms continue to manage headcounts carefully, relying on attrition and selective reductions rather than expansion. Manufacturing is adjusting gradually to a more capital-intensive model, one that supports output without requiring significant labor growth.

This remains a cycle defined by capital discipline, not labor expansion.

The most important signal in the December report lies in inventories. Manufacturers’ Inventories fell sharply to 45.2, while Customers’ Inventories dropped further into “too low” territory at 43.3. Historically, this combination has been a reliable setup for a restocking cycle. Yet firms are still choosing restraint, running lean inventories and pulling back on imports rather than rebuilding stock.

This divergence confirms a key conclusion of our 2026 outlook: the inventory cycle is deferred, not broken. The ingredients for replenishment are present, but the trigger—greater confidence in policy, pricing, and demand visibility—has yet to emerge. When restocking does arrive, it is likely to be selective, not broad and immediate.

Inventories are lean, but confidence remains the binding constraint.

One major determinant on the timing of an inventory rebuild is costs. Cost pressures continue to shape behavior. The Prices Paid Index held at 58.5, with gains driven primarily by metals and tariff-affected inputs. This remains a cost-push environment rather than a demand-driven inflation story. Persistent input costs, combined with limited pricing power, continue to compress margins and discourage aggressive inventory rebuilding, even as logistics conditions improve.

Sector breadth underscores the narrowness of strength. Only two industries expanded in December, with Computer & Electronic Products again standing out. ISM estimates that 85 percent of manufacturing GDP contracted during the month, up sharply from November. Growth remains concentrated in capital-intensive and policy-supported segments, consistent with our expectation that 2026 expansion will be uneven and selective rather than broad-based. There has been some progress made in reshoring efforts, particularly with new and expanded facilities for steel, tech hardware, household appliances, and pharmaceuticals.

For policymakers, December’s ISM report supports a message of patience. Manufacturing is not generating renewed inflation pressure, nor is it weak enough to force urgent easing. The path likely remains unchanged, although the pace may slow a bit unless the labor market shows more dramatic signs of weakening. The data reinforce a backdrop in which policy clarity, particularly around trade, may matter as much as interest rates in unlocking a manufacturing comeback. The report also fits squarely within our broader 2026 framework: lean inventories, cautious managers, resilient execution, and a restocking cycle waiting on confidence and clarity on tariffs.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 5, 2026

Mark Vitner, Chief Economist

(704) 458-4000