While Production is Holding Up, Manufacturing Is Clearly Losing Steam

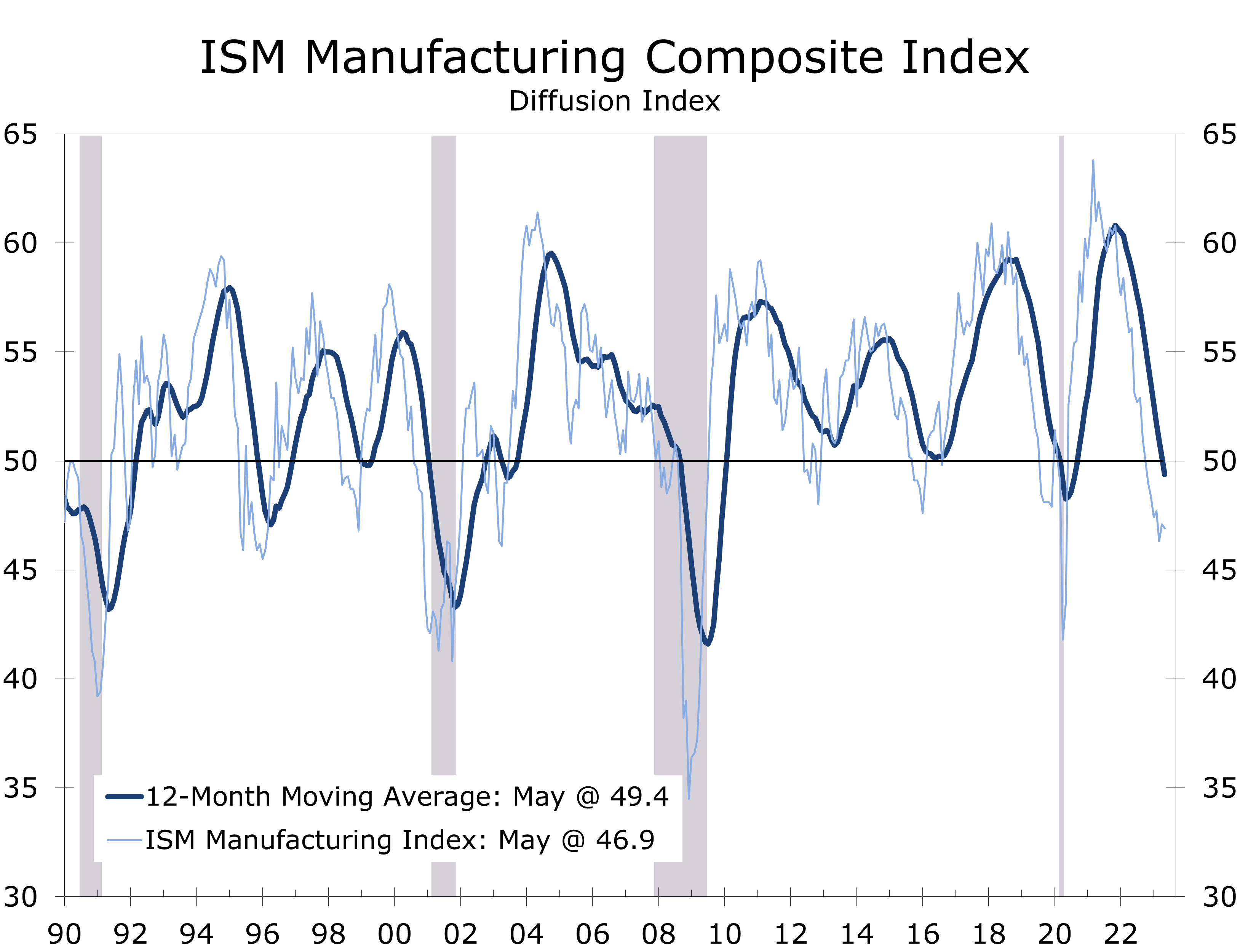

- The ISM Manufacturing Index fell 0.2 points to 46.9 in May, marking its sixth consecutive month in contraction territory.

- Production and employment – the Index’s most current components – both rose in May and are consistent with gains in industrial production and employment.

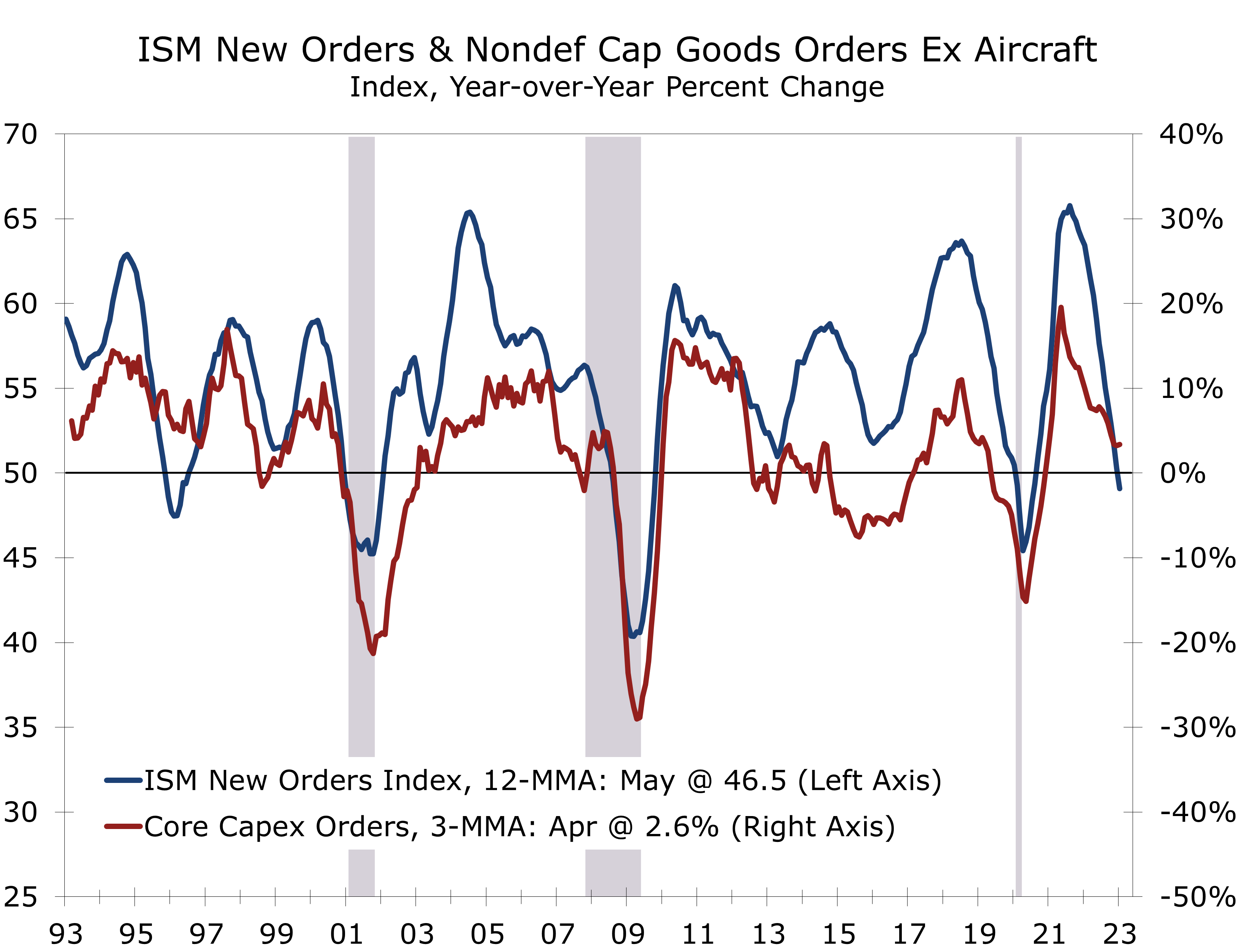

- New orders – the most leading component – fell 3.1 points to 42.6. The order backlog series tumbled 5.6 points to 37.6 and is consistent with production cuts and manufacturing layoffs later this year.

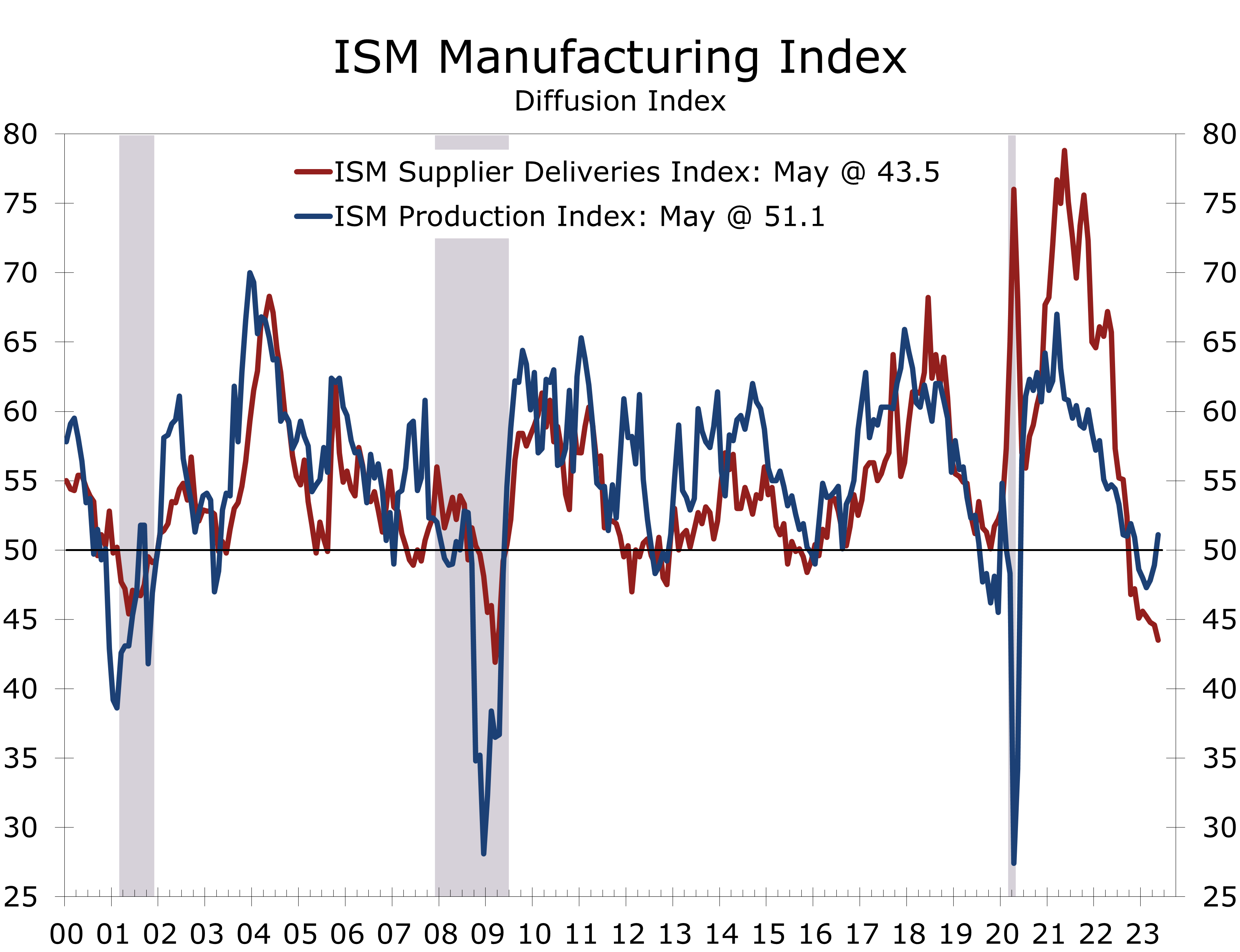

- Supplier deliveries fell 1.1 points to 43.5, with fewer firms reporting shortages.

- The prices paid index plunged 9 points to 44.2 in May, more than reversing the prior month’s increase and falling to its lowest level this year.

- Bottom line: Normalizing supply chains and diminishing labor shortages are providing a short-term boost to manufacturing but conditions will likely weaken later this year.

The Institute for Supply Management (ISM) noted manufacturing conditions continued to weaken in May. The ISM Manufacturing Index fell 0.2 points to 46.9 and has now remained below the key 50-break even level for the past six months. The details of the report are mixed. The more current components rose in May and remain in positive territory, while the more leading components fell sharply and hit levels that in the past have presaged a pullback in manufacturing activity or outright recession.

Early in his tenure, former Fed Chair Alan Greenspan noted the ISM manufacturing survey was one of the key pieces of data he reviewed closely each month to determine the health of the economy. While manufacturing represents a smaller share of the overall economy today, it still accounts for the bulk of cyclical swings in economic activity and is one of the earliest and most reliable reports released each month. The data are generated by a private trade association and are rarely revised in a significant way.

The 12-month average of the ISM has fallen below 50, consistent with a pause in rate hikes.

The ISM index provides insight into the direction and breadth of manufacturing activity. Generally, the broader a trend is, the more certain and enduring that trend will be. The 12-month moving average of the ISM index has now fallen below 50, something that has typically only occurred at the onset of a recession or soft landing. Moreover, in all prior instances, this event has also marked the end of Fed rate hikes.

The rebound from the pandemic has made interpreting the ISM report and most other economic data more difficult. The supplier delivery index surged as the economy reopened and vastly overstated the strength of the manufacturing sector, as longer delivery times are usually a sign that manufacturers are so busy, they take longer to respond to new orders. Following pandemic, however, epic supply shortages meant many manufacturers could not get the inputs needed to make their products.

Supply chains have normalized considerably over the past year, which has caused the supplier delivery index to plummet from its unusually high levels. Most manufacturers report delivery times have normalized, yet few have said they are unusually short. This may indicate normalizing supply chains are overstating the weakness in the overall ISM index.

One way you can easily see this is with the notable split between supplier deliveries and production. With inputs more readily available, production has increased. Transportation equipment is a notable example. Shortages of microchips slowed motor vehicle assemblies for months after the economy reopened. Production has ramped up more recently as shortages have subsided. The ISM noted that of the six biggest manufacturing industries, transportation equipment was the only one that grew in May.

Labor shortages have also eased a bit, enabling more hiring. The ISM employment index rose 1.2 points in May to 51.4. Among the largest industries, producers of transportation equipment and machinery both reported employment gains.

While overall production and employment likely expanded in May, the more leading components of the ISM are clearly pointing to a slowdown. The new orders index fell 3.1 points in May to 42.6 and none of the six largest industries reported a rise in orders. The recent slide in the ISM orders index suggests capital spending will be a drag on growth later this year. Moreover, unfilled orders tumbled 5.6 points to 37.5, a level that in the past has presaged a recession or significant slowdown in manufacturing activity and resulted in meaningful job losses.

The recent slide in ISM orders suggests capex will be a drag on growth later this year.

Cooling economic growth in the US and around the world has helped normalize supply chains and reduce input prices. The ISM prices index plummeted 9 points in May to 44.2, which is another piece of supporting evidence for a pause in rate hikes in June.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.