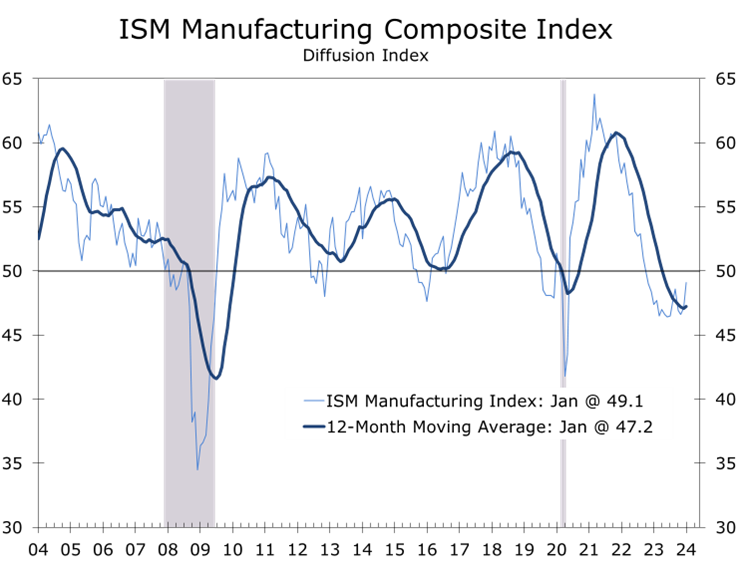

A Few Green Shoots in the Factory Sector

- The ISM Manufacturing Index rose 2 points to 49.1 in January, exceeding expectations.

- Most regional manufacturing surveys had posted declines in January, including notably sharp declines in surveys by the New York and Dallas Federal Reserve Banks.

- New orders, which are the most leading component of the ISM survey, surged 5.5 points to 52.5.

- Production, which rose 0.5 points to 50.4, also returned above the break-even level.

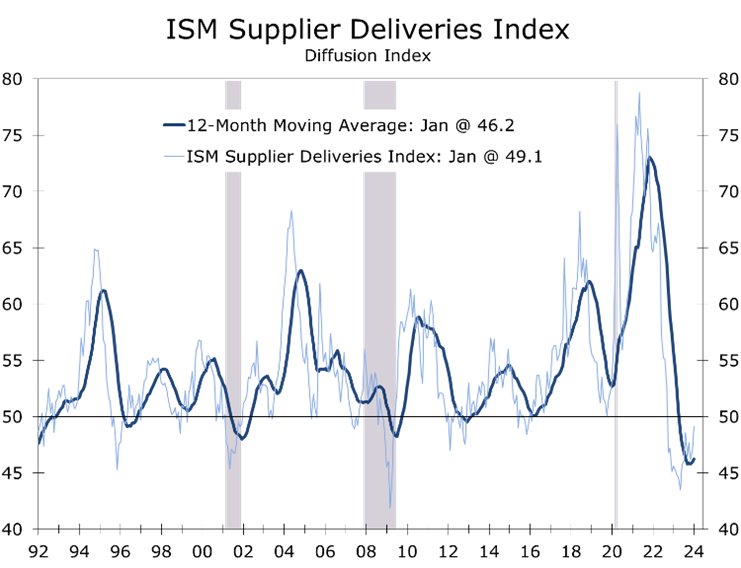

- The supplier deliveries index increased by 2.1 points to 49.1, indicating slower deliveries. While it is likely too soon to see effects from disruptions in the Red Sea, ongoing delays at the Panama Canal may be impacting delivery times.

- The prices-paid index soared 7.7 points to 52.9, likely indicating an end to the easing of raw material prices.

- January’s ISM report exceeded expectations, which had been weighed down by a series of weak regional manufacturing reports. While encouraging, the improvement in the ISM appears to be narrowly based. Manufacturers remain concerned about weak demand for goods and sluggish growth overseas.

The ISM Manufacturing Purchasing Managers’ Index (PMI) exceeded expectations in January, rising 2 points to 49.1, its highest level since October 2022. This follows declines in several regional manufacturing indexes earlier in the month. Despite remaining below the crucial 50-point threshold for the 15th consecutive month, there are signs of improvement, notably a 5.5-point increase in new orders and a 0.5-point rise in production.

The New Orders Index rose to 52.5, marking only the second time it has surpassed 50 in the last 20 months. Three major industrial sectors—Chemical Products, Transportation Equipment, and Fabricated Metals—saw increased orders. This improvement is attributed to strong demand for appetite suppressant medications, recovery from the UAW strike, and growth in industrial construction.

The long slide in manufacturing activity may be ending but a recovery remains uncertain.

The narrow improvement in new orders leaves the timing and extent of recovery uncertain. Only 20.2% of manufacturers noted a rise in new orders, while 23.5% saw a decline. Moreover, exceptionally low customer inventories suggest lower interest rates and less geopolitical uncertainty might quickly lift new orders.

Supplier deliveries rose by 2.1 points to 49.1, reflecting a lengthening in shipping times. Supplier delivery times have been normalizing for some time, even for highly sought after products such as semiconductors. The lead time for production materials increased by 1 day this past month, reaching an average of 83 days. This is still well above 66 days averaged in the year prior to the pandemic but well below the peak of 100 days last reached in July 2022.

Following the wide swings surrounding the pandemic, supply chains are now normalizing.

We believe it is too early to see any impact from delays emanating from attacks on shipping in the Red Sea and the resulting rerouting of traffic. Moreover, the impact from those delays is likely to be greater in Europe than in the U.S.

The Red Sea is not the only trouble spot. Delays in the Panama Canal due to low water levels have been a long running problem that looks likely to persist. Once onshore, however, goods are moving swiftly, with trucking, rail, air, and warehouses all operating with well within historic capacity norms.

With supply chains normalizing, fewer products are in short supply. Long-running shortages of electrical components and electronic components continue. In addition, steel alloy remains in short supply.

The ISM Employment index fell 0.4 points to 47.1, marking the for consecutive month the index has been below 50. Transportation equipment was the only large manufacturing sector where payrolls rose in January. One an overall basis 11% of manufacturers said they added to payrolls, down from 11.7% the prior month. The share of manufacturers reducing payrolls rose 0.4 points to 18.4%.

The moderation in raw materials prices appears to have largely run its course.

The ISM Prices-Paid Index surged 7.7 points to 52.9 in January, ending an 8-month run below 50. Key raw material prices have normalized due to lower energy costs, better supplies, and reduced shipping rates. However, recent energy price increases and higher global shipping rates, triggered by attacks on Red Sea shipping, suggest prices will like firm further.

While January’s ISM data are mixed, they generally support of the Fed’s intention to hold rates steady through late spring or early summer. At 49.1, the ISM index is consistent with 1.9% real GDP growth, which is close to consensus but well below the early projections from the Atlanta Fed’s GDPNow, which are at 4.2%.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.