Another Pivotal Week for the Economy

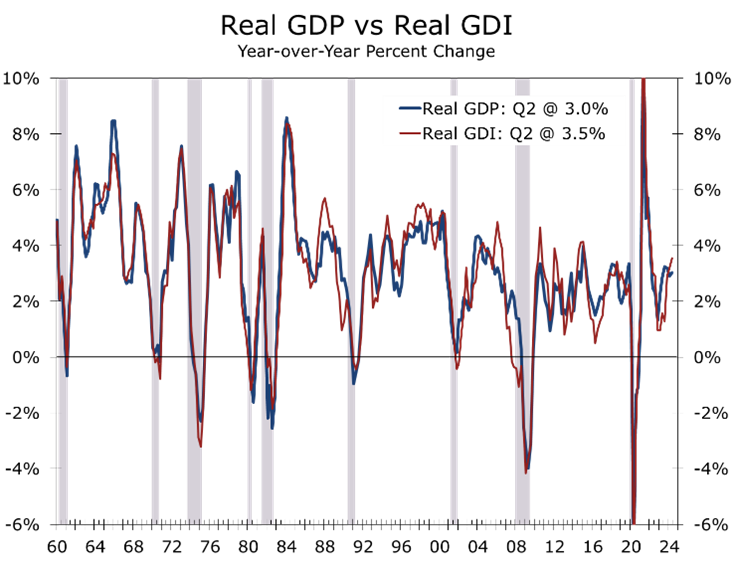

- Revisions to Q2 real GDP left growth unchanged at 3.0%. The composition is slightly weaker, with downward revisions in consumption and capital expenditures offset by higher government spending and increased business inventories.

- 2023H1 growth was stronger, while growth in the second half was revised lower.

- Gross Domestic Income (GDI) growth was revised up sharply, narrowing the statistical discrepancy with GDP.

- The saving rate for Q2 and earlier was revised higher, suggesting consumers have a little more spending capacity.

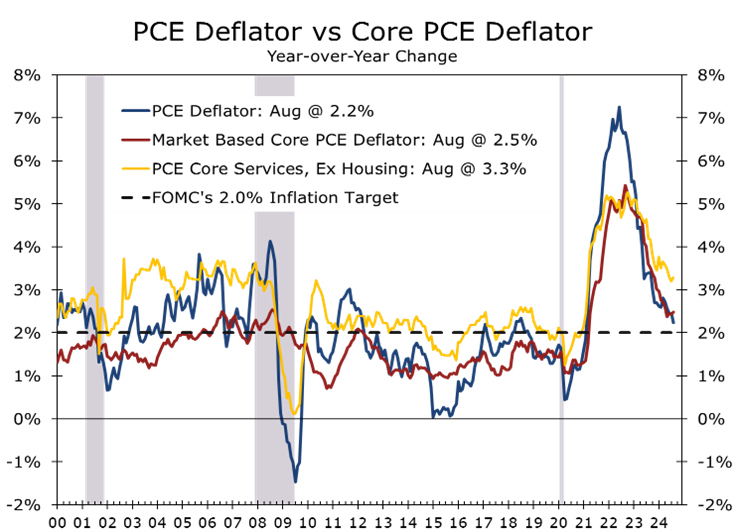

- Core PCE inflation rose 0.1% in August, with the year-over-year rise moderating to 2.7%.

- Economic data looks surprisingly benign, while inflation is moderating slightly more than expected. This gives the Fed room to lower rates further, but likely at a slower and more cautious pace. Geopolitical risks remain high, with Israel intensifying its response to Hezbollah’s attacks.

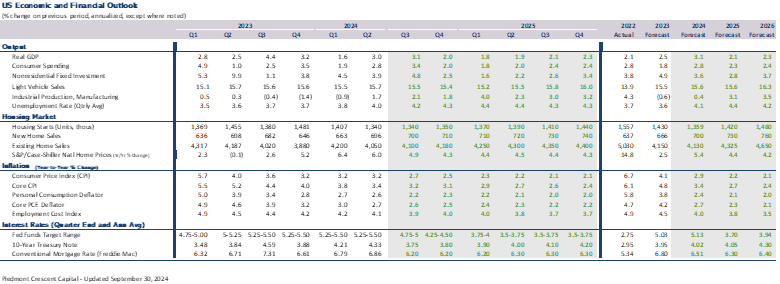

This past week featured a full calendar of economic releases, led by the third revision of second-quarter GDP growth. Overall growth remained unchanged from the previous estimate, with real GDP rising at a 3.0% annual rate in Q2. However, the composition of growth was slightly softer, with downward revisions to consumer spending, business investment, housing, and net exports. These declines were offset by upward revisions to government spending and business inventories. Real GDP growth for the first quarter was revised slightly higher, bringing the growth rate for the first half of the year to 2.4%, up from the previously reported 2.2%.

Although the second quarter now feels distant, this report included revisions dating back to 2019, revealing several surprises. The revisions show the economy is slightly stronger. Real Gross Domestic Income (GDI) growth for Q2 was revised up by 2.1 percentage points to 3.4%, narrowing the previously wide gap between GDP and GDI. GDI growth was also revised higher over the past few years, reflecting stronger corporate profits and net interest payments. These changes resulted in a 1.3 percentage point upward revision for 2023, with smaller adjustments for 2022 and 2021, moving the year-over-year GDI from 1.1 points below GDP to half a point above it.

With more income growth, the personal saving rate for Q2 was revised up by 1.9 percentage points to 5.2%. This improvement was driven by stronger employee compensation in late 2023 and early 2024, helping to explain the resilience of consumer spending this year despite slower job growth.

While earlier income data were revised higher, the most recent figures came in soft. Personal income rose just 0.2% in August, slightly below expectations, as solid gains in employee compensation (+0.5%), rental income (+0.7%), and transfers (+0.1%) were offset by declines in proprietors’ income (-0.2%) and interest and dividends (-0.5%). Consumer spending edged up 0.2%, driven primarily by a 0.2% increase in services spending, while real goods spending remained flat.

Wages and salaries are growing steadily, which should support holiday season spending.

The saving rate edged down to 4.8% from an upwardly revised 4.9% in July, reflecting recent national accounts revisions. A month ago, consumers appeared strapped, with the saving rate reported at just 2.9%.

Inflation continues to moderate gradually. The core PCE price index rose 0.1% in August, bringing the year-over-year change to 2.7%. Core services, excluding housing, increased 0.16% in August and are up 3.3% year-over-year. The market-based core PCE deflator rose 0.15% and is up 2.5% year-over-year. All measures seem to be on a path toward the Fed’s 2% target.

Despite a slight slowdown in August personal consumption, we have raised our Q3 GDP forecast to an annual rate of 3.1%. Advanced indicators point to a narrowing goods trade deficit and solid growth in core durable goods orders.

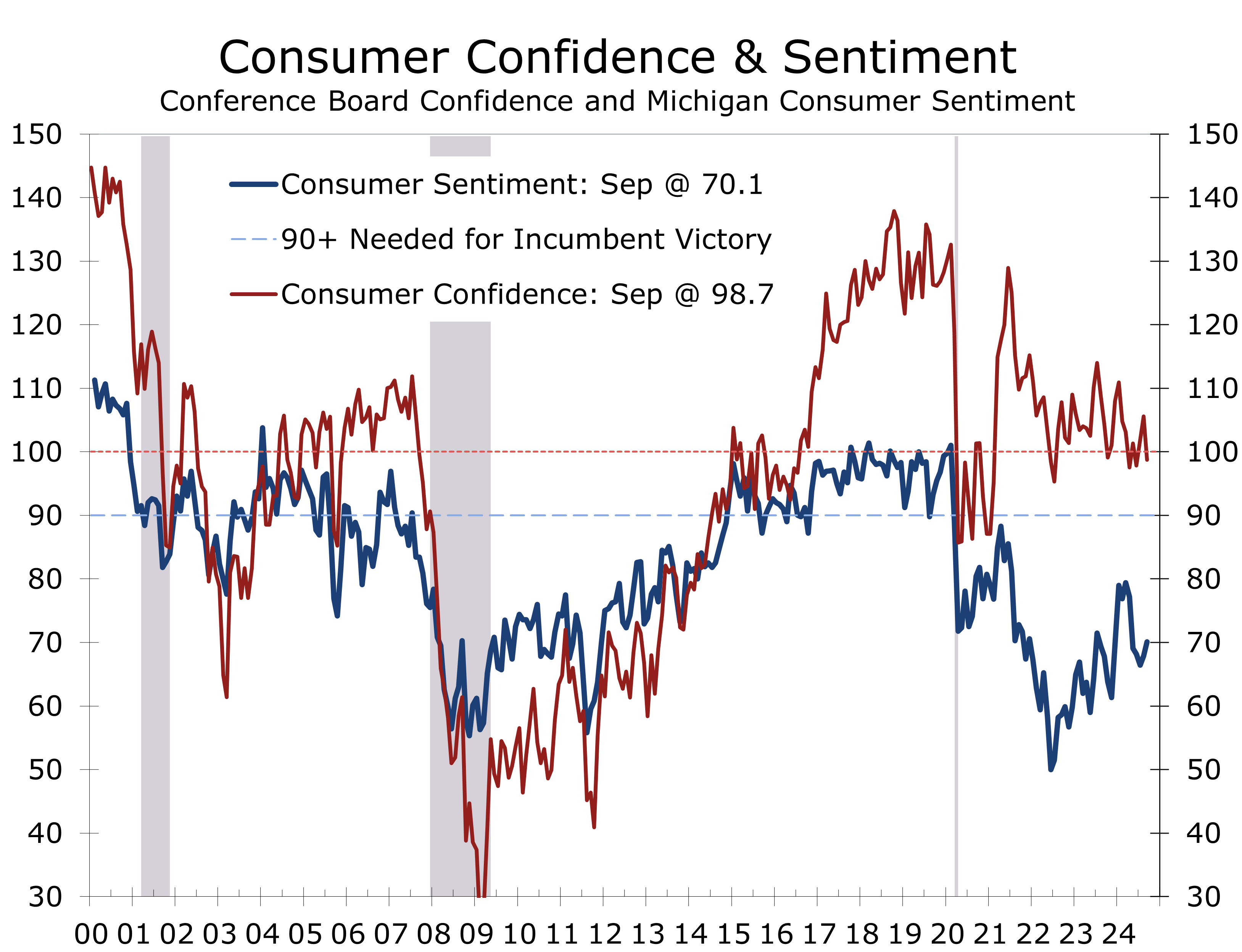

Despite upward revisions to GDP and earlier income growth, consumers remain uneasy about the economy. The Conference Board’s consumer confidence index fell by 6.9 points to 98.7 in September, below expectations. This drop was slightly offset by an upward revision to August’s data, which raised that month’s reading to 105.6. Both components of the index declined in September, with the expectations index down 4.6 points to 81.7, and the present situation index falling more sharply by 10.3 points to 124.3.

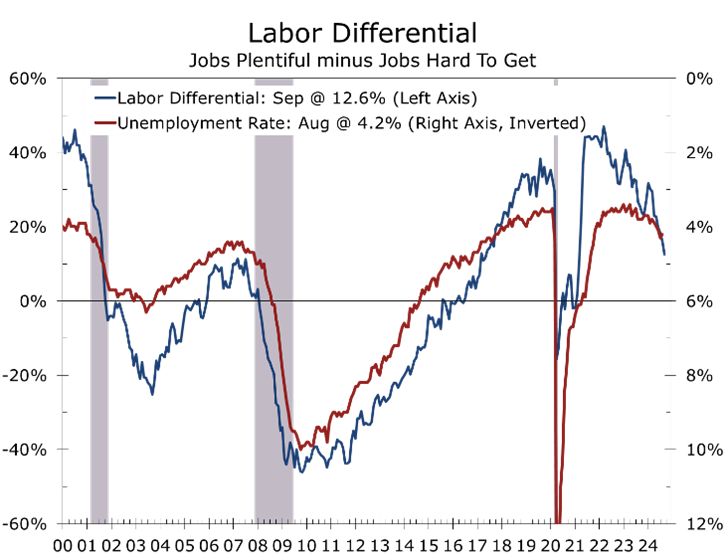

The labor market differential—the gap between respondents reporting jobs as plentiful and those saying jobs are hard to get—also weakened, falling 3.3 points to 12.6. This marks a significant drop from earlier in the year, sitting about 18 points lower than in Q1 2024 and well below the 2019 average of 33.2. The labor market appears to be correcting remarkably close to what monetary theory suggests, with job growth beginning to slow one year after the Fed started raising the federal funds rate, and the bulk of the impact from higher rates weighing on job growth 18 months after the first hike.

Consumer perceptions of the likelihood of a U.S. recession in the next 12 months rose 0.5 percentage points to 66.5%. The survey was completed by September 17, just before the Fed initiated its easing cycle with a larger-than-expected rate cut.

The half-point rate cut might help boost future sentiment. Despite declining confidence and labor market concerns, the outlook for consumer spending remains strong, supported by low jobless claims and healthy household finances. However, a clear divide persists between income groups: upper-income households benefit from a strong stock market, while middle- and lower-income households face rising costs for housing, groceries, and transportation.

The University of Michigan’s Consumer Sentiment Index showed slight improvement, rising 1.4 points to 67.8 in August, the first increase since March. Current economic conditions fell 1.8 points to 60.9, while the consumer expectations component rose 3.3 points to 72.1, likely influenced by the Fed’s larger-than-expected September rate cut, which came too late to affect the Conference Board’s data. From a political perspective, Consumer Sentiment remains well below the level typically needed for the incumbent party candidate to return to the White House.

Inflation expectations in the Michigan survey remained steady, with a 2.9% projected rise in prices over the next year, and long-term expectations for the next 5-10 years holding at 3.0%. This is still slightly elevated compared to historical norms and reflects the higher cumulative price increases, which continue to weigh on overall sentiment.

The other major story this past week was Hurricane Helene, which made landfall in Florida’s Big Bend region before rapidly moving north, dumping heavy rainfall across Georgia and North Carolina’s mountains. Early reports indicate over 100 lives lost, with monetary damages expected to exceed $150 billion. A significant portion of the damage is due to flooding, with many losses likely uninsured, which will slow the rebuilding process and dampen local economic activity in the coming months.

The geopolitical landscape remains volatile but shows signs of progress. Israel has swiftly neutralized threats on its northern border, utilizing superior intelligence and technology against what appeared to be a larger, more formidable force. Israel understands that decisive victories are essential to maintaining credibility in the Middle East. The swift dismantling of Hezbollah’s leadership sends a strong message to both Iran’s government and its opposition. Israel is expected to continue its efforts for a decisive victory over Hezbollah and the Houthis, particularly ahead of the U.S. elections. This could pave the way for broader peace agreements with Saudi Arabia and other Arab nations.

This coming week will feature several key reports, with ISM and employment data shaping market expectations for the Fed’s next move. We anticipate payrolls to increase by 150,000 in September, with a slight upward revision to the August figures. The Fed is likely targeting quarter-point rate cuts at both the November and December FOMC meetings. Powell noted that revisions to Gross Domestic Income and a higher saving rate have reduced some downside risks to the economy. We’ve raised our Q3 GDP forecast to 3.1%, though we still expect growth to slow toward its long-term potential. We’ve also adjusted our forecast for total rate cuts in this easing cycle to 175 basis points, 50 of which have already occurred.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 30, 2024

Mark Vitner, Chief Economist

Piedmont Crescent Capital

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000