Key Takeaways: Construction Spending July 2025

-

- Headline softness: Total construction spending fell 0.1% in July to $2.139T SAAR, the third straight monthly decline. Outlays are -2.8% y/y and -2.2% YTD. Adjusted for input cost inflation, real activity is slipping faster than the headline suggests.

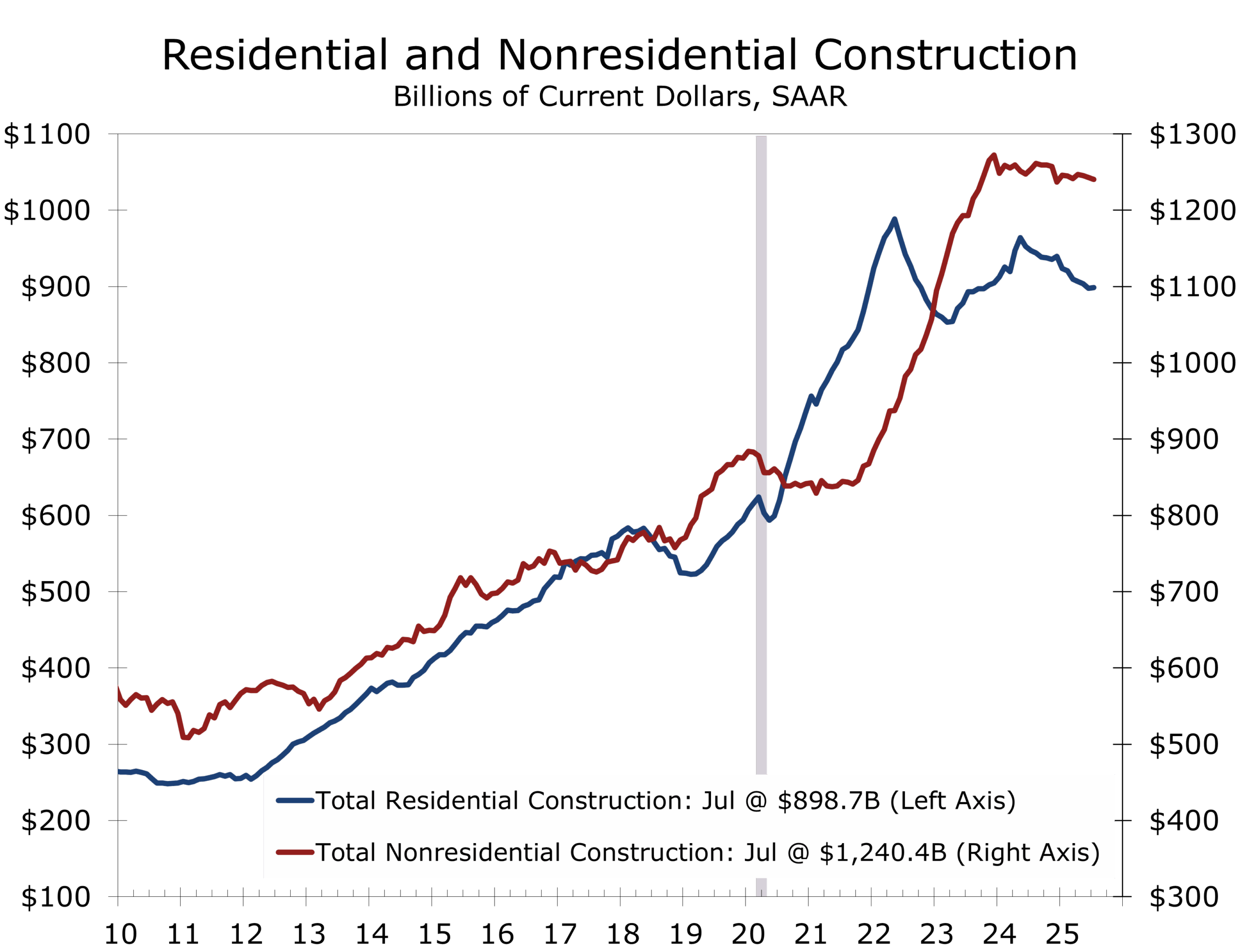

- Residential stabilization short-lived: Private residential rose 0.1% as single-family eked out a small gain while multifamily fell. A solid pipeline provides near-term support, but affordability pressures and weak builder sentiment (NAHB HMI 32 in August) point to renewed softness in Q3.

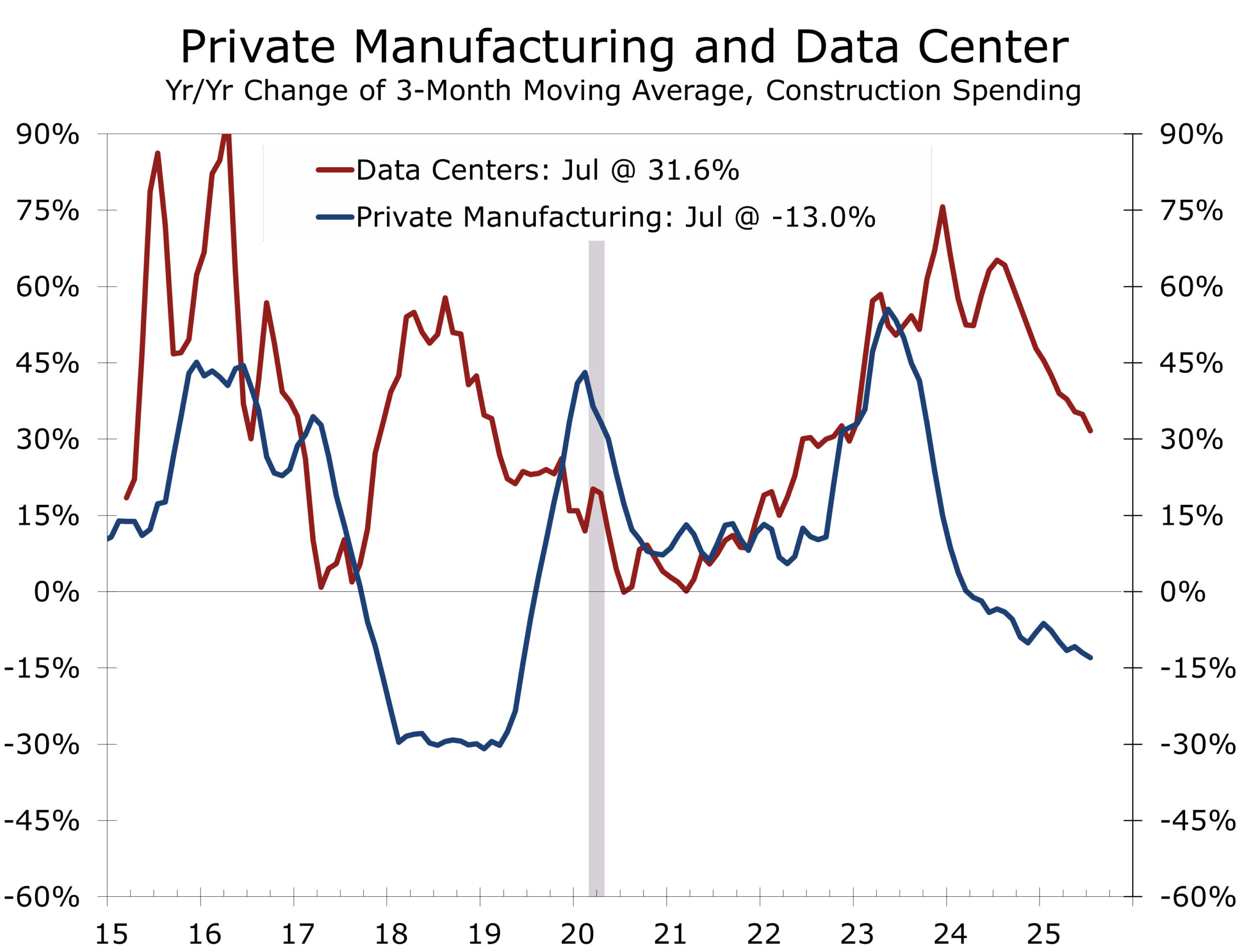

- Nonresidential drag: Private nonresidential fell 0.5%, with manufacturing (-0.7%) and commercial (-0.9%) leading the pullback. Fiscal tailwinds from CHIPS/IRA projects are fading, data center growth is slowing, and oil/gas exploration is weakening as rig counts fall with lower prices.

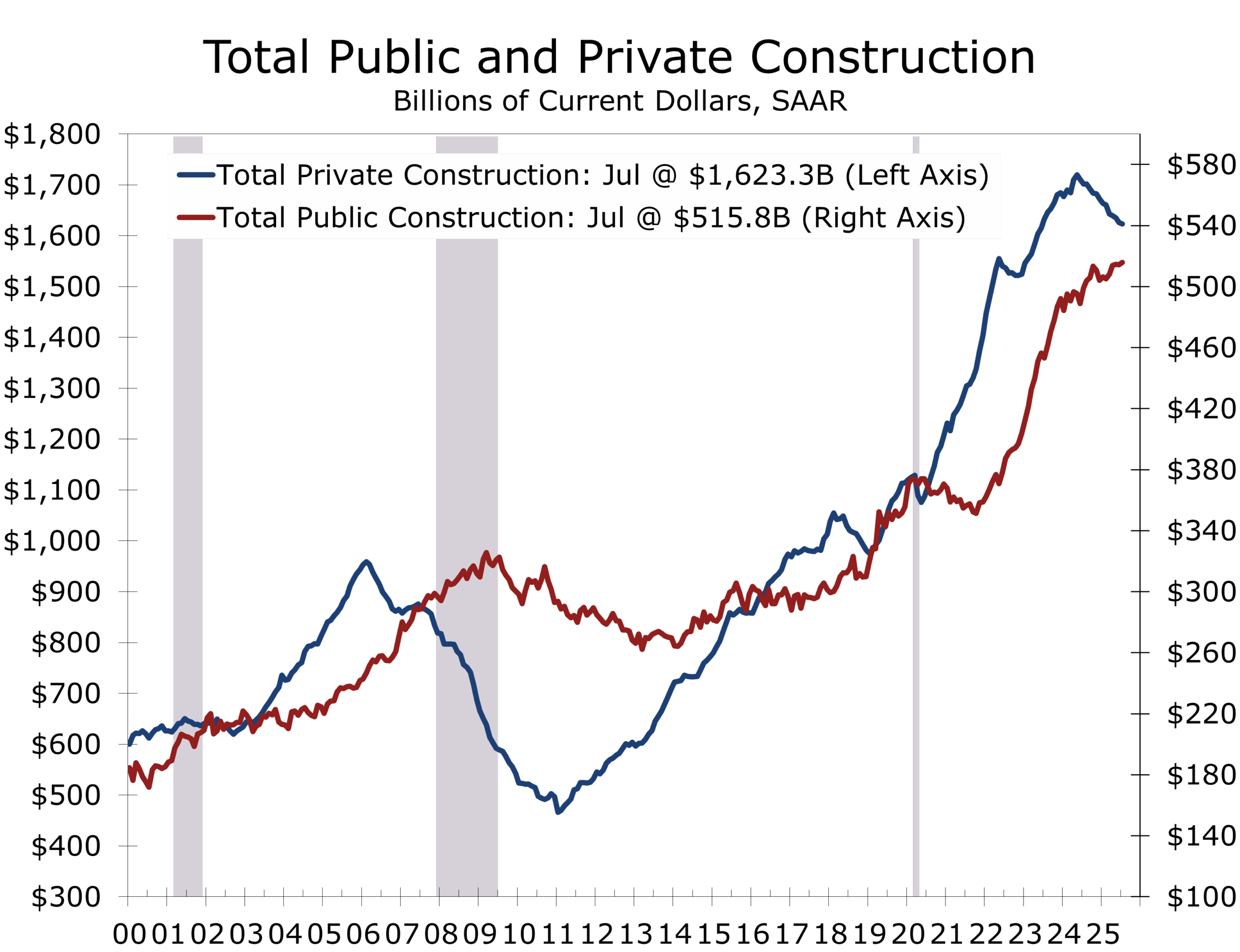

- Public support continues: Public outlays rose 0.3% in July, with transportation, water, and sewage projects benefiting from infrastructure funding. The sector is now +3.4% y/y, making it the most reliable area of support.

Housing Finds a Floor, Nonresidential Still Sinking

Construction spending edged lower in July, slipping 0.1% to a $2.139 trillion annual pace. That marks the third consecutive monthly decline and leaves outlays nearly 3% below last year’s levels. Once adjusted for higher input costs—up roughly half a percent on the month—the decline in real activity is even more pronounced, reinforcing the sector’s role as one of the economy’s weakest points heading into the second half of 2025.

Residential spending rose 0.1% in July, breaking a four-month losing streak.

The modest decline hides stark differences across categories. Residential spending ticked up 0.1% in July, breaking a four-month losing streak. Single-family construction posted a narrow gain while multifamily continued to contract. Yet the underlying fundamentals remain challenging. Home sales are subdued, price declines are spreading across more markets, and retail sales of building materials remain weak. The NAHB/Wells Fargo Housing Market Index slipped to 32 in August, with buyer traffic near cycle lows. While a strong pipeline of homes under construction will cushion activity in the near term, the broader outlook points to renewed weakness until mortgage rates ease meaningfully.

The heavier weight on the topline came from private nonresidential spending, which fell 0.5% in July. Manufacturing outlays dropped 0.7%, down nearly 7% from a year ago, as the wave of megaprojects tied to CHIPS and IRA incentives begins to crest. Commercial construction fell 0.9% in the month and is down nearly 10% year-over-year, with retail and warehouse categories struggling. Even data centers, which have been the most consistent growth engine, advanced at their slowest pace in months. Energy-related structures are also softening, with oil and gas drilling cutbacks reflecting profitability challenges at current crude prices.

Private nonresidential spending fell 0.5% in July as manufacturing and commercial weakened.

Public spending continues to serve as the sector’s stabilizer. Outlays advanced 0.3% in July, with gains concentrated in transportation, water, and sewage projects. Year-to-year, public construction is up more than 3%, supported by federal infrastructure dollars and relatively strong state and local balance sheets. While monthly figures remain volatile, the overall trajectory of public construction remains positive.

While current activity is contracting, forward-looking measures suggest the project pipeline is a bit healthier. The Architecture Billings Index slipped to 46.2 in July, consistent with near-term weakness in design activity, but the Associated Builders and Contractors backlog indicator climbed to 8.8 months, its highest since 2019. At the same time, the Dodge Momentum Index surged more than 20% in July to a record high, boosted by institutional and commercial planning—including another major Meta data center and multiple hospital projects. These indicators point to a late-2025 and 2026 rebound in construction activity.

For the broader economy, construction remains a modest but visible drag. The slowdown in nonresidential construction will likely pull structures investment down at around a 7% annualized pace in Q3, following an 8.9% decline in Q2. The combination of fading fiscal tailwinds, elevated financing costs, and policy uncertainty continues to weigh on private construction, while public infrastructure provides only a partial cushion. The message for contractors, developers, homebuilders, and construction supply firms is clear: the near-term environment will remain challenging, but the project pipeline suggests better opportunities ahead once financial conditions ease and long-duration projects in digital infrastructure and institutional construction ramp up.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 2, 2025

Mark Vitner, Chief Economist

(704) 458-4000