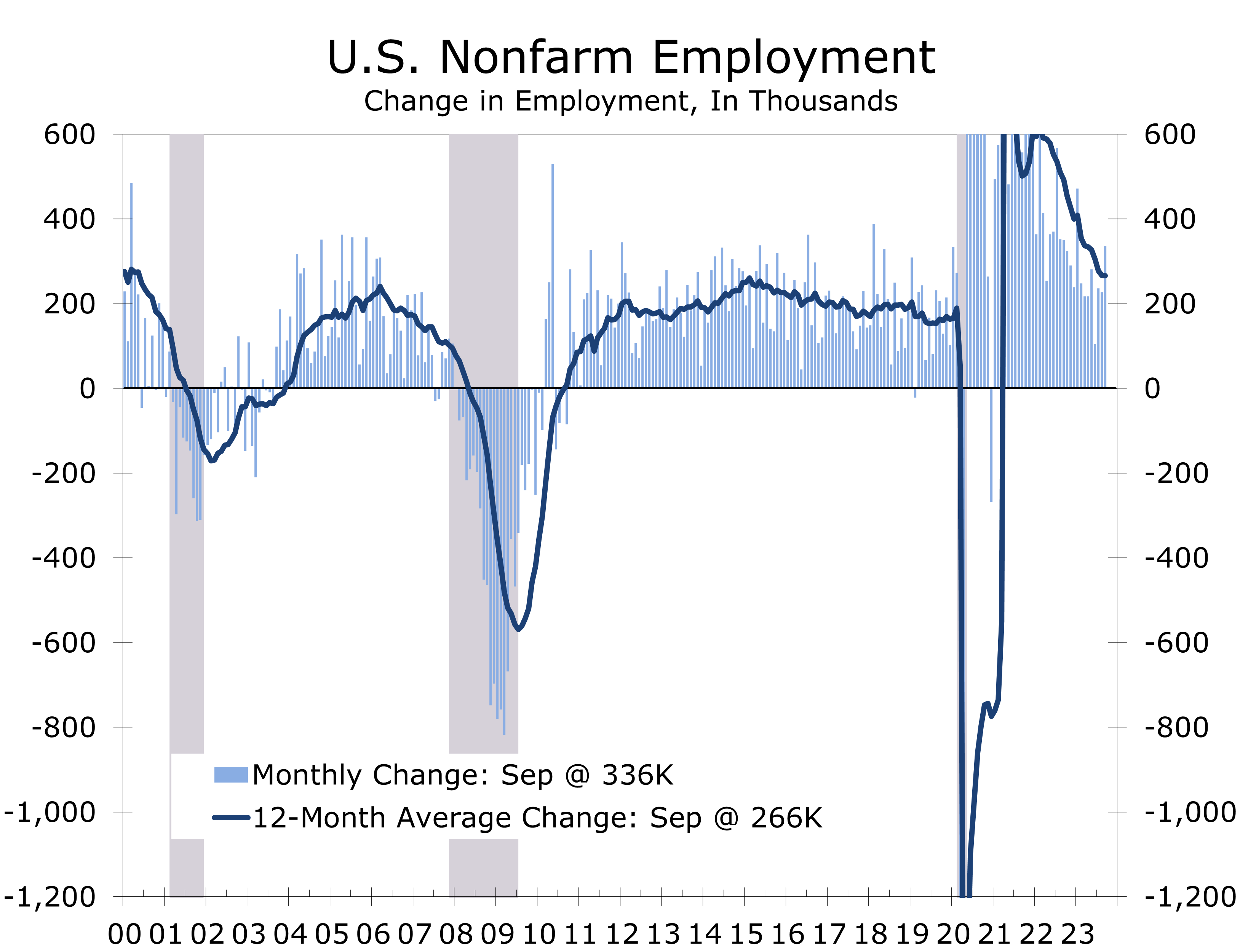

Hiring Surged in September

- Employers added 336,000 jobs in September, roughly twice the consensus estimate.

- The unemployment rate was unchanged at 3.8%, as the labor force and employed persons rose by roughly the same amount.

- Payroll gains were broadly based and were not affected by the UAW strike.

- September payroll data are often impacted by crosscurrents including the winding down of summertime jobs and teachers and professors returning to the classroom.

- Leisure and hospitality added 96,000 jobs this past month and government added 73,000 jobs, with more than half in education.

- Health care and social assistance added 65,900 jobs, and manufacturing (+17k), construction (+11k) and mining (+1k) all posted modest gains.

- Revisions lifted job growth in the two prior months by a combined 119,000 jobs, which adds an exclamation point to September’s strong jobs report. Underlying data in the jobs report suggest industrial production rose modestly in September and point to continued strong income growth. The data are consistent with our 3.6% Q3 GDP forecast.

September’s outsized nonfarm payroll growth initially set off fears the Fed had more work to do. On closer inspection, however, the job report is not as unsettling as the headline 336,000-job gain suggests. Most of the increase, as well as the upward revision to prior data, was in industries still striving to bring payrolls back to their pre-pandemic trend.

Leisure and hospitality continues to account for a disproportionate share of job gains, with restaurants and bars adding 61,000 jobs in September. With the increase, restaurant and bar payrolls are now back at their pre-pandemic level. Restaurants are still understaffed, however, with industry payrolls roughly 450,000 jobs below their pre-pandemic trend. Hotels added back 16,000 jobs in September, but payrolls remain 217,000 jobs, or 10.3%, below their pre-pandemic level.

Job growth continues to be driven by industries striving to regain their pre-pandemic trend.

Health care added 40,900 jobs in September, which is well under the average gain of 53,000 jobs added over the past year. Despite adding 625,800 jobs over the past year, health care remains chronically understaffed. While overall employment in health services is now 525,000 jobs above its pre-pandemic level, we estimate health care providers are still understaffed by at least 400,000 workers based on the pre-pandemic hiring pace.

Social services and state and local government are two other areas struggling to bring payrolls back to their pre-pandemic trend. Taken together, leisure and hospitality, health care and social services, and state and local governments accounted for more than two-thirds of September’s job growth. Moreover, most of the revision to the July and August data came from large upward revisions to state and local government payrolls. Private sector employment growth was revised slightly lower, and now shows gains of just 145,000 jobs in July and 177,000 jobs in August.

Large upward revisions to state and local government boosted July and August payrolls.

Private payroll growth picked up in September, with businesses adding 263,000 jobs. Hiring was broad based, with the diffusion index rising 2 points to an eight-month high 64.8 in September. As noted earlier, most of the job gain was in industries that remain chronically understaffed. But hiring rose modestly in most industries, including professional and business services (+21K), retail trade (+20K), manufacturing (+17K), construction (+11K) and mining (+1k).

Somewhat lost in the shock of September’s huge nonfarm payroll gain, the household survey was surprisingly weak. The unemployment rate was unchanged at 3.8%, as the labor force rose 90,000 and household employment rose by just 86,000.

The data look even weaker after adjusting household employment to the nonfarm payroll methodology. On this basis, household employment fell 7,000 in September. This employment measure has historically done a good job of picking up inflection points in the nonfarm employment data well before they become evident in the monthly data. The recent trend in adjusted household employment is well payrolls and is consistent with BLS data released in August that point to a sizeable downward revision to nonfarm employment when the annual revisions are reported early next year.

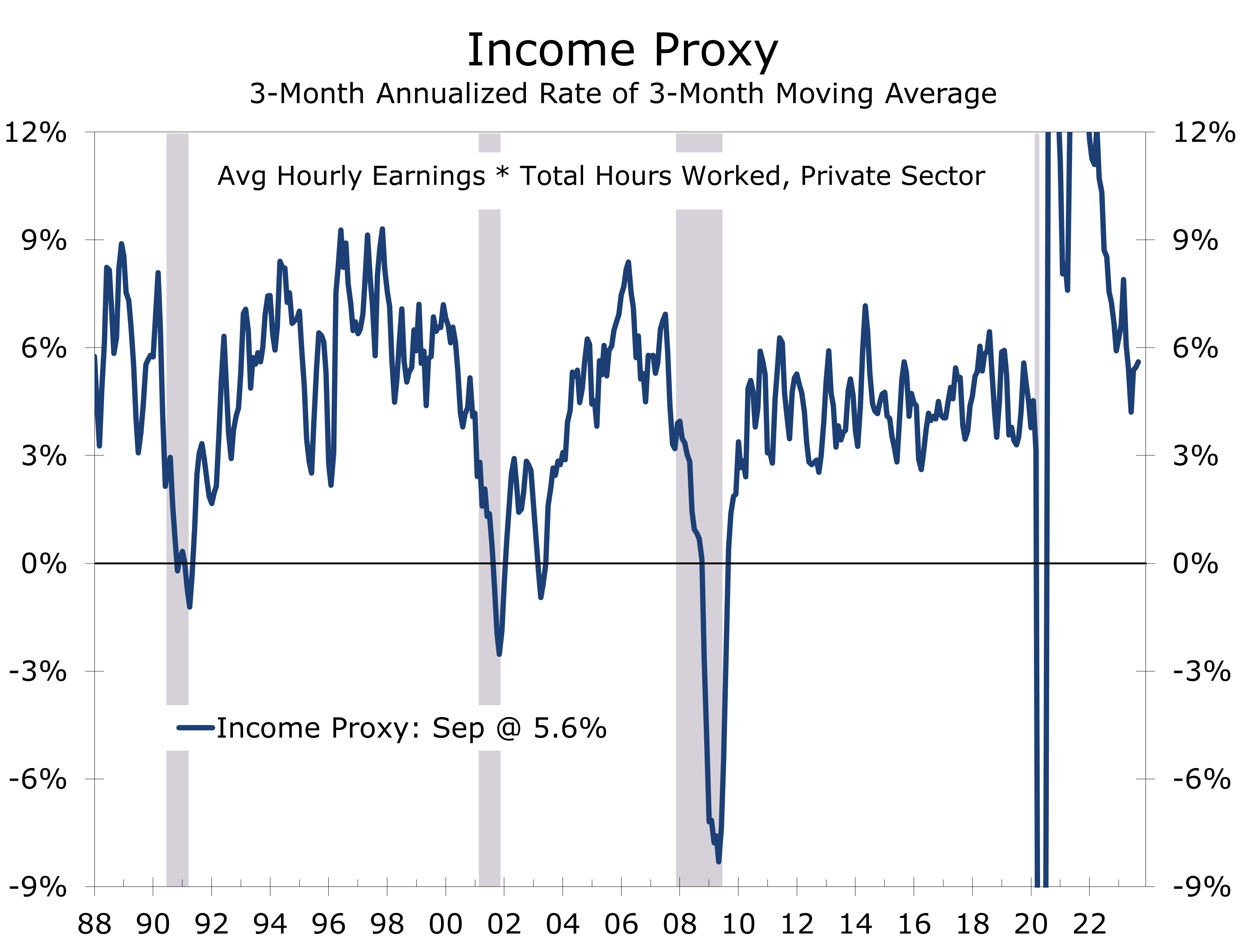

Strong job growth is bolstering incomes, which is why consumer spending is holding up so well.

While we see some potential soft spots, the economy has considerable momentum. Real GDP growth should rise at a 3.6% pace in Q3, driven by strong gains in consumer spending. Our income proxy grew at a 5.6% pace in Q3 and should rise solidly this quarter as well.

September’s stronger payroll growth should not alter the Fed’s stance on interest rates. The September CPI data will be more important and fear we may see some reacceleration in core services prices, excluding housing. While that may make the November rate decision a tough call, we expect the Fed to stand pat.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.