Hiring Has Clearly Lost Momentum

- Employers added 142,000 jobs in August, falling well below the 12-month average of 202,000. Revisions to June and July payrolls lowered job gains by a total of 86,000, emphasizing the ongoing slowdown in economic momentum.

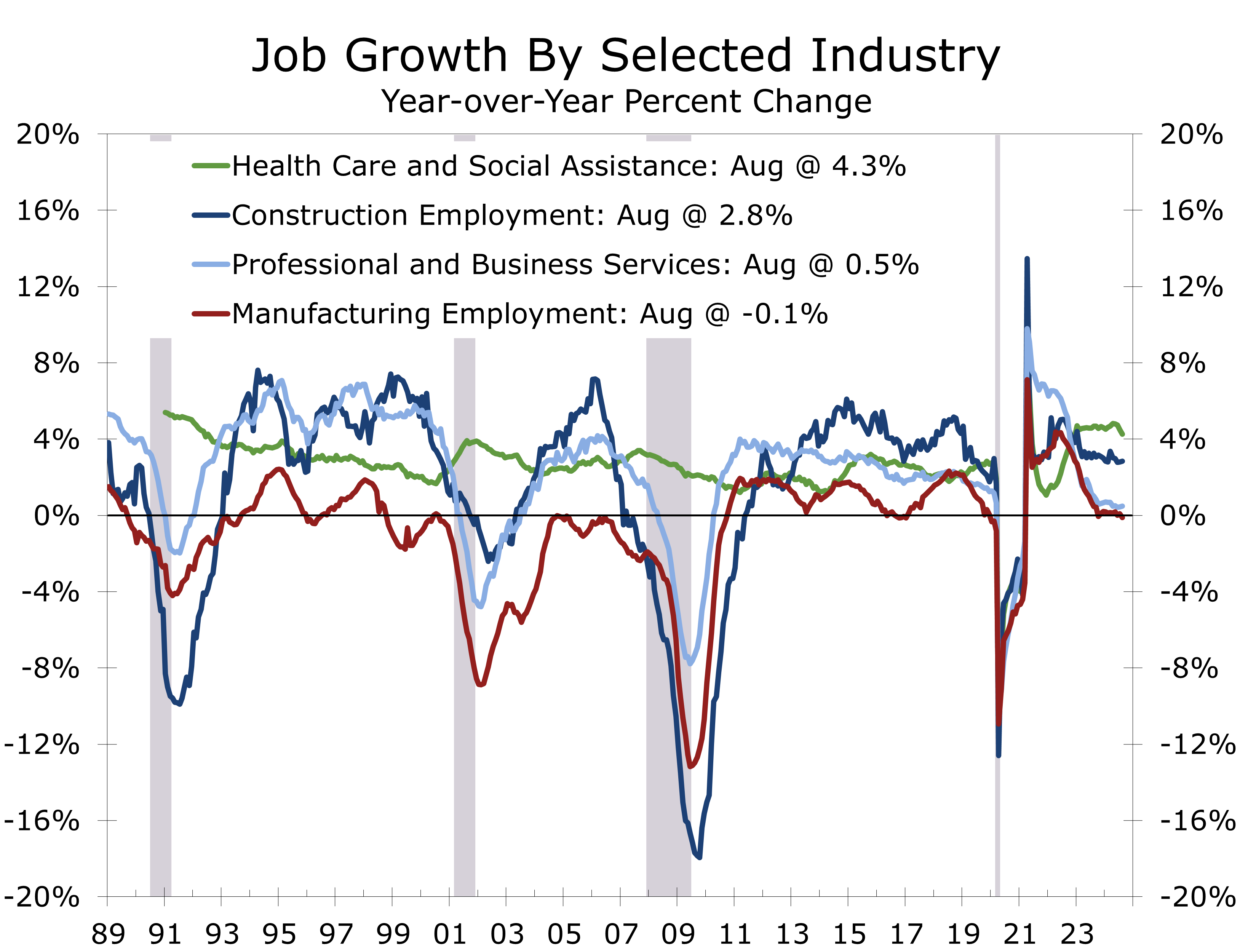

- Leisure and hospitality (+46K), health care and social assistance (+44.1K), construction (+34K) and government (+24K) continue to account for the bulk of net new jobs (80%+ of the total).

- The diffusion index improved slightly, climbing 5.4 point to 53.2. July is the only reading below 50 since the Pandemic.

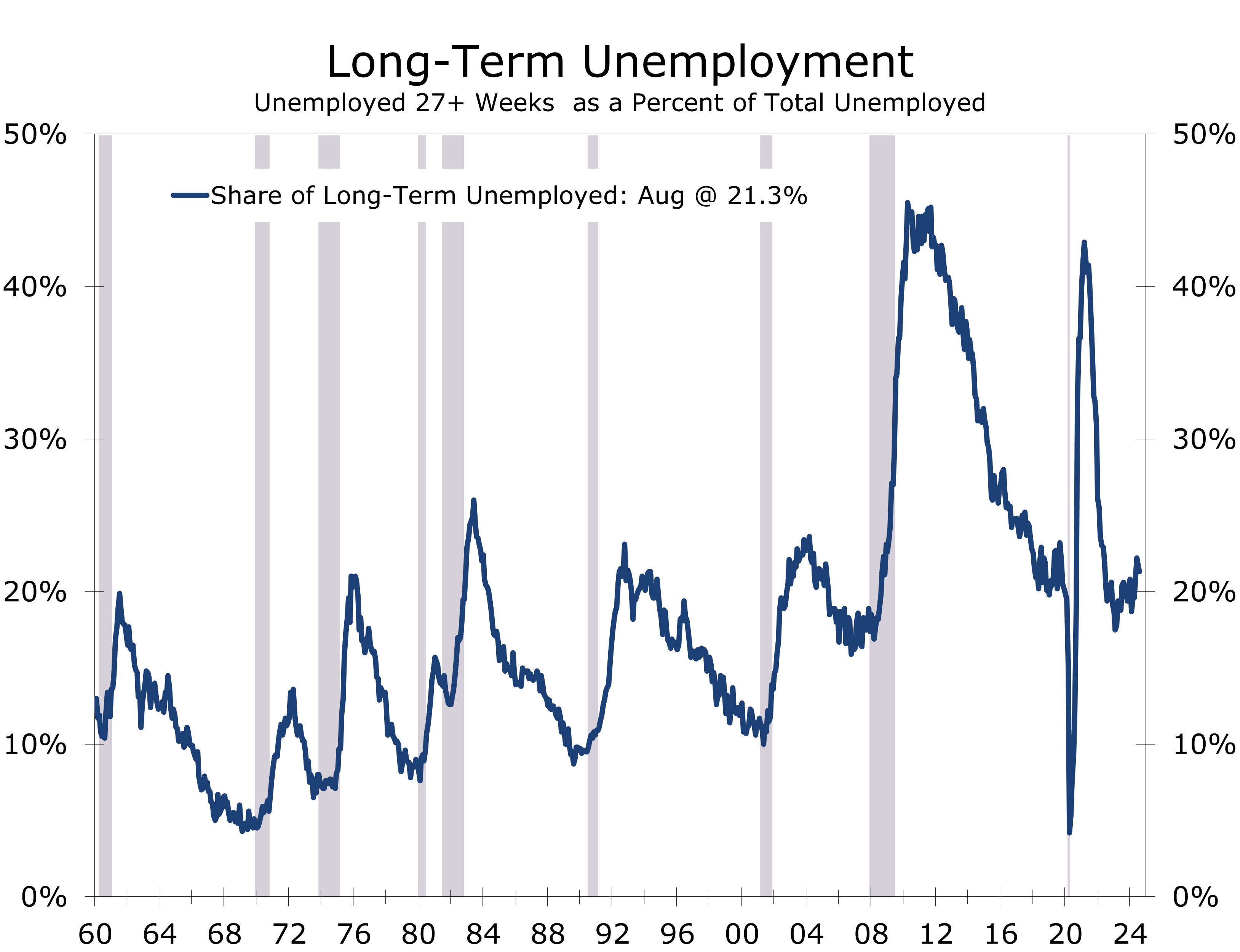

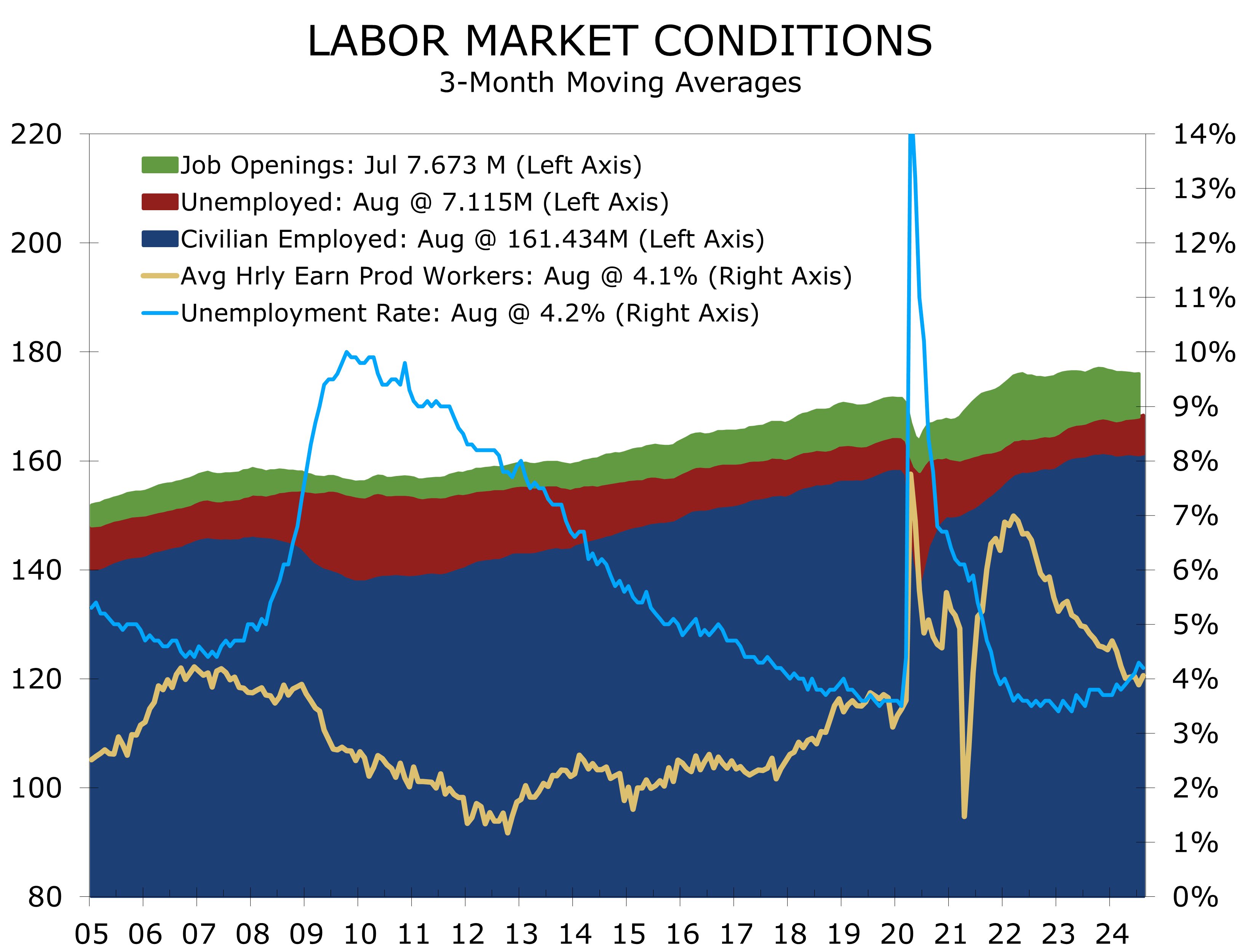

- The unemployment rate edged 0.1 percentage point lower to 4.2%. Long-term unemployment held steady at 1.5 million, making up 21.3% of total unemployment.

- The August employment report met expectations, but the composition of job gains and significant downward revisions to previous data suggest the report is weaker than it appears. Job growth continues to rely heavily on a few industries, many of which offer lower wages. Notably, hiring in professional services remains particularly weak.

Total nonfarm payroll employment increased by 142,000 in August, representing continued deceleration in job creation. This past month’s gain follows the smallest monthly gain since the Pandemic and is well below the prior 12-month average of 197,000 new jobs. Job growth was driven primarily by leisure and hospitality (+46,000), construction (+34,000), health care (+31,000), and government (+24,000). However, the broader slowdown in hiring was evident, as manufacturing lost 24,000 jobs, mainly due to a 25,000 drop at durable goods producers.

The narrowing breadth of job growth is likely pulling long-term unemployment higher.

Revisions to previous months were surprisingly large and negative, subtracting a combined 86,000 jobs from the June and July figures. The diffusion index, which measures the breadth of job gains across industries, rebounded 5.4 point August to 53.2 but the prior month’s reading was revised lower, to 47.6, marking the only month where more industries cut jobs than added them. Such declines are rare outside recessions.

The unemployment rate edged 0.1 percentage point lower to 4.2%. Despite the improvement, the jobless rate remains nearly half a percentage point higher than its year ago level. Long-term unemployment (those out of work for 27 weeks or more) remained flat at 1.5 million, representing 21.3% of all unemployed.

The number of long-term unemployed has risen over the past year, climbing from a cycle low of 1.05 million in March of last year to 1.53 million today. The increase partly reflects slower job growth in professional services. From this perspective the employment picture looks a little softer than a soft landing, particularly for college graduates. Hiring has also slowed in financial services and other occupations requiring a college degree.

Job growth is weakening in professional services but remains strong in many trades.

While professional employment has weakened, job growth remains strong in many trades. Construction added 34,000 jobs in August, surpassing the 12-month average of 19,000. Heavy and civil engineering contributed 14,000 jobs, as did nonresidential specialty trade contractors, reflecting the buildout driven by various fiscal initiatives. By contrast, residential construction job growth appears to be slowing, as the apartment boom winds down.

Health care employment increased by 31,000, well below the 12-month average of 60,000. Gains were led by ambulatory health care services (+24,000) and hospitals (+10,000), while social assistance added 13,000 jobs, with 18,000 coming from individual and family services.

Manufacturing employment edged lower, reflecting a net loss of 24,000 jobs, mostly in durable goods. Transportation equipment accounted for about half that loss, but cuts were broad based. Durable goods payrolls have shown little change throughout the year and remain a drag on broader job growth.

Other major industries, including mining, retail trade, transportation, information, and financial services, showed little change in employment. Average hourly earnings for private workers rose by 0.4% to $35.21 in August, translating to a 3.8% year-over-year increase. Production workers wages are up 4.1% year-to-year.

With job growth slowing, a quarter-point cut in the federal funds rate looks certain this month.

The weaker job growth, stagnating manufacturing sector, and higher unemployment rate make a quarter-point cut at the September FOMC meeting highly likely, with the possibility of a more aggressive move. Revisions to June and July data—showing a combined 86,000 fewer jobs—suggest labor market momentum may be waning faster than expected. Additionally, the narrowing breadth of job gains suggest the economy may be decelerating slightly beyond a “soft landing.”

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 6, 2024

Mark Vitner, Chief Economist

Piedmont Crescent Capital

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000