Inflation Once Again Tops Expectations

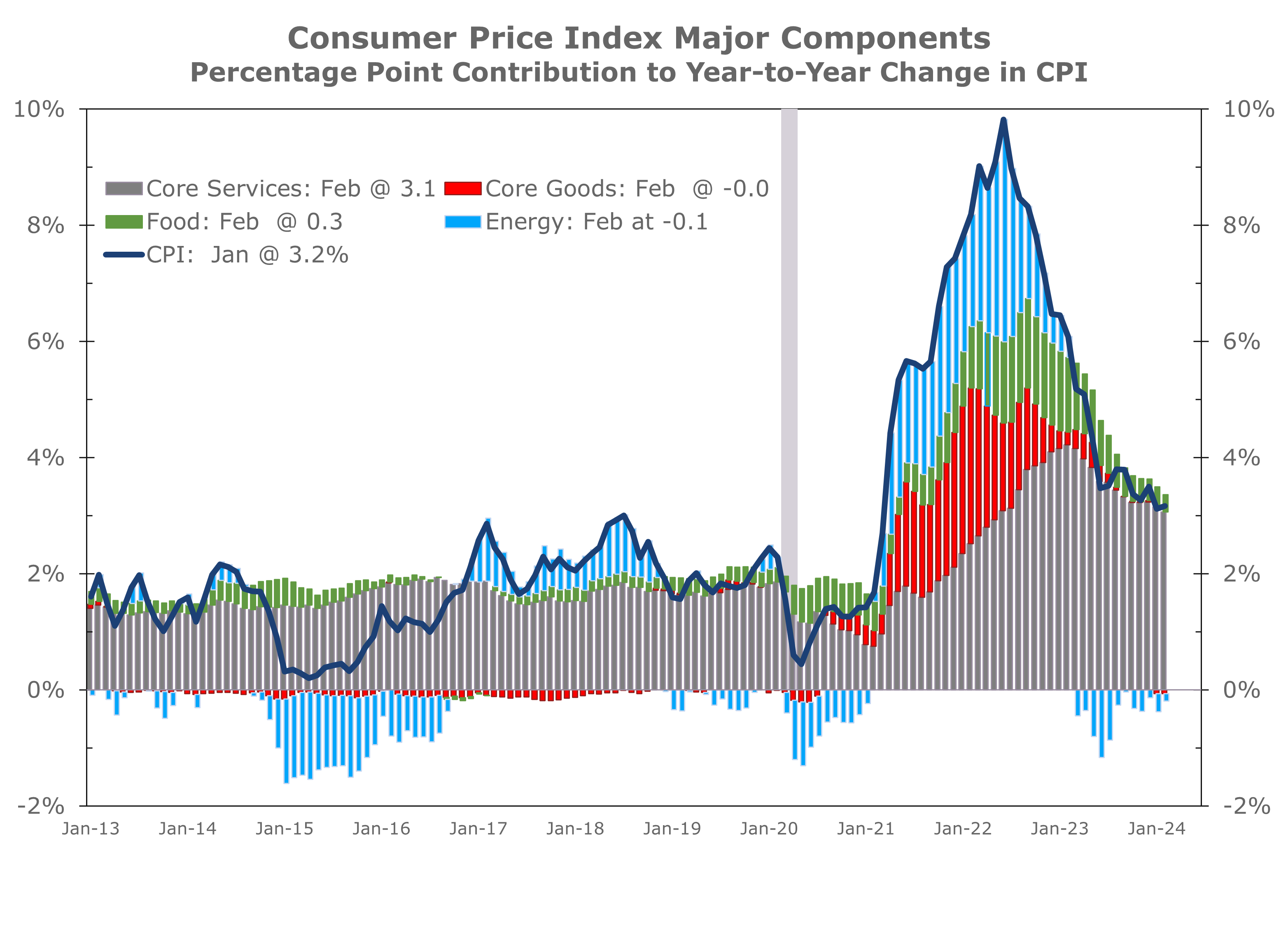

- Both the overall CPI and the core CPI rose 0.4% in February and are now up 3.2% and 3.8% year-to-year, respectively.

- We have continuously warned inflation would remain stubbornly high during the first half of 2024, reflecting continued pressures from labor-intensive sectors as well as some seasonal adjustment issues.

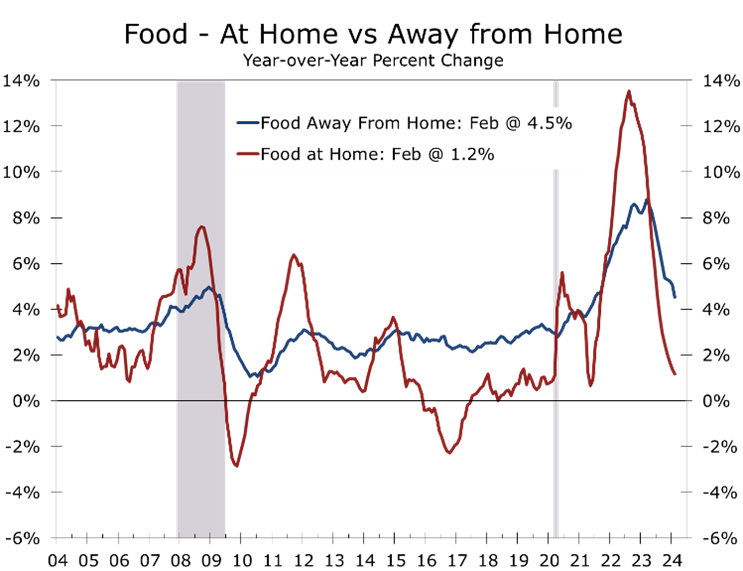

- Prices held steady at grocery stores and rose only slightly at restaurants. Unfortunately, both remain sharply higher than prior to pandemic, leaving budgets stretched.

- Energy prices rose 2.3% in February, with gasoline prices jumping 3.8% and prices for natural gas (+2.3%), fuel oil (+1.1%) and electricity (+0.3%) all climbing.

- Excluding food and energy products, the core CPI rose 0.4%, driven by another outsized rise in shelter costs. Prices for airline fares (+3.6%) and car insurance (+0.9%) also rose sharply.

- Inflation continues to come in hotter than expected. The breadth of price increases is narrowing, however, with much of this past month’s gains coming from higher housing and energy costs. We continue to expect the Federal Reserve to begin cutting interest rates in June, followed by additional quarter-point cuts in September and December.

Inflation once again exceeded expectations in February, with the CPI rising 0.4% and prices excluding food and energy also rising 0.4%. Despite the disappointing report, price increases were slightly less widespread than in January and show signs of moderating. However, the pace of moderation is slower than what financial markets had anticipated, leading many forecasters to push the Fed’s first rate cut out to June, a position we have held for some time.

One clear bright spot in the February data is that food prices are rising less rapidly. Prices remained unchanged at grocery store, following a 0.4% increase in January. Prices at restaurants rose just 0.1%, compared to a 0.5% increase in January.

Despite the moderation in food costs, consumers have not seen much relief. Grocery store prices are currently 25% higher than they were in February 2020 – the month before the pandemic hit.

Although prices eased last month, groceries and restaurant costs remain burdensome.

Prices at restaurants have risen by a similar magnitude since February 2020, surging 25.5%. Labor costs have increased sharply at both, rising by 24.9% at grocery stores over the past four years and 28.5% at restaurants. With wages sticky, a moderation in price increases is about as good as it is likely to get.

Persistently high food prices are one reason consumers feel discouraged about the economy. Families are spending 11% of their after-tax income on food, the highest proportion since 1991 according to recent USDA figures. With more income devoted to food, consumers have had to spend less on other items, had to dip into savings, or gone further into debt.

Election year politics is mischaracterizing the causes and remedies for high food costs.

President Biden has taken note of higher food prices and repeatedly cited “Shrinkflation” as one of the causes of higher inflation. Shrinkflation involves reducing the size or quantity of a product while keeping the price steady. The inference is that greedy companies or store owners are behind the higher prices. However, this explanation for inflation is fundamentally flawed and has been used over time, mostly by politicians, to shamelessly shift blame for higher prices, often toward middleman minorities.

Persistent inflation is always a monetary phenomenon. The money supply increased dramatically following the onset of the pandemic, as the Federal Reserve accommodated the massive increase in federal spending by increasing its purchases of federal debt. The growth in the money supply nearly perfectly matches the 25% cumulative increase in food prices.

Energy prices rose by 2.3% in February after two consecutive months of declines, with gasoline prices jumping by 3.8%. Energy prices have been the main contributor to lowering inflation over the past year. Even a slight reversal could significantly slow the improvement in the headline CPI.

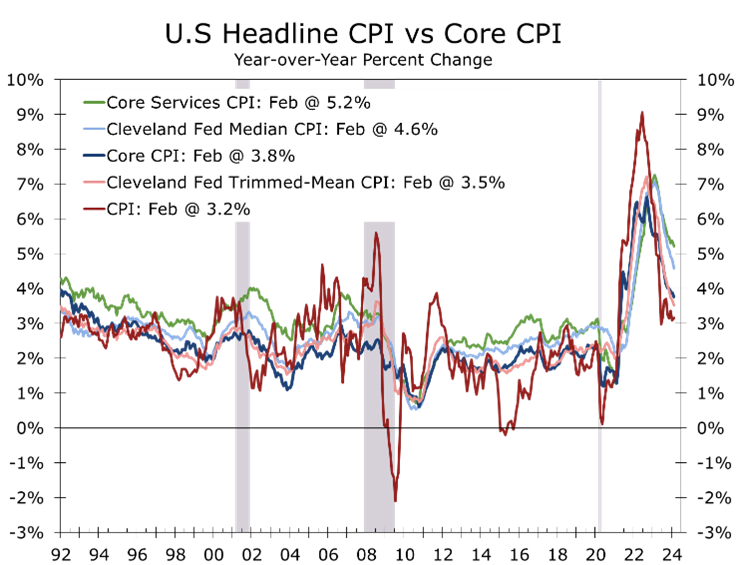

Excluding food and energy, the core CPI increased by 0.4% and rose by 3.8% year-on-year. Most goods experienced moderate price changes, although apparel and used car prices rebounded last month. Core goods prices fell 0.3% over the past year.

Core services present the greatest inflation challenge, with prices climbing 0.5% in February and 5.2% over the past year. Housing, particularly residential rent, drove much of the increase, with rents for single-family homes and lease renewals seeing significant rises. In contrast, rents for new leases are slightly declining.

We expect inflation to slowly moderate this spring and summer, allowing the Fed to begin cutting the federal funds rate in late June. We continue to closely monitor the median and trimmed mean inflation figures published by the Federal Reserve Bank of Cleveland, which continue to show a slower and longer journey back to the Fed’s 2% inflation target.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

704-458-4000