Housing Starts Stall, Remodeling Holds Firm

- Housing starts fell 11.4% in March to a 1.324 million-unit pace.

- Single-family starts fell 14.2% to 940,000 units — the slowest since May 2024. Multi-family starts fell 3.5%, as developers remain sidelined amid oversupply and financing hurdles. Building permits rose 1.6%, with all the gain coming in the more volatile multi-family sector.

- Starts plunged 31% in the West and 17% in the South, while the Midwest surged 76% on weather and timing.

- Tariffs, labor shortages, and uncertainty continue to weigh on builder confidence.

- While prospective buyer traffic remains weak, builders remain optimistic about sales over the next six months.

- Remodeling remains a bright spot, with spending supported by aging homes and strong homeowner equity.

- Tariffs, labor shortages, and policy shifts will continue to shape the housing landscape through 2025. Although mortgage rates are expected to ease slightly if the Federal Reserve follows through on anticipated rate cuts, affordability remains a challenge for buyers, especially in higher-cost regions.

Homebuilding entered the key spring building season on a cautious note, with a sharper-than-expected slowdown in new starts, even with better weather. Overall housing starts fell 11.4% month-over-month to a 1.324-million-unit pace, 100,000 units below consensus expectations. While total starts remained 1.9% above year-ago levels, the underlying trend remains weak, particularly the single-family segment.

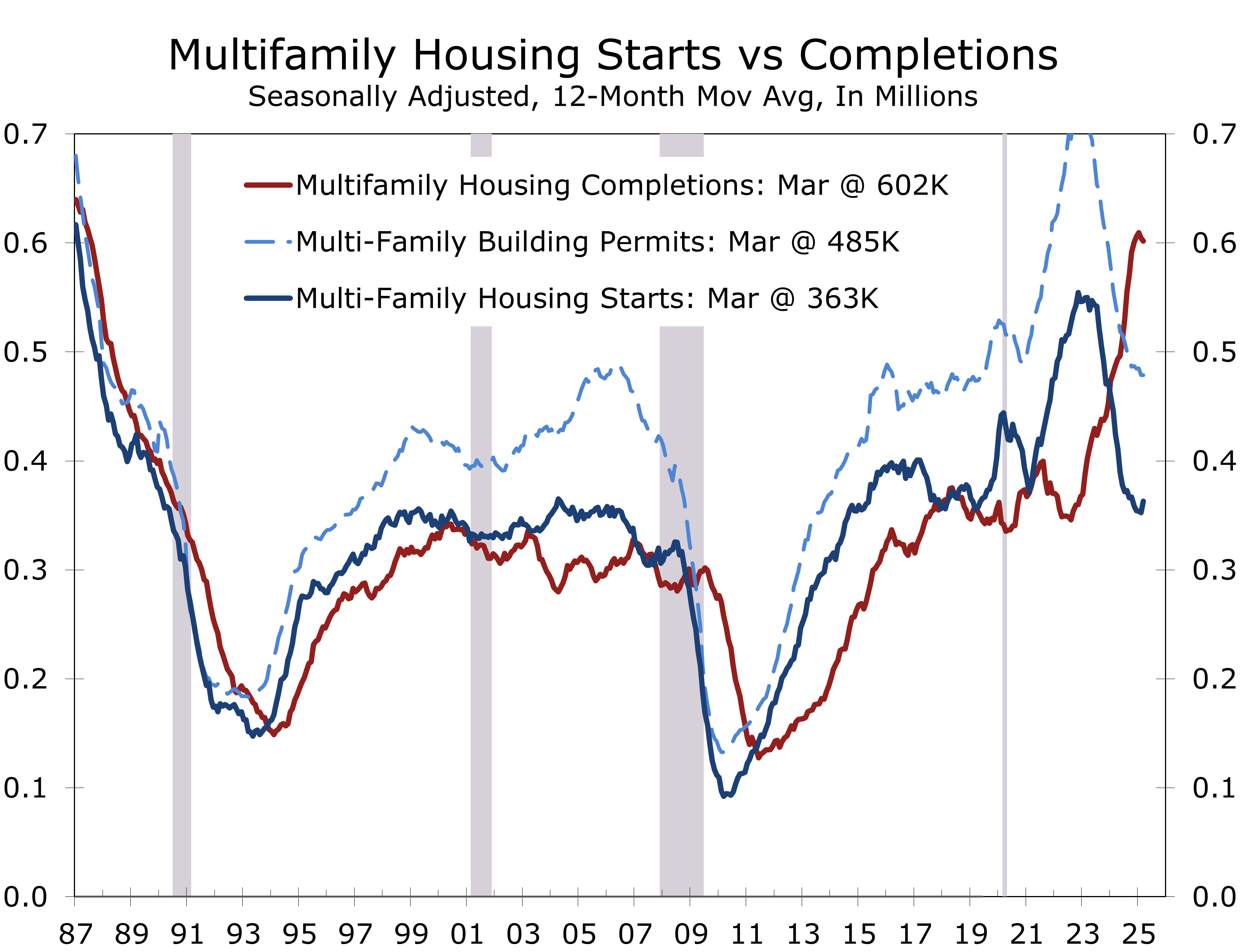

Single-family housing starts declined 14.2% to a 940,000-unit pace, the slowest pace since May and down nearly 10% from its year-ago pace. Single-family starts had remained above 1 million units during the prior four months, which is normally the slowest part of the year for homebuilding. The recent pullback underscores growing caution from homebuilders, even as mortgage rates have retreated modestly from their cycle highs. Meanwhile, multi-family starts held steady at 370,000 units, suggesting that developers remain sidelined amid oversupply concerns and persistent financing hurdles.

Building permits rose in March but the number of permitted-but-not-started projects has risen.

Building permits climbed 1.6% to a 1.482 million-unit pace — a modest upside surprise. Still, the wider than usual gap between permits and starts underscores the uncertain path forward, as rising inventories and tight credit temper future groundbreakings.

Regionally, the data painted a fragmented picture. The West posted a steep 30.9% drop, underscoring the sector’s greater vulnerability to rising materials costs and trade-related price volatility. The South — the nation’s largest housing market — fell 17.1%, in line with national trends. The Midwest surged an outsized 76.2%, likely driven by improved weather, lower land costs, and regionally specific, timing-related project launches rather than underlying demand strength.

Single-family homebuilding remains constrained by unrelenting affordability hurdles.

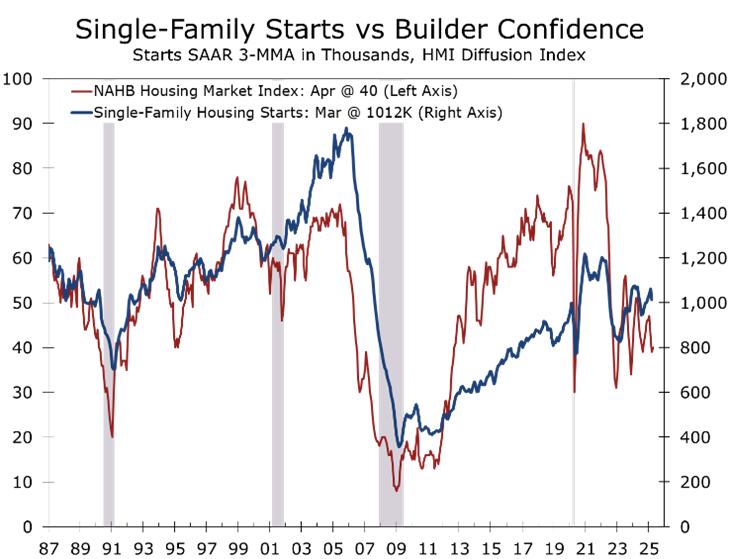

The single-family market remains constrained by affordability challenges, policy uncertainty, and a persistent shortage of buildable lots. The NAHB/Wells Fargo Housing Market Index (HMI) edged up to 40 in April but remains firmly in contraction, underscoring builder caution.

Tariffs have emerged as a key headwind, adding an estimated $9,200 in material costs per home. Higher costs will squeeze margins, particularly with nearly 30% of builders cutting prices and over 60% using sales incentives such as mortgage rate buydowns.

Despite these pressures, single-family starts are still expected to improve modestly this year as mortgage rates retreat toward the 6.5% range. Our baseline forecast assumes the U.S. narrowly avoids recession.

Multi-family starts, having already endured a steep 2024 contraction, remain stagnant. Developers face both an oversupply of new units and limited access to affordable capital, opening a wide gap between starts and permits. The NMHC Apartment Market Conditions Survey has now reported looser conditions for 10 consecutive quarters, while the Architectural Billings Index (ABI) for multi-family remains mired in negative territory for 31 straight months — a clear sign that recovery is unlikely in the near term. Leasing remains strong, which will hopefully help clear the deluge of completions from projects started back in 2022.

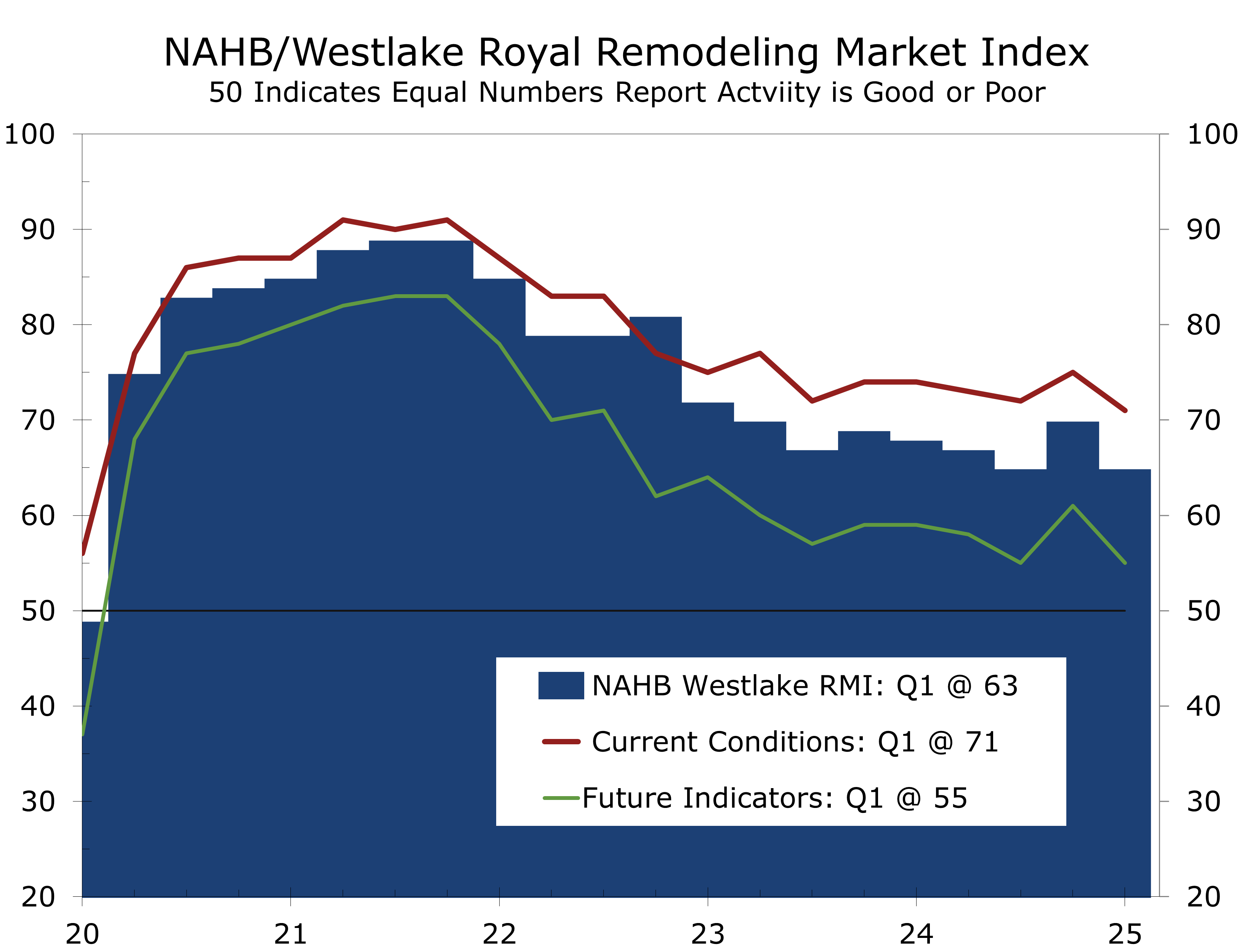

In sharp contrast to new construction, residential remodeling remains a relatively bright spot. The aging U.S. housing stock — now averaging 41 years — coupled with strong homeowner equity has fueled steady demand for renovations. The NAHB expects remodeling spending to grow 5% in 2025 and another 3% in 2026, despite higher material costs driven by tariffs on lumber and appliances.

The NAHB/Westlake Remodeling Market Index (RMI) slipped slightly to 63 in Q1 but remains in expansion territory. Homeowners continue to invest in upgrades, particularly as elevated mortgage rates keep more owners locked into their current homes.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

April 17, 2025

Mark Vitner, Chief Economist

(704) 458-4000