A Summertime Surge in Apartment Starts?

-

- Housing starts rose 5.2% in July to a 1.428 million SAAR, the strongest pace since February, and up 12.9% from a year earlier, with upward revisions to prior months adding further support.

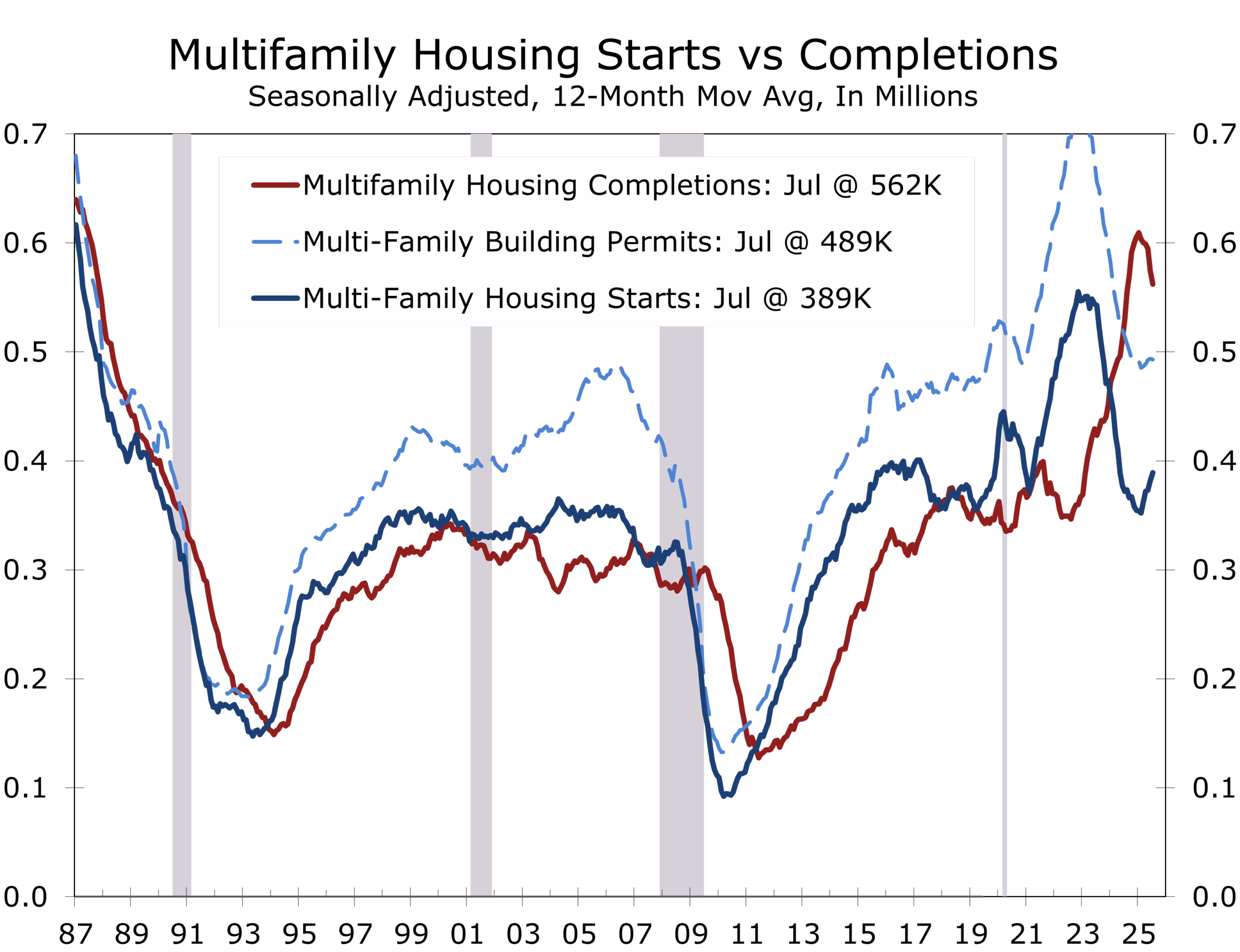

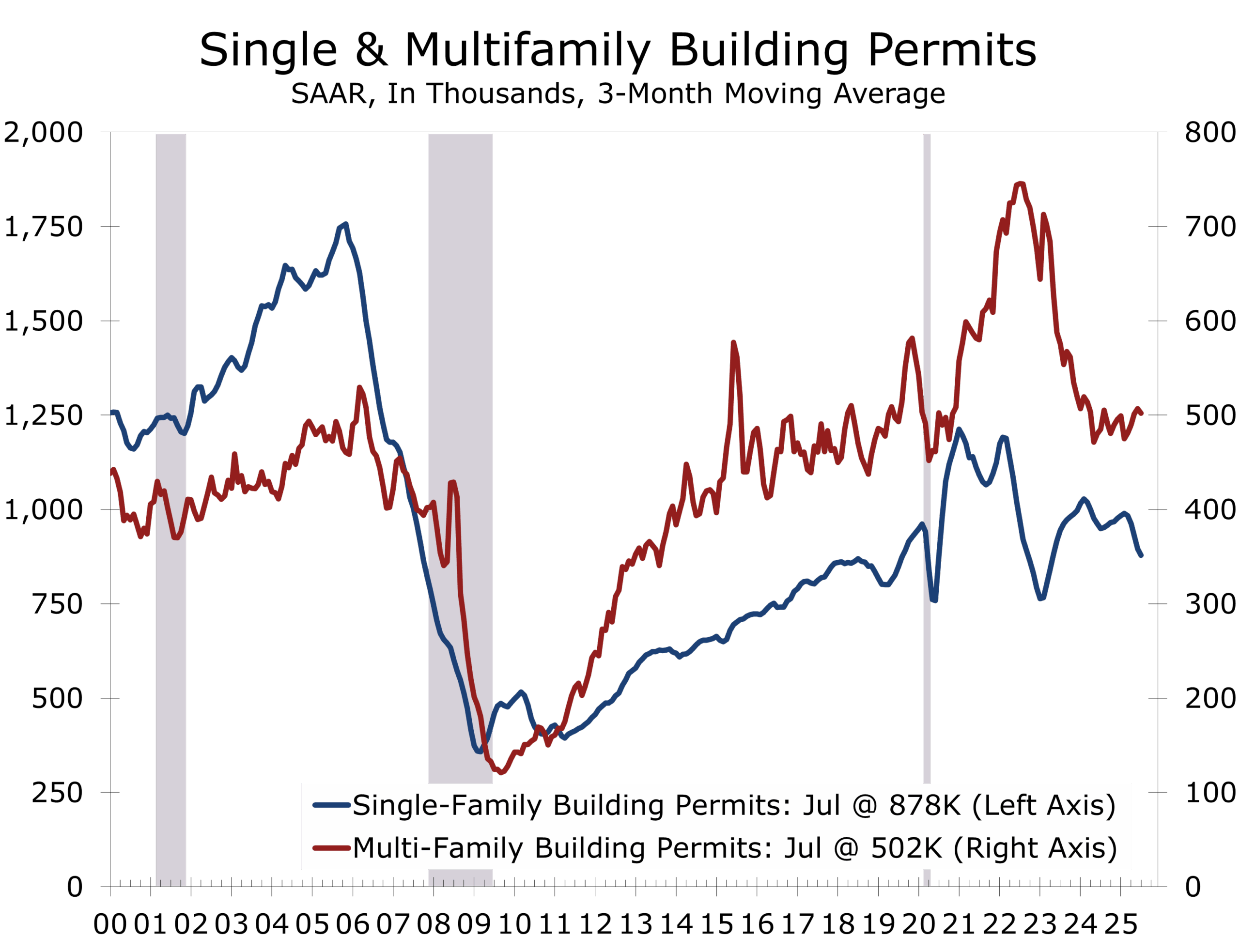

- Single-family starts edged up 2.8% to 939,000, while multifamily starts jumped 9.9% to 489,000, the highest since May 2023.

- Building permits fell 2.8% to 1.354 million, a five-year low, with single-family up modestly (+0.5%) but multifamily off sharply (-8.2%).

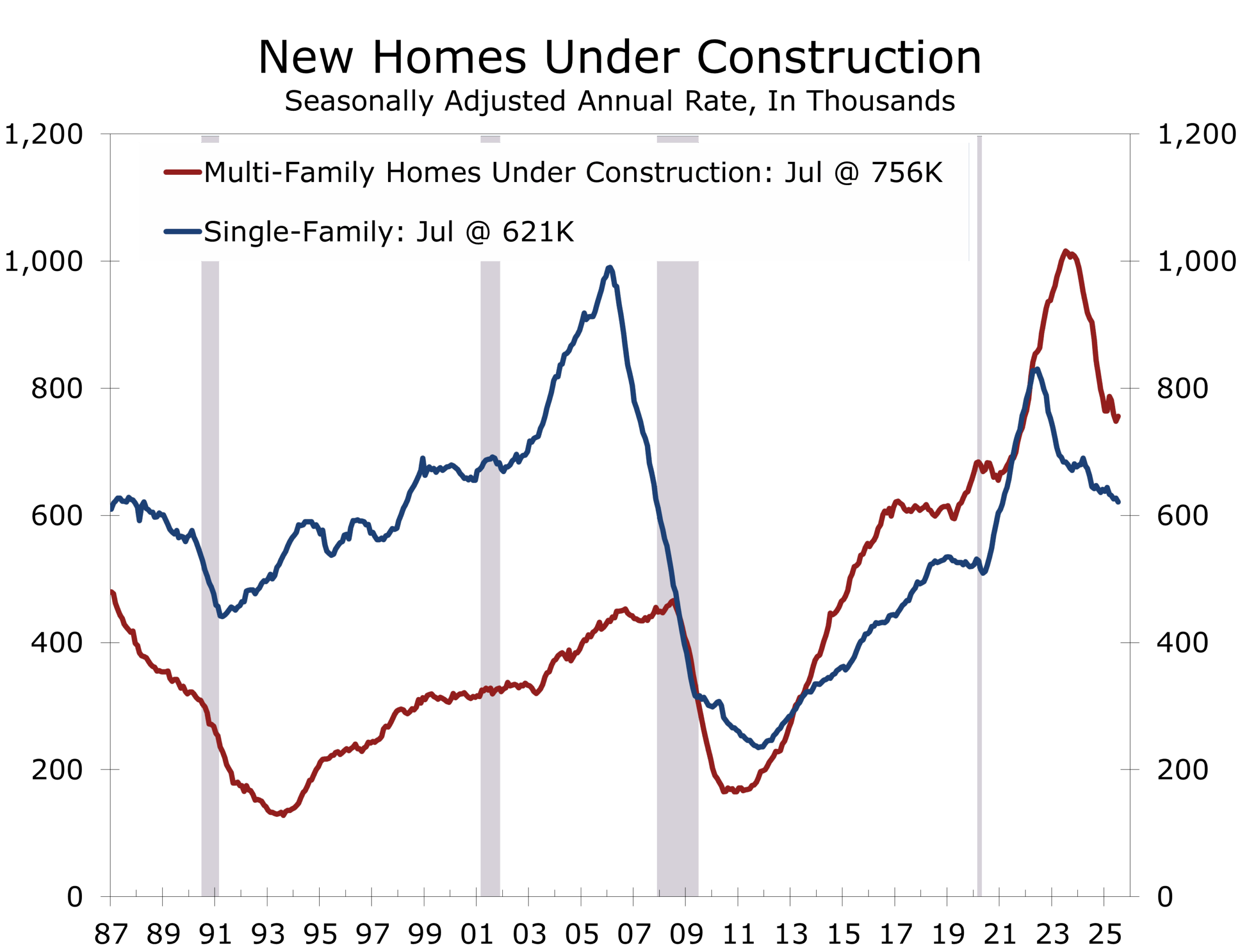

- Housing completions climbed 6.0% to 1.415 million, with single-family completions up 11.6% and multifamily up 2.9%, though units under construction remain elevated at 1.357 million, signaling ongoing supply pressures.

- Housing completions fell 4.0%, with single-family completions rising 7.1% and multifamily completions falling 20.8%.

- Builder sentiment dropped to 32 in August, the weakest since late 2022, as high mortgage rates and affordability constraints weighed on demand, with 37% of builders cutting prices and 66% offering incentives.

- Mortgage rates have eased to 6.6%, their lowest since October 2024, but affordability challenges and excess inventory are keeping buyers on the sidelines.

Apartment Building Drives Summertime Housing Starts Higher

Homebuilding reportedly firmed in July, with housing starts climbing to a seasonally adjusted annual rate of 1.428 million units. The 5.2% monthly gain was driven by a surge in multifamily construction, which offset only modest improvement in single-family building. While the rebound marks the strongest pace in five months, declining permits, which fell 2.8%, suggest that momentum may prove fleeting. Builders are discounting homes to clear inventories, which have risen to their highest levels in more than a decade.

Housing starts hit a five-month high in July, powered by a surge in multifamily construction.

July’s increase in starts was broad but driven largely by multifamily construction. Single-family starts rose 2.8% to 939,000, supported by slightly lower mortgage rates but still limited by affordability pressures. Multifamily starts jumped 9.9% to 489,000, the highest since mid-2023, though the surge may reflect reporting noise. Starts of five units or more climbed 11.6% to 470,000—the strongest July pace since the pandemic and the third highest in four decades. Permits have been running well ahead of starts for some time. Stronger than expected apartment demand this summer likely encouraged some delayed projects to break ground, especially those with permits issued earlier but postponed amid weaker conditions.

Regionally, the gains were concentrated in the South (+19.2%), which accounts for over half of all starts, and the Midwest (+33.3%), offsetting sharp declines in the Northeast (-26.0%) and West (-27.5%). Single-family starts rose only in the South, while multifamily starts tripled in the Midwest and grew strongly in the South but fell steeply elsewhere. Multifamily starts tend to be volatile on a monthly basis.

Single-family permits edged higher in July but are down 4.2% year-to-date and trending lower.

Permits offered a more cautious signal. Total authorizations fell 2.8% to 1.354 million, the lowest in five years. Single-family permits edged up to 870,000 in July. The gap between housing starts and permits quells any excitement about July’s stronger housing report. Permits are far less volatile than starts and are less prone to major revision.

Year-to-date through June, single-family permits declined 4.2% nationally to 577,600, with every region down except the Midwest (+8.2%), where affordability pressures are less severe. Houston and Dallas, the two largest markets, posted YTD declines of 8% and 10%. Starts also fell in Phoenix (-13%) and Atlanta (-14%) but held up better in Charlotte (-5%) and Nashville (-6%), while rising in Orlando (+13%) and Los Angeles (+5%).

Completions rose 6.0% to 1.415 million, with single-family completions up 11.6% to 1.022 million, reflecting builders’ focus on clearing backlogs. Multifamily completions rose modestly to 385,000. Units under construction remain historically high, most of which are apartment projects. The backlog of single-family homes under construction is more in line with historical norms and is steadily declining, hinting that single-family starts are near a bottom.

Builder sentiment continues to deteriorate, with the NAHB/Wells Fargo Housing Market Index falling to 32 in August, its lowest since December 2022. More than a third of builders report cutting prices, with average reductions of 5%, while two-thirds are offering buyer incentives. These trends reflect weak buyer traffic, affordability pressures, and caution going into the fall.

While mortgage rates have eased 40 basis points since early summer, now averaging 6.6%, high prices, labor shortages, and input cost pressures—exacerbated by tariffs—continue to constrain affordability. The recent improvement in starts provides a welcome boost but is unlikely to mark the beginning of a sustained upturn, with upward revisions to May and June appearing out of step with bloated inventories, weak builder confidence and more cautious lenders.

The outlook for housing remains challenging. With permits sliding to multi-year lows and builder sentiment eroding, construction activity is likely to soften in coming months. We expect housing starts to average 1.37 million units in the second half of 2025, with the sector continuing to drag modestly on GDP growth before conditions begin to gradually improve in early 2026

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

August 19, 2025

Mark Vitner, Chief Economist

(704) 458-4000