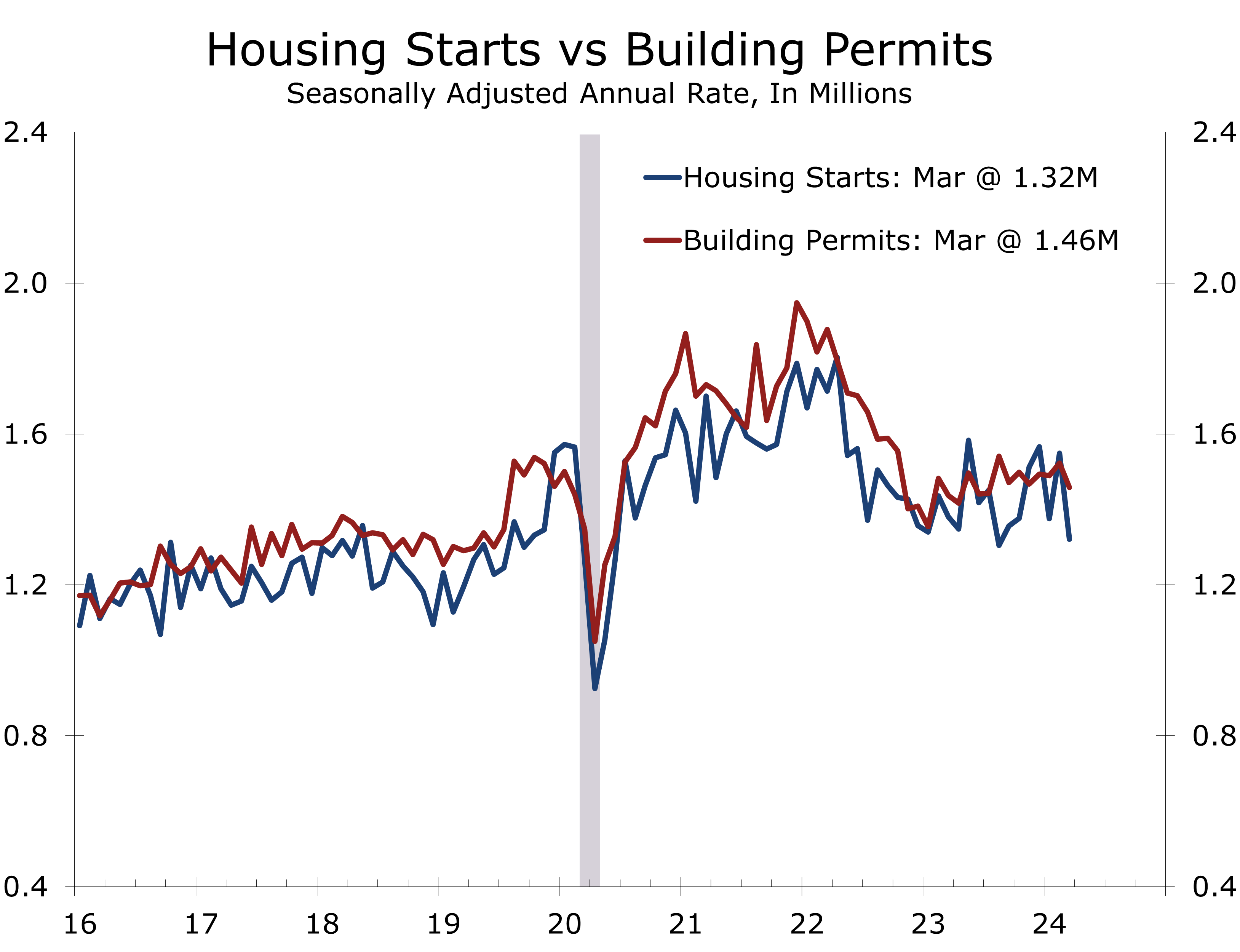

Surprising Weakness in Both Starts and Permits

- Housing starts plunged 14.7% to a 1.321 million unit annual pace in March.

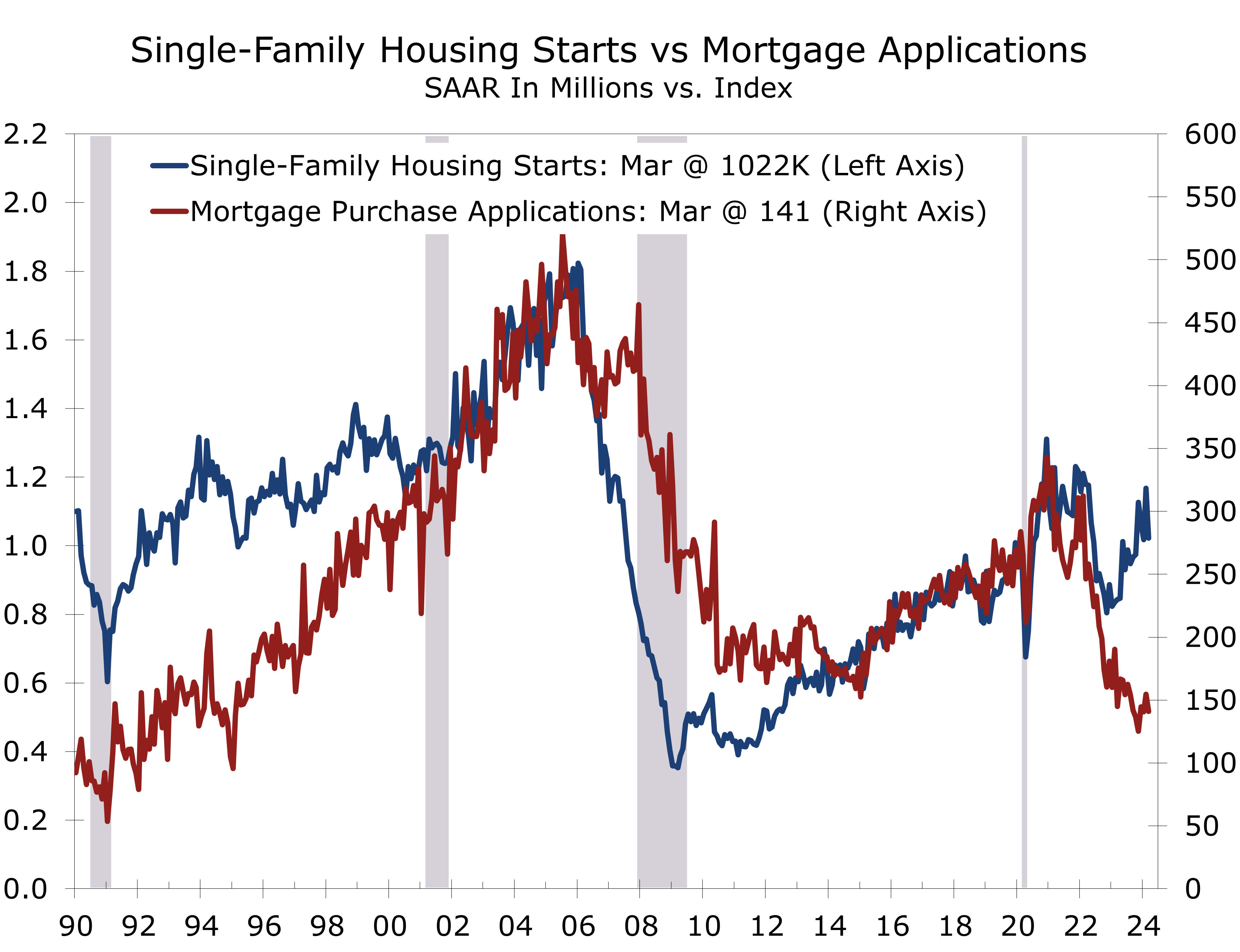

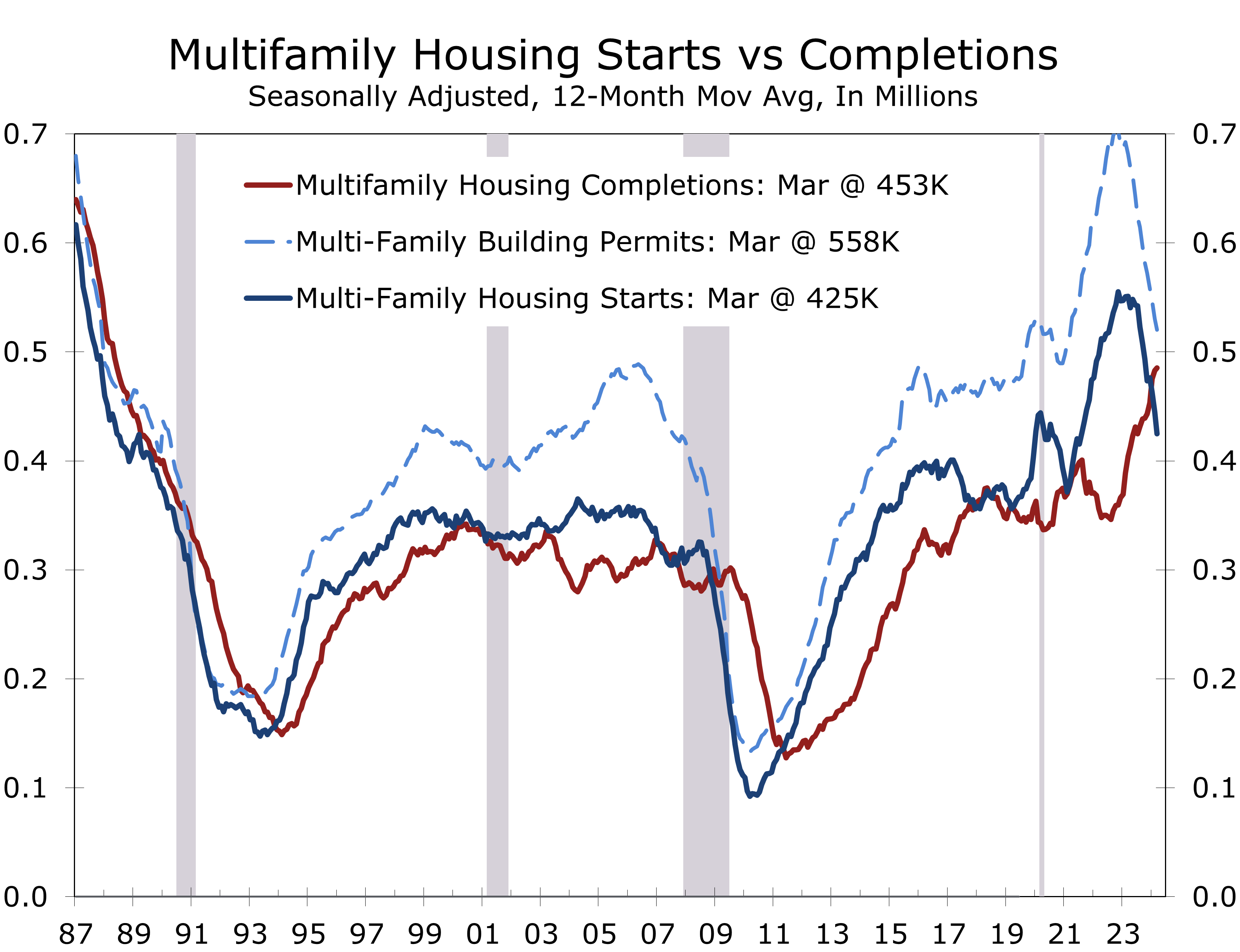

- Single-family starts fell 12.4% to a still solid 1.022 million unit pace, while starts of multi-family homes tumbled 21.7% to a 299,000-unit pace, the slowest pace since the pandemic low hit in April 2020.

- Building permits fell less dramatically, with single-family falling 5.7% and multi-family falling 1.2%.

- Home builder confidence was unchanged in April at 51, but expectations for home sales over the next six months weakened slightly.

- We suspect that seasonal issues are behind much of the pullback in housing starts. Milder than usual weather had allowed builders to begin work on more homes than usual during January and February, particularly in the Northeast and Midwest. As a result, there was a smaller than usual pickup in activity in March, resulting in a large seasonally adjusted drop. On a year-to-date basis through March, single-family starts are up a whopping 27.1% from the first three months on last year.

After months of predominantly upside economic surprises, housing starts plunged 14.7% to a 1.321 million unit annual rate, which was well below market expectations. Both single-family and multi-family starts fell sharply during the month, with the latter falling to its lowest level since its pandemic low, hit in April 2020.

Building permits fell less drastically, with overall permits falling 4.3% to a 1.458-million unit pace. Single-family permits fell 5.7% to a 973,000-unit pace, while multi-family permits fell 1.2% to 485,000 units.

While the drop in starts comes at a time that mortgage rates have spiked, the most recent spike in rates occurred well after the period covered by the March starts. We suspect the culprit was more innocuous. Milder weather allowed builders to begin work on more homes during the normally seasonally slow January and February period, which meant activity picked up less than usual in March, resulting in a large seasonally adjusted decline.

Seasonal factors likely exaggerated the slide in housing starts. Permits provide a better guide.

Permits are less volatile and provide a better indication of the underlying trend in home building. We expect starts to rebound, with single-family starts rising to around a 1.1 million unit pace later this spring and summer. Multi-family starts also appear poised for a rebound, with March’s 299,000 pace substantially below the most recent level for multi-family permits.

Higher mortgage rates will clearly impact the housing outlook. Rates spiked following the release of the March CPI, on April 10, and have remained high ever since. That news clearly came too late to impact March housing starts but also appears to have come too late to impact the April NAHB/Well Fargo Home Builders Index (HMI), which was unchanged at 51 in April.

The components of the HMI were mixed in April, with builders’ assessment of present sales rising 1 point to 57 and traffic of prospective buyers rising 1 point to 35. Expectations for sales over the next six months fell 2 points to 60, however, likely reflecting growing concerns about higher interest rates.

Higher interest rates puts hopes for revival in home building at risk.

So far, home builders have adapted to higher interest rates remarkably well. Builders have shifted incentive budgets to rate buy downs, which has helped reduce the sting from higher mortgage rates, particularly for first-time buyers. Unfortunately, interest rates now look like they will remain higher for even longer. A string of hotter than expected inflation reports and stronger than expected job growth and consumer spending has likely pushed the prospect of rate hikes into either late this summer or even this fall. We now expect the Fed to reduce rates only 2 times this year, with cuts coming in September and December.

Even our more cautious rate outlook looks like a stretch today, with the financial markets currently pricing in just 1 quarter-point cut in the federal funds rate over the next year. Housing starts may have gotten a little ahead of themselves, anticipating a continued buyer shift away from existing homes. A wide gap has opened up between single-family starts and mortgage purchase applications from its normally tight relationship.

A 21.7% plunge in multifamily starts accounted for much of the pullback in overall housing starts during March. At just a 299,000-unit pace, multifamily starts are now substantially below permits, which came in at a 485,000 unit pace. We expect the gap between starts and permits to narrow next month.

Longer term, apartment construction is undergoing a multi-year correction as projects started over the past few years are increasingly being completed. That surge in completions is pulling vacancy rates higher and reducing rents. Securing credit for new apartment projects is becoming more challenging, which will weigh on apartment starts. Our latest forecast has single-family starts rising to just under 1.1 million units this year, while multifamily starts fall to 350,000 units.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

April 16, 2024

Mark P. Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

Chief Economist (704) 458-4000