Single-Family Starts Rose Solidly in July

- Housing starts rose 3.9% to a 1.452-million-unit pace in July. Sales in June were revised lower, while sales in May were revised slightly higher. On net, starts are roughly 1.3% ahead of where they were initially reported to be for June.

- Permits rose just 0.1% and are running slightly below starts at 1.442 million units.

- Starts rose in every region except the South. Starts jumped 14% in the West, with all the gain coming in single-family homes.

- Housing completions fell 11.8%, with a huge 38.8% plunge in completions of projects with 5 or more units (mostly apartments).

- The backlog of apartment projects increased further, however, while the number of single-family homes under construction continued to edge lower.

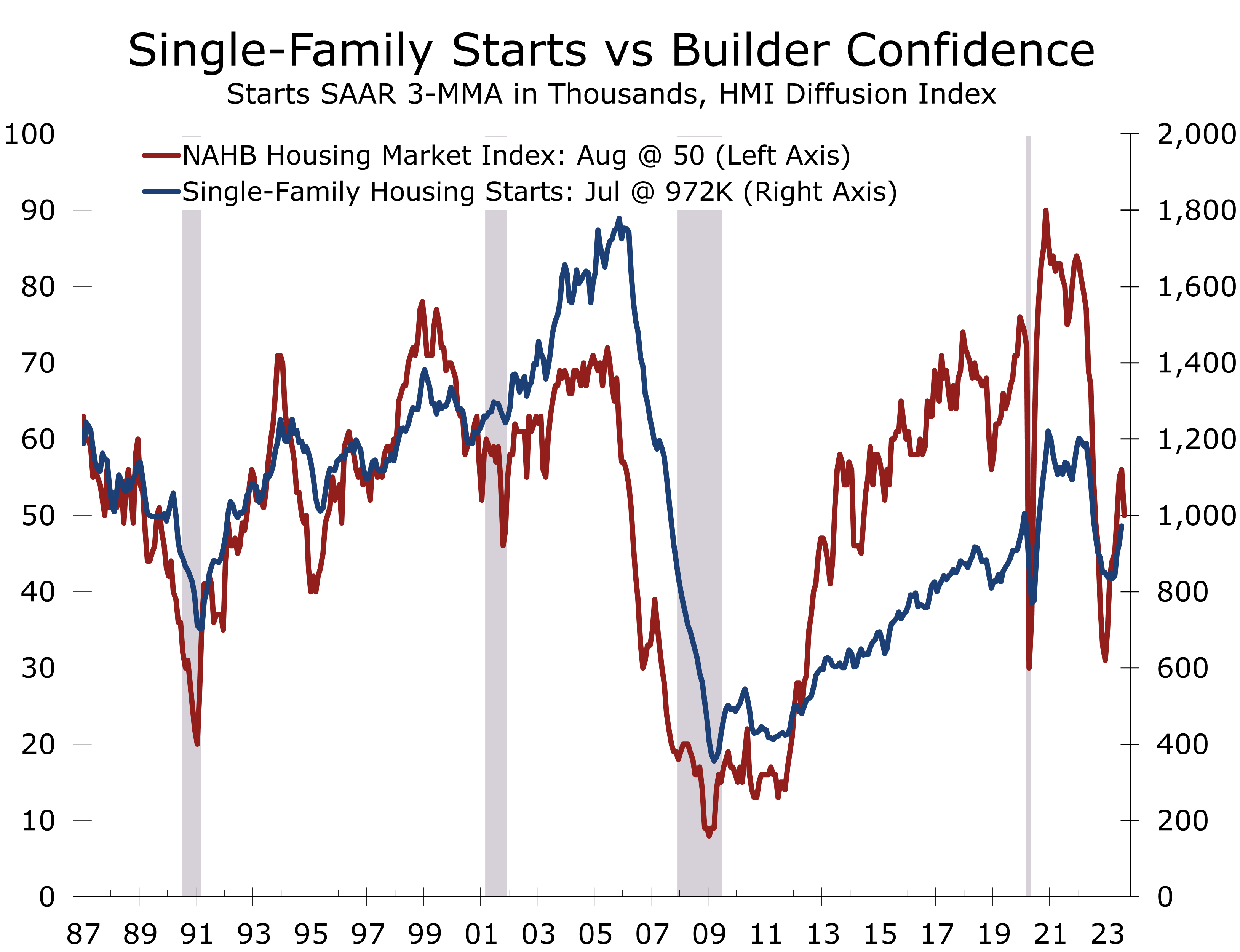

- Homebuilder confidence declined 6 points in August to 50, with both current sales (-5 pts) and expected sales (4 pts) falling decisively.

- Housing appears to be at an inflection point. Rising vacancy rates, weaker rent growth and tightening credit are slowing multifamily starts, while higher interest rates are restraining demand for single-family homes.

Housing starts rose 3.9% to a 1.452-million-unit pace in July, which was close to market expectations. Starts for June were revised down 36,000 units to 1.398-million-unit pace, while starts for May were revised up 24,000 units to 1.583-million unit pace. Overall housing starts were slightly lower than initially thought during the second quarter, which means current quarter starts are on a fairly strong footing.

Residential investment has been a net drag of real GDP for the past 9 quarters. Much of that weakness has come from declines in existing home sales, which have cut into commission income for realtors and home improvement spending. Sales of new single-family homes also weakened late last year but have revived more recently, as the paucity of existing homes for sale has sent more buyers into the new home market.

Housing affordability is currently stretched to historic levels relative to income.

The migration of buyers from the existing home market to the new home market is not a one-for-one tradeoff. Housing affordability is currently stretched to historic levels relative to income. Mortgage rates have also spiked back to levels briefly hit last November, which is prompting more builders to offer incentives.

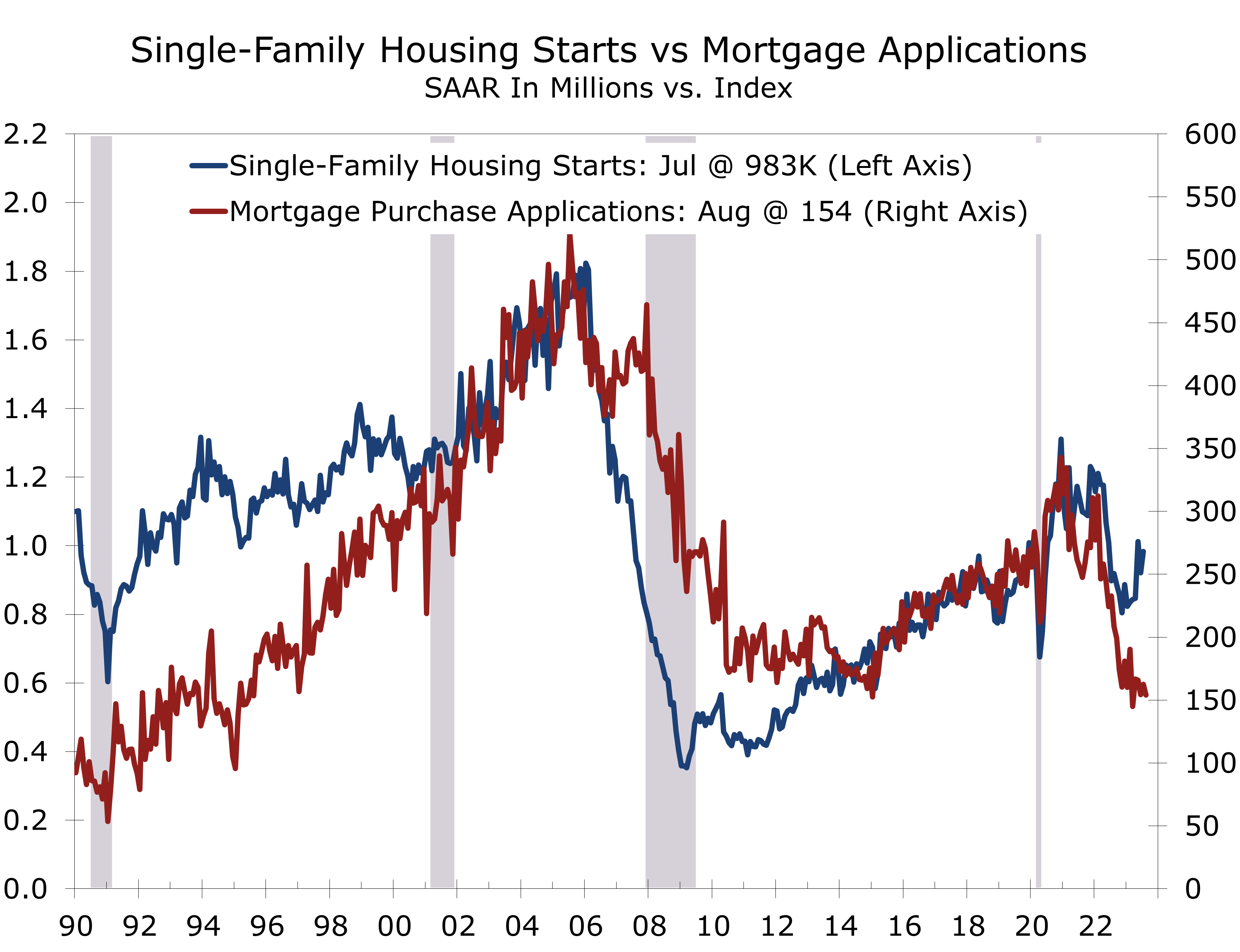

Cash buyers are also helping prop up the single-family market. Many buyers relocating from the Northeast and West Coast to the South and Midwest are able to pay cash for homes, which is one reason single-family starts have diverged from mortgage applications.

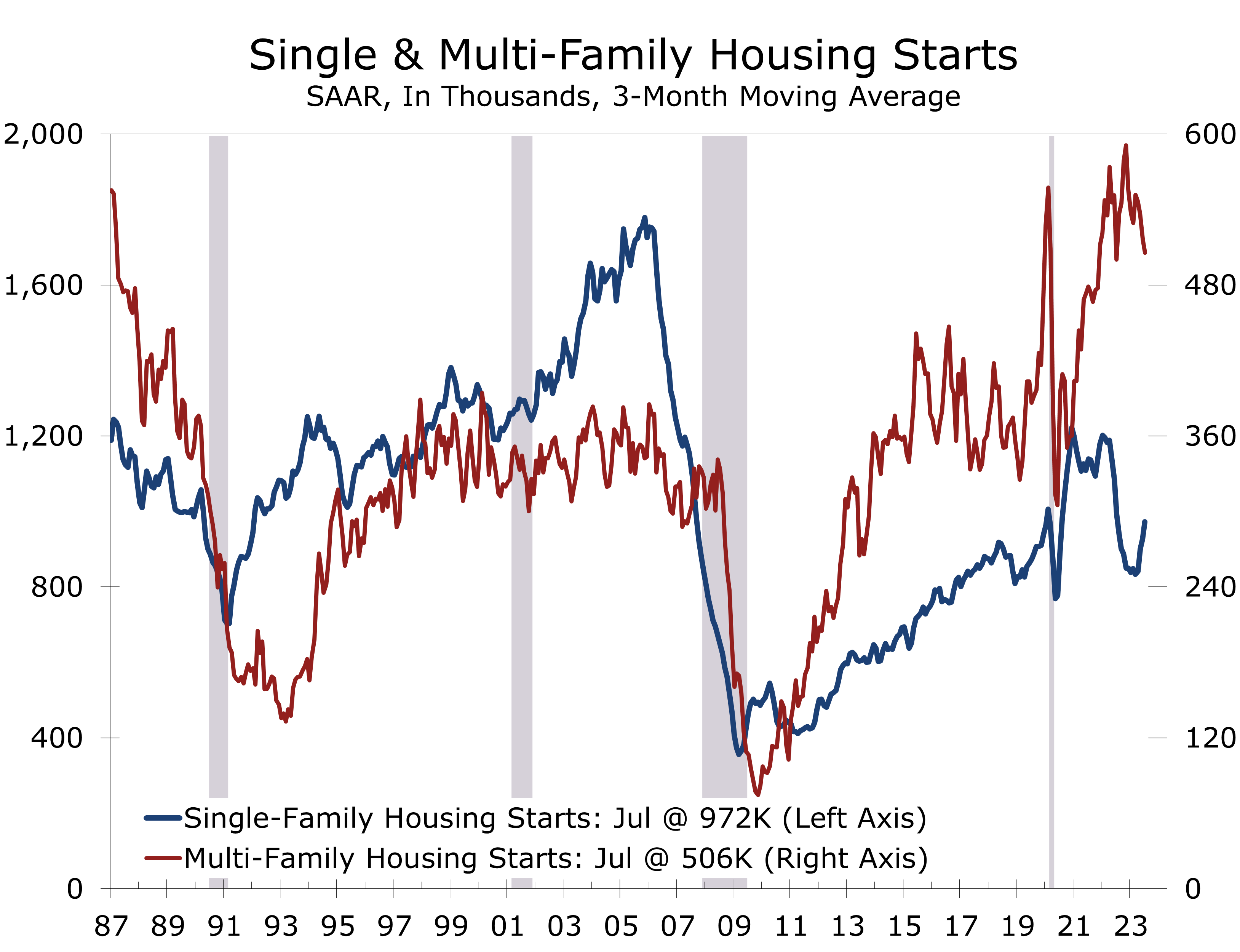

Single-family starts rose 6.7% in July to a 983,000-unit pace. The West accounted for the bulk of the increase in single-family starts, with starts jumping 26.5% to a 257,000-unit pace. Single-family starts also rose in the Midwest (+12.5%) but fell in the North (-3.4%) and the South (-1.3%), which is by far the largest region for single-family construction.

The large increase in the West looks suspect and will likely be reversed in the coming months. Single-family permits are less volatile than starts and rose just 0.6% in July. The South and Midwest both posted modest gains, while single-family permits fell 10.5% in the Northeast and were unchanged in the West.

Cash buyers can only support the housing market for a short time. Most home buyers finance their purchase and with mortgage rates currently near 7.25%, we suspect the housing market has reached a key pivot point. The inverted yield curve means there is relatively little savings from choosing an adjustable rate mortgage and underwriting remains still tight.

We look for single-family starts to decline modestly during the second half of this year. The earlier pullback in home sales and single-family starts, however, means most of the correction in the single-family market has already occurred. We see starts falling around 5% from their second quarter average by yearend.

The correction in multi-family construction is only beginning. Multi-family starts fell 1.7% in July to a 469,000-unit pace, after tumbling 16.5% the prior month. Multi-family starts are currently at their lowest level since September 2021. Permits fell slightly less, however, and are still running well ahead of starts.

The hurdles for financing new apartment projects have risen substantially.

The hurdles for financing new apartment projects have risen substantially, as is evident in recent surveys from the National Multifamily Housing Council. With nearly 1 million apartments under construction, there is a wave of supply set to come to market as vacancy rates are rising and student loan repayments begin to cut into disposable income. Multi-family starts will likely decline 11% from their Q2 pace by yearend.

The NAHB/Wells Fargo Housing Market Index fell 6 points in August to 50. Builders are increasingly having to offer discounts to counter the impact of rising rates. The drop ends a string of 7 consecutive increases and brings the HMI back in line with single-family starts. Builders will continue to focus on reducing their still high work-in-process inventory.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.