Housing Starts Rise from a Lower Level

- Housing starts rose a smaller than expected 5.7% in April to a 1.36-million-unit annual pace. Data for prior months were also revised lower and permits declined.

- The underlying details in the report were weaker than expected, with all of the gain in housing starts coming from a partial rebound in volatile multi-family units.

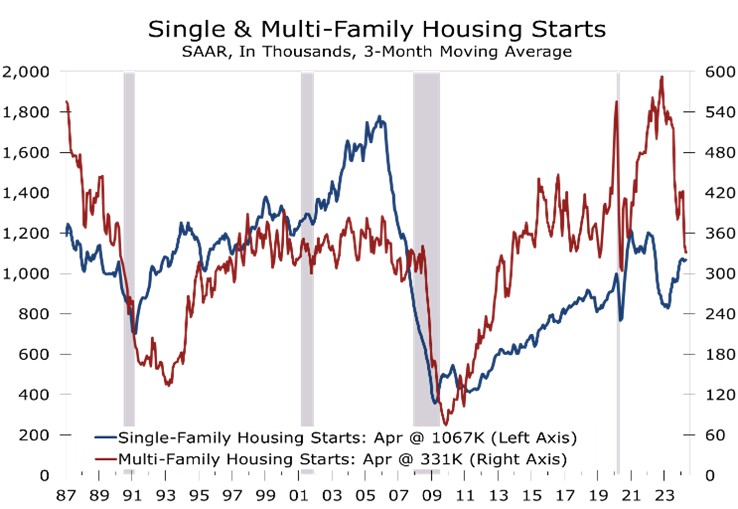

- Multi-family starts rose 18.7% in April, following a 43.8% plunge the prior month. Apartment starts have been trending lower for more than a year.

- Single-family starts fell 0.4% to a 1.031-million unit pace. Starts fell in every region except the West.

- Housing permits fell 3.0% overall, with single family dipping 0.8% and multi-family permits declined 6.9% and are now at their lowest level since October 2020.

- Housing completions jumped 8.6% in April, with all of the gain coming in single-family.

- Higher mortgage rates are clearly impacting home building, resulting in reduced buyer traffic and decreased builder confidence. Builders are holding off starting construction on new homes as they finish existing ones and now have inventory to sell.

Housing starts rose less than expected in April and starts for the prior month were revised sharply lower. Overall starts rose 5.7% to a 1.36-million-unit annual rate. Starts for the prior month were revised down by 34,000 units, revealing a softer underlying trend.

The monthly housing data have been harder to read recently. Builder optimism surged late last year on renewed hopes for lower interest rates following the Fed’s December FOMC meeting. This optimism primarily impacted the single-family market, prompting a jump in starts during a typically slow seasonal period. A string of stronger economic reports earlier this year, however, led to renewed uncertainty about the timing and extent of any interest rate cuts, leading builders to adopt a more cautious approach.

Home builders have become more cautious about interest rates, leading to fewer starts.

Meanwhile, multi-family starts have been pulling back for more than a year. An earlier surge in starts combined with longer cycle times, due to long-running shortages of labor and key building components, led to a huge backlog of projects which are now being finished. This backlog of projects is now being completed, resulting in a surge of new supply, rising vacancy rates, and less new construction.

Single-family permits fell even more than starts, dropping 0.8% in April following a 4.2% drop in March.

Builders may have gotten a little bit ahead of demand. Buyer traffic has been bolstered by a persistent shortage of existing homes for sale, which has shifted more buyers to the new home market. Home builders have embraced the influx and shifted marketing dollars to rate buydowns and also shifted the mix of homes being built toward lower priced models in the outlying areas of rapidly growth parts of the South and West.

While those shifts have helped bolster sales, particularly among first-time home buyers, housing affordability remains challenging across much of the country and a growing proportion of renters are opting to renew their leases rather than purchase a home.

Reduced housing affordability will likely keep a low ceiling on single-family starts this year.

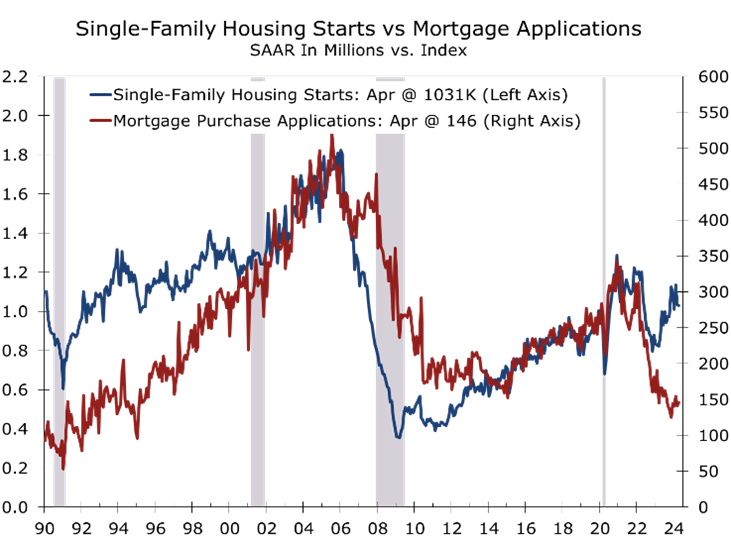

We are concerned about the wide gap that has opened up between and single-family housing starts and mortgage purchase applications. The two series have historically moved closely together. Part of the gap likely reflects the larger proportion of single family homes being built for rent, which is particularly popular in rapidly growing parts of the South. An influx of home buyers in the South and Midwest, flush with equity from selling their home in higher priced markets in the West and Northeast, might also being bolstering cash sales. A third explanation, however, is that builders just got a bit ahead of demand.

The correction in the multi-family market is more straightforward. The past decade saw a migration back into center cities and major employment centers, spurring a boom of mid-rise and high-rise apartments. The long cycle times for these projects led to a growing backlog of projects, which really took off after the pandemic as demand surged and lower interest rates set off a building boom.

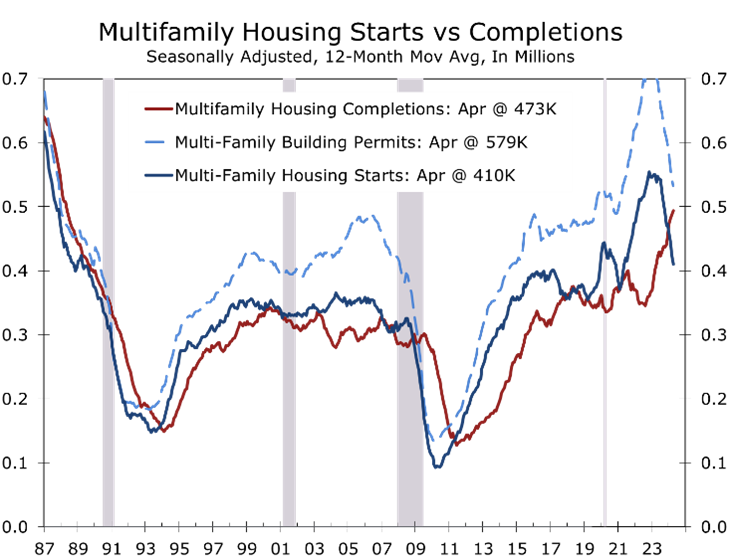

A wave of 473,000 new multi-family units, mainly rental apartments, entered the market this year. The bulk of that new supply was delivered in the South., mirroring recent migration trends. Multi-family starts have totaled just 410,000 units this past year and are running 33% below their year ago pace through April. Multi-family permits are running 23% below their year ago level and remain well above starts. Tighter credit will likely keep many of those projects on hold.

April’s softer housing data suggests building activity will moderate this spring. Any hit to output from a drop in starts will at least partially be offset by the still hefty pipeline of single-family homes and apartments in the construction pipeline. Moreover, lower mortgage rates should boost single family starts in the second half of the year.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 16, 2024

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000