Affordability Hurdles Limit Existing Home Sales

- Existing home sales fell 5.4% in June to a 3.89-million-unit pace and are also down 5.4% on a year-to-year basis.

- Sales are well below their pandemic lows and essentially running even with levels hit at the bottom of the Global Financial Crisis.

- Sales of existing single-family homes fell 5.1 in June and are down 4.3% over the past year. Sales of condominiums and co-ops fell 7.5% in June and are off 14% year-to-year.

- The inventory of unsold homes rose 3.1% to 1.32 million units at the end of June and translates to a 4.1-month supply.

- The median price of an existing home rose 4.1% year-to-year to $426,900. Prices are up 9.7% in the Northeast, 5.5% in the Midwest, 3.5% in the West and 1.7% in the South.

- Sales fell in every region, led by an 8.0% drop in the Midwest and 5.9% drop in the South. Sales fell in every region year-to-year except the West, which was unchanged.

- Affordability challenges persist, but rising inventories are gradually balancing the housing market and offering buyers more options. With mortgage rates falling, sales should improve this fall.

Sales of existing homes fell by 5.4% in June to a 3.89-million-unit annual rate. Persistently high mortgage rates and record-high home prices have sidelined many potential buyers. However, sales of higher-priced homes are holding up relatively well, helping pull the median price 4.1% higher year-over-year to a record $426,900 in June.

The rise in median home prices highlights the ongoing economic disparity in the U.S. Upper-income households are benefiting from a booming stock market, while middle-income families struggle with increasing costs for food, transportation, and housing. Over the past year, sales of single-family homes priced at $1 million or more have risen by 15%, while sales of all other homes have fallen by 5.9%. Many middle-income buyers have been priced out of the market and continue to rent.

Higher home prices and persistently high mortgage continue to weigh on home buying.

Regional variations in sales contributed to higher home prices. In the West, the highest-priced housing market with a median price of $629,800, sales remained unchanged year-over-year. By contrast, sales fell by 6.9% in the South, where the median is $373,000, and by 6.1% in the Midwest, with a median price of $327,100—both regions being larger and more affordable than the West. In the Northeast, another high-priced but smaller market with a median price of $521,500, sales declined by 6% year-over-year.

June’s decline in home sales, although slightly larger than expected, is not surprising. Existing home sales reflect closings, which typically lag pending home sales (signed purchase contracts) by one to two months. Pending home sales have dropped sharply over the past year, as many potential buyers are choosing to wait for mortgage rates to decrease further.

According to Freddie Mac, mortgage rates averaged 6.77% during the week of July 18, an improvement from recent months when rates hovered around 7%. We anticipate that more buyers will return to the market once rates drop below 6.50%, which we expect to happen this fall. However, a return to sub-4% mortgage rates is unlikely, and buyers will need to adjust to rates in the 6% to 7% range.

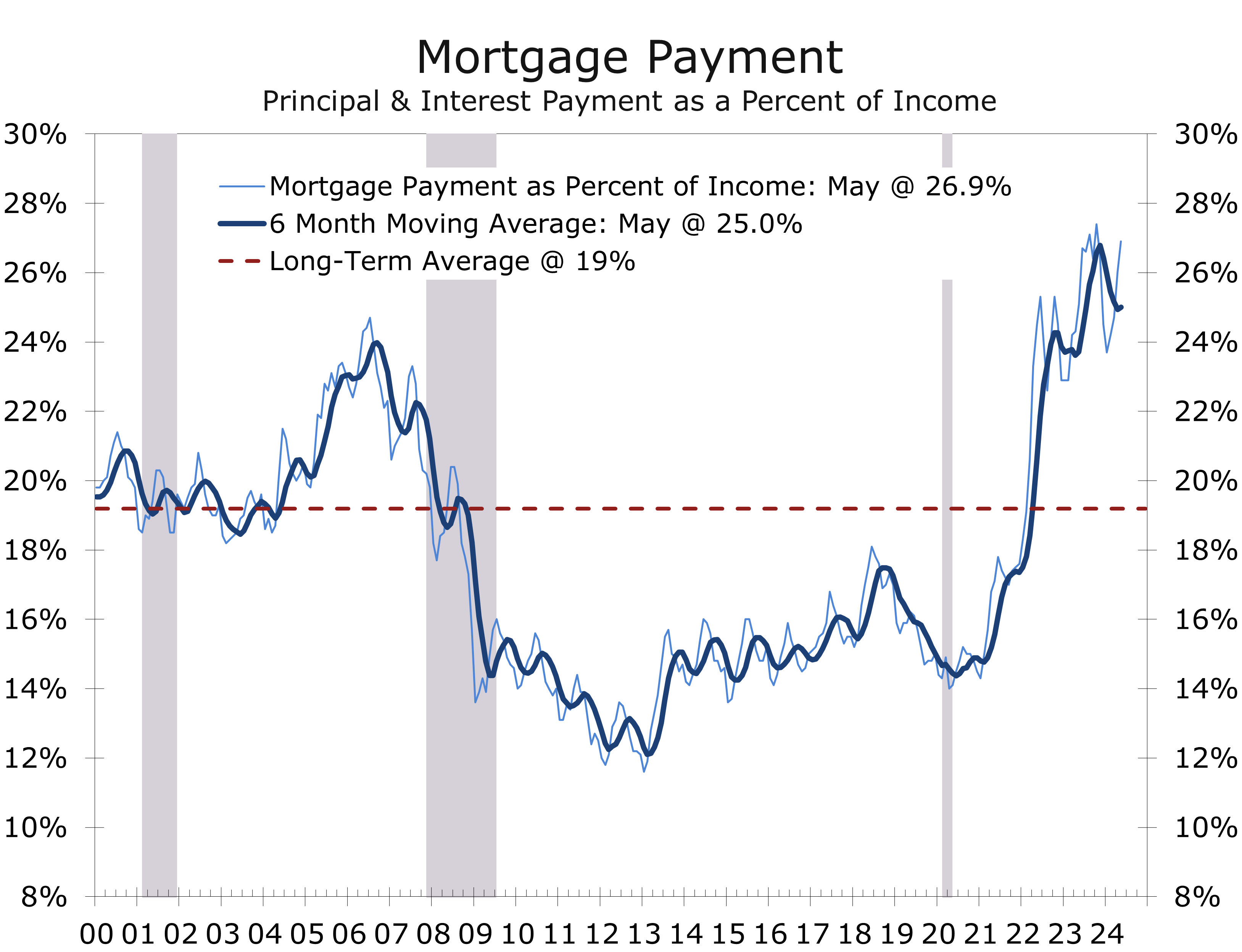

Higher home prices and persistently high mortgage rates have significantly impacted affordability. For a family purchasing a median-priced home with a 20% down payment, monthly principal and interest payments have soared from $984 in February 2020 to $2,291 in May 2023, a 132% increase. These payments now consume 26.9% of the median household income, up from 14% before the pandemic and well above the long-term norm of 19%. Consequently, we anticipate only a modest rebound in sales, even as mortgage rates decline this fall.

The high cost of homeownership is prompting many current homeowners to stay put, especially those with homes owned outright or financed with 30-year fixed mortgages at 4% or less. This “lock-in effect” is significantly impacting the economy by reducing housing turnover and limiting options for prospective buyers, which is further discouraging trade-ups, downsizings, and relocations.

The slowdown in new home sales has also affected related sectors. Furniture and home furnishings sales have dropped 6.8% over the past year, and sales at home improvement stores have also struggled. Typically, there is substantial spending to prepare homes for sale and again after purchase, but this has decreased. Spending on home improvements has grown more slowly, mirroring trends in home sales, with stronger performance at the high end of the market compared to the middle and lower ends.

This weakness in existing home sales is expected to produce a slight drag on second-quarter GDP growth. Besides the direct effects on housing-related spending, existing home sales impact real GDP through Realtors’ commissions and fees earned by lenders, insurers, appraisers, home decorators, and others.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000