Higher Rates and Tighter Lending Reign

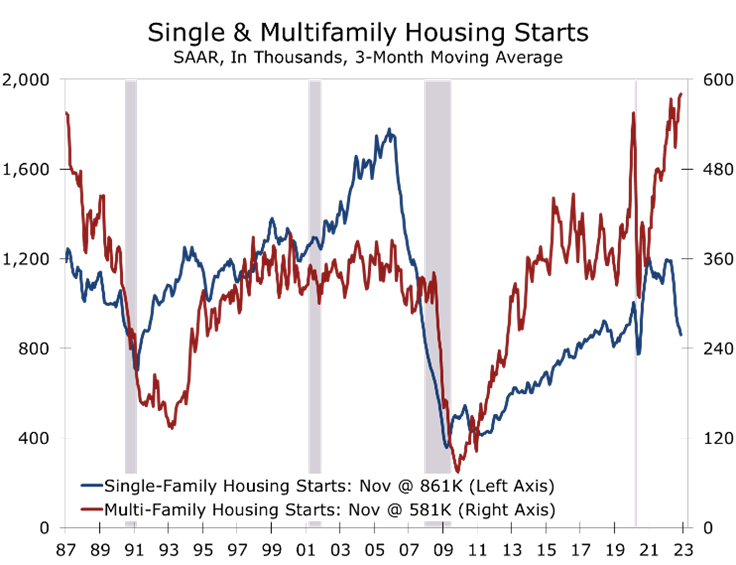

- Housing starts fell 0.5% in November to a still respectable 1.427-million-unit pace, with single-family starts tumbling 4.1% and multi-family starts rising 4.9%.

- Higher mortgage rates continue to weigh on single-family construction, while the threat of tighter lending conditions continues to fuel a rush of apartment starts.

- Housing permits fell a much larger 11.2% to a 1.342-million-unit pace. Single-family permits fell 7.1%, while multifamily tumbled 16.4% Permits fell sharply in every region except the Northeast.

- Completions jumped 10.8% in November to a 1.49-million-unit pace, rebounding from storm-related distortions that sharply reduced completions the prior month.

- Builders continue to work down their backlog of single-family projects, while the mountain of apartment projects under construction continues to increase.

Housing starts declined only marginally in November, with declines in single-family starts offset by continued gains in apartment construction. Overall starts fell 0.5% in November to a 1.427-million-unit pace. Single-family starts fell 4.1% to an 828,000-unit pace, while multi-family starts rose 4.9% to a 599,000 unit-pace. The latter was driven mostly by apartment starts, where developers are likely trying to keep a step ahead of rising interest rates and tightening credit.

Permits, which tend to provide a more consistent read on the housing market, fell 11.2% in November, with single-family permits falling 7.1% and multi-family permits tumbling 16.4%. Permits fell in every region except the Northeast in November, where they rose 1.8%. Permits fell 16.4% in the West, 12.2% in the South and 6.2% in the Midwest.

While there were few surprises in November housing starts, the underlying details provide a good idea of how far along the housing correction is. Overall starts are down 16.4% from last November, with single-family starts down a whopping 32.1% and multi-family starts remaining 23.2% higher than their year ago level.

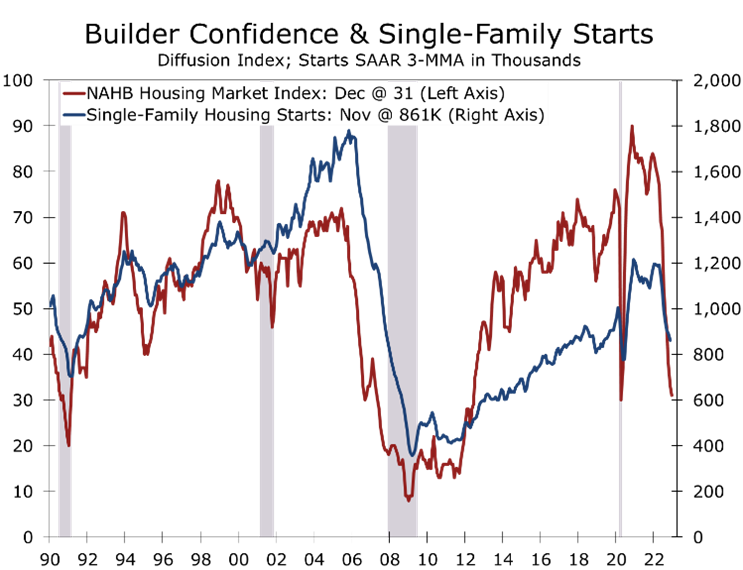

Single-family and multi-family starts are clearly in different places today. Potential single-family buyers face some of the greatest affordability hurdles ever, with rising interest rates compounding the challenge from the previous run-up in home prices. Builders have reported a sharp falloff in prospective buyer traffic, with the NAHB/Wells Fargo Home Market Index (HMI) falling 2 points to 31 in December. A reading below 50 means more builders rate the housing market as bad than rate it as good. The HMI has fallen every month this year, although the pace of decline has moderated somewhat in recent months.

While the single-family starts are clearly under pressure, apartment developers appear to be in a race to get projects started before interest rates rise even higher or the credit window closes. Apartment demand has slowed the past few months, with absorption cooling off, following a surge in demand when the economy reopened from the pandemic and workers began to return to the office.

Multi-family starts rose 4.9% in November to a 599,000-unit pace. Nearly all that increase was in projects with 5 or more units, which is mostly apartments. The strength in multi-family starts adds to the extensive backlog of apartments currently under construction. There are currently 932,000 multi-family units under construction, which is the more than any other time since 1974. Part of the backlog reflects continuing problems sourcing labor and key materials, but part also reflects a surge in starts this past year, which now appear a bit overdone in some markets.

The backlog of single-family homes is beginning to come down, although it remains considerable at 777,000 homes. Single-family starts have tumbled 32.1% over the past year, which was from a pace close to peak for this cycle. Builders really began to slash starts once the Fed ramped up the pace of rate hikes around the middle of the year. Supply shortages are also less problematic than they were a year ago.

While home builders have made some progress reducing their backlogs, the environment remains challenging. There was huge spike in cancelations for new home purchases when conventional mortgage rates spiked above 7%. The rate has since moderated to under 6.5%, but many buyers remain on the sidelines. Prospective buyer traffic remains stuck at its lowest level since December 2011 and home builder confidence is back at the low hit at the onset of the pandemic. Builders have responded by cutting prices and buying down mortgage rates.

Housing permits provide some indication of where the market is headed. Single-family permits fell 7.1% in November to a 781,000-unit pace. Multi-family permits tumbled 16.4% in November. Multi-family permits are volatile, however, and it is too soon to tell if they have peaked just yet. Single-family permits are down 10.8% on a year-to-date basis, while multi-family starts are up 14.4%.

The huge backlog of homes under construction will keep builders busy through at the least the first half of 2023. Housing starts are headed much lower, however, and we suspect apartment construction has either peaked or is very close to peaking for the cycle.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.