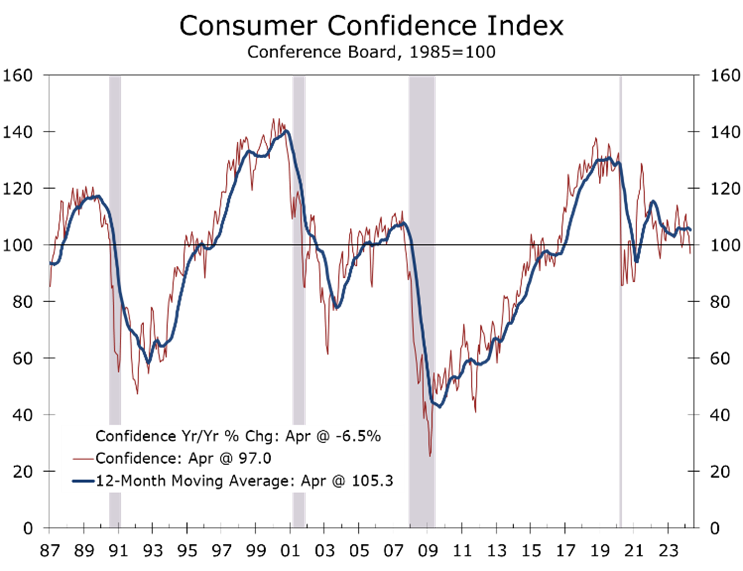

Consumer Confidence Slipped in April

- Consumer Confidence fell a large than expected 6.1 points to 97.0 in April, marking the weakest reading since July 2022.

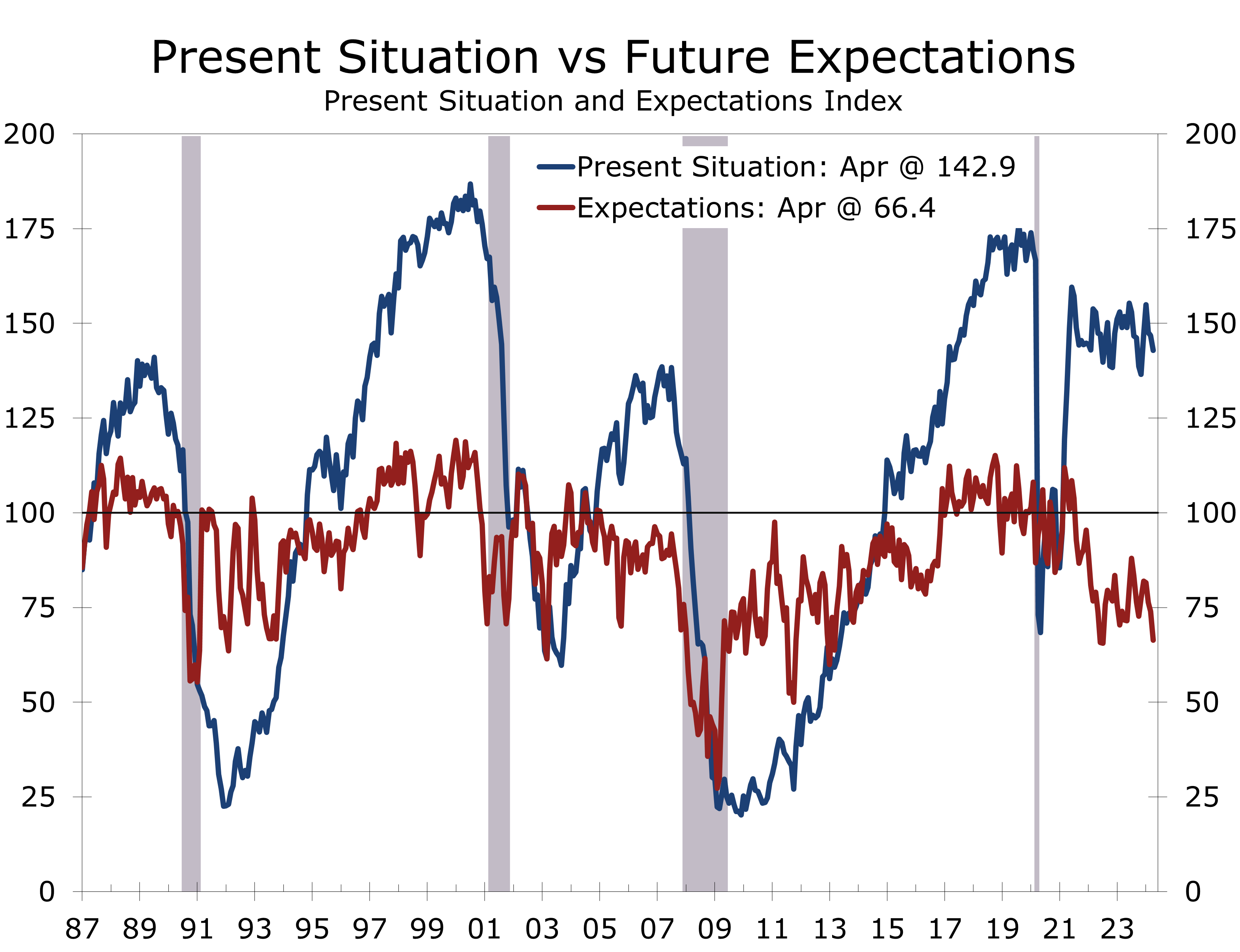

- The Present Situation Index fell 3.9 points to 142.9, while the Expectations Index fell 7.6 points to 66.4, reflecting less optimism about the current labor market and growing caution about future business conditions, job availability, and income growth.

- Confidence declined across all age groups and most income brackets and geographies.

- Higher prices, particularly for gasoline and food, remain a top concern, leading many households to curb discretionary spending to offset increased spending on necessities.

- Buying plans for homes and light vehicles continued to weaken.

- April’s weaker Consumer Confidence report adds to the growing discussion of stagflation. Consumer do not appear to be fearing a repeat of the 1970s, however. We may see a low altitude stagflation. Job and income growth will moderate, while inflation remains persistently high. This backdrop will make it difficult for the Fed to lower rates this year.

In April, The Conference Board’s Consumer Confidence Index plummeted by 6.1 points to 97.0, reaching its lowest point since July 2022. This marks the third consecutive monthly decline, with March’s data also being revised downward. Falling below the 100 mark is significant and historically indicates challenges for incumbent presidents seeking re-election.

Consumer Confidence have tumbled 13.9 points over the past three months. The period has been marked by a gradual reversal of the optimism that dominated the markets following the December FOMC meeting, when the Fed strongly hinted that they were finished raising interest rates and would likely cut the federal funds rate in 2024. Hopes for a rate cut have faded as job growth has come in much stronger than expected and wages and inflation have proven more resilient.

Consumer Confidence dipped below 100 for only the fourth time in the past three years.

With the latest drop, consumer confidence is now at the lower end of the range that it has maintain over the past two years. Falling below the 100 benchmark level is psychologically significant. Incumbent presidents have generally lost their re-election bids if Consumer Confidence was below 100 on election day. Confidence appears to be weighed down by lingering frustration about higher inflation.

Consumers’ assessment of the present economic situation fell 3.9 points in April to a still robust 142.9. This strong assessment makes sense give the recent strength in retail sales and job growth. The present situation index consists of two questions: how do you rate current business conditions and are jobs plentiful or hard to get? Business conditions improved slightly, with the share of consumers rating conditions as ‘good’ rising 1.4 points to 20.6, and the share rating conditions as bad falling 0.2 points to 17.4.

Views on the labor market were decidedly less upbeat. The share stating ‘jobs were plentiful’ fell 1.5 points to 40.2 and follows a 1.2-point drop in March. The share stating jobs were ‘hard to get’ rose 2.7 points to 14.9. The labor market differential, the difference between the two, fell 4.2 points to 25.3. This drop may tamp down expectations for Friday’s employment report.

Expectations have weakened decisively, reflecting concerns about persistent inflation.

The expectations series fell decisively, tumbling 7.6 points to 66.4 in April. The share of consumers expecting business conditions to improve over the next six months fell 1.5 points to 12.8, while the share looking for conditions to worsen rose 1.4 points to 19.9. The share expecting more jobs to be created over the next six months and share expecting their incomes to increase both declined meaningfully as well.

The Conference Board’s tally of write-in responses noted ‘elevated price levels, especially for food and gas’ dominated consumers’ concerns. Politics and global conflicts were ‘distant runners up’. Consumers assessment of their family’s current and future financial situation both deteriorated in April.

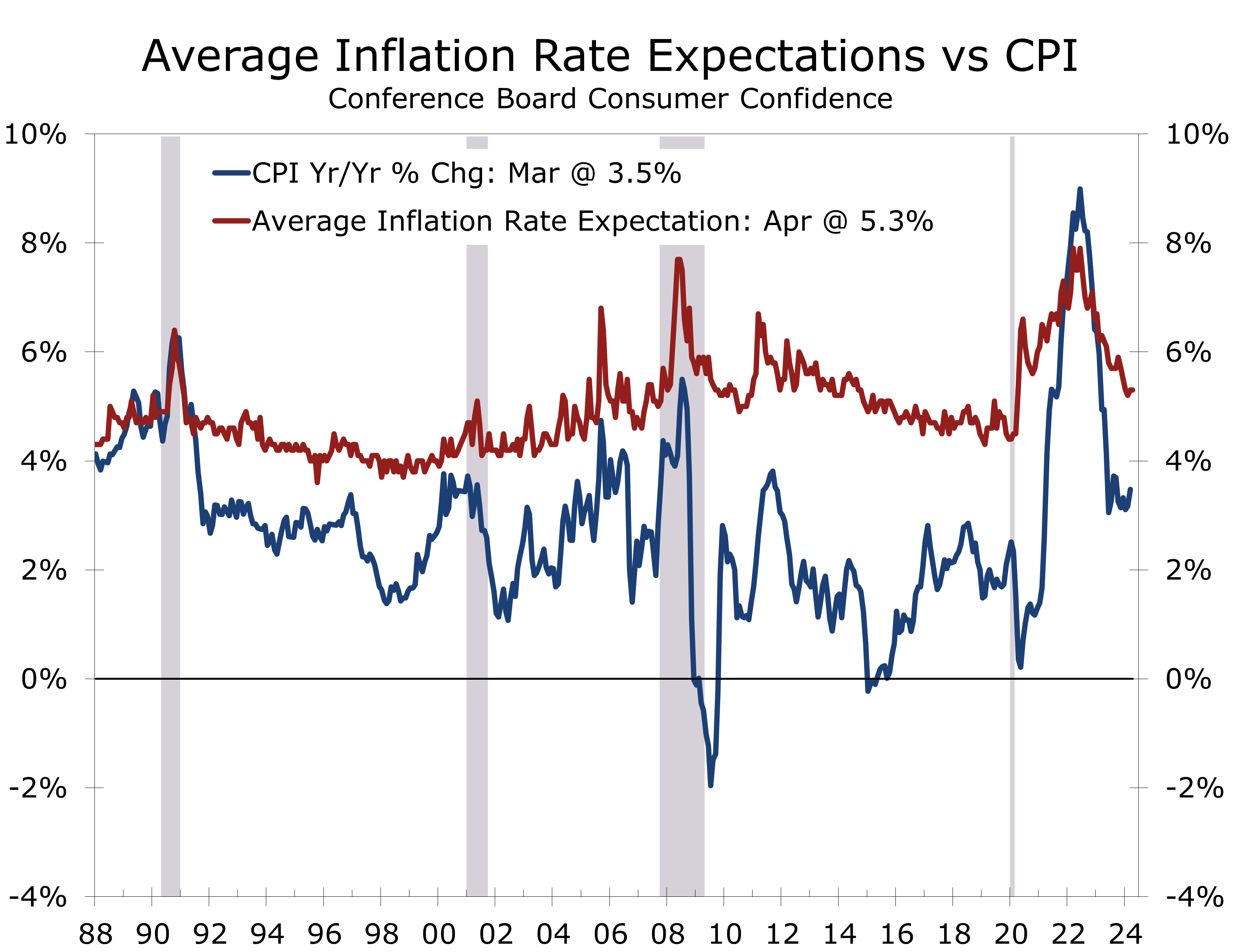

Expectations for inflation over the next 12 months were unchanged at 5.3%. Moreover, the proportion of consumers expecting interest rates to increase over the next year edged higher to 53.8, while the share expect the stock market to rise over the next year fell 1.5 points to 12.8, sliding to its lowest share since March 2009. The cutoff date for the survey was August 24.

Pinched household finances are causing consumers to pull back on interest-rate sensitive purchases. The proportion of consumers planning to buy a home in the next six months fell 1.5 points to 2.5, while the share expecting to purchase a light vehicle fell 0.5 points to 2.2. Consumers also plan to reduce spending for discretionary goods and services, such as dining out (44.8%), clothing (31.5%), entertainment away from home (30.7%), and vacations (23.3%), according to a special survey question ask by the Conference Board.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

April 30, 2024

Mark P. Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

Chief Economist (704) 458-4000