Find a Way to Balance Rising Risks at Both Ends of the Mandate

- Decision: The Federal Reserve cut the target range for the federal funds rate by 25 bps to 3.75–4.00%, marking a second consecutive reduction as policymakers sought to buffer a cooling labor market and maintain financial stability.

• Liquidity Management: The Fed announced it will halt balance sheet runoff on December 1 and begin reinvesting proceeds from maturing MBS into Treasury bills, effectively restarting limited Treasury purchases to preserve market liquidity.

• Tone: The statement acknowledged that “downside risks to employment rose in recent months,” while inflation “remains somewhat elevated.”

• Context: The decision was complicated by the federal government shutdown, which limited access to official data and forced reliance on private-sector indicators.

• Dissents: Governor Stephen Miran favored a 50 bp cut; Kansas City Fed President Jeffrey Schmid preferred no change. The split underscores the uncertainty about how much economic activity and job growth have slowed and how much more tariffs will add to headline inflation.

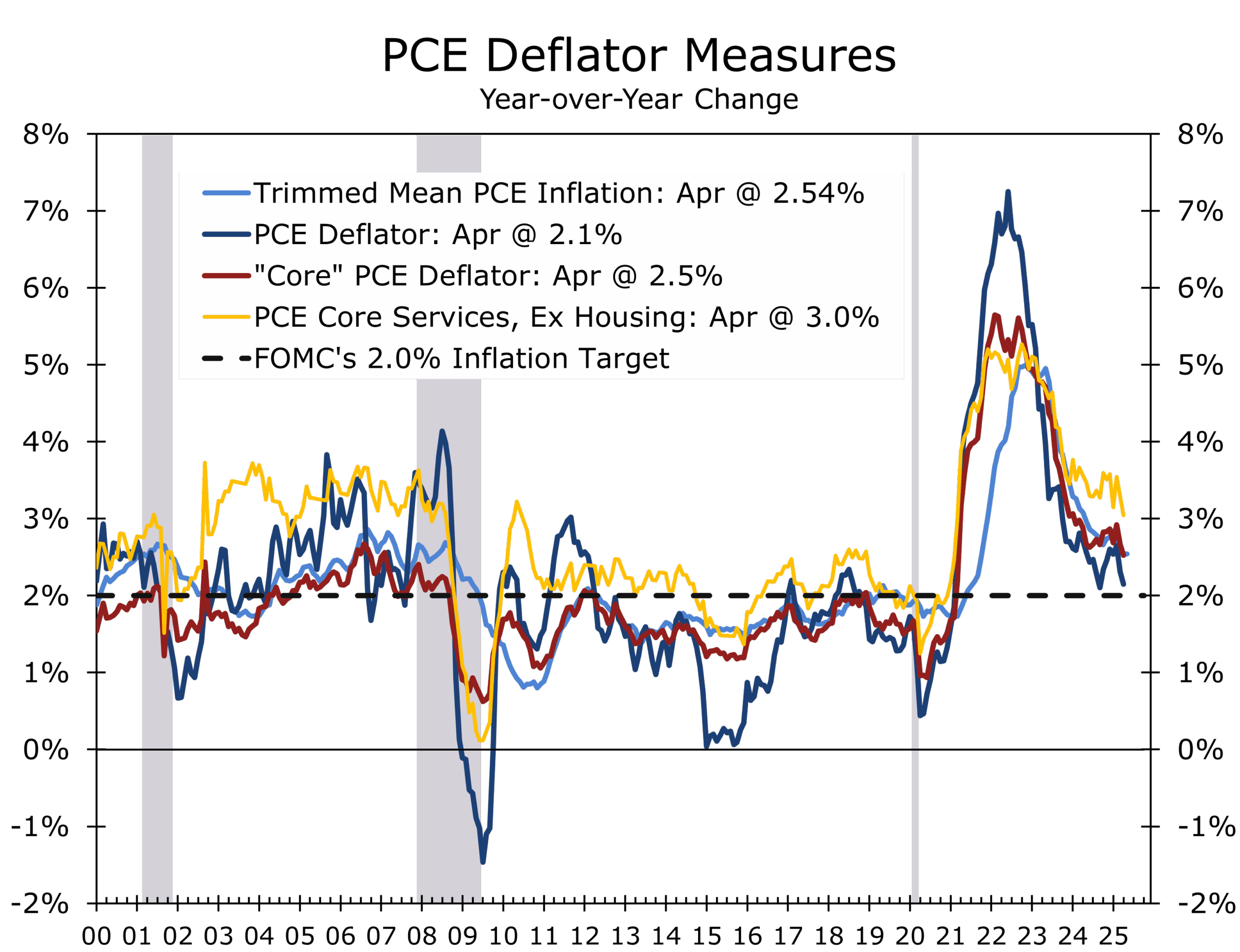

• PCC View: We expect quarter-point cuts in both December and January, with the funds rate bottoming at 3.125% in Q1. The Fed may opt to skip a meeting, however, which would extend the duration of the easing cycle but not the depth. While headline inflation remains “elevated, the core PCE deflator should end 2026 near 2.5%, down from around 3% this year.

Policy Decision and Statement

The Federal Reserve lowered the federal funds rate by 25 basis points to 3.75–4.00%, citing a “shift in the balance of risks” toward weaker employment. The statement described economic activity as expanding at a “moderate pace,” but noted that job gains have slowed and the unemployment rate has edged higher.

Inflation was said to have “moved up since earlier in the year and remains somewhat elevated,” language suggesting concern about price stickiness but confidence that inflation pressures will subside over time. The Committee acknowledged elevated uncertainty and reaffirmed it would “carefully assess incoming data” ahead of any further adjustments.

The Fed needs to find a way to balance rising risks at both ends of its mandate.

The policy statement also confirmed that the Fed will conclude its balance sheet runoff on December 1, marking the end of quantitative tightening and a shift to full reinvestment of maturing securities, primarily into short-dated Treasuries. This reflects concern about tightening liquidity conditions and the Fed’s longstanding commitment to maintaining “ample reserves.”

The operational shift is a technical but meaningful adjustment. By reinvesting MBS proceeds into Treasury bills, the Fed will maintain the size of its balance sheet while subtly improving liquidity in the front end of the curve..

Recent strains in money markets—compounded by the government shutdown’s disruption of Treasury issuance—prompted the move. Powell and key officials have been explicit that this is not a return to quantitative easing, but rather a precautionary step to stabilize short-term funding markets and prevent another repo-style disruption.

This balance-sheet decision complements the rate cut: one addresses the cost of money; the other ensures the availability of money.

FOMC members will likely have a wider range of forecasts for growth, inflation and rates.

The 10–2 vote revealed the most ideologically divided Committee since the pandemic era.

- Governor Stephen Miran, who again dissented in favor of a 50 bp cut, is effectively playing the role once held by the Vice Chair—serving as the public voice of the Administration and advocating a faster easing pace to support employment.

- Kansas City Fed President Jeffrey Schmid, who voted against any rate cut, reflects the Kansas City Fed’s long-standing hawkish tradition, shaped by its historic focus on price stability and commodity-related inflation risks.

This dual dissent—from opposite ends of the policy spectrum—highlights the Fed’s internal balancing act: navigating slowing job growth without reigniting inflation or appearing politically influenced.

The government shutdown has limited official data, forcing policymakers to rely on alternative sources such as ADP, Homebase, and private job postings, which collectively suggest the labor market is weakening faster than the headline numbers imply.

At the same time, business investment remains firm, supported by AI infrastructure, defense technology, and reshoring of critical manufacturing. These conflicting signals—resilient capital spending versus softening labor demand—make this one of the most complex policy environments of Powell’s tenure.

Inflation from recent tariffs has been milder than anticipated. The Fed now sees price pressures easing back toward target over the next 18 months, assuming no renewed supply disruptions.

Powell’s Press Conference: Themes to Watch

Powell struck a measured, data-dependent tone at his press conference, reinforcing the Fed’s pivot from a rules-based framework to one guided by “discretion, diligence, and destination.”

Key themes:

- Labor risk management: “We cannot declare victory on inflation, but we must acknowledge the emerging risks to employment.”

- Liquidity assurance: Reinvesting MBS into T-bills is about function, not stimulus.

- Data limitations: Powell Stress the difficulty of policymaking amid a statistical blackout. “What do you do when you are driving in a fog? You slow down.”

- December outlook: “Policy is not on a preset course” Powell emphasized this point repeatedly and is keeping his options open while implying that another 25 bp cut remains on the table.

- Neutral Rate and the next move: We are now back in the range of where most FOMC participants believe the neutral funds rate is. “There is a growing course that maybe we should wait a cycle.”

- Equity Markets: “We do look at any particular asset, we look at the overall financial system and ask whether it can withstand a shock.”

- The AI Boom: It is different from the 1980s. The companies driving the boom are earning money. These are investment not just ideas.

Piedmont Crescent Capital’s baseline scenario now assumes:

- We still see two additional 25 bp cuts — most likely in December January — bringing the funds rate to a cycle low of 3.125% in Q1 2026. The markets are pricing in less than that, with the 2-Year Treasury rising to 3.59%—essentially pricing in one more cut by the middle of next year.

- Core PCE inflation ending 2025 at around 2.5%, down from 3% this year, as supply normalization and tighter credit cool demand.

- The Fed may opt to skip a meeting and wait for more hard data on inflation and employment. That would essentially extend the duration of the easing cycle without making it any deeper.

- We see the long-run neutral rate around 3% but it is likely edging higher as the buildout of AI infrastructure boosts productivity and long-run potential growth.

We see the Fed nearing the end of its easing cycle, shifting from active accommodation to sustained vigilance. Cutting rates while headline inflation remains “elevated” demands precise messaging. Lower short-term rates and a stable balance sheet should gradually support credit-sensitive sectors in early 2026, fostering a modest pickup in activity without reigniting inflation. If markets perceive the Fed as easing too aggressively, however, long-term yields could rise and offset much of the intended benefit.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 29, 2025

Mark Vitner, Chief Economist

704-458-4000