A Hawkish Quarter Point Cut in December

- The Dow Jones Industrial Average sold off 1,123 points following the Fed’s interest rate decision and Powell’s press conference.

- The FOMC lowered its target range for the federal funds rate by 25 basis points (bps) to 4.25%-4.50%, marking the third consecutive cut since September.

- There were few changes in the Fed’s policy statement, but it now emphasizes the “extent and timing” of additional adjustments, signaling a potential pause and higher endpoint for future rate cuts.

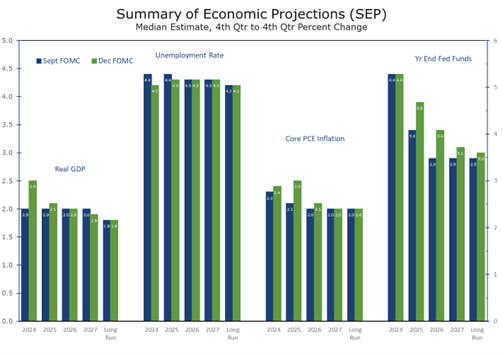

- The December Summary of Economic Projections (SEP) now calls for stronger GDP growth, higher inflation, and a higher federal funds rate in 2025 and 2026.

- The financial markets were clearly put off by the Fed’s policy statement and Powell’s press conference. The stock market sold off sharply, and the yield on the 10-year Treasury surged to 4.52%. The rise in long-term yields reflects reduced expectations for Fed rate cuts and higher expectations for growth and inflation, all of which argue for higher long-term rates.

The Fed’s Federal Open Market Committee (FOMC) cut its federal funds rate target by 25 bps to 4.25%-4.50%, bringing the cumulative reduction to 100 bps since September. While the Fed’s decision was widely expected, changes to the language in the policy statement and Summary of Economic Projects revealed a more hawkish shift to monetary policy than had been expected.

Chair Powell characterized the decision as a “closer call” and described the meeting as more contentious than previous ones. Cleveland Fed President Beth Hammack dissented, opposing further rate cuts. Additionally, the “dot plot” indicates that other Federal Reserve Bank presidents might have dissented if they were voting members this year.

The Fed’s policy statement suggests the Fed will slow the pace of rate cuts, with periodic pauses.

Despite the contentious nature of the meeting, the Policy Statement saw minimal changes. The most notable was the addition of the phrase “the extent and timing” when referencing the process for analyzing future rate cuts, signaling the possibility of a pause at the January meeting and fewer cuts ahead.

The Summary of Economic Projections (SEP) reflects expectations for stronger near-term growth, higher inflation, and a slower trajectory for future rate cuts. Additionally, the estimate for the long-run neutral federal funds rate has been slightly increased.

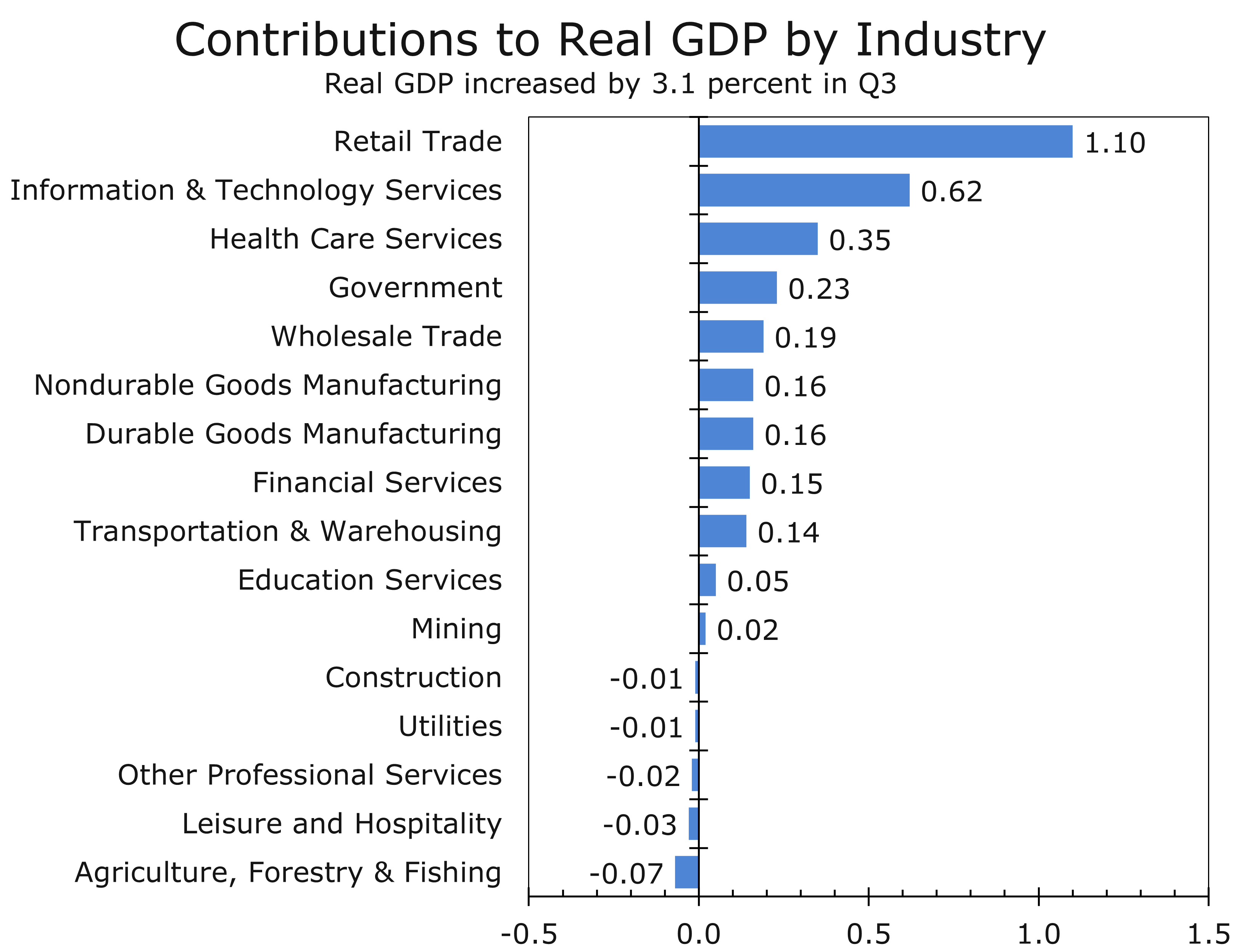

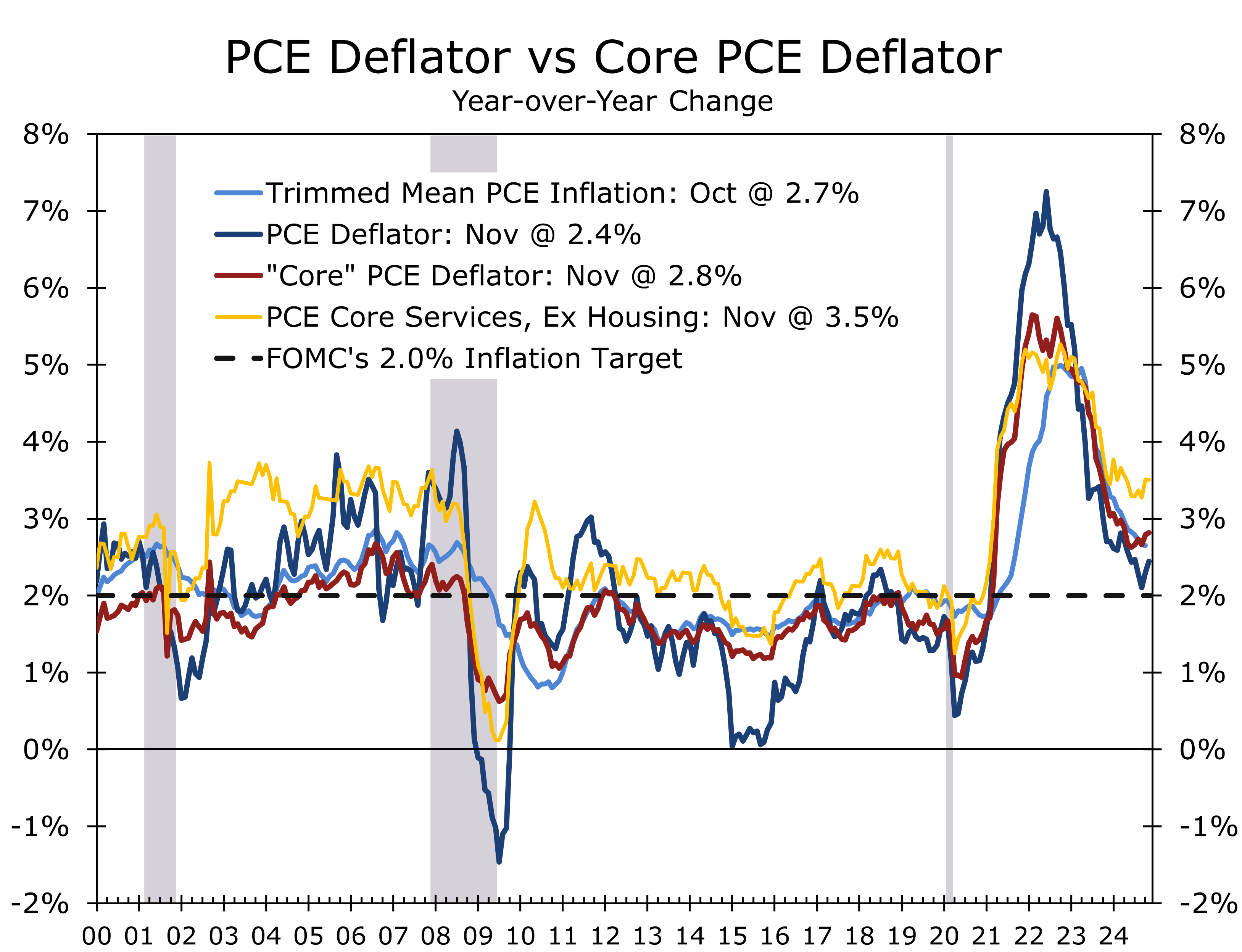

The latest data largely validate the Fed’s actions and Chair Powell’s remarks. Q3 real GDP growth was revised up to 3.1%, and the core PCE deflator, the Fed’s preferred price measure, continues to decelerate. Both the overall and core PCE deflators rose just 0.1% in November. Year-to-year, the overall PCE deflator increased 2.4%, while the core PCE deflator rose 2.8%. Excluding housing, the core PCE deflator is up 3.5%.

The benefits of economic growth are unevenly distributed across industries and sectors.

The strong GDP numbers present a paradox for the Fed. Real GDP has been growing at nearly a 3% pace for the past two years, and the unemployment rate remains near full employment. Why, then, would the Fed need to cut interest rates? The answer lies in the lagged effects of monetary policy. Changes to interest rates today influence the economy 12 to 18 months down the road, when growth is expected to slow, and unemployment is anticipated to rise modestly.

The economic data reveal another paradox: the benefits of economic growth are unevenly distributed. This disparity is evident in GDP by industry, where just 4 categories accounted for nearly three-quarters of Q3 growth. Similarly, the stock market reflects this concentration, with the “Magnificent 7” and their peers generating the bulk of this past year’s surge.

Monetary policy is a blunt instrument, and the Federal Reserve has limited ability to target rate cuts to specific sectors. Construction is a notable weak spot, with overall home sales near the lows of the financial crisis and rising inventories of unsold new homes. Commercial construction also remains under pressure. Lower interest rates would benefit both sectors.

Powell acknowledged that while inflation is declining, prices remain high—particularly for necessities such as food, transportation, and housing. He emphasized that the Fed works for those most affected by these costs, which is why it has adopted a more cautious approach to achieving its 2% inflation target.

Powell stressed that while inflation is slowing, prices for key necessities remain high.

The extended timeline for reaching 2% inflation still leaves room for rate cuts. We expect two quarter-point cuts in the first half of 2025, though the timing remains uncertain. While the Fed may prefer to pause, it may act to avoid provoking President Trump, who takes office just before the January FOMC meeting. Annual revisions to nonfarm payrolls, released a week later, are also expected to reveal weaker prior job growth.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 20, 2024

Mark Vitner, Chief Economist

704-458-4000