Confidence Firms as Labor Slack Deepens

- The Conference Board’s Consumer Confidence Index® rose 2.0 points to 97.2 in July.

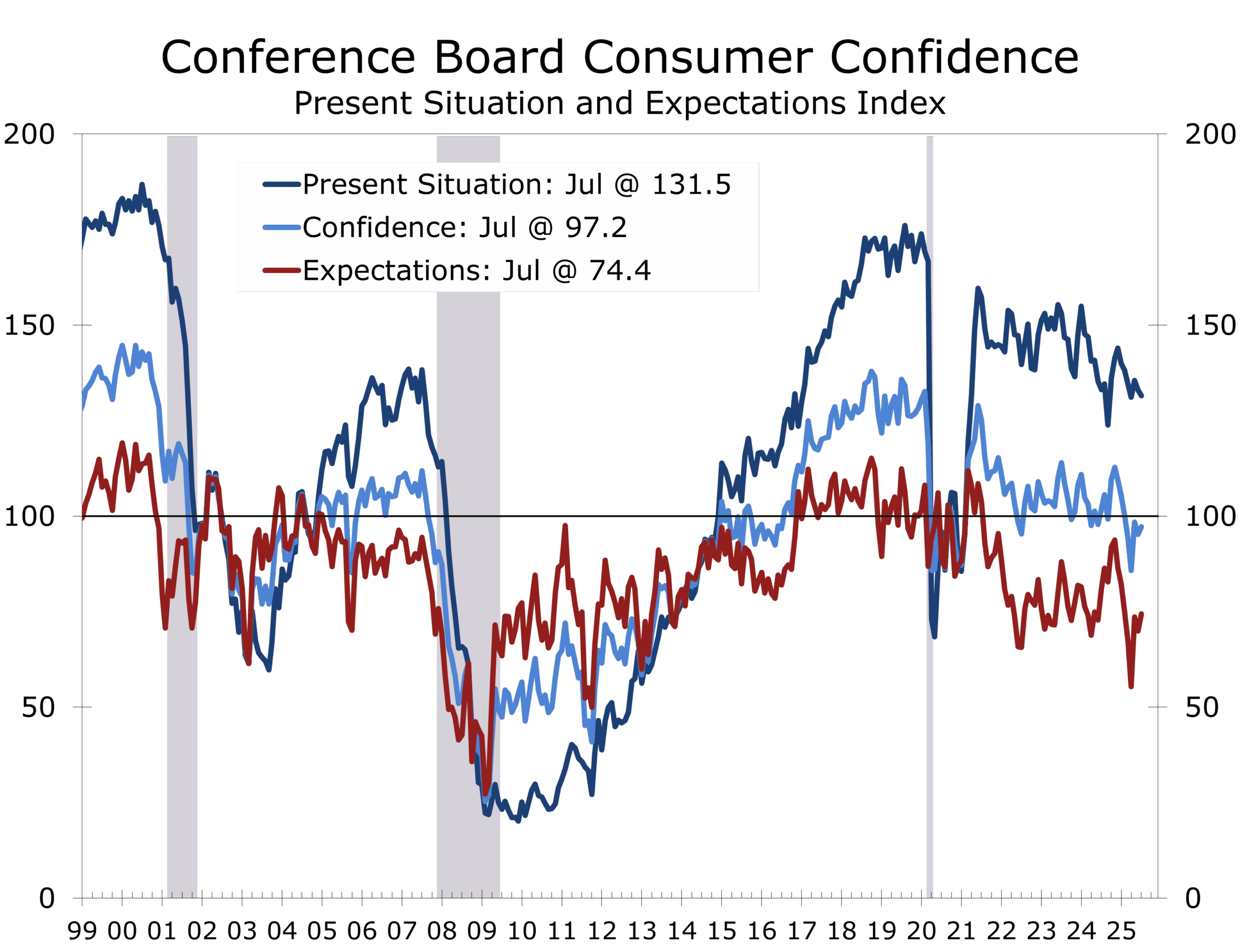

- Consumers’ view of present economic conditions slipped 1.5 points to 131.5, while the Expectations Index rose 4.5 points to 74.4.

- The Expectations Index remained below the key 80 threshold for the sixth straight month—a traditional recession warning signal.

- The July 20 survey cutoff allowed consumers time to digest the “Big Beautiful Bill,” which modestly lifted sentiment among Republican respondents.

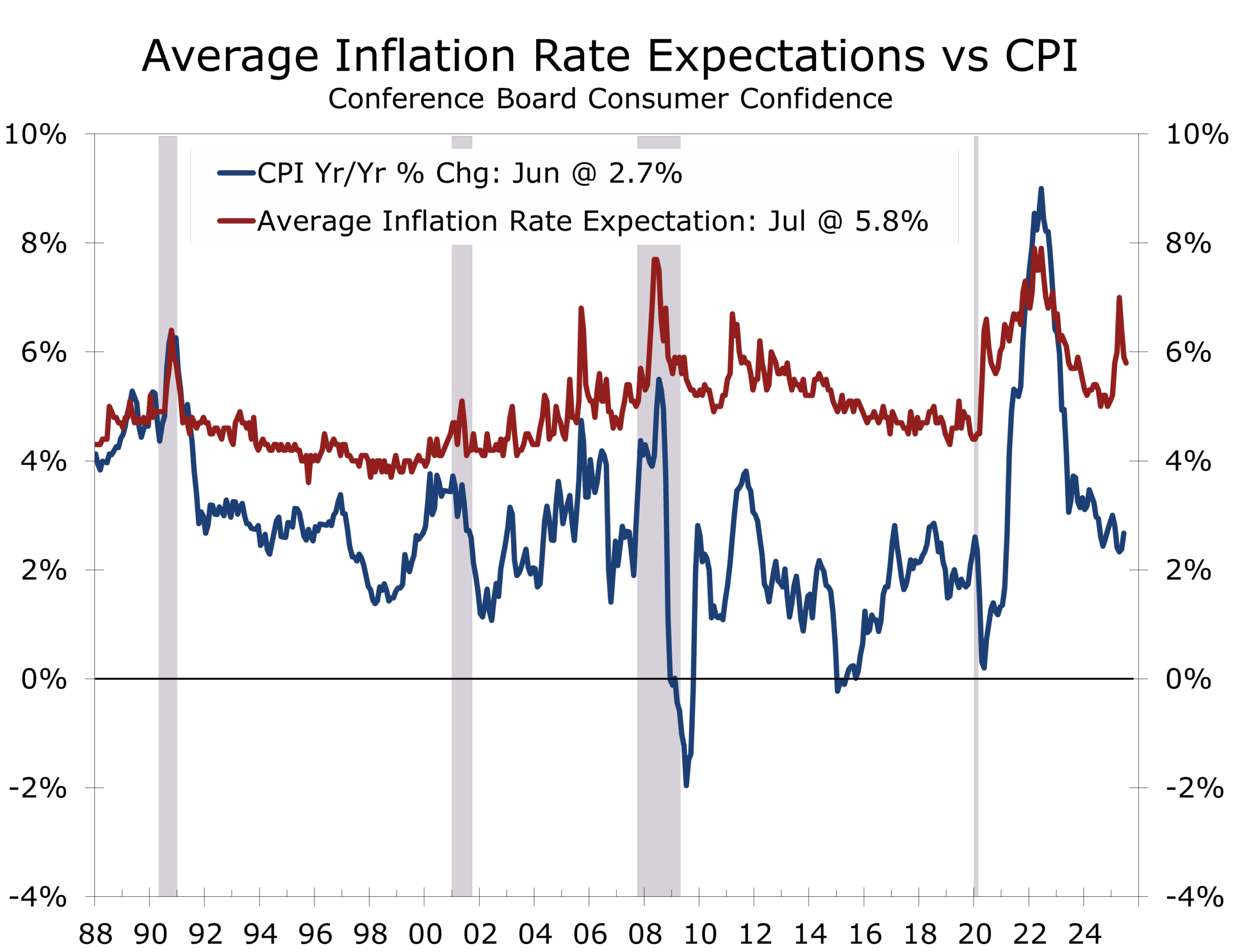

- Tariffs remain top of mind, continuing to stoke inflation fears—even as 12-month expectations eased slightly to 5.8%.

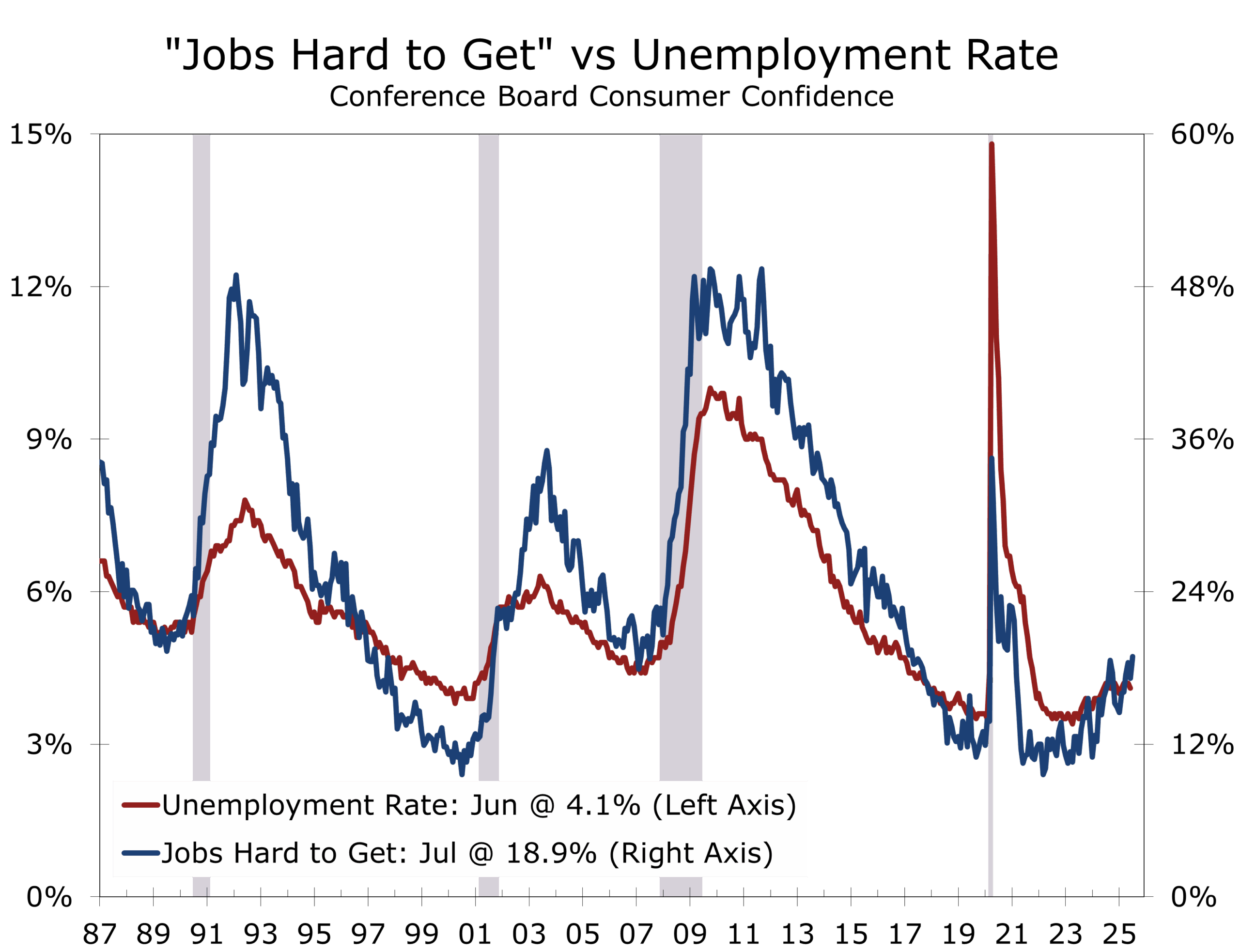

- Labor market concerns are intensifying, particularly among younger workers facing a tightening job market.

- We forecast just 90,000 net new jobs were created in July and expect the unemployment rate to tick up to 4.2%.

The Conference Board’s Consumer Confidence Index® rose 2.0 points in July to 97.2, marking a third straight monthly gain but remaining below the critical 100 level historically associated with strong economic expansion. The Present Situation Index declined 1.5 points to 131.5, while the Expectations Index climbed 4.5 points to 74.4—still under the 80 recession-warning threshold for the sixth consecutive month.

The survey’s cutoff date of July 20 allowed consumers ample time to digest the passage of the budget reconciliation package informally dubbed the “Big Beautiful Bill.” The legislation appeared to bolster sentiment among Republican respondents, while leaving Democrats relatively unmoved. Still, the bill did not rank high among consumer concerns, and few viewed it as a decisive factor shaping their economic outlook.

Tariffs, however, remain top of mind. Consumers continue to associate tariffs with higher prices, reinforcing concerns about persistent inflation. That said, the absence of a renewed inflation surge—despite the hectic pace of trade negotiations and announcements—has begun to shift perceptions. Inflation expectations edged down to 5.8% in July, a modest improvement from the 7% peak in April.

The labor market outlook continues to deteriorate. Although 30.2% of consumers still say jobs are “plentiful,” a growing 18.9% say jobs are “hard to get”—the highest reading since March 2021. The labor market differential has narrowed to just 11.3, suggesting growing concern about job availability. Notably, younger workers appear to be bearing the brunt of this shift, as firms scale back entry-level hiring. These trends support our call for just 90,000 net new jobs in July and rise in the unemployment rate to 4.2%.

While overall sentiment improved modestly, consumers earning under $15,000 reported no gains in confidence—underscoring how the hiring slowdown, inflation, rising borrowing costs are disproportionately burdening the most vulnerable households. Write-in responses revealed that tariffs remain closely tied to inflation fears, while concerns about rising credit card interest rates grew more prominent in July.

Confidence is eroding most among younger households worried about jobs and expenses.

Equity market sentiment offered a partial offset but likely to upper income households. The share of consumers expecting stock prices to rise climbed to 47.9% in July, rebounding from a 16-month low in April. This optimism, however, has not translated into stronger spending plans. Purchasing intentions for big-ticket items like appliances and vehicles remain mixed, and domestic vacation plans continued to decline—even as international travel interest ticked higher.

Spending intentions are beginning to fray. Plans to purchase cars and homes slipped modestly, though longer-term trends remain flat. Consumers’ appetite for discretionary services weakened for a second consecutive month. Dining out, travel, and lodging—previous mainstays of post-pandemic spending—saw the steepest pullbacks. Vacation intentions declined overall, with more consumers looking abroad while domestic travel plans fell.

Despite the modest headline gain in confidence, the narrowing of the gap between current and expected conditions continues to reflect a softening baseline. The number of respondents expecting a recession over the next 12 months ticked lower but remains elevated compared to pre-2024 levels.

The slight rise in confidence reflects growing unease—not growing optimism.

Consumers appear to be cautiously recalibrating their expectations following what now looks like irrational fears about tariffs. Few are confident enough to spend freely. The prevailing mood is one of restraint, shaped by uncertainty over jobs, prices, and interest rates.

Consumer confidence edged up in July, but recession risks remain embedded in the data. Tariff-driven price fears linger, even as inflation expectations ease. The labor market is cooling more visibly, with younger workers feeling the pinch first. While Republican-leaning respondents saw a confidence boost following the “Big Beautiful Bill,” broad-based concerns over inflation, jobs, and political uncertainty remain. The Fed is likely to take these mixed signals seriously as it prepares for a potential pivot in September, with three or four quarter-point cuts by spring 2026.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 29, 2025

Mark Vitner, Chief Economist

(704) 458-4000