Economic Growth Once Again Tops Expectations

- Real GDP grew at a 3.3% annual rate in the fourth quarter, easily topping expectations that were centered around a 2% pace.

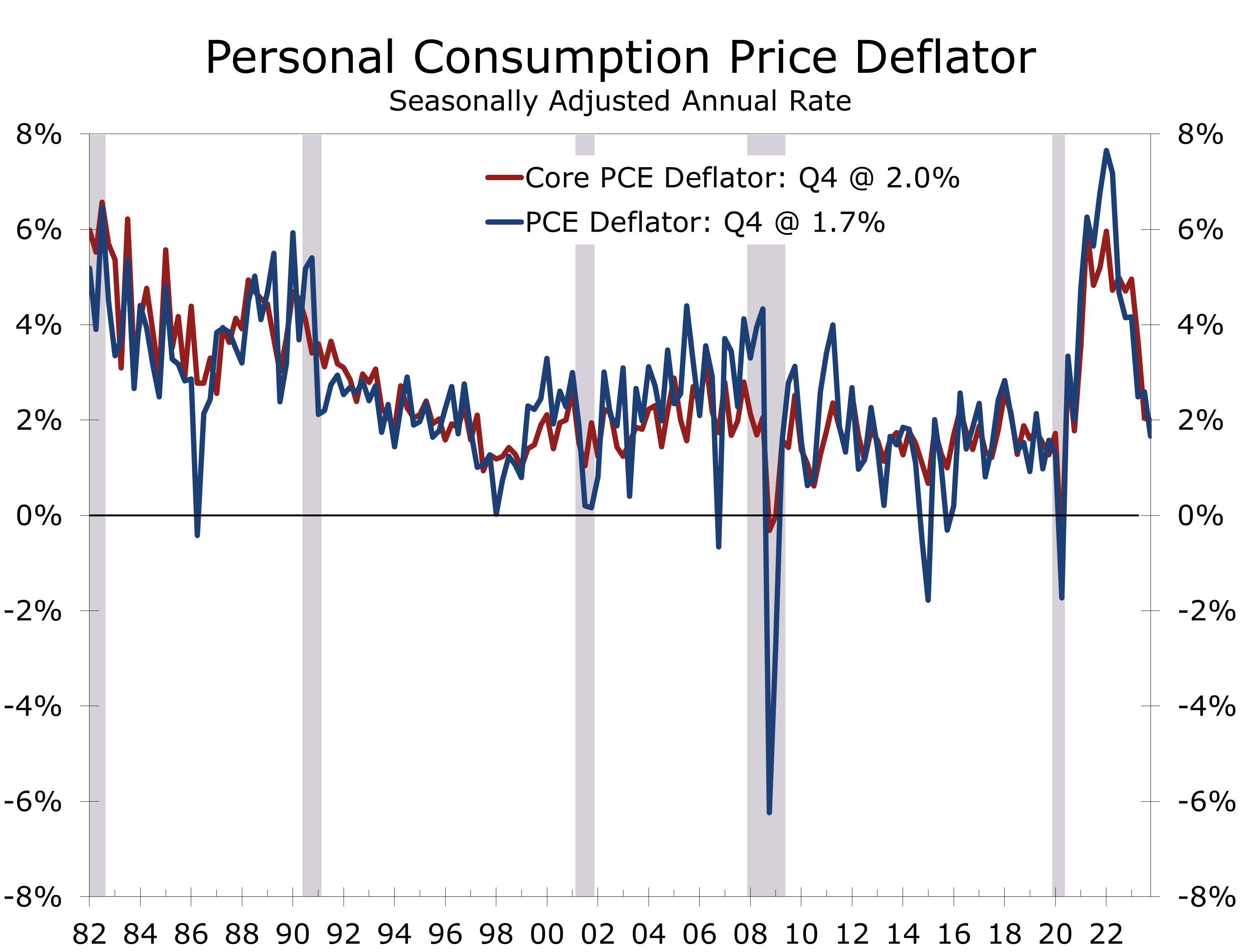

- While growth topped expectations, inflation came in lower, with the core PCE deflator rising at a 2% annual rate in Q4.

- Q4 growth was solid, with consumer spending rising at a 2.8% pace and business fixed investment climbing at a 1.7% pace.

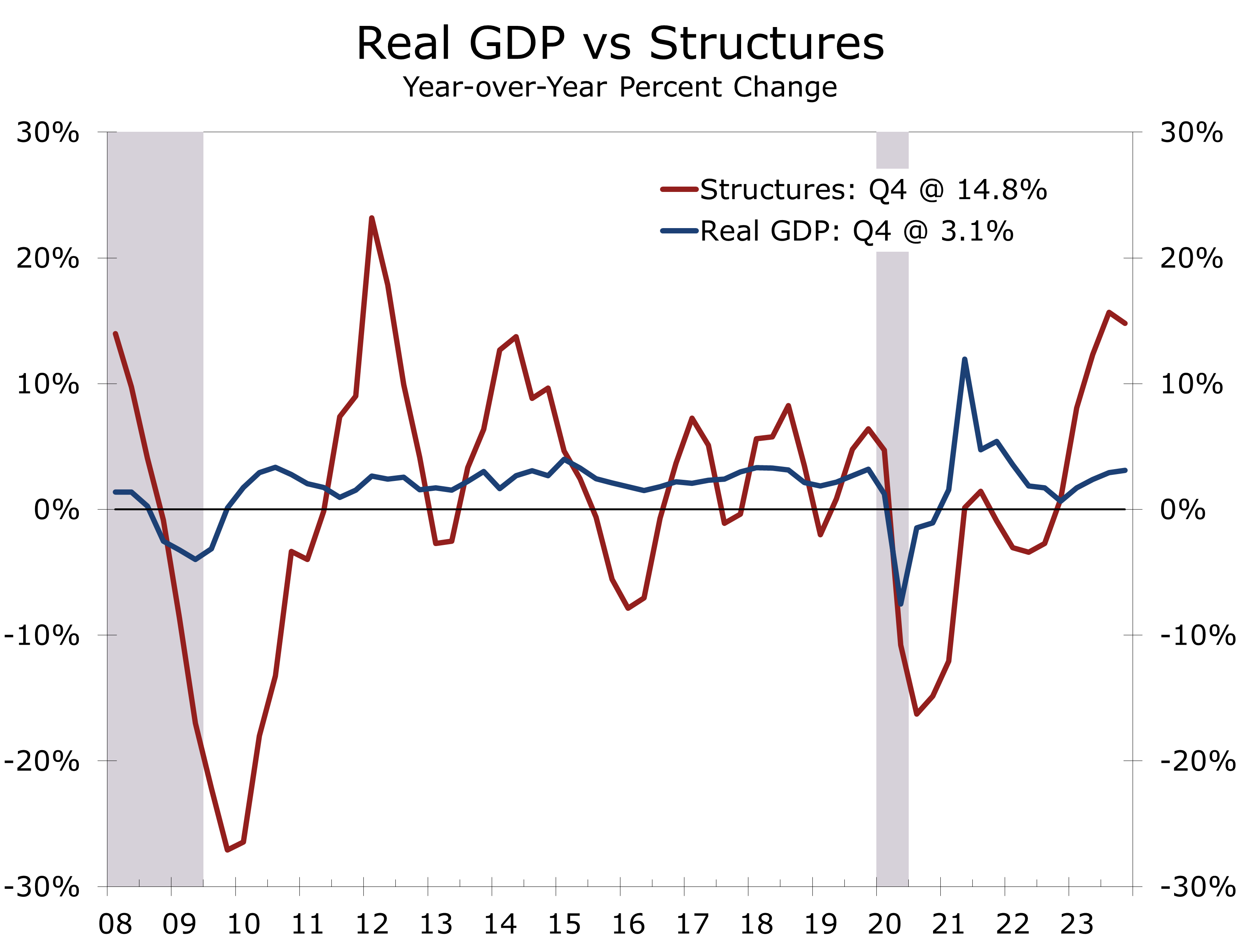

- Both nonresidential and residential construction rose, climbing at a 3.2% and 1.1% pace, respectively. The gain reflects the large pipeline of projects underway.

- International trade was a major surprise, with a narrowing trade deficit adding 0.4 percentage points to Q4 GDP growth.

- Inventories came in stronger than expected, adding 0.1 percentage point to headline GDP growth.

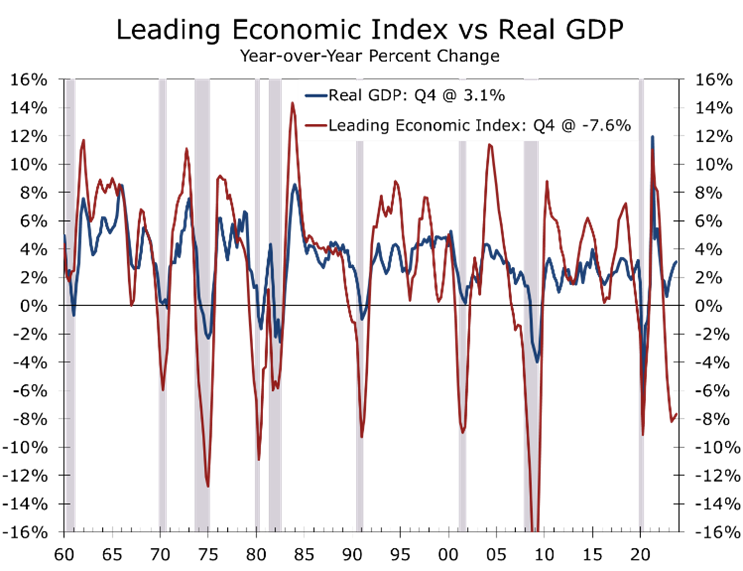

- Economic growth continues to come in well above expectations, defying an anticipated slowdown indicated by measures like the Leading Economic Index. The unexpected strength is likely due to lingering stimulus and the still historic construction backlog of factories, apartments, and homes.

The economy ended the year on a strong note. Real GDP grew at an impressive 3.3% annual rate during the fourth quarter, easily surpassing market expectations that were centered around 2%. Growth was broad based, with every major component posting gains. The strength remains at odds with other leading and coincident measures of economic activity, including the Leading Economic Index and the ISM surveys.

Consumer spending rose at a 2.8% pace in Q4. Durable goods outlays particularly stood out, surging at a 4.6% annual rate, while nondurables climbed at a 3.4% pace. The strength in durable goods is surprising, considering the lingering effects of the United Auto Workers Strike depressed sales of cars and SUVs. All of the growth in durables came outside the automotive sector.

Spending on nondurable goods was fueled by outlays for pharmaceuticals and might reflect demand for new appetite suppression drugs. Continued growth in travel and leisure and a rebound in health care outlays drove growth in services.

The strength in GDP appears at odds with other key measures of aggregate economic activity.

The Conference Board’s Leading Economic Index has declined for 21 straight months, and both the ISM manufacturing and services surveys for December were weaker than expected. This divergence between these key measures is unusual is one reason why consensus estimates for Q4 GDP were so low.

The gap between real GDP growth and other economic indicators likely stems from volatile shifts during the Pandemic. The sudden reopening post-vaccines disrupted supply chains, inflating the Leading Economic Index and ISM surveys. Now that supply chains are normalizing, the decrease in order backlogs and faster deliveries are exaggerating the slowdown.

While growth is moderating, there is still plenty of stimulus in the pipeline. Real GDP grew 3.1% on a fourth quarter to fourth quarter basis, led by a 4.3% spike in government outlays. Most of that was at state and local governments, which continue to benefit from the American Rescue Plan. Hiring at state and local government has also increased, as public schools, universities and municipalities look to replace workers displaced during the pandemic.

Stimulus is also spurring growth in nonresidential construction, particularly new manufacturing facilities. The Inflation Reduction Act and CHIPS and Science Act are driving construction of EV and microchip plants nationwide, leading to a 14.8% surge in nonresidential structures outlays this past year.

Investment outlays grew at a more modest 1.7% pace in Q4, with the AI boom lifting investment in software and IT equipment. Purchases of transportation equipment were a notable soft spot, reflecting some hangover from the UAW strike as well as last year’s slowdown in transportation and shipping.

International trade and inventories were positive surprises in Q4. The narrower trade gap contributed 0.4 percentage points to growth, fueled by a 6.3% rebound in exports and a 1.9% rise in imports. Given the weakness in global growth, particularly in Europe, Q4 exports might have been bolstered by supply chain issues resulting from the Red Sea shipping disruptions.

Inventories rose slightly in Q4, adding 0.1 percentage point to growth. Inventories were expected to subtract 0.1 percentage point from Q4 growth.

While economic growth exceeded expectations, inflation came in on the low side. The price index for gross domestic purchases rose at a 1.9% annual rate in Q4, down from 2.9% in the prior quarter. The core PCE deflator rose at a 2.0% pace, the same as in Q3. The subdued inflation data more than offset concerns that Q4 economic growth came in ahead of expectations.

Private sales to domestic purchasers, rose at a slightly less robust 2.6% pace in Q4, and rose just 1.8% in 2023, down from 2.3% the prior year. This is the part of the economy monetary policy has the most sway over and the moderation is a big reason inflation cooled off as much as it did this past year.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.