A Conflict of Visions: Growth, Credibility, and the Political Clock

- The expansion remains intact, but its composition continues to shift. January brought solid job gains, firmer manufacturing surveys, and housing starts that ended 2025 stronger than expected. Existing home sales weakened in January, however, reflecting tight inventories and the return of harsh winter weather.

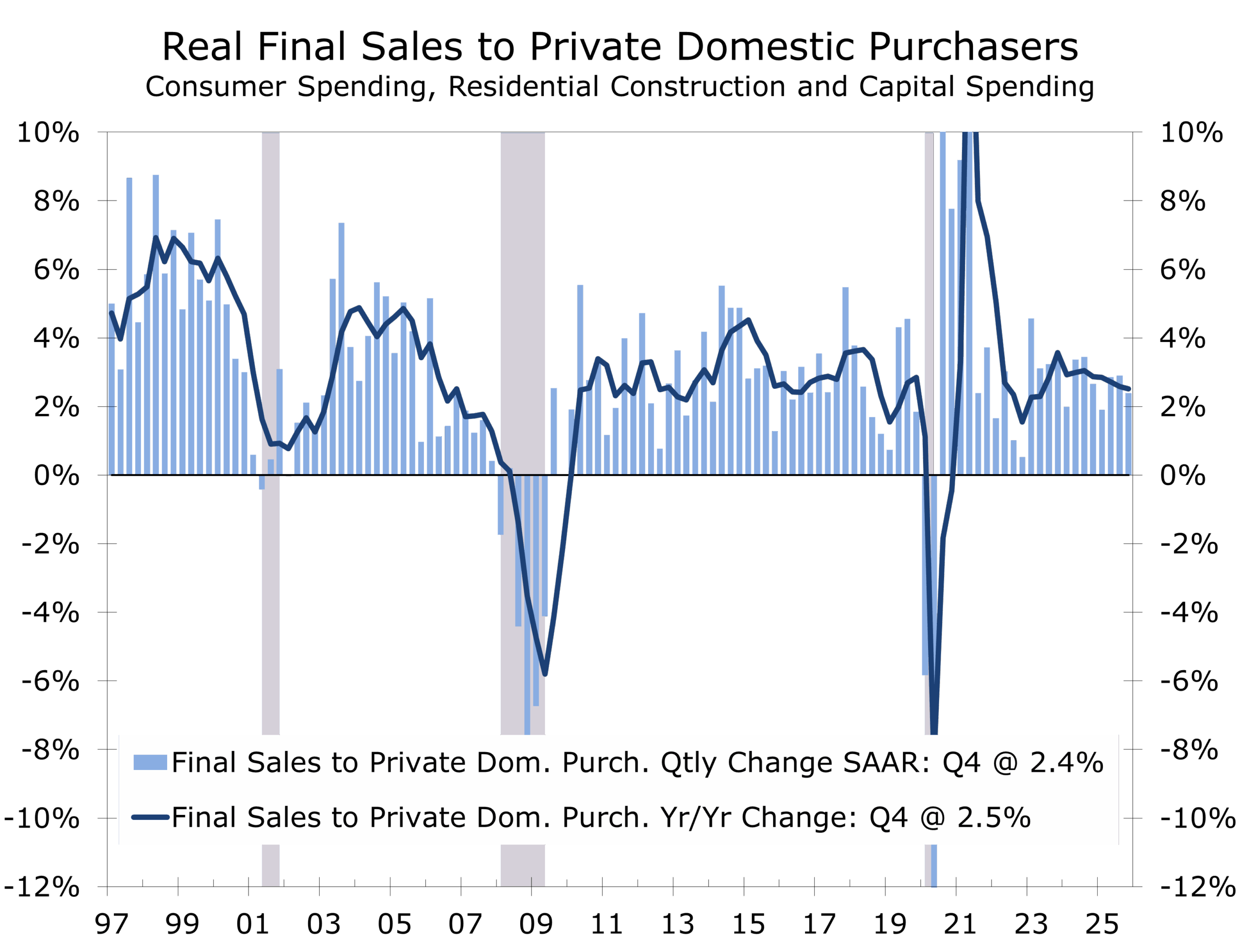

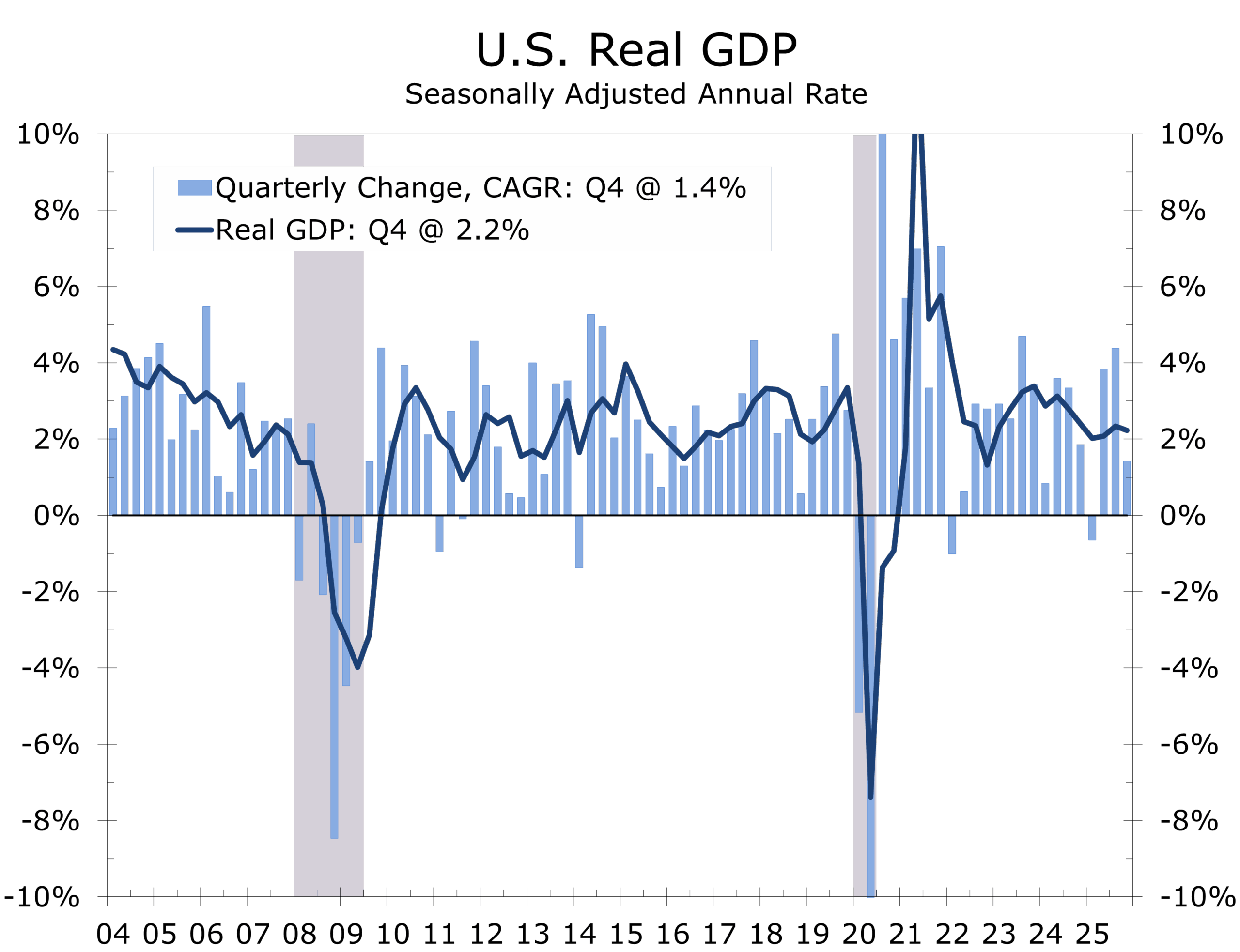

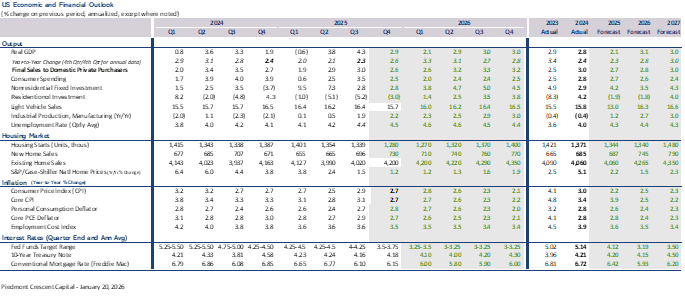

- Q4 GDP resets expectations. Headline growth came in at a 1.4% annualized pace, well below the 3.0% consensus and our 2.8% call. Composition matters more than the headline: the shortfall stemmed largely from a larger-than-expected 1.2-percentage-point hit from the federal government shutdown. Private final domestic demand rose 2.4%, matching our estimate. Advance data put 2025 GDP growth at 2.2%, down from 2.8% in 2024; private final domestic demand grew 2.7% in 2025, down from 3.1% the prior year.

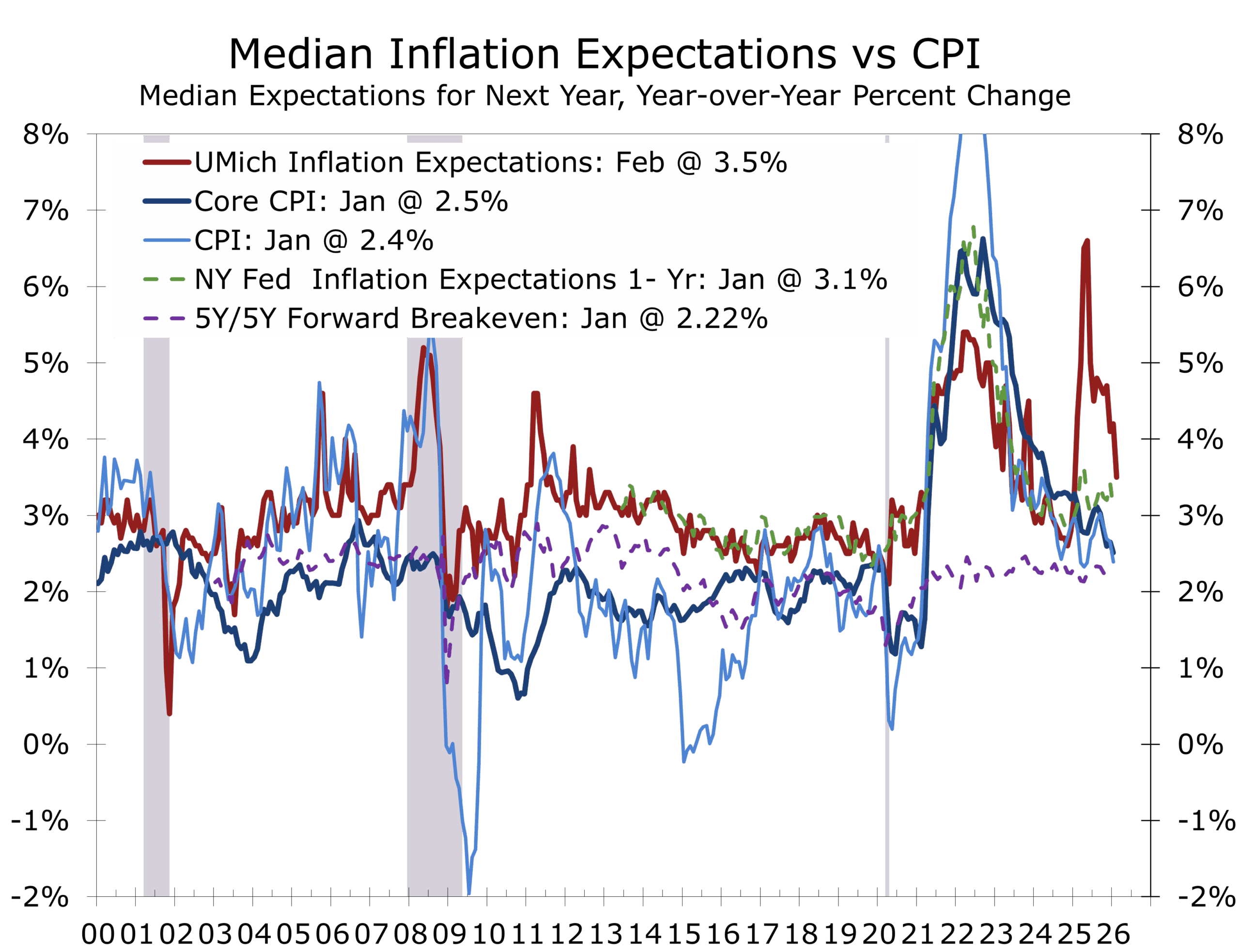

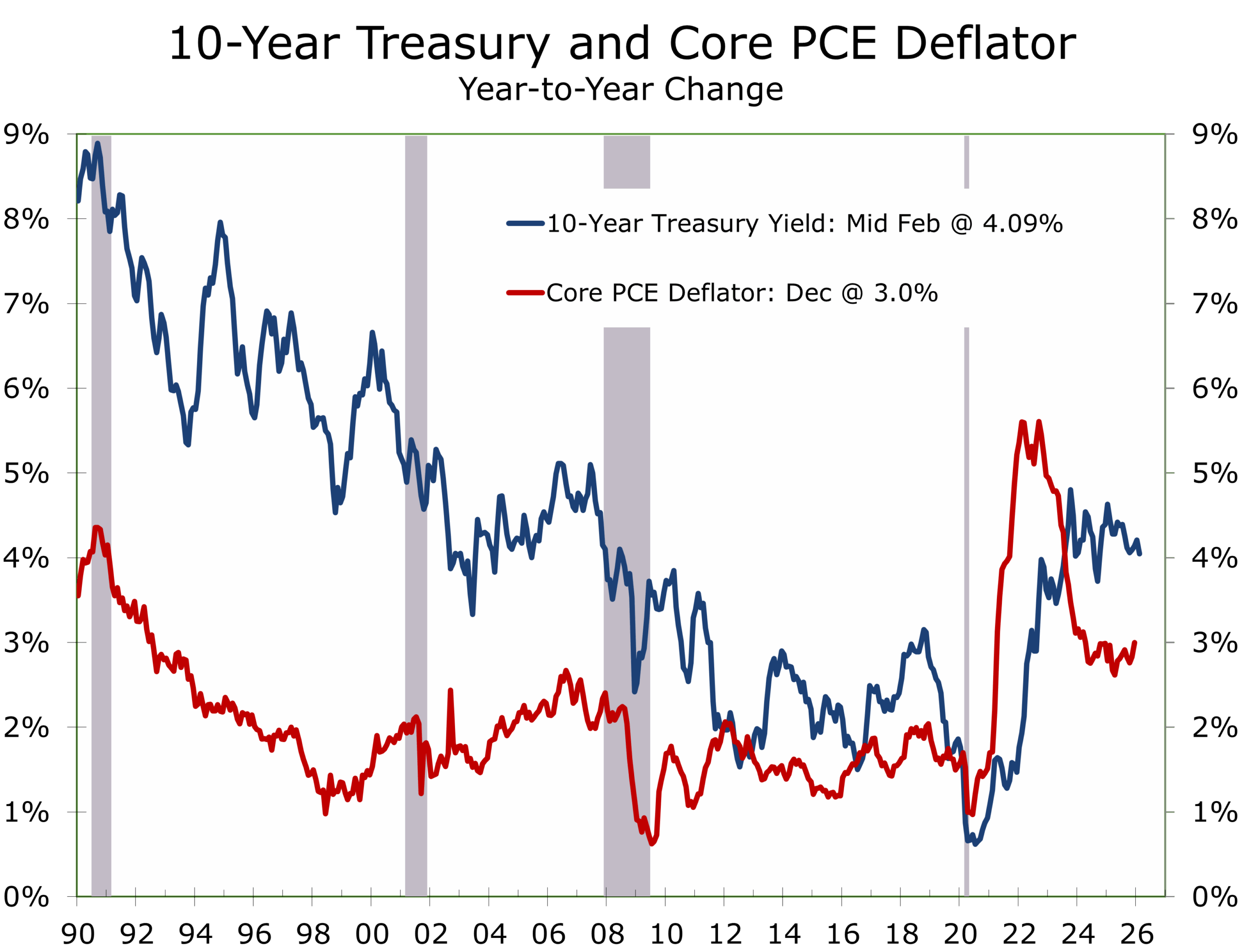

- Inflation continues to drifting lower. Accelerating productivity growth and decelerating shelter costs are driving the improving trend. Core measures cooled as the impact from tariffs fade and unit labor costs stabilize at a slower pace. Q4 saw a bit of an uptick, with the Gross Domestic Purchases price index rose 3.7% (up from 3.4% in Q3), PCE prices +2.9% (from 2.8%), but core PCE +2.7% (down from 2.9%).

- Markets continue to price a quarter-point rate cut in June followed by another in September. We view that timetable as appropriate, but meaningful Q1 softness might pull the first move into May.

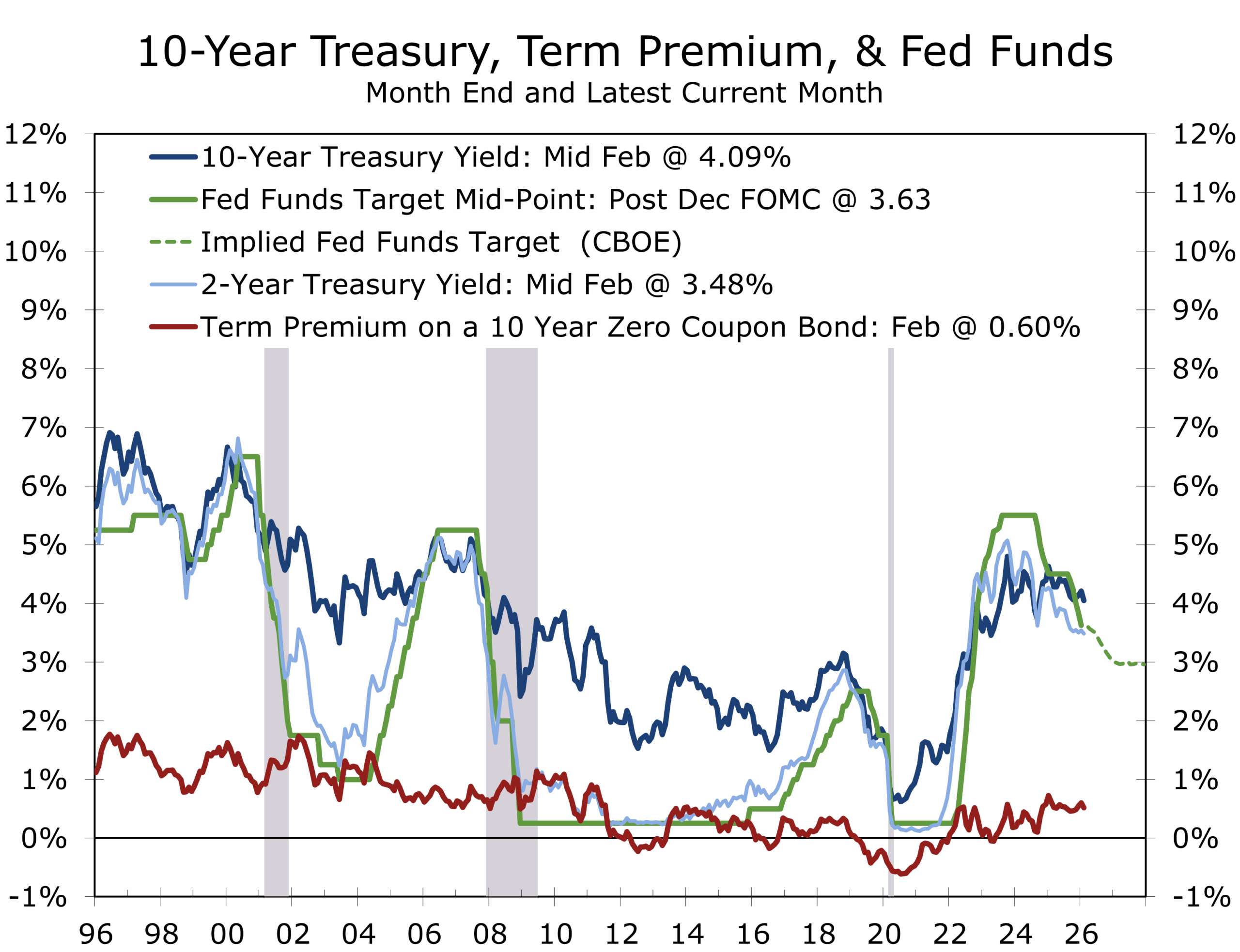

- Treasury supply and geopolitics keep term premia sticky. Oil’s risk premium and heavy issuance limit long-end rate relief. A direct conflict with Iran would likely prove more disruptive than recent military actions and could initially trigger a flight to safety even as energy prices rise, possibly opening a window to lock in lower rates.

- The State of the Union accelerates the political clock. Midterm dynamics compress the timeline for visible economic gains. We look for Trump to pivot on immigration and trade.

- As Thomas Sowell articulated in A Conflict of Visions, durable expansions respect constraints rooted in incentives and institutional limits, rather than unconstrained attempts to design outcomes. This framework, which highlights hard trade-offs over pronouncements and grand visions, applies aptly during Black History Month, reminding us that sustainable progress emerges from disciplined processes, not from platitudes or engineered utopias. Attempts to outrun economic arithmetic will always eventually meet up with market realities.

The Expansion is Evolving

The economy entered 2026 with more underlying momentum than year-end forecasts implied, and with more steam than the 1.4% advance Q4 GDP print suggests. A flurry of delayed releases following the government shutdown has filled in important details, but the story is far from complete.

Nonfarm payrolls rose 130,000 in January, with private payrolls up 172,000 and government employment declining. Healthcare and social assistance continued to lead hiring, but construction and manufacturing also added jobs. Manufacturing payrolls increased for the first time in 14 months. While gains were modest, they were broad-based and consistent with firm national and regional surveys and improving factory output.

Industrial production rose 0.7% in January, with manufacturing output up 0.6%. Durable goods industries posted widespread gains, and the share of manufacturing subsectors contracting year over year has fallen to its lowest level since early 2022. Both the ISM index and payroll diffusion measures moved back above 50. Output now stands near its highest level since mid-2019. We would label this as a legitimate green shoot.

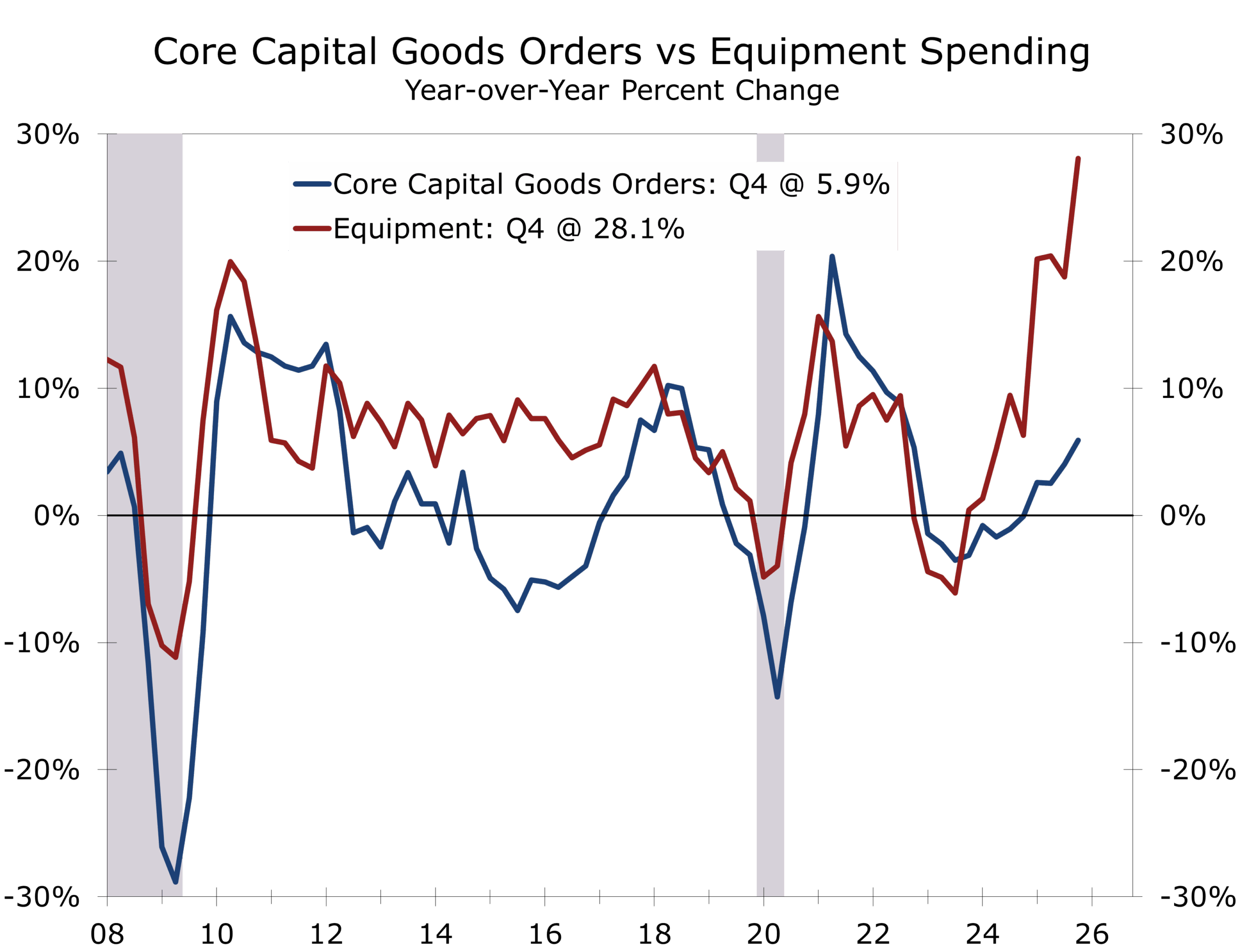

Capital spending ended 2025 on solid footing. Core capital goods orders rose 0.6% in December and core shipments—what feeds directly into GDP—rose 0.9%. Aircraft volatility distorted the headline durable goods data, but underlying investment trends strengthened. AI-related equipment remains a clear tailwind, yet investment gains are gradually broadening beyond technology-linked sectors, supported by fiscal incentives, healthy margins, and expectations of eventual rate relief. Imports tied to AI infrastructure widened the December trade deficit, temporarily obscuring underlying strength in Q4.

Housing remains uneven. Housing starts ended the year at a 1.404 million annual rate, with upward revisions to prior months, and permits suggest stabilization in single-family construction. Mild December weather likely boosted late-year activity, while January storms dampened home sales, starts, and consumer spending. Existing home sales weakened in January. New home sales slipped 1.7% in December after a sharp November gain and finished the year at a solid 745,000 annual pace. Inventories declined but remain elevated at a 7.6-month supply. Builders must work through completed inventories before sustained acceleration resumes.

Wintertime data are unusually noisy. Utilities output surged while mining fell due to weather disruptions, distorting the industrial production headline. Strip out the volatility, however, and the factory sector is improving. Greater clarity around tariff policy, even if duties persist under alternative authorities, reduces one source of hesitation for manufacturers. We expect a cyclical recovery to take hold this year as supply chains normalize, inventories rebuild, and housing turnover stabilizes.

The December FOMC minutes included discussion of possible additional tightening should the deceleration in inflation stall. While that risk appears low, it cannot be dismissed outright. Broader economic data does not point to the economy overheating or anything near that. Cyclical segments—durable goods consumption, housing turnover, and non-AI capital spending—remain soft, with only tentative signs of improvement. The parts of the economy that are growing primarily reflect structural shifts toward AI-driven productivity, healthcare demand, and energy infrastructure.

At the same time, the economy is not deteriorating. The moderation in job growth reflects slower labor supply growth as much as softer demand. Layoffs remain low, with weekly initial unemployment claims hovering just above 200,000. Private-sector hiring remains sufficient to keep the unemployment rate near current levels, which are widely viewed as consistent with full employment.

Productivity growth is improving, supported in part by AI-driven efficiency gains extending beyond technology into logistics, manufacturing, finance, and professional services. Growth is rotating away from lower productivity sectors, reflecting the impact of tighter immigration enforcement on the labor supply, while rotating toward higher productivity sectors in AI, life sciences and aerospace and defense.

Inflation Is Moderating, But Not Smoothly

Inflation continues to ease, though the progress remains uneven. Slower job growth has restrained consumer spending, contributing to softer new and used vehicle sales and easing used car prices. Housing demand has similarly cooled, tempering home price appreciation, while a surge in apartment completions has generated rental concessions across much of the country, helping moderate shelter inflation. January CPI came in at 2.4% year over year on the headline and 2.5% on core, broadly in line with expectations and consistent with gradual disinflation. Inflation expectations have also eased.

The year-end PCE data came slightly hotter than expected. December core PCE rose 0.36% month over month and accelerated to 3.0% year over year, slightly above consensus expectations. Headline PCE also rose 0.36% in December and stands at 2.9% year-over-year. The Q4 GDP report showed the gross domestic purchases price index rising at a 3.6–3.7% annualized pace, reflecting firmer consumption and government deflators.

The divergence between softer CPI readings and firmer PCE measures reflects weighting differences and temporary distortions. The PCE has recently run hotter than CPI in part due to housing measurement effects and stronger financial services inflation. Non-housing services’ inflation remains elevated, but unit labor costs are drifting lower amid moderating wage growth and improving productivity.

Goods inflation, which re-accelerated in 2025 due to tariff passthrough, now appears to be moderating. We expect the headline PCE to decline toward 2.0% by year-end. We estimate that tariffs added roughly 0.4 percentage points to headline inflation over the past year. Absent that effect, the deflators would likely be closer to target already. The impact from tariffs will partially reverse this year.

The broader takeaway is that disinflation is occurring through normalization in demand and supply rather than forced through tighter credit and weaker economic growth. The shutdown-related drag directly subtracted roughly 1.15 percentage points from Q4 growth and should at least partially reverse in Q1. As tariff effects fade and productivity improves, growth can remain positive without reigniting broad price pressures. This means the Fed can cut interest rates before inflation moves back to its 2% target.

Q4 GDP: Resetting the Mix, Not the Cycle

Fourth-quarter real GDP rose 1.4% annualized. The headline was disappointing, but much of the weakness reflected the temporary drag from the federal shutdown, which depressed government spending and will likely reverse in Q1. Strip away that distortion and the underlying economy remains on a stable footing.

Private domestic final sales rose 2.4%, only modestly below Q3’s pace. Consumer spending slowed but remained positive. Business fixed investment increased at a solid clip, led by intellectual property and equipment. Residential investment continued to contract, underscoring that housing remains a lagging sector in this cycle. The composition matters more than the disappointing headline 1.4% print.

This is increasingly a capital-heavy, job-light expansion. Equipment, software, and R&D spending remain firm, particularly in AI-linked sectors. Hiring, by contrast, has moderated materially. Job growth in 2025 was the weakest of any non-pandemic year since 2009, yet output continues to expand near trend. That divergence is the defining feature of this cycle and partly reflects payback for the COVID period.

Productivity gains are allowing firms to generate higher output without proportional increases in headcount. Returns to physical capital, intellectual property, and specialized skills are rising faster than aggregate wage income. Higher-income households, who disproportionately own financial assets and benefit from equity-market strength tied to AI investment, are capturing a larger share of income growth. Meanwhile, lower- and middle-income households, which are more dependent on wage gains and more exposed to goods inflation, are experiencing less improvement in purchasing power.

This dynamic produces what is often described as a K-shaped outcome: aggregate growth continues, but the distribution of gains is uneven. This is not unusual for periods in which the economy endures a transformational shift. As tariff distortions fade and fiscal incentives broaden equipment spending, capital deepening should remain a central theme in 2026. Lower interest rates should eventually lift key cyclical sectors that have been lagging, particularly interest-sensitive areas like housing, consumer spending on durables and capital spending by small and mid-sized businesses that have been squeezed by many of the same forces squeezing consumers.

Full-year 2025, 2.2% real GDP growth marks a moderation from 2024 but remains consistent with an economy expanding within labor-force and productivity constraints.

The takeaway is straightforward. The economy is not rolling over. It is rebalancing. Growth is being driven more by capital formation and efficiency gains than by payroll growth or credit expansion. That mix supports continued expansion with less inflation risk.

The Fed Path: Cuts in a Volatile Policy Backdrop

Markets continue to price the next Fed cut in June, followed by another in September. That path aligns with moderating inflation, a stabilizing labor market, and growth that is steady but no longer accelerating. The January FOMC minutes show a divided Committee—several participants are prepared to ease if disinflation continues, while others prefer patience until further confirmation emerges. The bias remains toward waiting for clearer evidence.

Our base case is two 25bp cuts beginning in June. Inflation is drifting lower, tariff pass-through is fading, and productivity gains are containing unit labor costs. At the same time, labor conditions have stabilized. Claims remain low, yet hiring is measured and increasingly concentrated in healthcare and services. This is not an overheating economy or anything approaching that. Talk of rate hikes is extremely premature.

The Supreme Court’s ruling striking down portions of the administration’s IEEPA tariffs temporarily lowers the effective tariff rate and marginally improves the 2026 growth and inflation outlook. Lower input costs reduce pressure on goods prices and ease the Fed’s burden at the margin. However, the administration retains alternative trade tools and has already signaled potential new levies. Policy uncertainty therefore remains elevated. For the Fed, this argues for maintaining flexibility rather than becoming more reactive.

Risks to our call skew slightly toward an earlier move, particularly if Q1 data softens materially. But absent a clear labor-market break, June remains the most credible starting point. Expect a Warsh-led Fed to emphasize institutional credibility and measured adjustments over forward-guidance activism. Two cuts to roughly 3%–3.25% remains the central path; more would require cleaner evidence that core PCE is sustainably at or below 2%, which very well could happen.

Funding & Issuance: Why the Long End Won’t Cooperate

Even if the Fed trims short rates, the long end faces structural constraints. Fiscal deficits near $2 trillion imply sustained Treasury issuance, while global sovereign supply also remains heavy. The result is a firm term premium and 10-year yields holding near 4%–4.25%, despite cooling inflation.

The tariff ruling modestly reduces near-term inflation risk, but it also injects fresh uncertainty. If the effective tariff rate ultimately settles lower, that supports disinflation and growth. If alternative tariffs are imposed, which appears likely, volatility returns. Markets will need to price that optionality.

Geopolitical tensions, particularly around Iran and energy supply routes, add another layer of caution. Oil risk premia can flatten the curve initially through flight-to-safety flows, but sustained energy shocks would ultimately push inflation expectations and long yields higher. A successful resolution to the Iran situation would benefit markets. An unsuccessful one could prove unfriendly or even ugly.

The message is straightforward: front-end relief does not guarantee long-end relief. Opportunistic issuance on rallies makes sense, but duration exposure should be managed carefully. Ladder maturities. Maintain liquidity. Do not underwrite financing plans on the assumption of aggressive easing.

In a capital-heavy expansion, funding discipline matters as much as rate levels.

The Political Clock

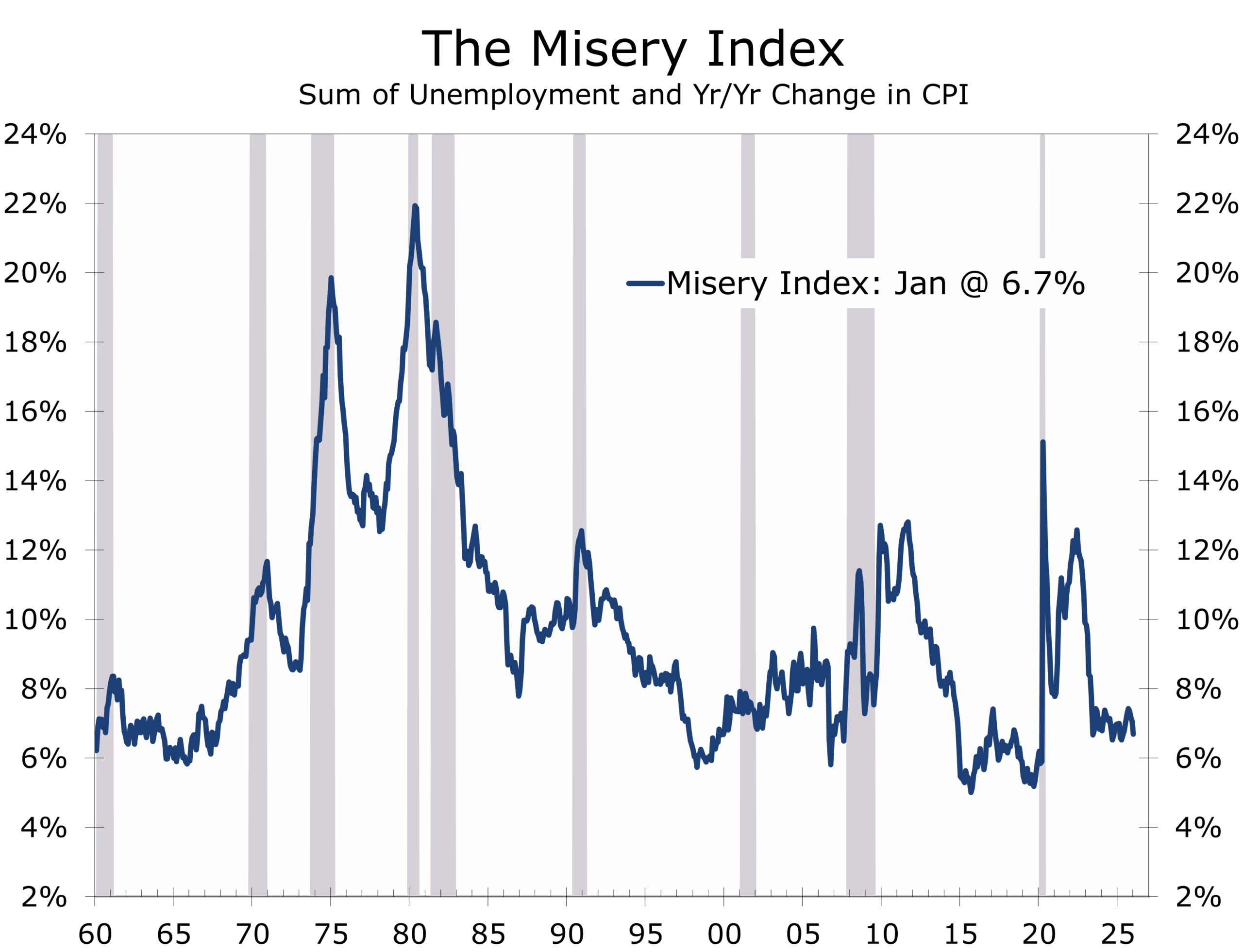

The January employment report points to early stabilization in the labor market. Payrolls rose 130,000 and the unemployment rate edged down to 4.3%. Hiring outside healthcare and social services remains uneven, but layoffs are low and labor supply growth has slowed materially, with net immigration running near 0.2 million annually. That reduces the breakeven pace of job creation to roughly 50,000 per month by year-end. Against this backdrop, we expect the unemployment rate to remain in a 4.0–4.5% range in 2026. Growth near 3.0% this year is supported by fading tariff drag, steady fiscal support, and easier financial conditions, even as elevated valuations and AI-related uncertainty contribute to periodic volatility. At 6.7%, the Misery Index is well below its post-pandemic peak, reinforcing that the macro backdrop is stable, not strained.

The political calendar now matters more. As the midterm elections approach, the window for policy experimentation narrows. Durable initiatives—reshoring, infrastructure, energy expansion, AI investment—typically take time to yield visible results. Those results are currently visible in business fixed investment and should become increasingly across the board visible by this summer. A stronger-than-expected economy reduces the urgency for short-term stimulus and shifts the focus toward sustaining momentum rather than engineering an acceleration.

The Supreme Court’s decision to strike down key tariffs under IEEPA served as an important check on trade policy. President Trump responded strongly, criticizing the ruling and vowing to use alternative authorities for tariffs. This highlights a key risk: policy volatility. Markets now must price in possible tariff relief alongside the chance of new levies under different laws. We believe existing trade deals will hold. Leaders know provoking

President Trump is unwise and often counterproductive. Overall, uncertainty increases, even if the economic impact stays modest.

That said, our base case sees the administration nearing a pivot. As midterms approach, trade and immigration policies should become less disruptive. Incentives will favor stability and clear economic wins. Less policy friction lets fiscal measures and private capital spending drive growth. Uncertainty premiums should then ease, not rise.

This supports our positive 2026 outlook. We currently track Q1 growth near 3.1%, which is where the Atlanta Fed GDPNow also begins the quarter, and expect full-year GDP around 3%. Real GDP looks stronger in the first half, while private final domestic demand picks up in the second half. Inflation heads toward the Fed’s 2% target with moderating shelter costs and broader productivity gains. As inflation cools and rates dip, cyclical sectors like housing, manufacturing, and capital goods outside the AI boom stand ready to rebound. The expansion’s next stage focuses less on credit and more on productive capital use. As far as staffing goes, companies are increasingly focused on putting the right person in role rather than simply hiring more staff. If policy volatility fades as anticipated, the economy gains a second wind: stronger, balanced, and less reliant on heavy fiscal or monetary support—echoing Thomas Sowell’s constrained vision in A Conflict of Visions, where sustainable progress respects incentives and limits over engineered designs.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 23. 2026

Mark Vitner, Chief Economist

704-458-4000