Upside Surprise, Gradual Rebalancing Ahead

-

- Housing starts rose 6.2% in December to 1.404 million (SAAR), with upward revisions to prior months.

- On a November–December average basis, starts increased 5.1%, well above expectations, adding support to our above-consensus Q4 2.8% annual rate GDP call.

- Permits rose 1.3% across November and December, also beating consensus.

- Full-year 2025 starts totaled 1.36 million, down 0.6% from 2024.

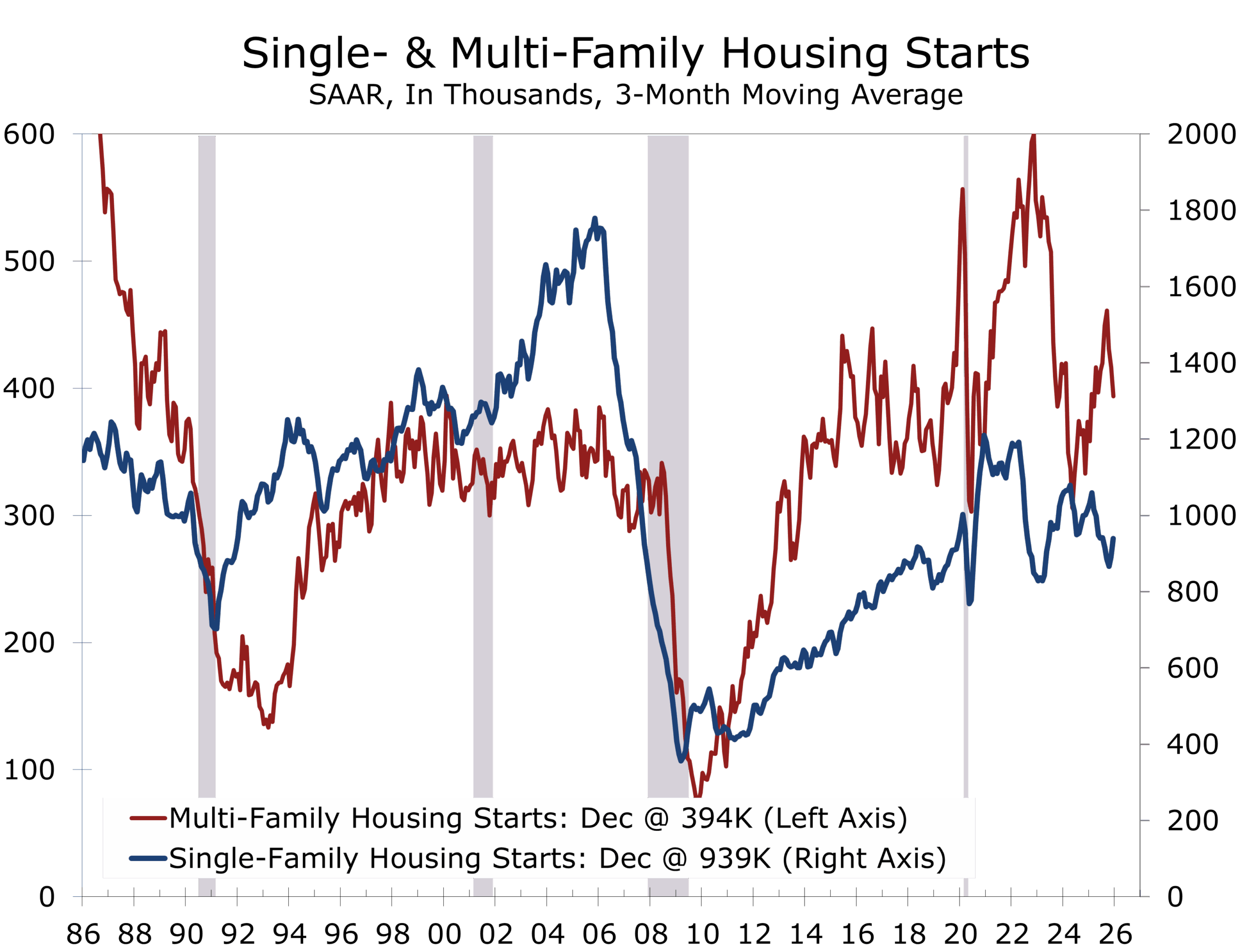

- Single-family starts fell 6.9% in 2025, while multifamily rose 17.4%.

- Builder sentiment slipped again in February amid affordability pressures.

- Remodeling remains structurally stronger than new construction, benefiting from reduced housing turnover.

- Homebuilding finished 2025 on a strong note, but activity is likely to pause in the first half of this year as builders work to reduce elevated inventories.

A Firm Close to a Mixed Year

Housing starts ended 2025 with more momentum than previously believed. Total starts rose to 1.404 million at an annual rate in December, and prior months were revised higher. Averaging November and December together, starts increased 5.1%, comfortably exceeding expectations. October was revised up meaningfully to 1.272 million, reinforcing the view that the fourth quarter ended on firmer footing than initially reported.

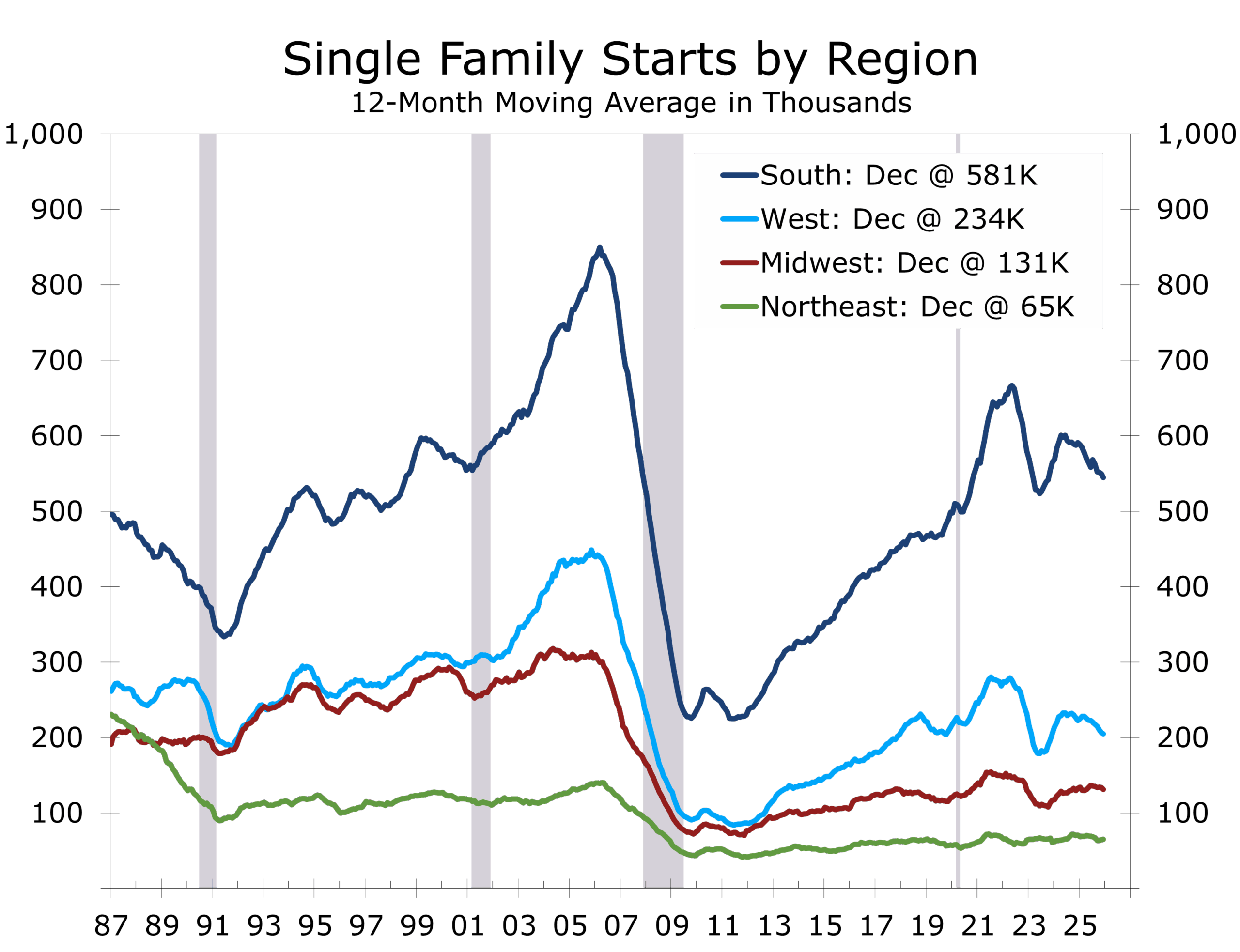

Both major components contributed. On a two-month average basis, multifamily starts increased 5.9%, while single-family starts rose 4.8%. Regionally, activity rose sharply in the West and posted gains in the South and Northeast, though the Midwest declined. The geographic dispersion suggests broad improvement rather than a single-region anomaly, though weather likely amplified the December print. Favorable conditions likely pulled some activity forward, suggesting potential payback in January.

December’s strength improves Q4 growth optics but likely reflects partial weather distortion.

For 2025 overall, total housing starts were 1.36 million, down 0.6% from 2024. The modest decline masks meaningful internal rotation. Single-family construction totaled 943,000 units, down 6.9% year-over-year, reflecting persistent affordability constraints. Multifamily starts rose 17.4% for the year, supported by projects initiated during the earlier rent-growth cycle and relative strength in low-rise formats.

Permits also surprised modestly to the upside. Averaging November and December, building permits rose 1.3% to 1.448 million, above consensus expectations. Multifamily permits increased 3.8% over the two-month period, while single-family permits edged up 0.2%. Regionally, permits rose in the Northeast, Midwest, and West but slipped slightly in the South. The stabilization in permits suggests the downturn in housing is behind us, though not yet replaced by broad-based acceleration.

This remains a payment-constrained cycle, not a credit-driven downturn.

Single-family construction remains constrained by affordability. Elevated mortgage rates, high price-to-income ratios, and cost pressures continue to limit first-time buyers. February’s NAHB/Wells Fargo Housing Market Index underscores that reality. Builder confidence slipped to 36. Traffic of prospective buyers fell further, and builders continued to rely on incentives, including price reductions and financing concessions, to close transactions. The market is functioning, but it remains highly payment sensitive.

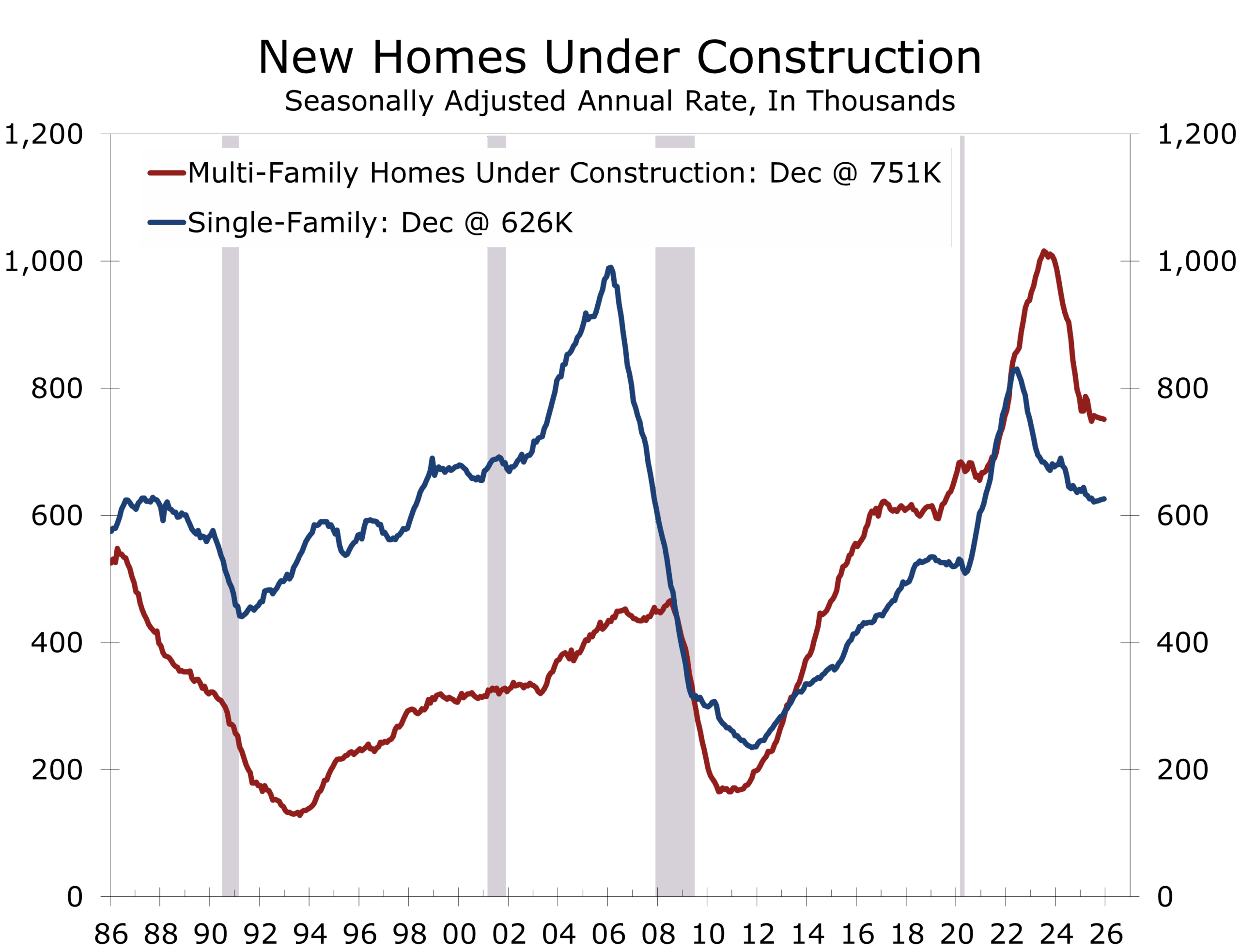

Multifamily construction is entering a normalization phase. December’s 11.3% increase brought the pace to 423,000 at an annual rate. However, rising completions and slower rent growth are shifting the focus from expansion to absorption.

One notable divergence within residential construction is the sustained strength in remodeling. While new construction sentiment has softened, the NAHB Remodeling Market Index has remained above 50 for 24 consecutive quarters. Structural forces continue to support this segment. The housing stock is aging, the mortgage rate lock-in effect continues to discourage mobility, and elevated home equity provides financing capacity for improvements.

Housing is no longer subtracting from GDP, but it is not yet driving growth.

Remodeling now represents a materially larger share of residential construction than in prior cycles. NAHB expects real remodeling activity to grow modestly in both 2026 and 2027. In this environment, renovation has become the primary outlet for housing demand constrained by interest rates.

Regional performance in 2025 reflects cyclical rebalancing. The Northeast and Midwest posted gains for the year, while the South and West softened modestly. The pandemic-era surge into the Sunbelt has cooled cyclically, though longer-run demographic fundamentals remain intact. Relative affordability remains a key driver with migration patterns shifting away from previously overheated Sunbelt markets toward more affordable and less congested areas in the Carolinas, eastern Tennessee, Alabama, Mountain West, and portions of the Midwest.

Taken together, the housing market is stabilizing rather than reaccelerating. December’s strength supports our above consensus call for 2.8% Q4 real GDP growth and suggests that the worst of the housing slowdown is behind us. Yet affordability constraints, elevated inventory levels, and incentive-driven sales dynamics indicate that the next phase will be gradual.

Housing is recalibrating as homeowners and buyers reassess what the future path of mortgage rates is likely to be. Mortgage rates remain below their long-run historical norm, but we expect them to hover near 6% in the near term, with only brief breaks below that level possible this spring. A sustained acceleration in homebuilding will require meaningful improvement in affordability, not simply favorable weather or short-term inventory adjustments.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 18, 2026

Mark Vitner, Chief Economist

(704) 458-4000