Inflation Continues to Ease Back to Historic Norms

-

- Headline CPI rose 0.3% in December, while year-over-year inflation held steady at 2.7%, reinforcing evidence that inflation has likely peaked for this cycle.

- Core CPI increased 0.2%, leaving core inflation unchanged at 2.6% y/y, slightly softer than expected once shutdown-related distortions are accounted for.

- Shelter prices rose 0.4%, the largest contributor to the monthly increase, though part of the recent volatility reflects data distortions tied to the federal shutdown rather than a change in trend.

- Food prices surprised to the upside, rising 0.7% on the month, with both grocery and restaurant prices contributing.

- Energy prices increased modestly, driven by natural gas, as unseasonably cold weather offset falling gasoline prices.

- Core goods inflation appears to have peaked, while services inflation outside of shelter continues to trend lower, supported by improving productivity and easing unit labor costs.

Headline Inflation: A Firm Finish to the Year

Consumer prices rose 0.3% in December, a step up from November, driven primarily by shelter and food. On a year-over-year basis, headline inflation held at 2.7%, confirming that inflation has stabilized at a lower level even as month-to-month readings remain uneven.

December’s report was noisier than usual due to the federal shutdown, which compressed data collection and distorted comparisons with prior months. November prices were collected only for late in the month, exaggerating some December increases, particularly in seasonal and holiday-sensitive categories. Even so, stepping back from the volatility, the broader signal suggests inflation continues to decelerate, and the bulk of the impact from tariffs is now behind us.

Inflation continues to decelerate and is now roughly even with its long-run trend.

Energy prices added modestly to the headline, while food prices delivered an outsized monthly gain. The combination pushed the CPI headline higher even as underlying inflation trends remained broadly consistent with the Fed’s target range.

Core Inflation: Stable, but Not Yet Settled

Core CPI rose 0.2% in December, matching recent monthly averages and keeping core inflation at 2.6% year over year. The rise in the core CPI was slightly softer than expected once shutdown distortions are considered, reinforcing the view that underlying inflation pressures are easing.

Tariffs are most evident in core goods inflation, which now appears to have peaked.

Core goods prices declined again, led by sharp drops in used cars and trucks (-1.1%), communications (-1.9%), and household furnishings (-0.5%). Broader core goods inflation now appears to have peaked, reflecting slower tariff pass-through, easing supply-chain pressures, and growing efforts by the Administration to reduce the sting of tariffs.

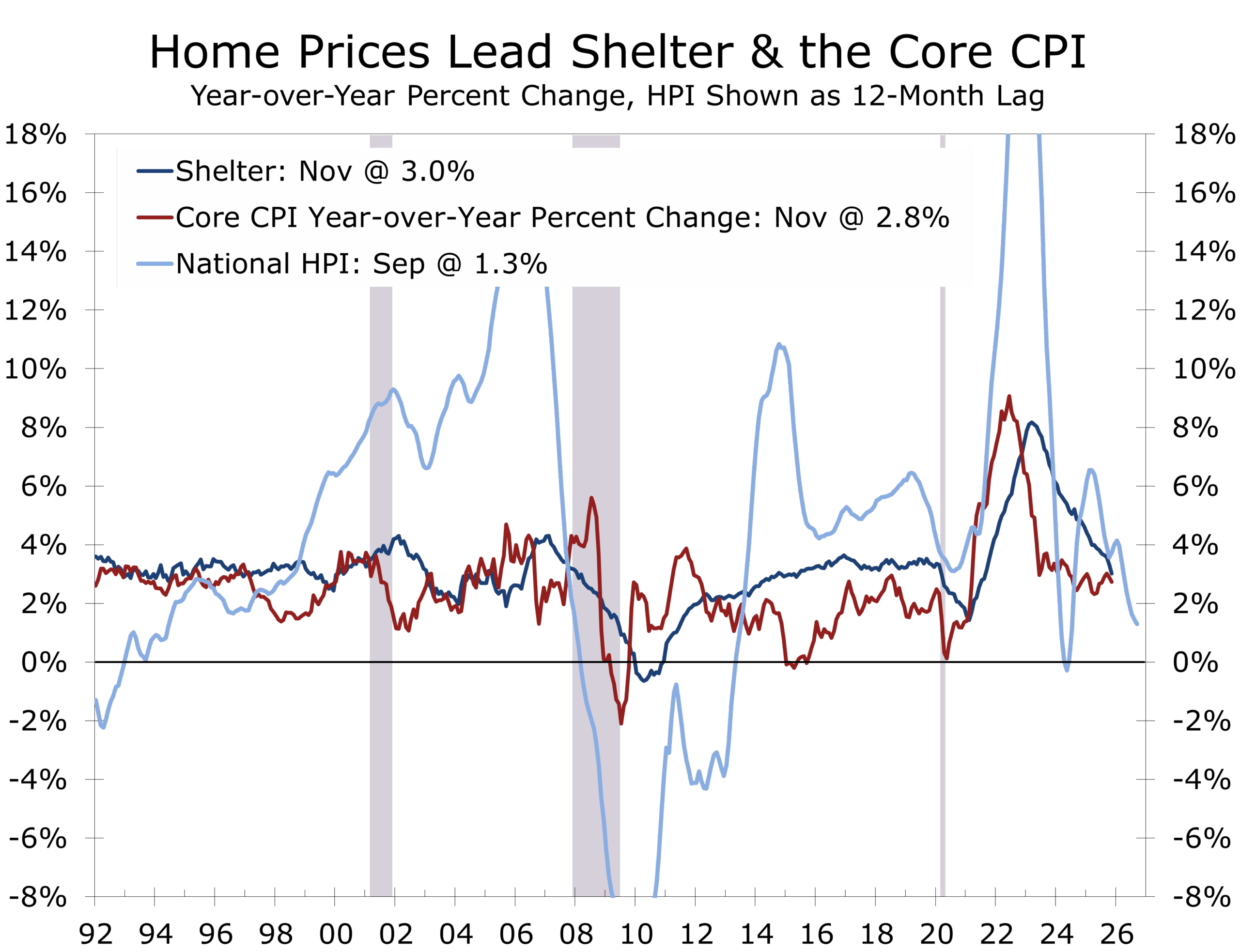

Shelter prices rose 0.4% in December, firmer than in recent months, with both rent and owners’ equivalent rent up 0.3%. The headline was rose more than its two largest components because hotel and other lodging costs surged 3.5%. The spike likely reflects the later survey period, which picked up more holiday season demand. Year-over-year shelter inflation now stands at 3.2%, well below cycle highs but still elevated relative to pre-pandemic norms.

Market-based rent indicators continue to point toward further moderation in 2026 as elevated multifamily supply works through the system. Moreover, home prices, which have reliably provided a leading signal for shelter costs 12 to 18 months ahead, continue to ease.

Shelter costs continue to follow home prices lower and will likely bring the core CPI back to the Fed’s target by year-end.

The message is clear; core inflation is headed lower this year and will likely finish 2026 close to the Fed’s 2% target.

Food prices rose 0.7% in December, marking one of the strongest monthly gains of the year. Grocery prices increased broadly, while restaurant prices continued to reflect elevated labor and operating costs.

Food away from home inflation remains particularly sticky at 4.1% y/y, reinforcing why many consumers remain skeptical of improving inflation data despite easing headline measures. The jump in food and energy prices are the least encouraging elements of the report. We suspect that the later than usual timing of the survey meant that the survey picked up much more of holiday season price hikes. We are looking from more modest gains in grocery prices in 2026.

Higher restaurant prices are likely to weigh on office workers as the return-to-office trend solidifies, with higher beef prices remaining a key upside risk. Restaurants have little room to cut prices, as labor costs are rising along with the minimum wage.

Energy: Volatile but Contained

Energy prices rose 0.3% in December, driven by a sharp increase in natural gas prices amid colder weather, while gasoline prices declined. Over the past year, gasoline prices are down 3.4%.

While falling global oil prices are easing gasoline costs, rising electricity demand, including from data centers, is limiting the pace of disinflation in utilities. Even so, energy continues to behave as a swing factor rather than a structural inflation driver.

We are looking for energy costs to moderate this year, as natural gas prices fall back and restrain electricity prices. The Trump Administration is also likely to lean on utilities this year to avoid passing on the costs of ramping up capacity to serve data center. Finally, the move against Venezuela’s ghost fleet of supertankers will keep oil prices lower.

Services inflation firmed in December, with notable increases in recreation (+1.2%), airline fares (+5.2%), and lodging away from home (+2.9%). These categories remain closely tied to upper-income demand and labor intensity. This past month’s hikes, however, were largely overstated, as the survey took place later than usual and was impacted by holiday season travel.

Goods prices, by contrast, continue to ease, reversing last year’s tariff-driven run-up. Improving productivity growth is helping to slow unit labor costs, which should support further moderation in services inflation outside of shelter in 2026.

Inflation pressure is becoming more concentrated, not widespread.

December’s CPI reinforces a clear shift in the Fed’s reaction function. Both the headline and core CPI have returned to their long-run average of 2.7% and 2.6%, respectively, easing the central bank’s policy dilemma. Inflation is no longer the dominant risk, though residual seasonality and shutdown distortions will complicate interpretation in coming months.

The federal funds rate remains modestly restrictive, and rate cuts are best viewed as insurance rather than stimulus. With inflation fears fading, the Fed has greater flexibility to respond to downside risks in the labor market should conditions weaken.

The inflation data argues for patience rather than urgency. President Trump has gotten the affordability memo and is also likely to use his bully pulpit to pressure firms to restrain price increases, an approach that should prove marginally effective at the margin. With price pressures already easing, we expect both headline and core inflation measures to be near the Federal Reserve’s target by year-end.

December closes the year with inflation lower than a year ago, but still uneven across categories. Shelter is cooling gradually, goods prices are deflating, and services inflation remains the final hurdle. Strip away shutdown distortions, and the evidence increasingly suggests inflation has peaked and is on a slow glide path lower into 2026. Disinflation is intact, but the last mile will remain uneven and politically sensitive as the new year begins.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 13, 2026

Mark Vitner, Chief Economist

(704) 458-4000