Inflation is Still Too High for the Fed to Ease

- Both the headline and core CPI rose 0.3% in April, which was in line with market expectations but less than market fears.

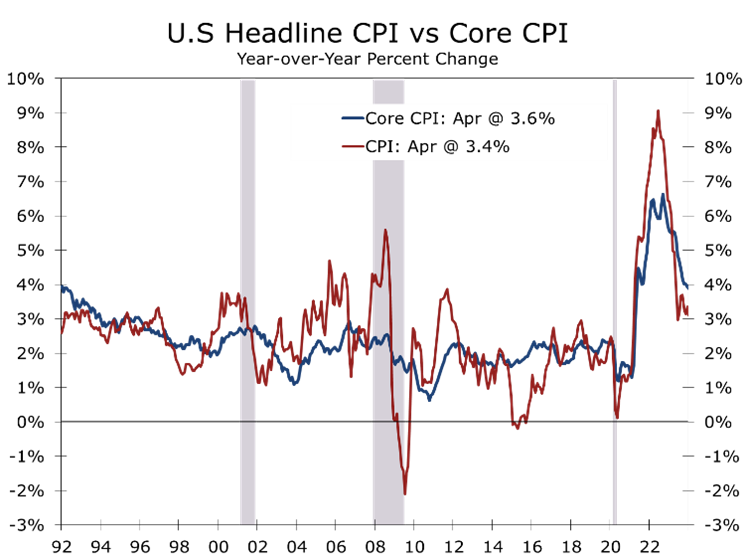

- Year-to-year headline CPI edged down to 3.4%, while the core CPI is now up 3.6%, both are the smallest rises since April 2021.

- The underlying details were encouraging, with price pressures easing in many problem areas, including residential rent.

- Energy prices rose 1.1%, led by higher gasoline prices. Food prices were unchanged, with prices falling at grocery stores and continuing to rise at restaurants.

- Price increases remain problematic in services, with core services prices rising 0.4% in April and 5.3% over the past year.

- Inflation has slowed most notably in the goods sector, where earlier spikes in prices for used cars, household appliances, and a few other items are now reversing.

- The financial markets rallied following the CPI report, which rose largely in line with expectations but followed three CPI reports that came in hotter than expected. While price increases are still broad based, the underlying details suggest inflation should ease further in coming months.

The Consumer Price Index rose 0.3% in April, both on an overall basis and after excluding food and energy prices. The report was close to market expectations but comes on the heels of three consecutive hotter than expected CPI report.

The financial markets breathed a sigh of relief that inflation came in as expected. On a year-to-year basis the overall CPI edged back down to 3.4%, while the core fell back to a 3.6% rise. Price increases ebbed across a wide assortment of categories, including some of the more problematic areas over the past 3 months.

Price increases ebbed across a wide assortment of categories, including some problem areas.

Higher prices for shelter and gasoline accounted for the bulk of the CPI’s rise in April. Combined these two categories accounted for over 70% of the rise in the overall CPI. Gasoline prices rose 2.8% in April, reflecting a larger than usual springtime rise. Gasoline prices are up only 1.2% year-to-year.

Food prices were unchanged, with grocery store prices declining 0.2% in April. Much of that drop was due to a pullback in egg prices, which had surged earlier. Prices for fresh fruits and vegetables also eased. Prices continue to rise at restaurants, reflecting higher labor costs. Prices at limited-service restaurants rose 0.4%, while prices at full-service restaurants rose 0.3%.

While prices ebbed slightly at grocery stores in April, consumers are still suffering from sticker shock. Grocery store prices are roughly 25% higher than they were prior to the pandemic. That gain far outstrips income growth, which has left consumers scrambling on ways to stretch their household budgets.

Prices have risen even more rapidly at restaurants and the pace has moderated less. Prices for food purchased for consumption away from home (primarily restaurants) rose 4.1% over the past year and are currently about 26% higher than they were prior to the pandemic. Wages for restaurant workers have risen just over 37% over this period, which leaves restaurant operators with little room to offer discounts or cut prices.

Price increases are easing somewhat at grocery stores but continue to rise at restaurants.

Inflation has slowed most notably in the goods sector. Core goods prices declined by 0.1% in April and have fallen by 1.3% over the past year. This decline is largely due to lower used car prices, which surged during the pandemic but have since stabilized. Used car prices fell 1.4% in April and have dropped 6.9% over the past year. Additionally, home appliance prices have fallen by 5.6% in the past year, led by a huge 11.6% plunge in prices for washers and dryers, the prices of which had surged earlier.

The post-pandemic inflation resurgence sparked a debate on its causes. We view it as stemming from the Fed accommodating the massive expansion of fiscal policy following the pandemic. This massive relief allowed income and spending to rebound faster than output, exacerbating shortages and driving prices higher.

Despite attempts by some politicians to blame others (such as greedflation or shrinkflation), there is scant evidence to suggest businesses are responsible for the post-pandemic surge in prices. The Federal Reserve Bank of San Francisco analyzed price markups across industries. Their findings showed minimal changes in overall operating margins, with only a few industries experiencing increases, most notably motor vehicle dealers and petroleum refiners. This aligns with intuition, as it is improbable that businesses suddenly became more greedy.

The San Francisco Fed’s research aligns with recent data from small business owners, which shows small business confidence has weakened due to the inability to offset rising operating costs. While price increases may slow further, the increased pressure on margins is expected to weigh on hiring and capital spending in coming months, consequently slowing overall growth.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

May 15, 2024