Protein Over Sugar: Flipping the Script

- 2026 is setting up as a better year than most year-end consensus forecasts projected. The economy continues to shift from a consumption-led to a capital-led expansion with a meaningful assist from inventory rebuilding and a gradually thawing housing market.

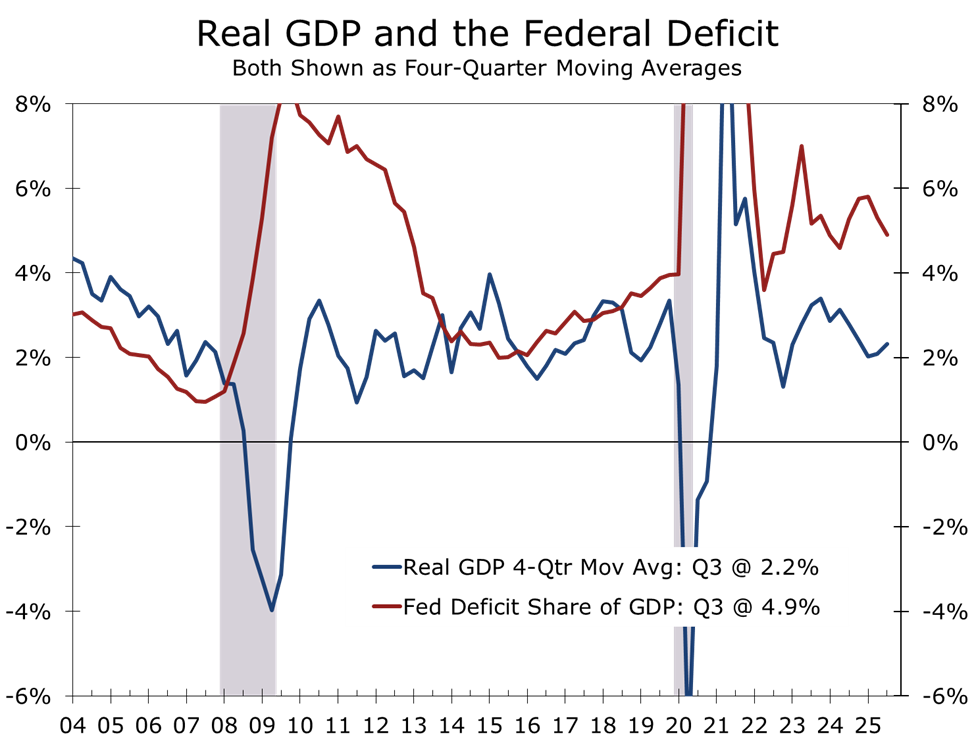

- Fiscal policy is still pushing, not pulling. The deficit is large, front-loaded, and additive to demand. CBO estimates the federal deficit totaled $601B in the first quarter of FY2026.

- Inflation is drifting back toward target. Productivity gains and shelter disinflation are doing the heavy lifting, with tariffs now largely in the rear-view mirror rather than a forward shock.

- Rates likely settle lower than feared. The market story is less “cut now” and more “you can cut later without regret” as inflation normalizes. Look for the federal funds rate to undershoot this year as the economy moves to the new next thing.

- Fed leadership is now a market variable. The next Chair choice matters, but the more immediate question is which candidate can preserve credibility, avoid politicization, and keep the inflation-expectations anchored but still allow for capital-intensive economic growth to run well above its past long-run trend.

- Geopolitics continues to have surprisingly little market impact. Pressure on European allies to help craft a deal on Greenland is a negative surprise but we do not expect a material change in relations with NATO nations. Some action against Iran remains likely, which is putting a higher floor under natural gas prices.

The Script Has Flipped

For most of the post-GFC era, economic growth was fueled by cheap credit, asset inflation, and a steady diet of policy sugar. After a sluggish start, that model delivered quick calories through leverage and wealth effects, but it left the economy dependent on low rates and loose financial conditions. Growth was demand-heavy, inflation-prone, and increasingly fragile.

The 2026 playbook looks fundamentally different. The key drivers of growth have flipped, much like RFK Jr. flipped the food pyramid. This expansion is being built on protein rather than sugar. Capital spending, productivity gains, inventory rebuilding, and a housing thaw are the economy’s key drivers this year. Growth is less reliant on consumption pulled forward by credit and more grounded in the economy’s ability to produce.

The next phase of expansion is less about how much consumers can borrow and more about how productively capital is deployed.

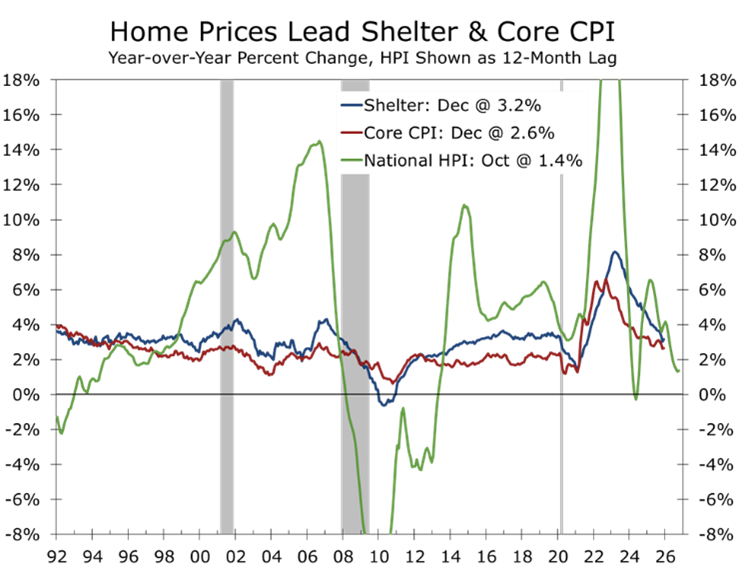

These drivers are inherently disinflationary. Productivity expands supply faster than demand. Capital deepening allows firms to raise output without bidding up labor costs. Inventory rebuilding reduces scarcity premiums rather than creating them. A housing recovery driven by volumes instead of prices helps cool shelter inflation rather than reignite it.

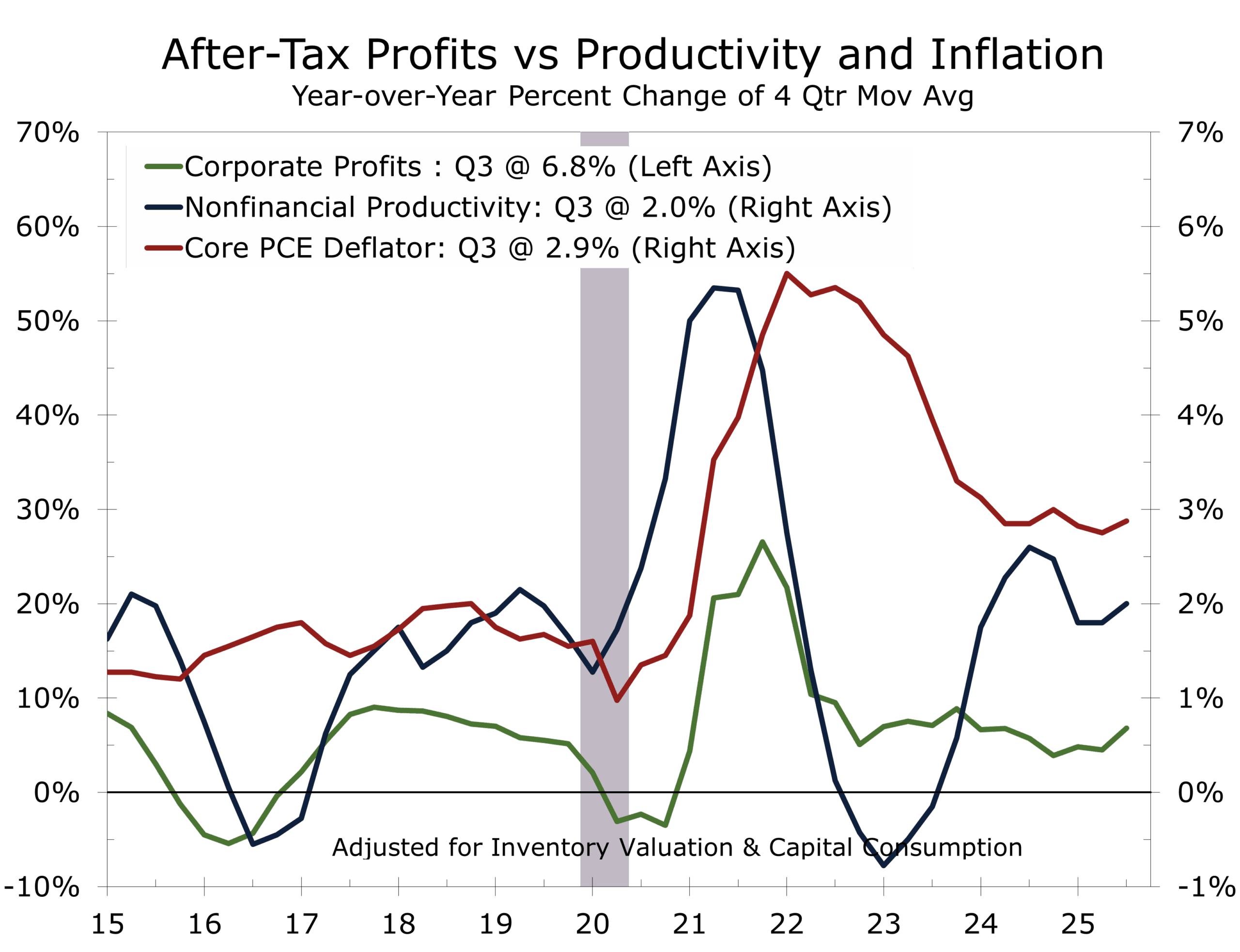

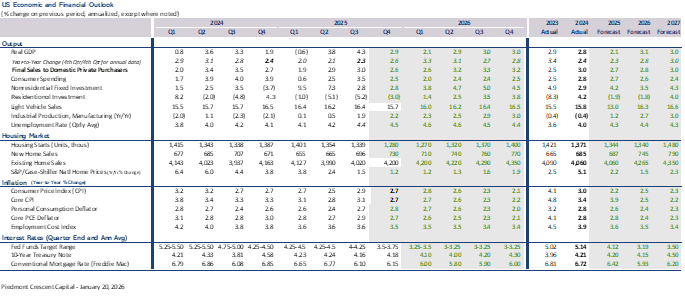

This is also a profit-led expansion, and that distinction is critical. Firms are increasingly generating earnings through efficiency and capital discipline rather than price increases. Margins are being protected by productivity gains even as nominal growth moderates. Profits can grow in a disinflationary environment when costs fall faster than revenues. We are looking for productivity growth to ramp up to a 2.7% pace and look for inflation to fall back toward the Fed’s 2% target by the end of this year. Such a scenario should be good for corporate profits.

Importantly, this does not require a weak consumer. Consumer spending is likely to prove resilient, supported by income growth, balance-sheet repair, and a gradual easing in interest rates. The consumer is no longer the accelerant but will serve more as a stabilizer. Once home buying catches a second wind, we should see notable knock-on effects for furniture, appliances, and related goods and services.

That balance matters for markets. Equity valuations are already full, reflecting confidence that profits continue to compound despite slower headline growth. In this regime, upside is less about multiple expansion and more about execution. The risk is no longer runaway inflation, but whether earnings growth can continue to validate a fully priced market in a capital-driven cycle.

Fiscal Impulse: Still Additive

Fiscal policy remains a tailwind. Even without new legislation, the federal deficit is large enough to support nominal growth and cushion periods of private-sector softness. This is not a tightening environment by any reasonable historical standard.

According to the Congressional Budget Office, the deficit totaled roughly $601 billion in the first quarter of FY2026. The Bipartisan Policy Center notes that the CBO projects a $1.7 trillion deficit for FY2026, equivalent to roughly 5½ percent of GDP. That level of borrowing is inconsistent with austerity and continues to provide meaningful macro support.

The implications are straightforward. First, the economy has a built-in demand buffer, reducing downside risk even as growth moderates. Second, because fiscal restraint is not doing the work, disinflation must come from the supply side—through productivity gains, easing shelter costs, and improved capacity utilization rather than weaker demand.

Washington is not tightening. The private sector is adapting.

Against that backdrop, targeted fiscal initiatives can still matter at the margin. The Big Beautiful Bill (BBB) functions less as baseline support and more as an accelerator, channeling stimulus through higher-multiplier mechanisms. Front-loaded infrastructure spending and expanded middle-income tax credits tend to recycle quickly through local labor markets and construction pipelines, supporting private-sector CAPEX and employment before broader deficit effects fully materialize.

The result is a fiscal environment that is not merely passive, but selectively stimulative. This mix should reinforce growth while leaving the burden of disinflation squarely on productivity and supply-side normalization rather than policy restraint.

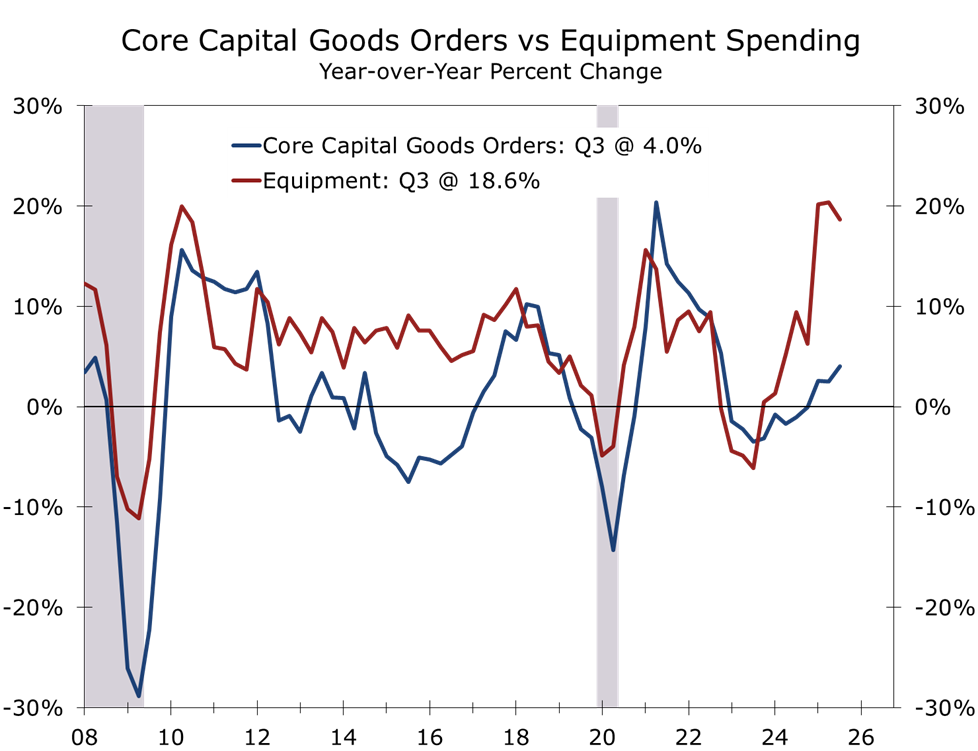

Capital Spending: The Cycle’s Anchor

With fiscal policy setting the floor, capital investment is defining the ceiling. Business fixed investment remains the backbone of this cycle. AI infrastructure, power generation and grid upgrades, biopharma, aerospace, defense modernization, and selective reshoring are driving a multi-year capex stack that is far less sensitive to consumer sentiment than typical late-cycle investment.

This investment reflects a reordering of priorities shaped by demographics, energy intensity, national security, and technological scale. Firms are not expanding because demand is overheating, but because capacity, resilience, and productivity matter more in this cycle than marginal labor growth.

Business investment remains the cycle’s anchor, allowing the expansion to regain traction as housing re-engages and seasonal tailwinds lift spring growth.

A near-term accelerant is tax uncertainty. When firms face ambiguity around expensing rules, credits, or corporate rates, they do not typically freeze investment. They pull it forward, especially when balance sheets are healthy and strategic projects are already approved.

Trade data reinforce the point. Capital goods imports have been a clear outlier, supported by high-tech equipment tied to AI infrastructure and data centers, even as other import categories have softened. That divergence underscores how investment demand is being driven by structural needs rather than cyclical exuberance.

This matters for inflation. Capital deepening expands productive capacity, eases bottlenecks, and allows output to grow without proportionate increases in labor or prices. In other words, the same forces lifting capex are also reinforcing disinflation, validating the broader theme of a supply-led, profit-sustaining expansion.

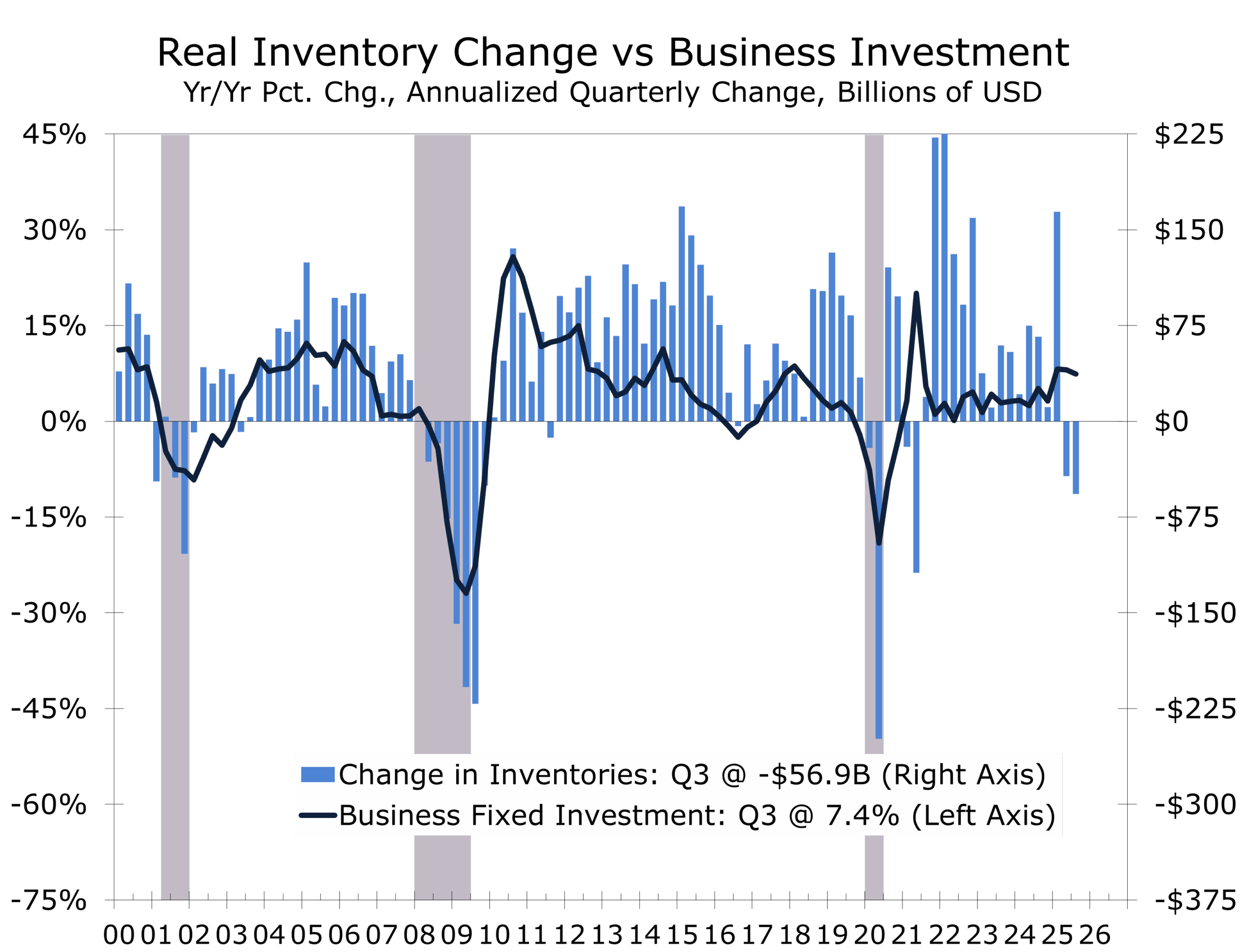

Inventories: A Quiet Tailwind

After a long stretch of lean inventories and cautious ordering, the economy is positioned for incremental inventory rebuilding. That is not glamorous, but it is powerful and will help broaden economic gains beyond the narrow subset that has been driving capital spending.

Think of inventory as the cycle’s flywheel. When inventory moves from drag to neutral, growth accelerates even if final demand merely holds steady. Inventory rebuilding will also help drive demand in transportation and warehousing, which has been noticeable soft since tariffs were introduced in early April of last year.

.

Housing: Thaw First, Then Build

Housing has been the missing transmission mechanism in this cycle. That is beginning to change.

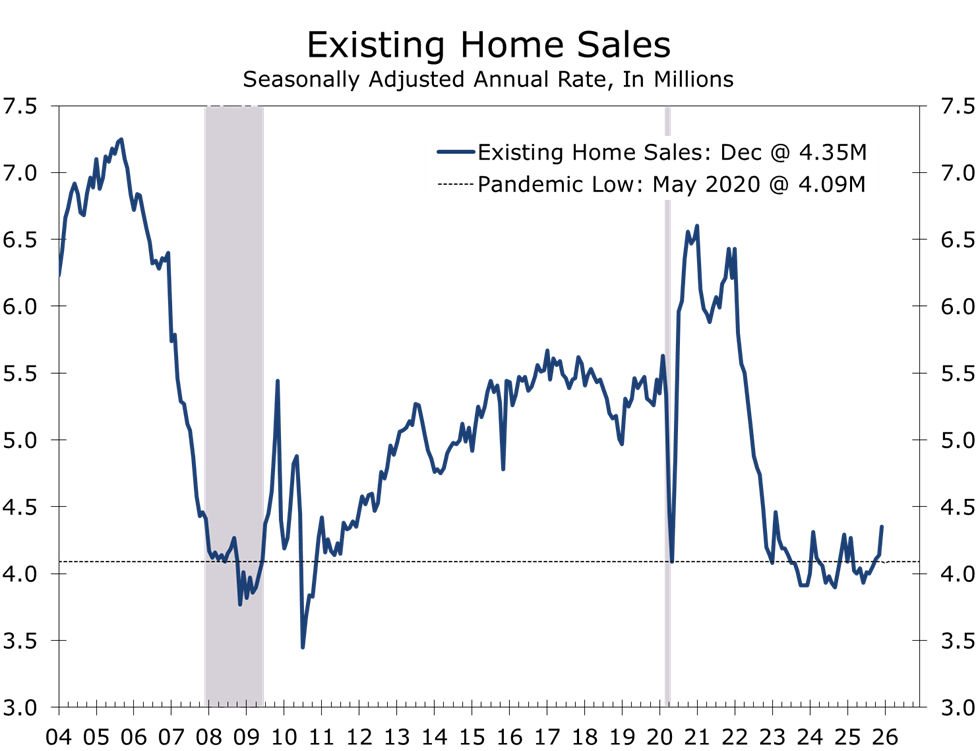

The initial response is showing up in stronger home sales, not a surge in construction. As mortgage rates drift lower and inventories improve at the margin, existing home sales can rebound quickly from depressed levels. Preliminary data suggest sales averaged roughly 4.06 million units in 2025, then firmed late in the year, reaching a 4.35-million-unit pace in December, the strongest reading since early 2023.

That improvement matters, even if conditions remain uneven. Many markets are still buyer-friendly, with easing prices and affordability constraints keeping pressure on sellers. Turnover is the key transmission channel. Rising sales support brokerage income, renovation activity, furniture and appliance demand, and a confidence lift that feeds back into consumption.

Mortgage rates in the 6% range, and occasionally a little under that, appear to be the psychological threshold that re-engages buyers and begins to unlock existing homeowners who have been content to remain in place with sub-4% mortgages. Housing cycles are behavioral as much as financial. Rising activity draws in additional sellers, improves inventory, and reinforces momentum.

The second phase comes later: stronger homebuilding, most likely in the back half of the year. Builders remain focused on managing affordability and elevated inventories of completed homes, while a sizable pipeline of projects under construction continues to work through. That backlog limits the risk of a rapid supply surge even as demand improves. Apartment overbuilding will also keep a low ceiling on multifamily construction.

Housing does not need to boom to matter. It simply needs to improve off recent lows.

This sequencing is critical for the macro-outlook. Housing first supports growth through turnover and consumption; construction follows with a lag. In a capital-led expansion, that delayed response helps extend the cycle rather than cause it to overheat.

Productivity, Inflation, and Rates: The Supply-Side Flywheel

The most underappreciated driver of this cycle is productivity. The third-quarter surge was not a statistical fluke, but an early signal of a broader shift now underway. As output accelerates ahead of hiring, productivity growth is likely to remain elevated over the next several quarters before settling into a higher structural run-rate.

Our expectation is that productivity growth stabilizes between 2.5 and 3.0 percent, materially above the post-GFC norm. That alone is powerful. At that pace, the economy can sustain real GDP growth near 3 percent in both 2026 and 2027 without recreating the inflation pressures that defined earlier expansions.

In this cycle, productivity is doing the heavy lifting that policy usually does.

This is the mechanism that makes the broader 2026 outlook coherent. Capital spending expands supply-side capacity. Productivity rises. Unit labor cost pressure eases. Services inflation moderates. The Federal Reserve gains room to normalize rates without re-accelerating inflation. Growth is no longer dependent on policy stimulus or excess demand. It is being earned through efficiency.

Inflation, in that context, is not collapsing. It is normalizing. The tariff-driven pulse that interrupted disinflation has largely peaked. The next leg lower comes from shelter, where home prices have flattened and rents historically follow with a 12 to 18-month lag. As shelter inflation rolls over and productivity restrains services inflation outside housing, the glidepath back toward the Fed’s target becomes increasingly plausible.

That combination reshapes the interest-rate outlook. Markets remain focused on the timing of the next cut, but the more important question is why rates can be lower. If inflation drifts back toward target while growth holds near trend, the rate regime shifts from restrictive protection to neutral normalization. Historically, that environment supports lower front-end volatility, a gradual decline in real yields, and only modest curve steepening—unless fiscal dynamics force term premia higher.

This backdrop elevates the importance of Federal Reserve leadership. With Chair Powell’s term ending in May 2026, the Chair decision is no longer a distant personnel matter; it is now part of the market narrative. The central issue is not loyalty or ideology. It is credibility.

Markets can accommodate a new Chair. What they cannot accommodate is ambiguity around the Fed’s objective function. The next Chair must be unambiguously committed to the 2 percent inflation target, credible on independence, pragmatic rather than doctrinaire, and experienced in the mechanics of liquidity and market functioning when term premia move. Continuity lowers risk premiums. Perceived regime change raises them.

Recent reporting has highlighted a short list that includes sitting and former Fed officials as well as White House advisers. Our view is straightforward. If the objective is continuity and minimal credibility risk, an experienced Fed leader with a strong inflation-fighting record is the cleanest outcome. If the objective is a sharp break, markets will demand a higher risk premium until credibility is re-established.

In this cycle, growth, disinflation, and lower rates are not in conflict. They are linked by productivity. The forecast rests less on policy easing and more on the economy’s improved ability to grow without overheating. We expect two quarter-point rate cuts this year, most likely in March and June, with a third cut possible if labor market conditions weaken convincingly or inflation returns to target more rapidly than expected.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 20, 2026

Mark Vitner, Chief Economist

704-458-4000