Cooling Cycles, Recalibrated Policy, and an Economy Pulling in Different

- Growth becomes increasingly uneven. The expansion continues, but affordability pressures and demographic shifts reshape spending patterns, hiring decisions, and regional performance.

- A virtually jobless start to 2026 is increasingly likely. Payroll gains slow sharply, but tighter immigration enforcement and weaker labor-force growth keeps unemployment from rising significantly.

- Policy calibration expected by spring. Border security tightens, but a “wide door” opens for needed skill sets; tariffs rotate away from broad-based levies toward exemptions for more foodstuffs, raw materials and goods not able to be produced domestically.

- Capital, not labor, remains the cycle’s backbone. AI infrastructure, energy systems, aerospace, defense, biopharma, and advanced manufacturing continue driving investment.

- Housing begins to stabilize. Mortgage rates drift toward 6% (and maybe a little less for short periods of time), inventories rise, and affordability slowly improves—setting the stage for a mid-2026 rebound.

- Lower interest rates and steadier sentiment revive inventory building. Inventory trends were erratic in 2025 as firms first raced to get ahead of tariffs and then paused while waiting for trade policy to settle and supply chains to be reconfigured. With interest rates drifting lower, tariff policy becoming less volatile, and consumer spending and fixed investment holding firm, we expect a modest but meaningful rebound in inventory building in 2026.

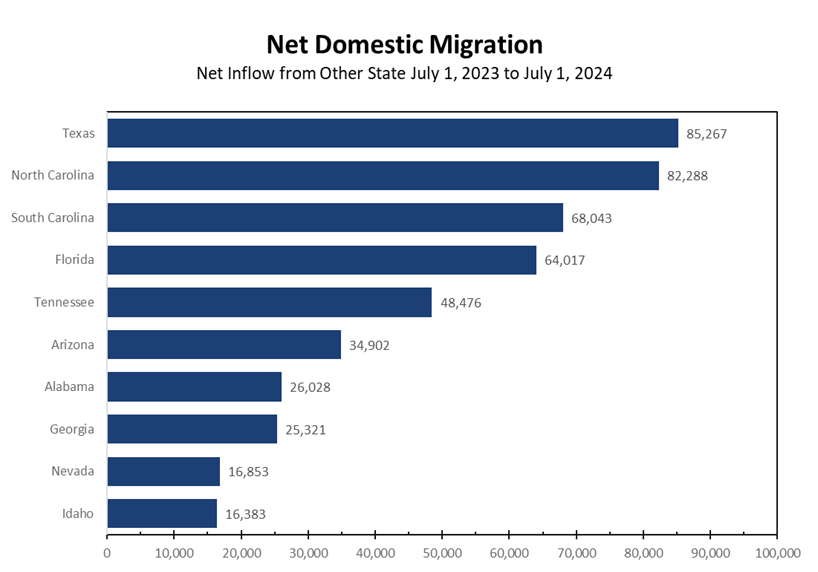

- Regional divergence widens. Two forces drive wider regional gaps in 2026. First, the fuller return to the office bolsters employment in office-adjacent sectors—retail, hospitality, and transportation—across major urban cores, including New York City, Boston, and Washington, D.C. Second, households and businesses continue migrating toward markets with more attainable housing, reinforcing growth in affordable, high-momentum regions. The Carolinas, Tennessee, Georgia, Florida, Alabama, Arkansas, and non-Triangle Texas metros are all notable standouts. Arizona, Utah, Idaho, Missouri, Ohio, and Indiana strengthen further, while Louisiana and Mississippi gain traction. The Texas Triangle, Colorado and Nevada cool as affordability ceilings and slower migration temper demand.

- Geopolitical risks remain elevated but more concentrated. The Russia–Ukraine conflict, instability across the Middle East, and U.S.–China strategic tensions continue to shape energy, trade, and supply-chain dynamics. While broad escalation risks have eased, localized flare-ups and policy missteps still pose outsized market impacts—making geopolitical communication risk a more important market variable.

Cooling Cycles, Rebuilding Foundations

As 2025 draws to a close, the U.S. economy is entering a more uneven, capital-intensive, and policy-sensitive phase of the expansion. The top-line data still points toward a soft landing, but the underlying distribution reveals an economy moving on several different tracks. Growth has cooled yet remains positive. Consumers are more selective rather than retrenching. Capital spending continues to anchor the cycle, while affordability pressures, trade volatility, and tighter immigration enforcement shape decisions in boardrooms and households alike.

The story of 2026 begins with this divergence. Younger households—who consume more relative to income as part of the life-cycle arc—face the sharpest affordability squeeze, particularly around housing, transportation, and services. Middle-income households remain constrained by accumulated price increases. Higher-income households continue to drive discretionary spending through wealth effects and better access to credit. The result is a consumer sector that looks resilient from altitude but is increasingly polarized at ground level.

Geography intensifies the divide. The nation’s growth map is tilting decisively toward affordability and industrial momentum. The Carolinas, Tennessee, Georgia, and Florida remain pillars of the expansion, but the outperforming regions now extend more broadly:

- Alabama’s I-65/I-565 industrial corridor and Gulf Coast—anchored by Birmingham, Huntsville–Decatur–Muscle Shoals, and Gulf Shores—continues to attract aerospace, automotive, defense, and logistics investment.

- Arkansas benefits from an expanding logistics, retail, and advanced-manufacturing ecosystem centered on Northwest Arkansas and the Mississippi River corridor.

- Louisiana and Mississippi gain ground through energy infrastructure, petrochemical capacity, port modernization, and manufacturing expansions from Baton Rouge to Gulfport-Biloxi and North Mississippi’s automotive cluster.

- Arizona and Utah remain two of the strongest performers nationwide, drawing semiconductor, data-center, finance, and tech investment, while consistently ranking among the fastest-growing states demographically.

- Idaho, even after cooling from its pandemic-era surge, remains a net beneficiary of affordability migration from higher-cost western states.

- Missouri, Ohio, and Indiana remain at the center of the rapidly growing EV, battery, aerospace, and defense supply-chain corridor—forming the backbone of a durable industrial renaissance.

- Texas metros outside the Triangle—including the Gulf Coast energy corridor, the Permian Basin, and the emerging industrial crescent between Amarillo, Lubbock, and Wichita Falls—show continued strength.

By contrast, the Texas Triangle (Dallas-Fort Worth-Houston-Austin), Colorado and Nevada have cooled, as affordability ceilings and slowing inbound migration weigh on hiring, housing formation, and broader economic momentum.

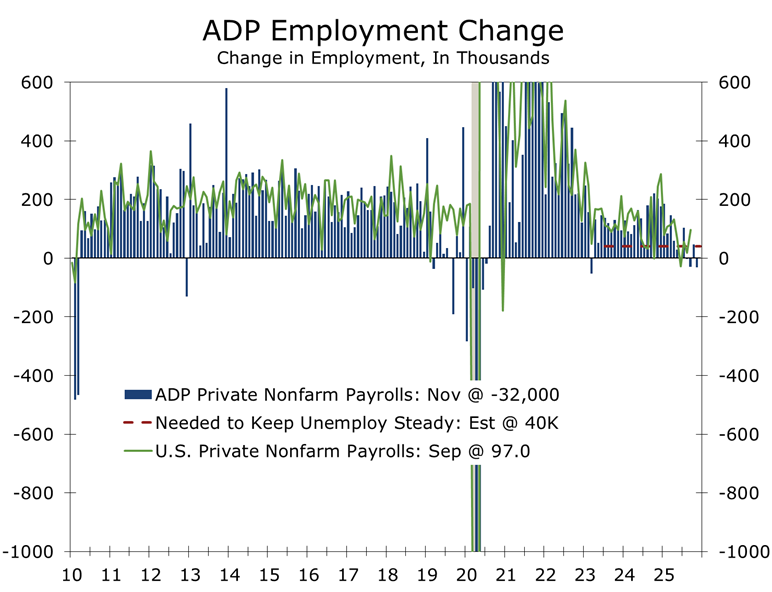

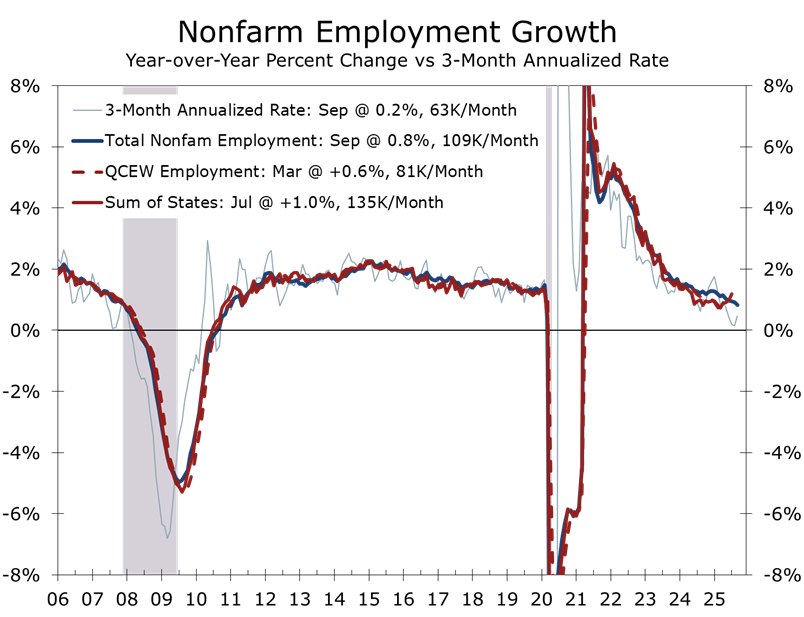

Labor-market dynamics tell a similar story. The first months of 2026 are increasingly likely to deliver what amounts to a virtually jobless expansion. High-frequency indicators—from ADP and online postings to diffusion indices—point toward minimal net hiring through late winter. Substantial downward revisions to 2024-2025 payrolls, expected in early February, will likely confirm the softening trend. Yet the unemployment rate is poised to rise only modestly. Slower labor-force growth—driven by demographic constraints, reduced participation among recent arrivals, and tighter immigration enforcement—lowers the break-even level of job creation. Employers remain reluctant to cut staff but equally hesitant to add headcount, producing a labor market that cools sharply without breaking.

These dynamics set the stage for a policy pivot by spring. With the midterms approaching and economic crosscurrents mounting, the Trump Administration is likely to recalibrate at the margins. Border security will remain central, but we expect the Administration to pair a tighter perimeter with a “wide door” for strategically needed skill sets in AI, energy, aerospace, logistics, and advanced manufacturing. A similar adjustment appears likely on tariffs: as negotiations deepen and USMCA deliberations unfold, we expect a rotation away from broad-based levies toward exemptions for foodstuffs, goods and raw materials not produced domestically. That would ease pressure on household budgets and small businesses while preserving strategic leverage against key trading partners.

These economic and policy crosswinds set the stage for evaluating our Top Calls for 2025 and laying out a sharpened and forward-leaning set of Key Calls for 2026. If 2025 was the year the economy cooled without cracking, 2026 is shaping up to be the year the expansion grows with fewer workers, more capital, and increasingly calibrated policy.

Looking Back at our Top Calls for 2025 — Graded and Expanded

- The U.S. Economy Would Enter 2025 with More Momentum Than Consensus Expected

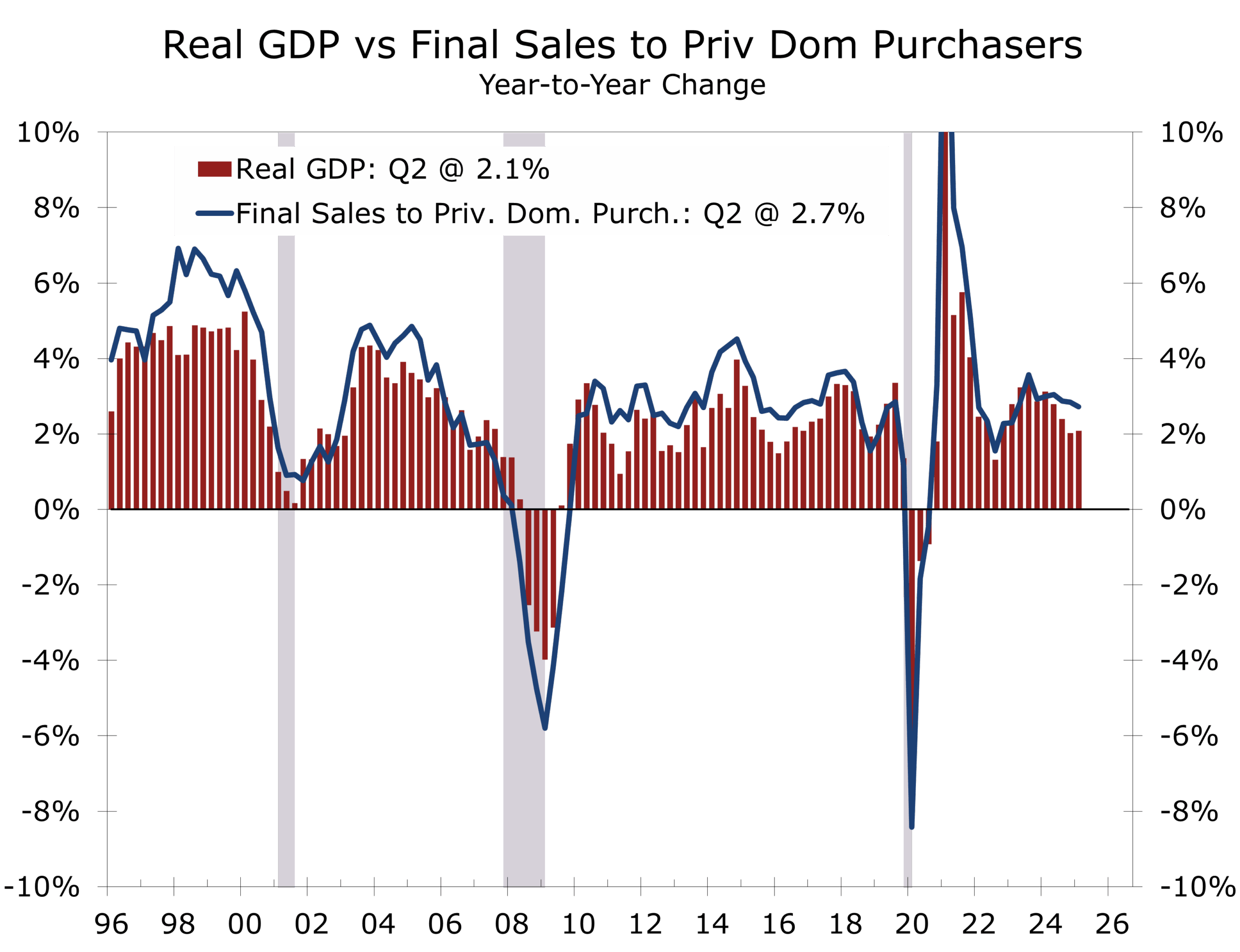

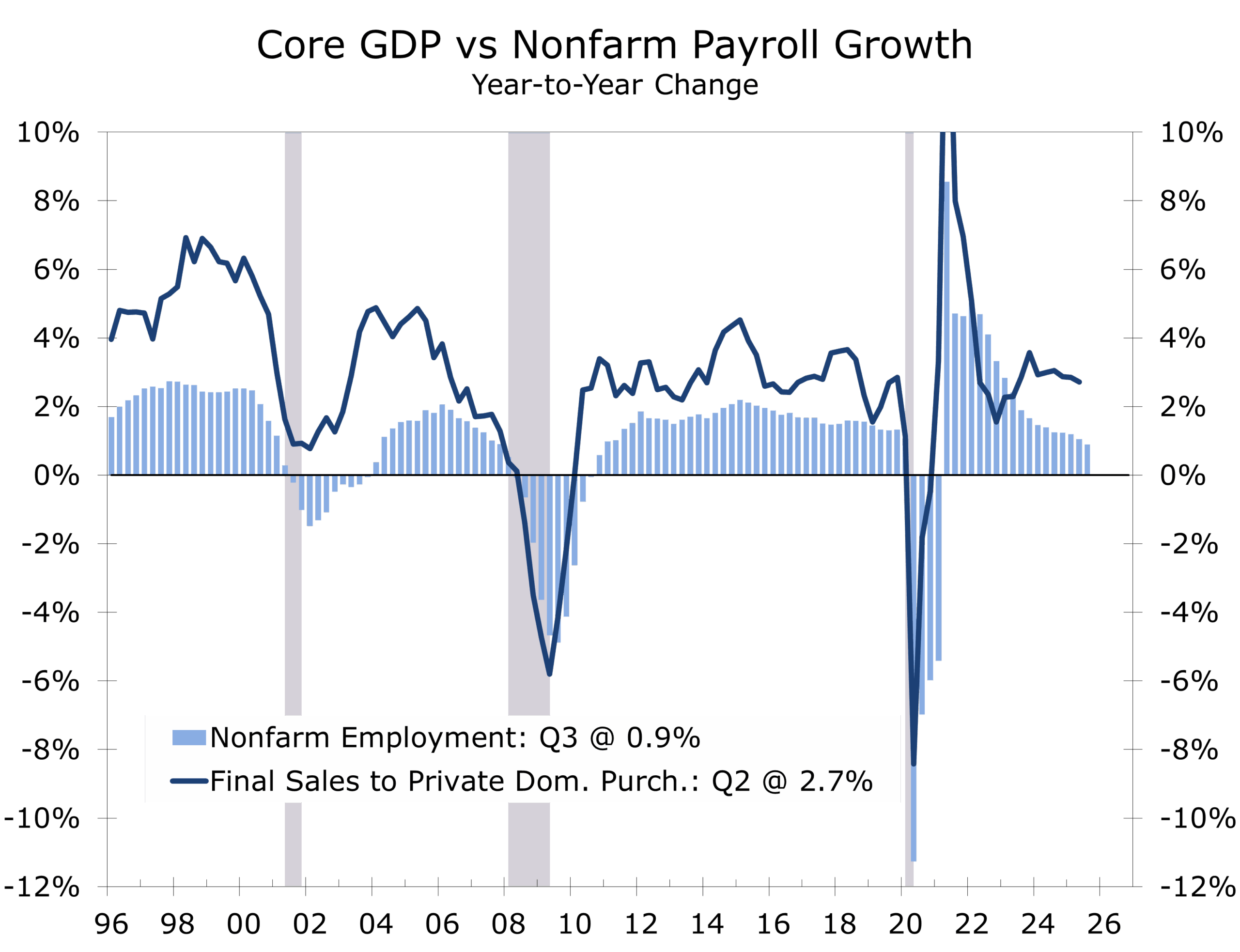

While real GDP swung widely from quarter to quarter, underlying demand remained firm. Real Final Sales to Private Domestic Purchasers—what we refer to as “Core GDP”—likely maintained a better than 2.5% pace into year-end, underscoring stronger momentum than most forecasters anticipated. Private final domestic demand was supported by services spending, business fixed investment, and an unusually long tail of major construction projects. Consumption softened slightly but held up well enough to avoid a more pronounced downshift.

Verdict: Correct.

- Beneath the Surface, Momentum Would Be Softer Than the Headlines

We consistently warned that headline payroll data overstated true labor-market strength. The Quarterly Census of Employment and Wages (QCEW) and state data showed materially slower job creation than the closely watched establishment survey. Diffusion indices narrowed all year, reflecting reduced breadth in hiring.

Verdict: Correct.

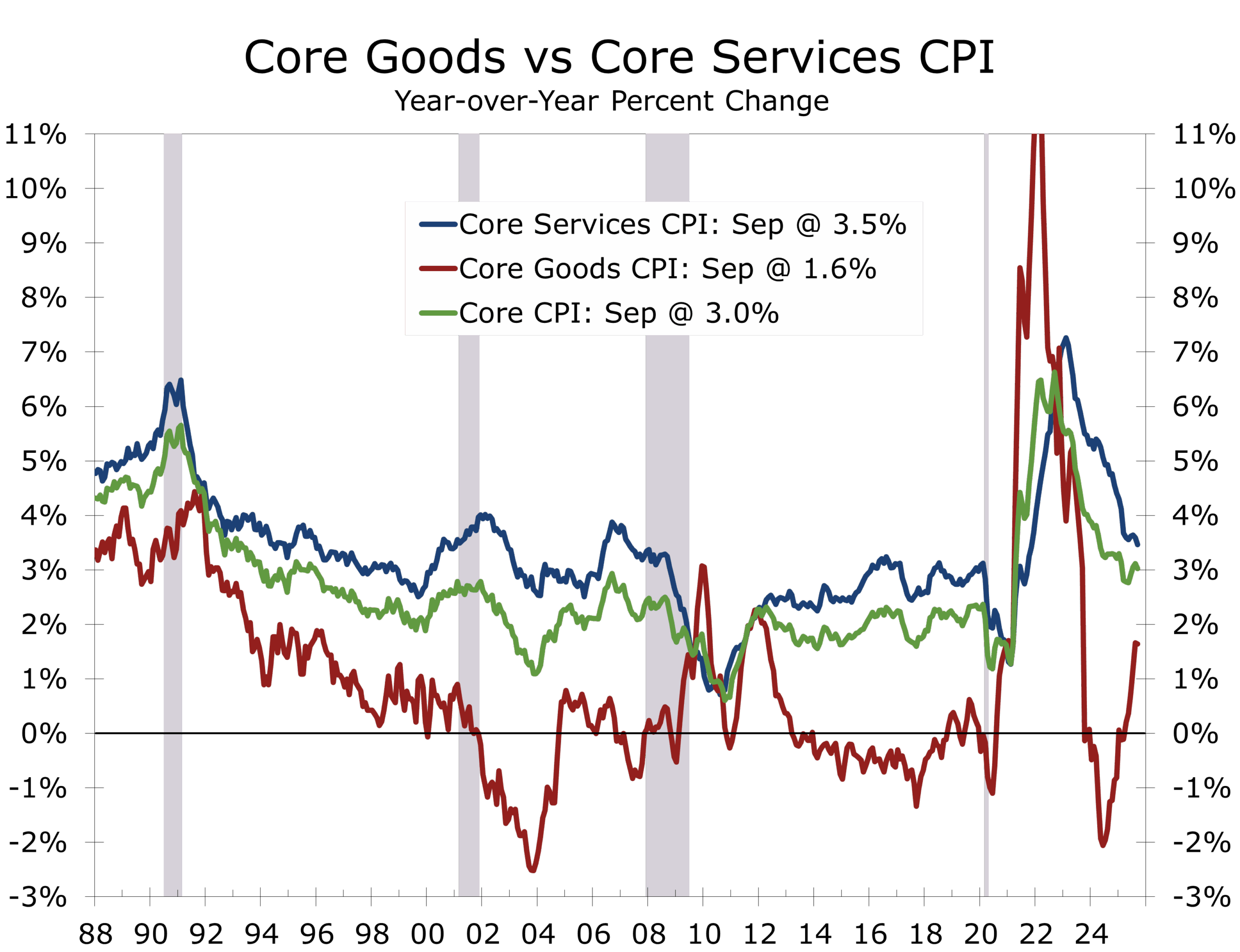

- Inflation Progress Would Stall, With Sticky Core Services

Shelter, insurance, and medical services slowed the descent of inflation earlier in the year. Goods disinflation continued, but sticky components of the CPI basket kept overall progress gradual. We expected tariffs to lift goods inflation in the second half, with the impulse peaking around year-end.

Verdict: Correct.

- Fed Easing Would Be Limited — Fewer Cuts Than Markets Expected

The Fed maintained a cautious posture, prioritizing credibility over speed. We argued that the Fed could accomplish more by doing less—and by communicating that conviction (“A December cut is not a sure thing – far from it.”) clearly. The first meaningful rate cuts were delayed until late summer, as uncertainty surrounding tariffs and initially strong reported job growth complicated the easing case.

Verdict: Correct.

- Long-Term Rates Had Moved into a New Structural Range

The 10-year Treasury traded in a 4.20%–4.80% band for most of the year, reflecting a higher term premium, large and persistent fiscal deficits, and firmer potential growth. Markets steadily adjusted to this new equilibrium. Yields drifted toward 4% after the September rate cut and retested that level during the elongated government shutdown, amid concern that the AI boom might grossly misprice risk and inflate asset valuations.

Verdict: Mostly Correct.

- Tariffs Would Rise, But Their Inflation Impact Would Be Modest

We anticipated the effective tariff rate rising from 2.5% to roughly 10%, while the inflation impact remained limited. Even with more aggressive rhetoric and tactics than expected, the actual pass-through to consumer prices proved far more muted than many feared. We consistently argued that consumers would resist meaningful price increases—given slower income growth and depleted excess savings—and that the pandemic-era inflation spike reflected extraordinary factors (stimulus payments, outsized fiscal spending, and an overly accommodative Fed) that were no longer operative. Moreover, unless the Fed accommodated the rise in tariffs, higher import prices would leave consumers with less money to spend on services, which would slow price increases there.

We also went to great lengths to emphasize that tariffs are assessed on the landed value of goods—net of shipping, insurance, and financing costs—not on retail prices, which significantly reduces the consumer-facing inflation impulse. In the end, the largest tariff effect was supply-chain adaptation, not consumer inflation.

Verdict: Correct in Substance.

- Housing Would Be a Drag Through at Least the Second Half of 2025

Elevated mortgage rates constrained resale supply and sidelined buyers. Builder incentives helped lift new-home sales in the fall, but affordability remained the dominant headwind, and rising concerns about job security kept many prospective buyers on the sidelines late in the year. Home prices have been gradually correcting, a necessary step toward restoring affordability and setting the stage for a more durable recovery in 2026.

Verdict: Correct.

- A Late-2025 Mortgage Repricing Window Would Begin to Open

Funding conditions and mortgage spreads showed meaningful early improvement, though not enough to materially shift demand before year-end. The groundwork for a 2026 improvement is clearly in place.

Verdict: Too Early to Call.

- Capital Spending Would Remain the Cycle’s Backbone

AI infrastructure, aerospace, defense, energy systems, and long-lead industrial projects continued advancing even as consumer spending slowed. Investment remained the most reliable engine of growth throughout the year.

Verdict: Correct.

- Market Volatility Would Rise as Growth Remained Firm and Yields Remained High

Equity markets grew increasingly sensitive to long-end yields, and volatility rose as the 10-year moved above 4.5%. Rate dynamics—more than Fed communication—drove the bulk of market repricing.

Verdict: Correct.

- Trump’s Trade Strategy Would Emphasize Negotiation, Not Extremes

Policy signals out of Washington leaned heavily on leverage and renegotiation rather than broad tariff escalation. The unexpectedly large “Liberation Day” tariffs served to strengthen the U.S. negotiating position and enabled more comprehensive trade discussions. Businesses adapted quickly, reducing policy risk.

Verdict: Correct.

- A Russia–Ukraine Framework Would Require NATO/EU Guarantees

Diplomatic readouts confirmed that any workable settlement must be anchored in credible security guarantees. This framework remains central to ongoing negotiations.

Verdict: Correct.

- Middle East Stability Would Hinge on a Ceasefire Plus Abraham Accords Expansion

The region moved incrementally closer to long-term normalization, though progress varied significantly across theaters. While the direction aligned with expectations, timelines slipped. Israel’s geopolitical isolation has increased, complicating any durable peace agreement. Rebuilding Gaza and fully integrating Saudi Arabia into the Abraham Accords will require a credible path to a Palestinian state or autonomy.

Verdict: Mostly Correct.

- China Would Study Ukraine as a Blueprint for Sanctions Resistance

China accelerated efforts to build supply-chain redundancy, develop alternative financial channels, and hedge against sanctions risk. Japan and Southeast Asia undertook similar adjustments.

Verdict: Correct.

- Global Political Turnover Would Raise Market Uncertainty

Elections across major economies introduced new rounds of volatility in currency and bond markets. Investors priced political risk more explicitly, with Japan serving as the most recent example.

Verdict: Correct.

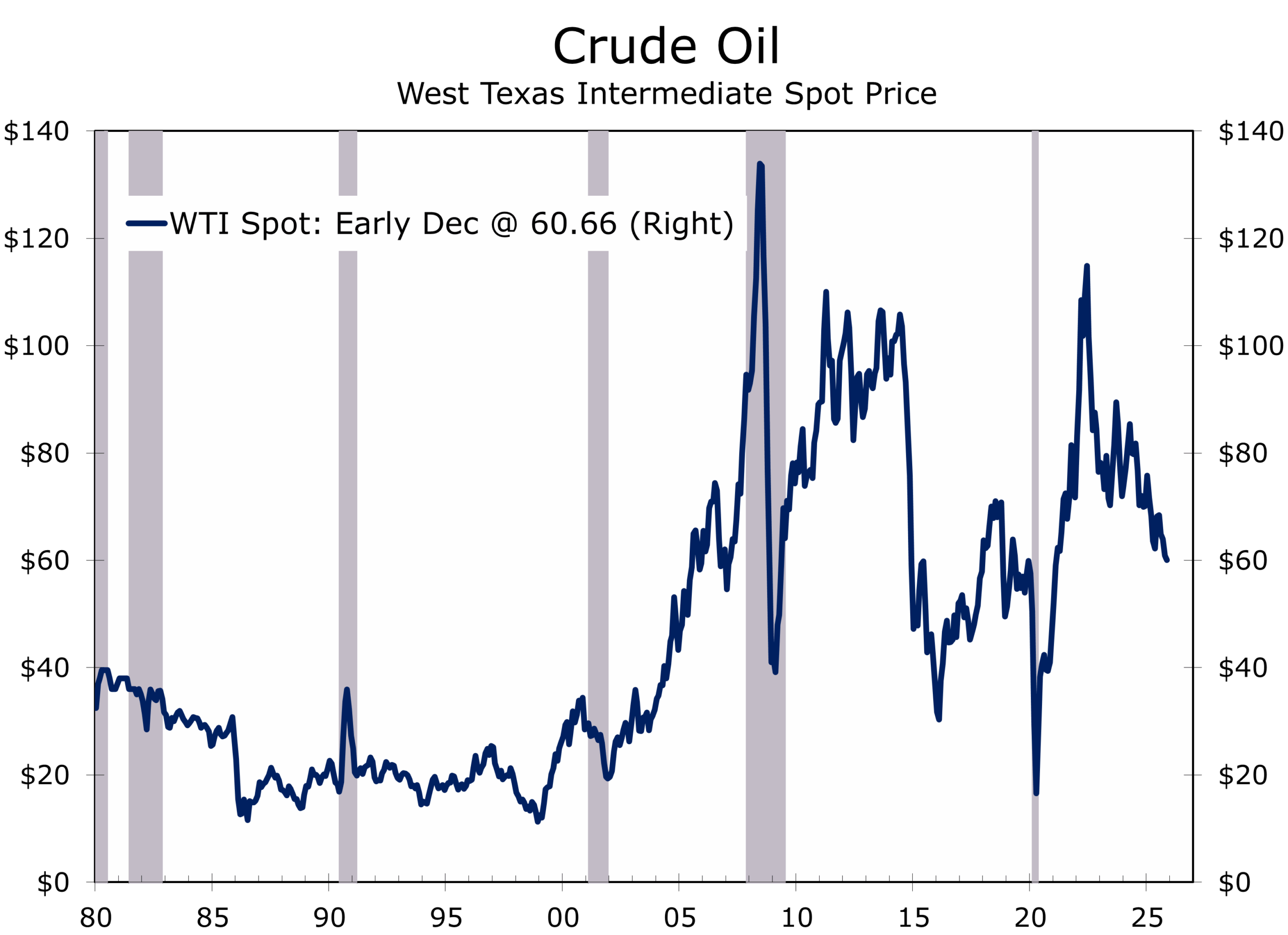

- The U.S. Would Make It Easier for Domestic Energy Producers and Lean on Saudi Arabia to Pressure Oil Toward $60/bbl.

U.S.–Saudi coordination signaled a preference for maintaining higher output to pressure Russia and support broader diplomatic objectives. Oil prices softened substantially during the year—including brief dips near $60/bbl., depending on the benchmark used—though not consistently enough to verify the full thesis.

Verdict: Directionally Correct — Awaiting Full Confirmation.

Key Calls for 2026

- A Softish Landing Early in 2026, Followed by a More Durable Expansion

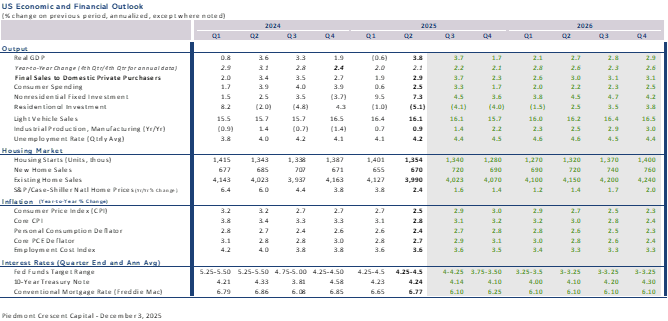

The government shutdown lasted longer and proved more disruptive than expected, with mounting pressure on air travel finally breaking the stalemate. After a surprisingly strong third quarter, we look for Q4 GDP to slip below 2% and for early 2026 to begin slowly. Business fixed investment remains the cycle’s anchor, led by AI infrastructure, biopharmaceuticals, energy and power, and selected reshoring initiatives. By spring, larger tax refunds and a nascent recovery in home buying should lift growth back toward 2.5%.

2026 Call: Stronger-than-consensus GDP growth, with real GDP rising at a 2.6% annual rate. The latest Survey of Professional Forecasts pegs 2026 growth at 1.8% and the OECD forecast for the U.S. is currently at 1.6%.

- A Capital-Led Expansion Defines the Cycle

AI infrastructure, power systems, aerospace, defense, biopharma, and advanced manufacturing remain the most durable engines of growth. These sectors are anchored in structural investment cycles and rising foreign direct investment and are far less sensitive to household sentiment.

2026 Call: Private fixed investment posts one of its strongest multi-sector performances in decades.

- The Consumer Reset Takes Hold

Consumers remain constrained by affordability pressures rather than job insecurity. Real wage gains strengthen as inflation cools, supporting firmer spending in the second half. Rising home sales also revive durable-goods spending.

2026 Call: Early caution gives way to a gradual firming in consumer activity by mid-year.

- Housing Rebounds as Inventory Improves and Mortgage Rates Drift Toward 6%

Existing home inventories are rising from historically low levels as market leverage shifts from sellers to buyers. Single-family homebuilding has slowed as pandemic-delayed projects reach completion, and builders have turned toward incentives to clear inventory. Lower mortgage rates and modest price declines should bring more buyers back into the market.

2026 Call: Housing transitions from a drag to a stabilizing force by mid-2026 and becomes a modest positive by late summer and fall.

- Employment Conditions: A Soft Patch Early in the Year, Followed by Gradual Firming

With September still the latest official payroll print, high-frequency indicators—including ADP’s measures—continue to point toward downside risk in private payroll growth, and large downward revisions to 2025 employment expected in early February add further caution. The preliminary QCEW data imply that 911,000 fewer jobs were created from March 2024 to March 2025—roughly 76,000 per month. That slower trend likely extends into the remaining months of 2025. We expect labor-market conditions to remain under pressure early in the year, with monthly nonfarm job growth hovering near zero during the first few months of 2026 before gradually improving to roughly 60,000 per month by year-end. The unemployment rate is likely to rise only modestly, reflecting unusually slow labor-force growth, while wage pressures ease further, with the Employment Cost Index advancing between 3.0% and 3.5%.

2026 Call: The labor market cools sharply early in the year but avoids a deeper contraction, stabilizing by midyear with moderate job creation and easing wage growth.

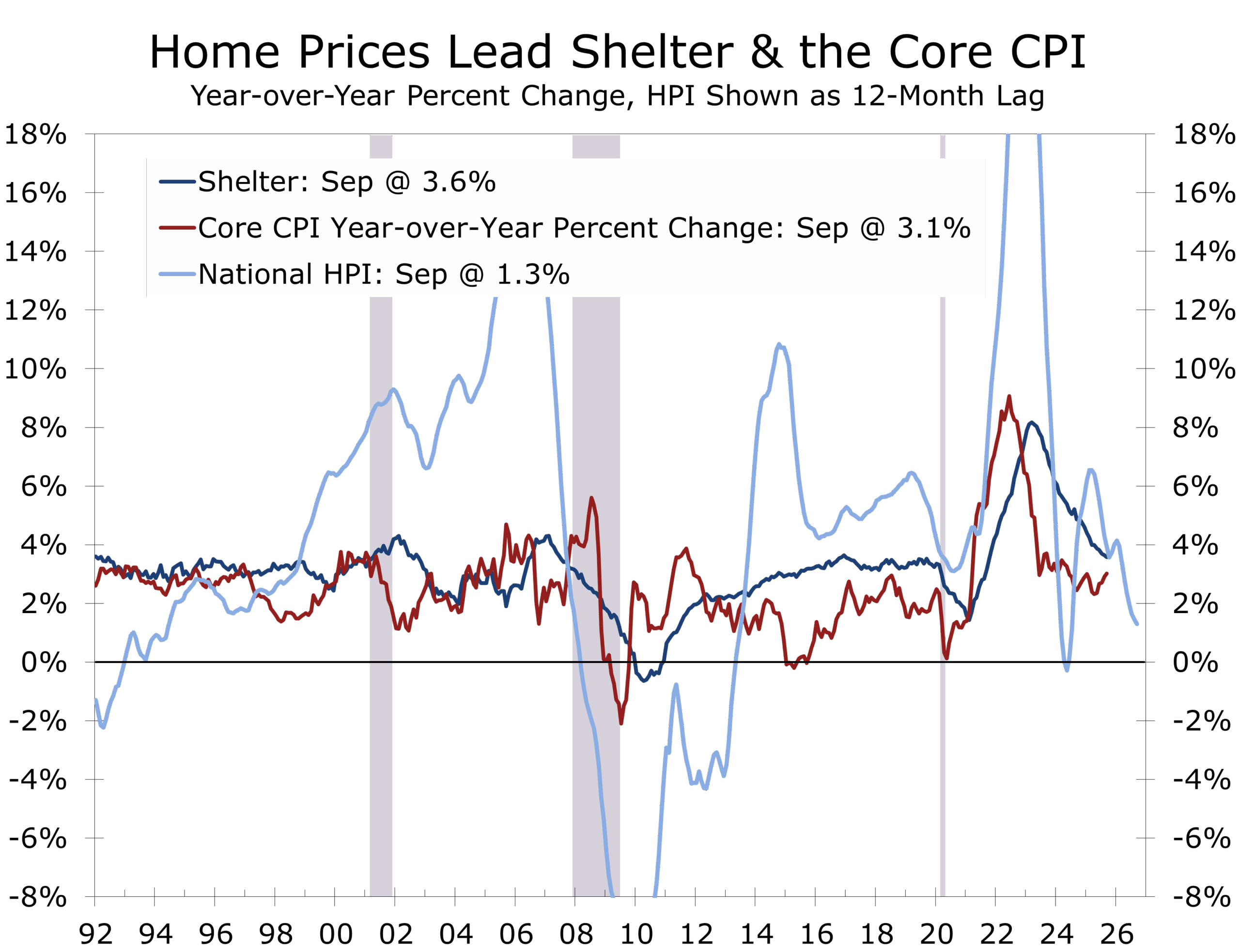

- Shelter Disinflation Drives Core CPI Toward the Fed’s Comfort Zone

Cooling home prices nationwide signal the onset of sustained shelter disinflation. With rents lagging home prices by 9–12 months, the CPI’s largest component finally begins to ease, reinforced by a surge of new rental supply.

2026 Call: Shelter CPI slows to 3% or less, pulling core inflation back under 2.5% by yearend.

- The Fed Executes a Long, Shallow Cutting Cycle

The Fed continues to prioritize credibility and careful calibration over rapid easing. Following the December rate cut, policymakers signal that subsequent cuts will proceed gradually, with an elongated cycle extending through mid-year and the federal funds rate hovering near 3% for much of 2026. The base case calls for quarter point cuts at alternating meetings during the first half of 2026.

2026 Call: The policy rate trends lower but not dramatically. We see the Fed cutting rates at alternative meetings in 2026, with at least two cuts.

- Firms Adapt to Tariff Volatility Faster Than Policymakers Adapt Policy

Businesses increasingly treat policy volatility as a structural feature rather than a temporary disruption. This reduces macro uncertainty and encourages renewed investment in supply-chain diversification, automation, and information technologies.

2026 Call: Tariff noise persists, but private-sector adaptation neutralizes most of the disruption.

- Energy Turns Disinflationary as the LNG Wave Arrives and Risk Premia Ease

A major wave of LNG supply, combined with a softer geopolitical premium, puts sustained downward pressure on natural gas and electricity prices. This shift provides relief for both households and industry.

2026 Call: Energy becomes a structural disinflationary force throughout the year.

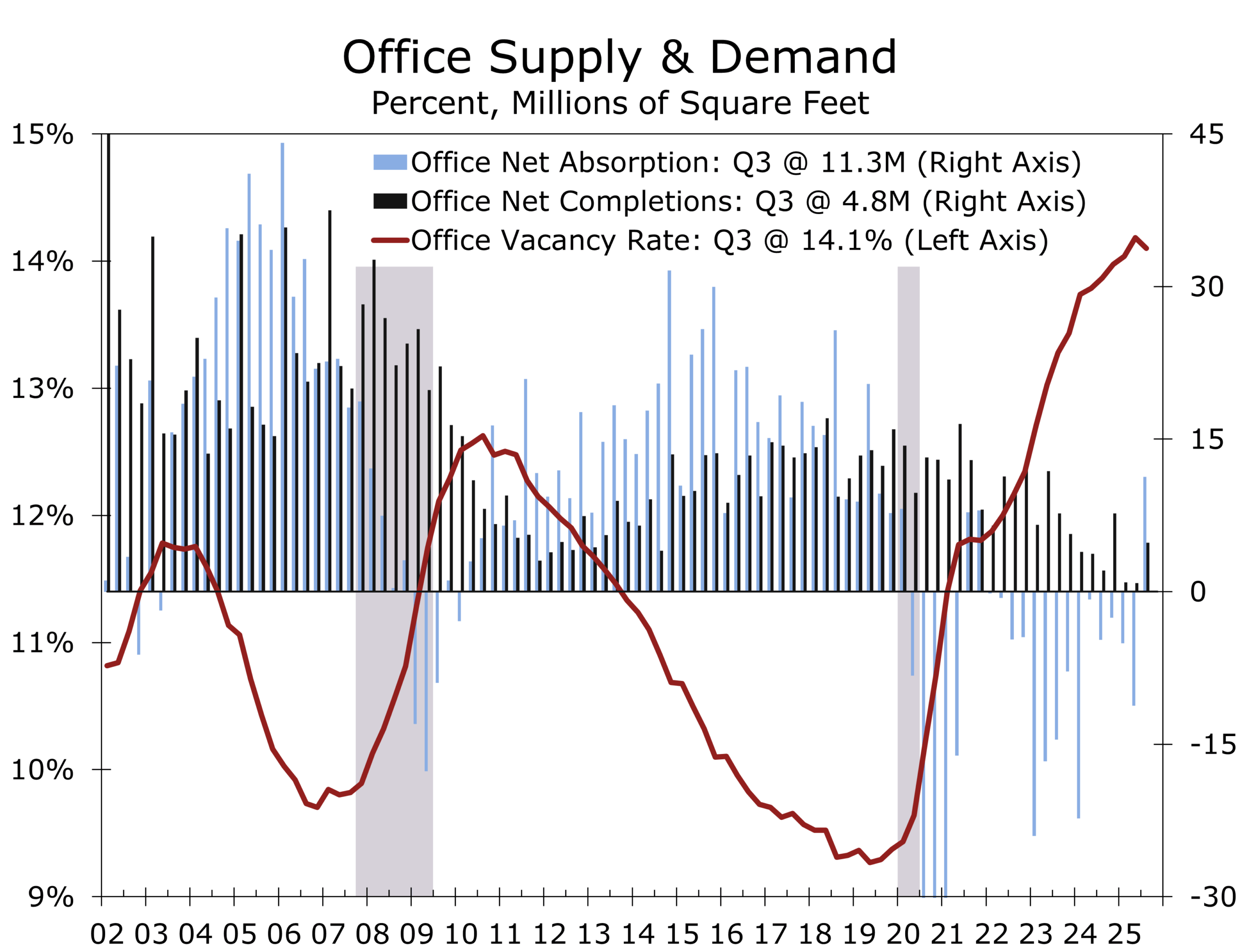

- Office and CRE Reach a True Trough

Construction pipelines have cleared, and absorption is improving across high-quality urban assets. Landlords are repositioning properties more aggressively, signaling a bottoming process. Selective markets will see meaningful new construction.

2026 Call: 2026 marks the trough for the office market and CRE more broadly, with selective recovery emerging late in the year.

- The Sunbelt Reasserts Its Role as America’s Growth Engine

Migration continues to favor the South, where affordability and industrial development remain compelling. These dynamics support faster job growth and stronger capital spending relative to national averages.

2026 Call: The Carolinas, Tennessee, Georgia, Texas, and Florida again outpace national growth. Virginia, Alabama, and Arkansas see notable gains. Outside the South, Arizona and Utah remain notable outliers, while the Midwest – particularly Indiana, Ohio, and Missouri – continues to experience an industrial renaissance.

- Global Investment Becomes a Macro Variable

International investment flows into the U.S. continue rising, especially in energy systems, AI infrastructure, the automotive sector, biopharmaceuticals and advanced manufacturing. These inflows deliver both geopolitical leverage and macroeconomic tailwinds.

2026 Call: Foreign direct investment boosts productivity and strengthens long-run potential growth.

- China’s “Ukraine Lesson” Reshapes Global Supply Chains

China’s efforts to hedge against sanctions risk accelerate diversification into Southeast Asia and drive broader supply-chain reshaping. Regionalization and redundancy increase across global production networks.

2026 Call: Supply chains become more capital-intensive and structurally disinflationary.

- Oil Trades in a Narrow, Lower Range

Growing LNG supply, steady Saudi output, and improved European energy posture limit oil’s upside. Geopolitical flare-ups still occur but exert less influence on pricing.

2026 Call: Oil prices remain range-bound ($55–$65/barrel) with a slight downward bias, resulting from a confluence of geopolitical influences, technological gains and regulatory changes.

- Narrative Shocks Become More Market-Relevant Than Data Shocks

Institutional trust and political communication increasingly shape market reactions. Messaging missteps produce sharper volatility than typical data releases—especially as midterm campaigning intensifies. This is particularly true for the Fed, which must convince the bond market that it can simultaneously support growth and contain inflation.

2026 Call: Communication risk overtakes data risk.

- The Inventory Cycle Turns Positive in Late 2026

With interest rates lower and downside risks to consumer spending easing, inventories normalize and begin contributing to headline growth. Reshoring projects move from construction to production, streamlining supply chains.

2026 Call: Industrial production strengthens meaningfully by year-end.

- The Expansion Catches Its Second Wind

The 2026 expansion gains renewed traction as early-year softness gives way to a firmer, more broad-based upturn. The labor market stabilizes after a near-jobless stretch, helped by easing wage pressures, lower interest rates, and a gradual pickup in hiring. Housing begins to re-engage as mortgage rates drift toward 6% and inventories improve. Capital spending—already the cycle’s backbone—broadens beyond AI infrastructure and energy systems into transportation, aerospace, and advanced manufacturing, reinforcing momentum across the most competitive regions of the country. Policy recalibration provides an additional tailwind: tighter border security paired with a targeted skills door alleviates pressure points in the labor market, while more selective tariff relief tempers cost burdens for households and small businesses.

2026 Call: Combined, these forces allow the expansion to catch its second wind—shifting from a narrow, capital-led phase into a more durable and better-balanced trajectory heading into the second half of the year.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 8, 2025

Mark Vitner, Chief Economist

704-458-4000