Inflation Continues to Run Hot

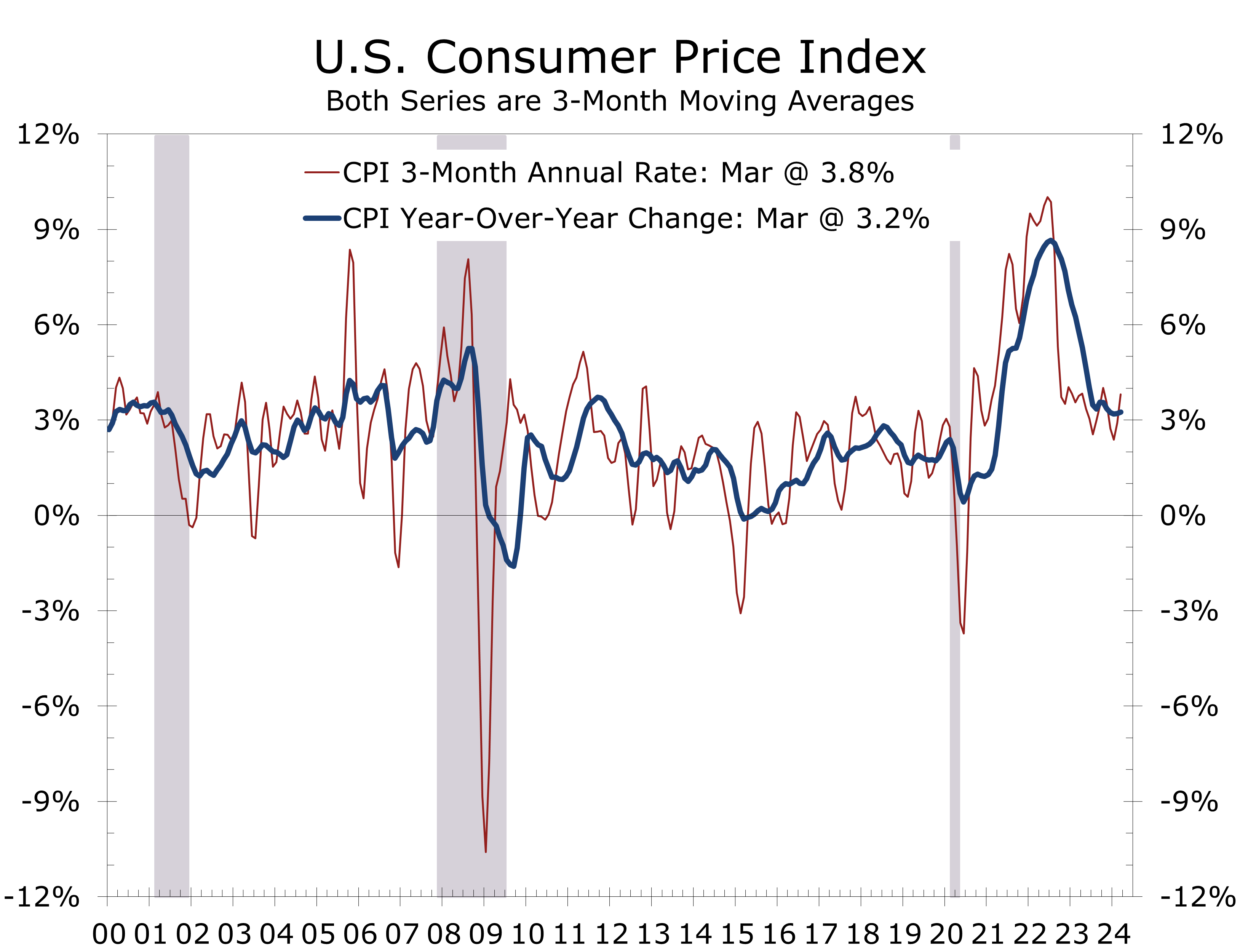

- Both the headline and core CPI rose 0.4% in March, matching gains for the prior month and besting the consensus by 0.1 percentage point. The overall CPI is now up 3.5% over the past year, while the core CPI is up 3.8%.

- We have continuously warned our readers the inflation data would come in hot during the first few months of 2024, reflecting higher labor costs, some catchup in insurance costs, and ongoing seasonal adjustment issues.

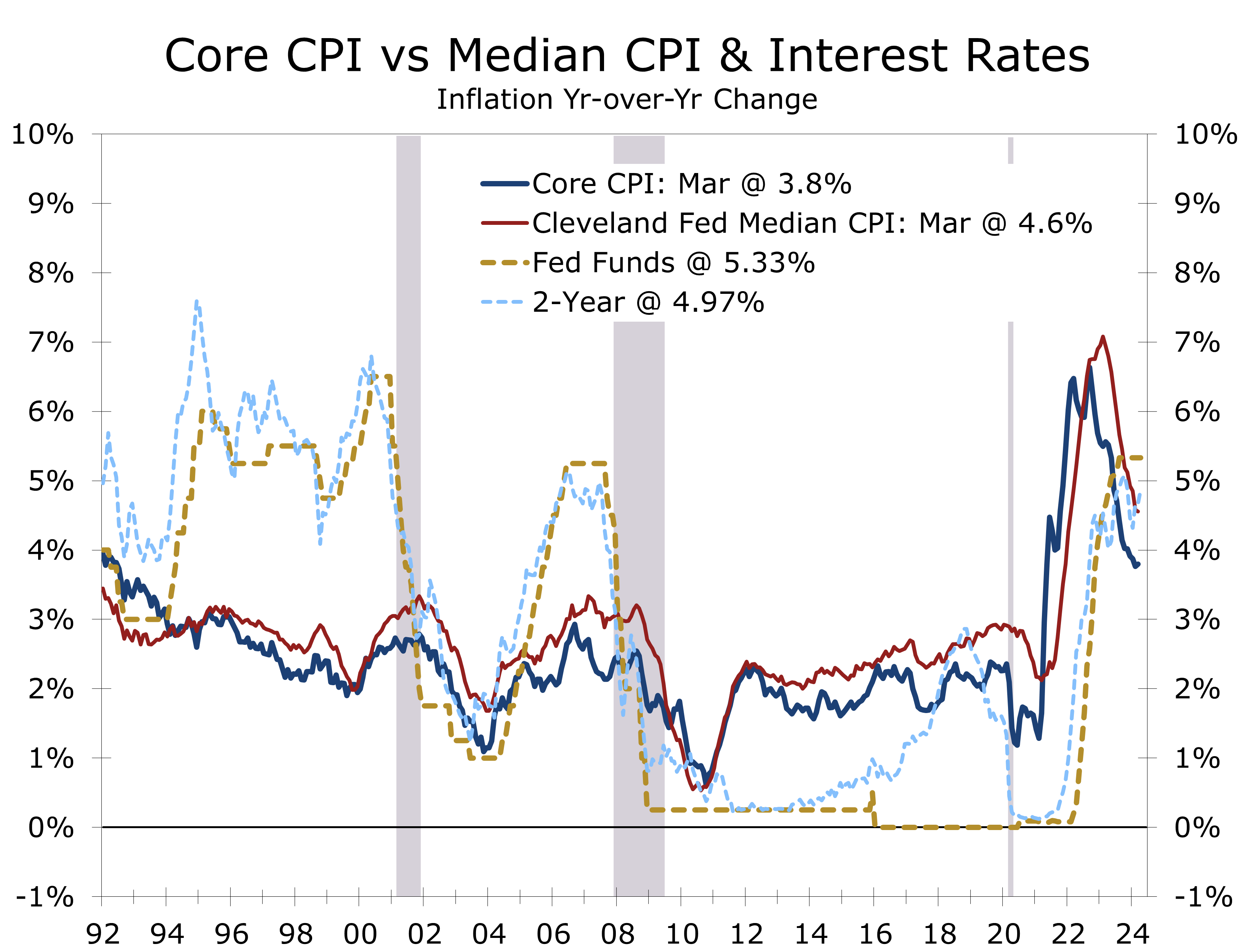

- While a handful of items, including motor vehicle insurance, auto reports and health care posted outsized gains in March, price increases continue to be fairly broad based. The median CPI rose 0.4% and is up 4.6% over the past year, while the trimmed mean rose 0.3% and is up 3.6% year-to-year.

- Energy prices rose 1.1% in March, with gasoline prices jumping 1.7% and electricity prices rising 0.9%. Food prices were tame, with grocery store prices unchanged for the second month in a row.

- Higher inflation will make it tougher for the Fed to cut interest rates. We expect the data to improve this summer, however, and look for job growth to moderate. Two cuts are now more appropriate than three, with the first in July, followed by another in September.

The latest inflation data surprised the financial markets, revealing that the higher-than-expected inflation reported earlier this year persisted into March. The Consumer Price Index (CPI) increased by 0.4% in March, matching the gains of the previous month. Prices excluding food and energy items, the so-called core CPI, also rose 0.4%, marking the third consecutive month the core CPI rose by that amount.

This uptick in inflation represents a bit of a reversal. The headline CPI surged at a 3.8% annual rate in the first three months of this year, bouncing back from a brief dip below 3% a few months ago.

The higher inflation figures for the past few months cast doubt on the sharp deceleration posted this past year. That earlier drop was mostly due to lower energy prices, which reversed late last year. Prices for other goods and services have also moderated.

The sharp moderation in the CPI since mid-2022 appears to have pivoted to a slower trajectory.

We look for inflation to moderate further this year but much less dramatically than it did from mid-2022 to late last year. Prices for labor-intensive services remain one of the greatest challenges, as do housing costs. Geopolitical risks could also slow progress by elevating oil prices and shipping costs.

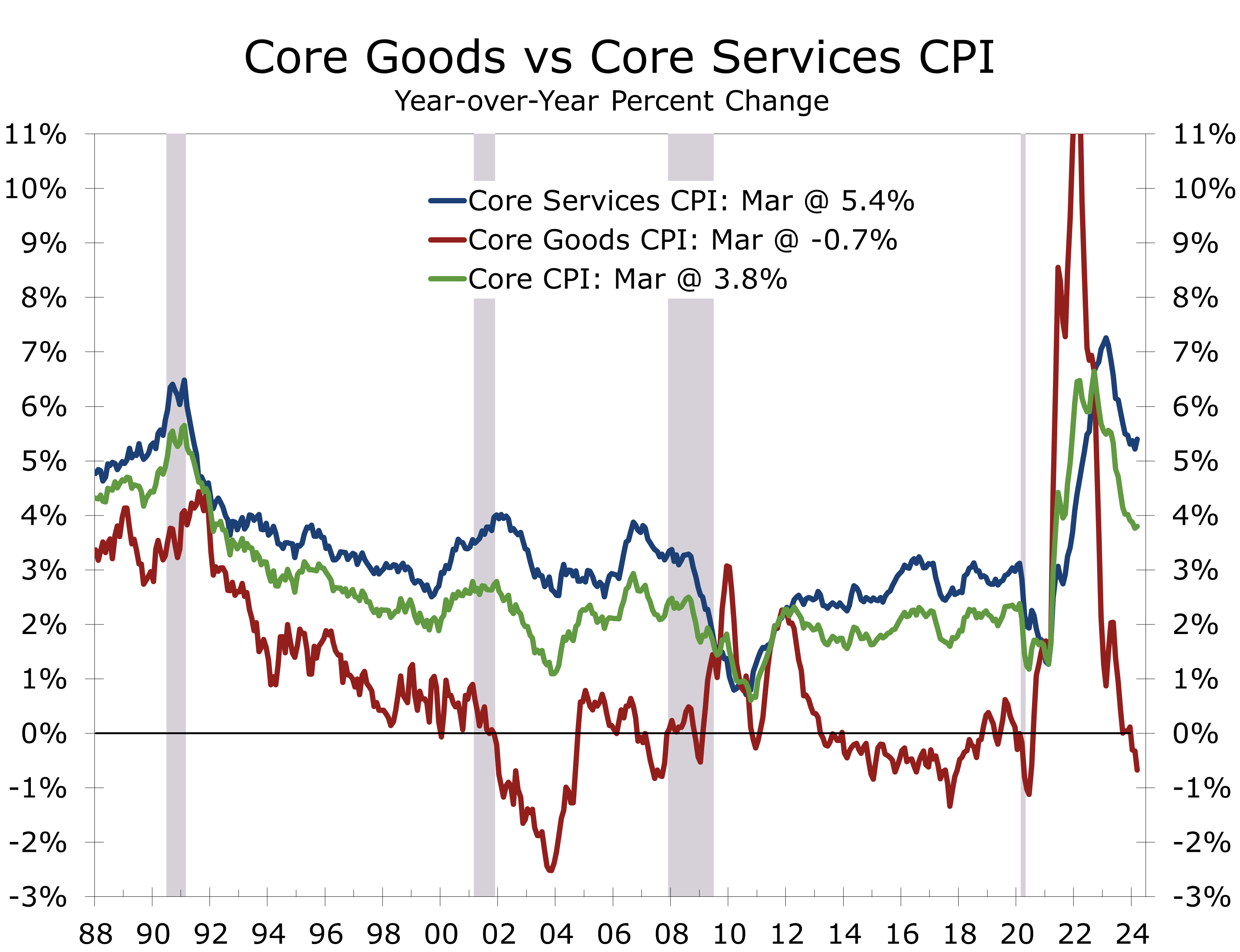

The Fed pays more attention to core inflation, with the Core PCE deflator being their preferred measure. The Core CPI and core PCE deflator do not match up perfectly but tend to move together over time. Core inflation has moderated less than the headline has. The primary impediment has been stubborn core services prices. Core goods prices have actually fallen 0.7% over the past year, reflecting large year-to-year drops in a variety of products, including used cars (-2.2%), furniture and bedding (-3.8%), major household appliances (-6.3%) and sporting goods (-2.2%).

Prices for motor vehicles and major household items have fallen this past year.

The drop in core goods prices followed a spike in the aftermath of the pandemic when consumers spent freely for discretionary goods, pulling prices higher. Goods prices have eased more recently, as spending has shifted to services, supply shortages have abated, and China has ramped up exports to the U.S.

Core services prices have moderated more slowly, having peaked at 7.3% year-to-year back in February 2023. Prices have gradually ebbed lower over the past year, although they picked up this past month following huge increases in motor vehicle insurance (+2.6%) and motor vehicle repairs (+1.7%). On a year-to-year basis insurance costs is up a whopping 22.2%, while vehicle repair costs are up 8.2%.

Shelter costs are another problem area. While asking rents for new apartments have come down recently, renewal rates have continued to increase. Rents for single-family homes are also proving more resilient. Owners’ equivalent rent and rent of primary residence both rose 0.4% in March and remain up 5.9% and 5.7% year-to-year, respectively.

We continue to see inflation moderating this year. Residual seasonality has bolstered prices in the first half of recent years and this trend appears to have been accentuated by the pandemic. Prices increases have tended to be smaller in the second half of the year – a pattern we expect to be repeated this year.

Residual seasonality has tended to bolster prices during the first half of recent years.

We expect inflation to moderate slightly this spring and look for the pace of disinflation to accelerate this summer and fall. We doubt we will see enough progress at reducing inflation in order for the Fed to reduce rates in June and are pushing out our first rate cut to July. We are now looking for just two quarter point cuts this year and look for the Fed to ultimately cut the federal funds rate to around 4.50% in this cycle.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

Mark Vitner, Chief Economist

Piedmont Crescent Capital

704-458-4000