Markets Find Comfort in Softer Inflation Data

- The headline CPI increased by 0.4%, driven by energy (+2.6%) and food prices (+0.3%).

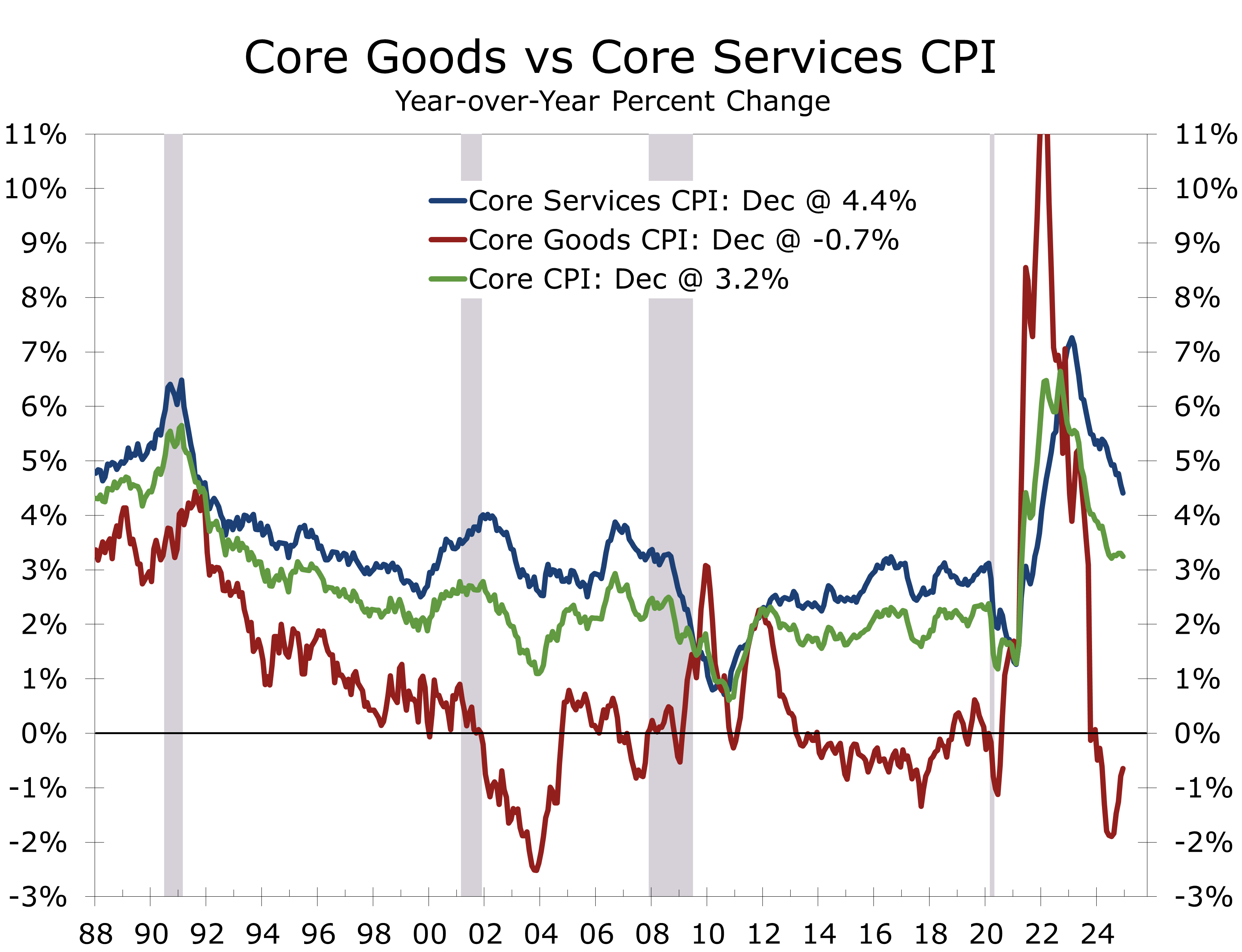

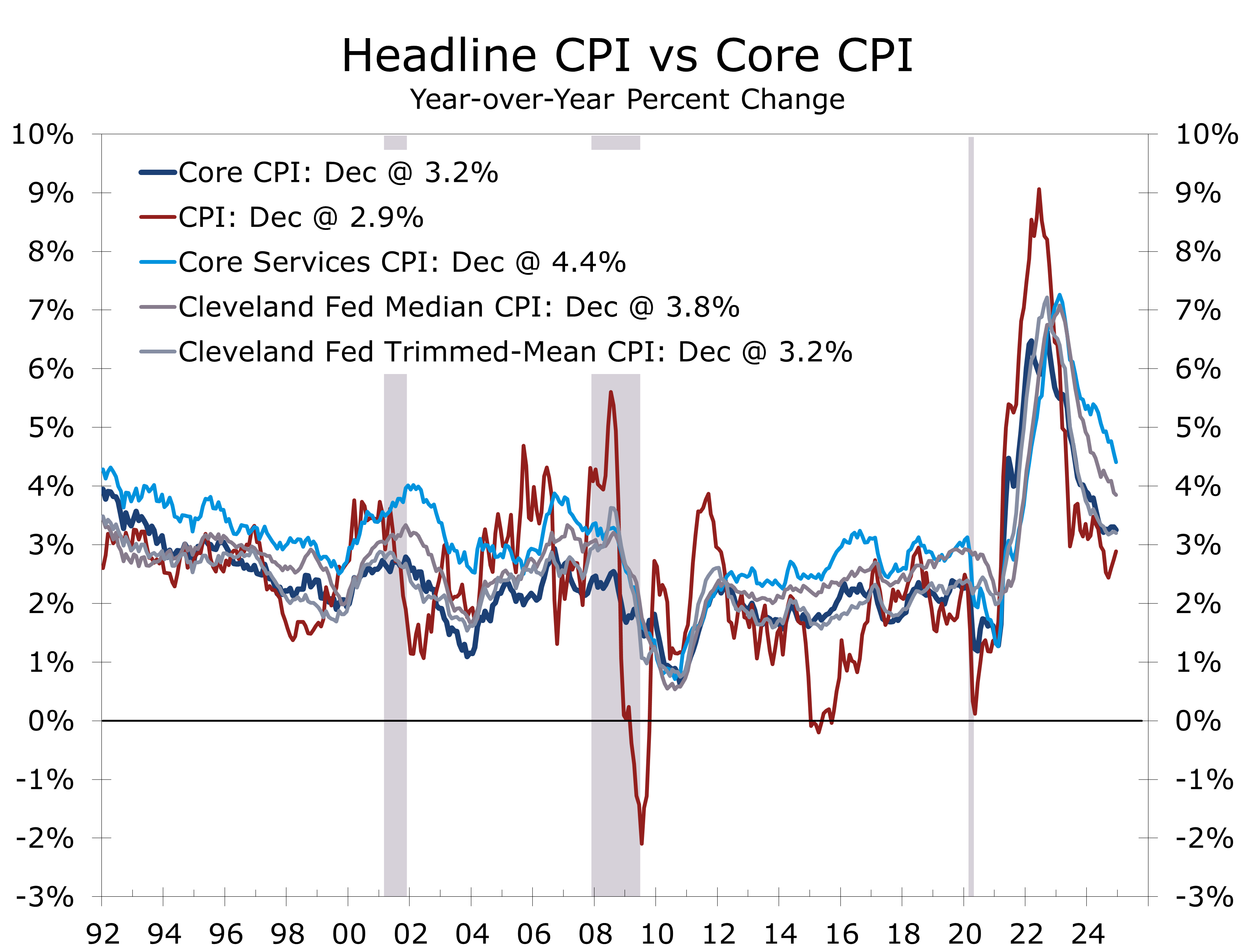

- The core CPI rose 0.2%, with year-over-year core inflation easing to 3.24%.

- Year-over-year headline CPI fell to 2.9%, its lowest since March 2021, while core CPI rose 3.2%.

- Rent and owners’ equivalent rent rose 0.3%, remaining the main contributors to core inflation.

- Core goods prices edged 0.1% higher but declined 0.5% over the past year.

- New (+0.5%) and used vehicle prices (+1.2%) increased, reflecting replacement demand from recent hurricanes.

- Motor vehicle insurance rebounded 0.4% after slowing the prior two month and remains up 11.3% year-over-year.

- Despite the market’s positive reaction, the inflation report met rather than exceeded expectations. Inflation continues to pressure middle- and lower-income households, with persistent price increases in food, energy, rents, used cars, and motor vehicle insurance.

Financial markets breathed a sigh of relief as the December Consumer Price Index (CPI) report came in largely in line with expectations. The headline index rose 0.4%, driven by rebounds in gasoline and food prices, while the core index rose 0.2%. This largely anticipated outcome initially sparked a rally in stock prices and a partial unwinding of the recent surge in bond yields. The reaction looks a bit overdone, but the markets have had a rough few weeks and have traded poorly on both good and bad news and were primed for a relief rally.

It is important to note that the December inflation data were not necessarily better than expected; they simply weren’t as bad as many feared. The headline number rose from 2.7% year-to-year to 2.9%, while the core CPI remained stubbornly elevated at 3.2%. The path to the Fed’s 2% target is not any shorter, reinforcing the Fed’s recently adopted more cautious stance.

Top of Form

December’s CPI was not better than expected, it simply was not worse than the markets feared.

The underlying data presented a mixed picture. Energy prices rose 2.6%, driven by a 4.4% surge in gasoline prices. Gasoline prices typically decline in December. This year’s smaller-than-usual drop, however, led to a large seasonally adjusted increase. In contrast, the rise in food costs was more straightforward, with both grocery store and restaurant prices increasing by 0.3%.

The continued strength in core inflation remains a significant concern, with shelter costs—particularly rent and owners’ equivalent rent—persisting as key drivers, albeit at a slightly slower pace. The persistent pressure on housing costs stems from factors such as limited for-sale housing turnover, robust apartment demand, and a higher-than-normal rate of lease renewals. Although asking rents have softened due to a wave of apartment completions, renewal lease rates continue to rise by 3.5% to 4%.

Rent and owners’ equivalent rent remain problematic, despite a wave of new apartments.

Outside of housing, core CPI showed more stability. Core goods prices edged up 0.1% in December but are down 0.5% year-over-year, primarily due to declines in used (-3.3%) and new (-0.4%) vehicle prices. However, both categories saw increases in December, rising 1.2% and 0.5%, respectively, likely driven by replacement demand after the Southeast’s devastating hurricanes. Replacement demand is also expected to rise in the aftermath of the Los Angeles wildfires.

The Los Angeles wildfires may have broader inflationary effects. Rents in the city’s already tight apartment market are likely to face additional upward pressure, further driving shelter costs. Additionally, insurance costs are expected to remain elevated due to the astounding losses faced by insurers.

The December CPI report highlights the challenges the Federal Reserve faces. While headline inflation has eased, many households, particularly middle- and lower-middle-income families, continue to grapple with inflation fatigue. Grocery prices remain significantly higher than pre-pandemic levels, impacting staples like meat, poultry, dairy, and bakery products. These elevated costs, combined with higher expenses for rent, used cars, and insurance, are straining household finances.

The Fed must navigate this complex environment while acknowledging a softening labor market. Job growth has slowed, with a noticeable shift towards lower-paying roles in healthcare, leisure, and hospitality and local government. This concentrated growth may be masking slower growth in other sectors, making it difficult to assess the true state of the labor market.

The upcoming release of annual revisions to employment data on February 7 will be crucial. If these revisions reveal significantly slower job growth than is currently reported, a March rate cut may be back on the table. Conversely, stronger-than-expected job growth would allow the Fed to proceed more cautiously with rate cuts.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 15, 2025

Mark Vitner, Chief Economist

(704) 458-4000