While Structural Forces Boost Growth, Cyclical Weakness Is Helping Curb Underlying Inflation

-

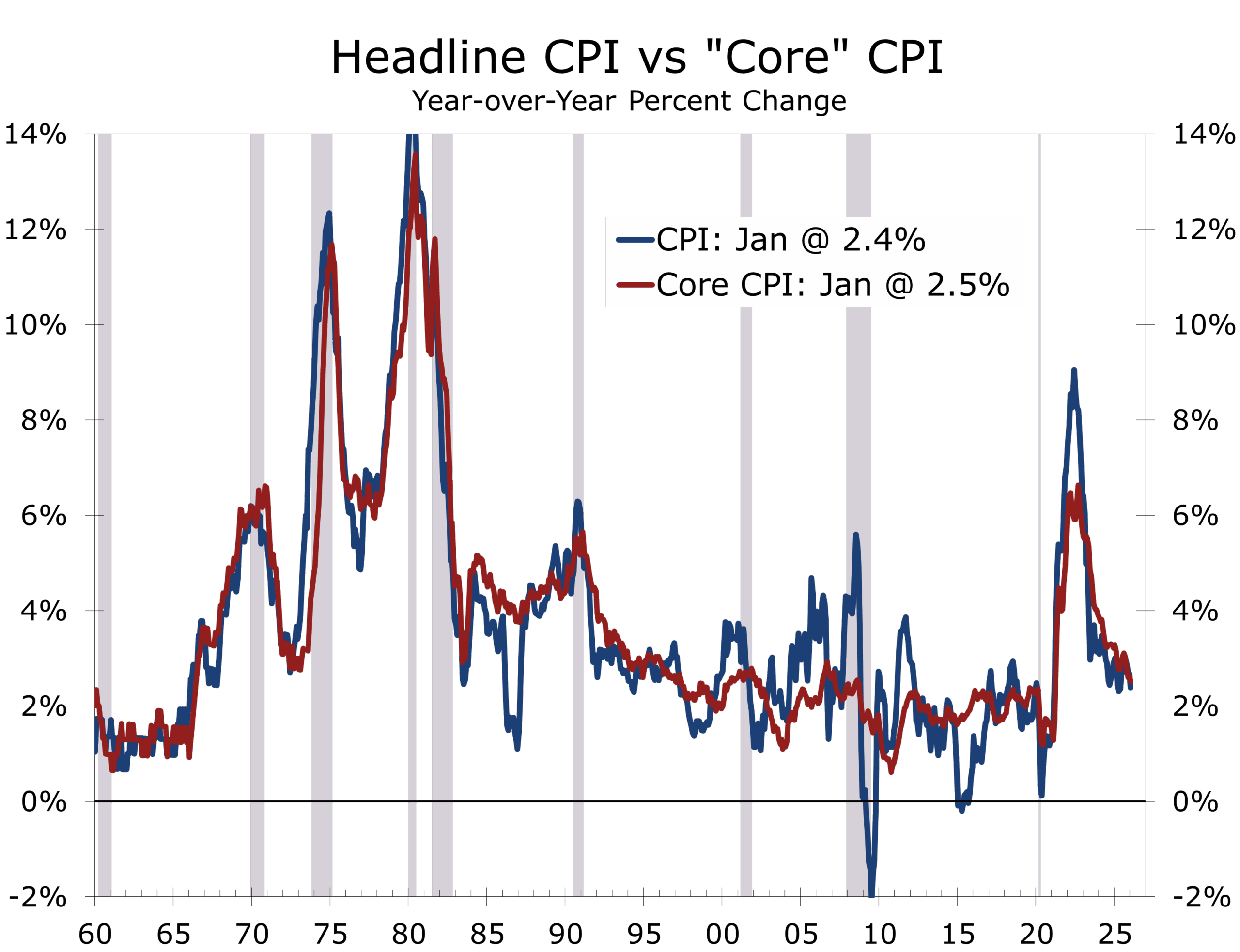

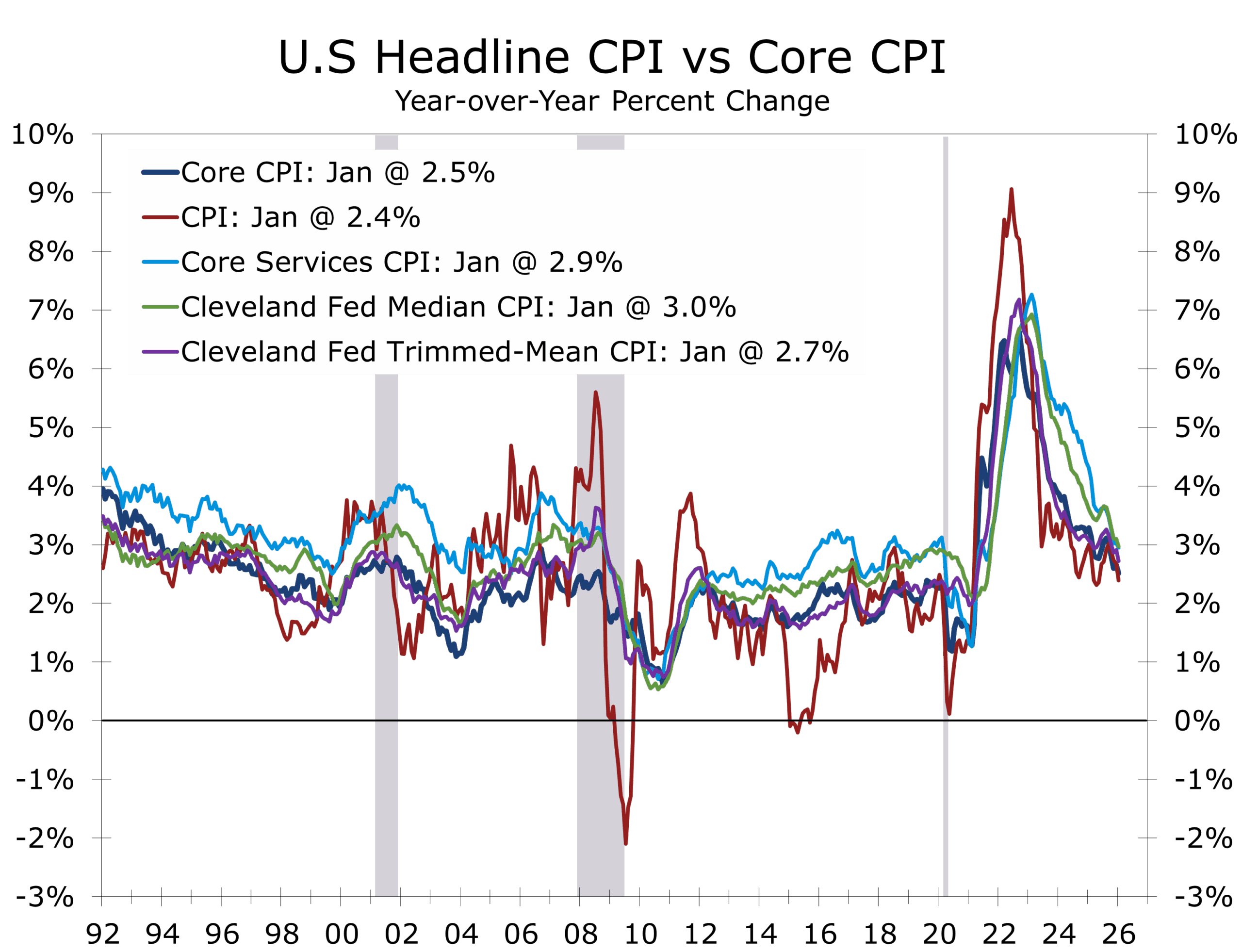

- Headline CPI rose 0.2% in January, slowing the year-over-year rate to 2.4%, the lowest since early 2021.

- Core CPI increased 0.3%, leaving core inflation at 2.5% y/y.

- Energy prices fell 1.5%, with gasoline down 3.2%, suppressing headline inflation.

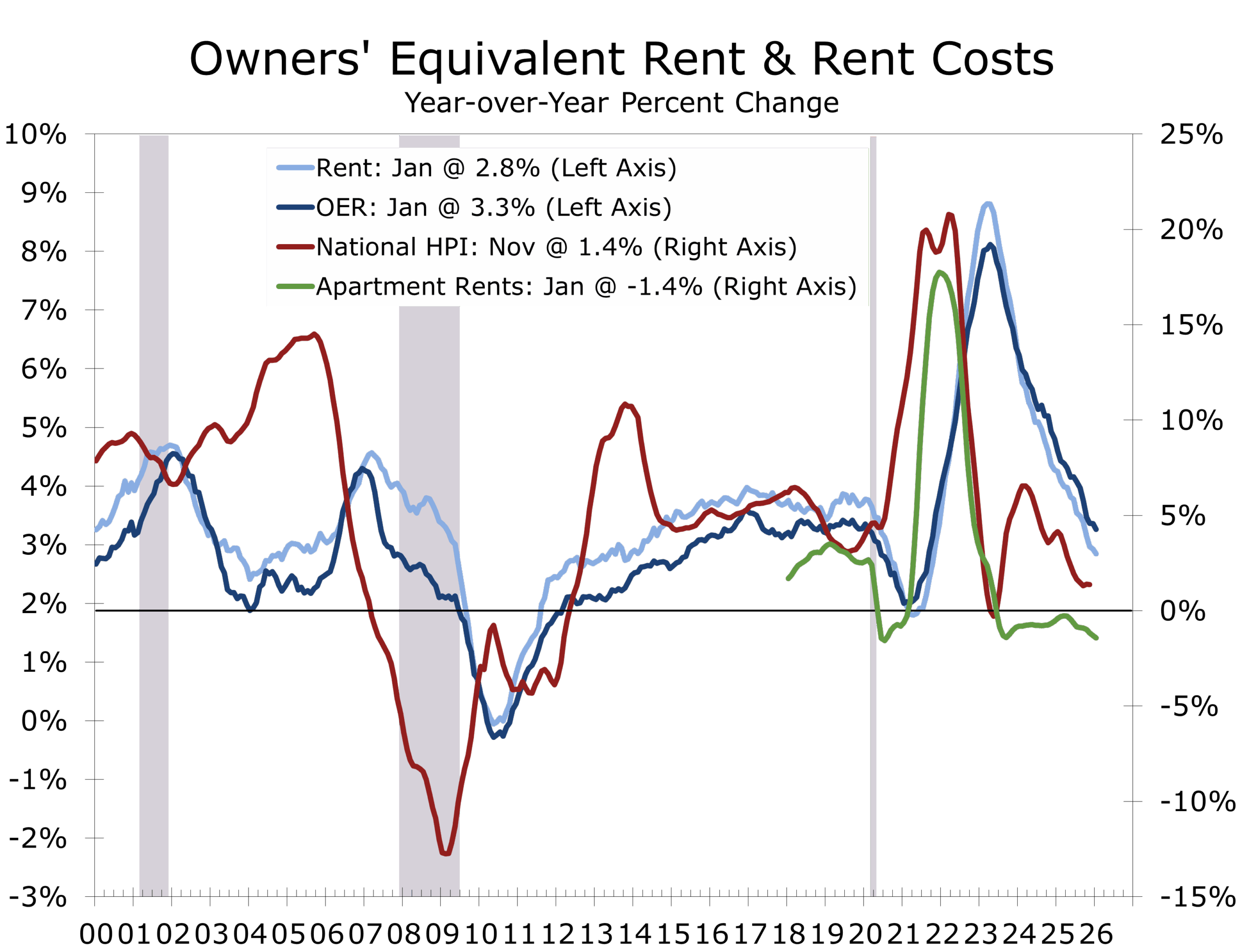

- Shelter rose 0.2%, as falling rents and easing home prices continue to restrain housing costs.

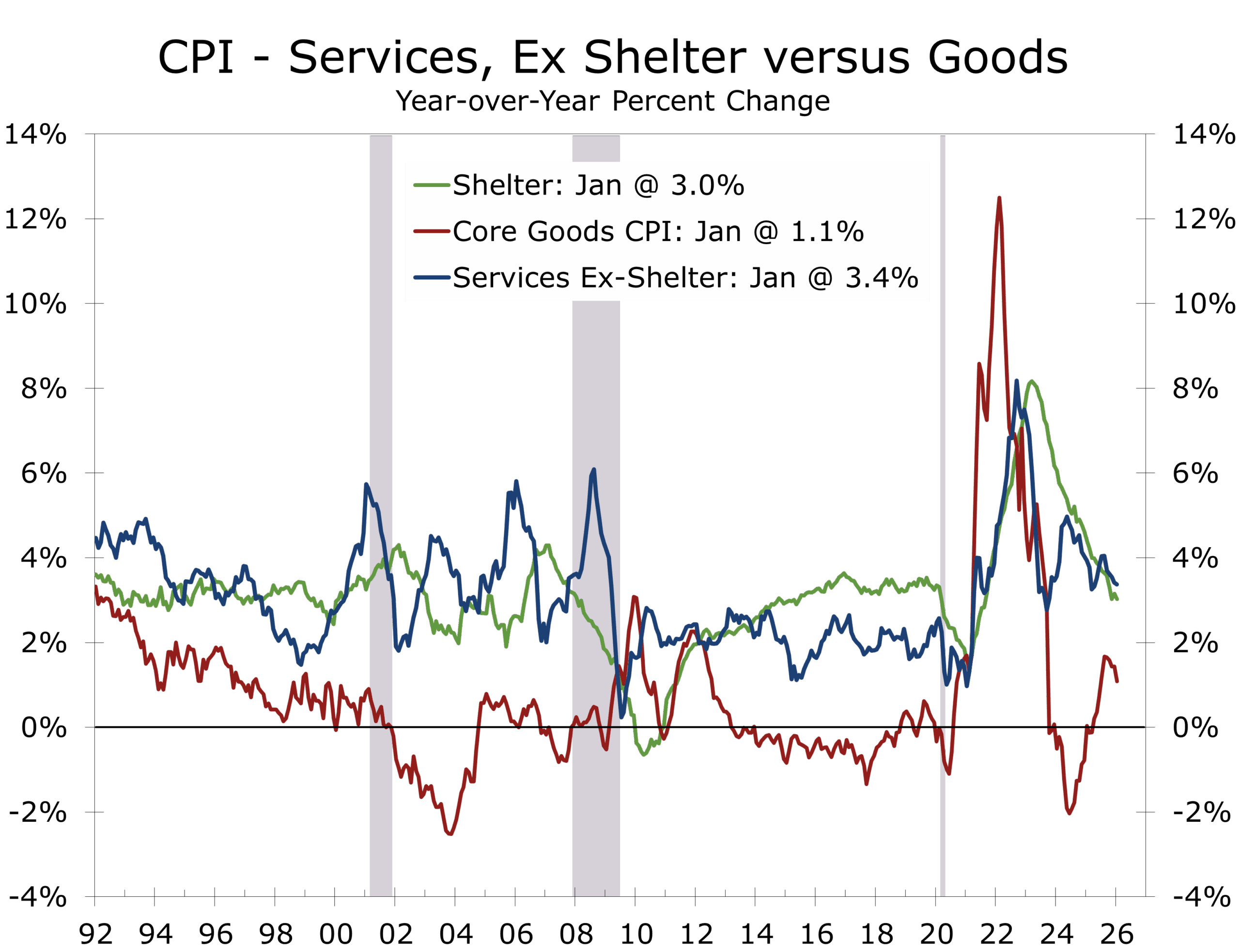

- Core goods inflation remains subdued, reflecting fading tariff pass-through and soft used vehicle prices.

- Services inflation firmed modestly, led by airline fares and medical care.

- Policy signal: Disinflation remains intact, giving the Fed room to cut rates further to support rate-sensitive sectors despite strong headline GDP.

Inflation Continues to Cool — Gradually, Not Dramatically

January’s CPI report confirms that the disinflation process is advancing, though not in a straight line.

Headline inflation eased to 2.4% year over year, down from 2.7% in December. The monthly increase of 0.2% reflects a continued moderation in broad price pressures, even as select service categories posted firm gains.

The story is increasingly one of composition rather than direction. Inflation is no longer broad-based. It is concentrated, uneven, and influenced by a handful of sectors.

Energy is suppressing headline inflation, while the fading impact of tariffs is helping pull the underlying trend lower. Housing costs, once the dominant source of acceleration, are now reinforcing the deceleration.

Inflation is cooling, both on an overall and core basis— and its footprint is narrowing.

Headline vs. Core: Energy Provides Visible Relief

Energy prices fell 1.5% in January, led by a 3.2% decline in gasoline. On a 12-month basis, gasoline prices are down 7.5%, pulling the overall energy index slightly negative year over year.

Energy once again acts as a suppressor of headline inflation rather than a driver. Absent a renewed commodity shock, energy’s contribution should remain neutral to mildly disinflationary in coming months.

Meanwhile, core CPI rose 0.3% in January, leaving the annual core rate at 2.5%. While slightly firmer month-to-month, the broader trajectory remains consistent with gradual convergence toward the Fed’s 2% objective.

Core Inflation: Goods Soft, Services Sticky

The composition of core inflation continues to improve.

Used vehicle prices fell 1.8% in January and are now down 2.0% year over year. Household furnishings declined modestly. Core goods inflation stands at just 1.1% year over year — a far cry from the broad-based goods pressures seen in 2022

Tariff-driven goods inflation has largely run its course. Services are the final battleground.

Retailers have largely worked through higher-cost inventory, and tariff-driven price resets have moderated. Supply chains have normalized, and competitive dynamics are reasserting themselves.

Services remain the primary source of pressure. Airline fares jumped 6.5%, while medical care services rose 0.3%. Recreation and personal care also posted firm gains. Part of this reflects continued strong demand for higher-end services and experiences. We see pricing power ebbing here as well, though at a slower pace than in goods.

Inflation is no longer systemic; it is sector specific.

Shelter: Lower Housing Costs Reinforce the Trend

Shelter rose 0.2% in January, with both rent and owners’ equivalent rent increasing modestly. Year-over-year shelter inflation now stands at 3.0%, down sharply from its peak.

This moderation reflects real market dynamics. Multifamily supply remains elevated across much of the country, particularly in the South and Sun Belt. Vacancy rates have increased. Concessions have become widespread. Lease renewals are resetting lower.

Lower rents and softer home prices are reinforcing disinflation into 2026.

At the same time, home price appreciation has slowed materially as mortgage rates stabilized near 6–6.5%. In several markets, prices have flattened or edged lower. That easing in home price momentum is feeding into OER with a lag.

Food Inflation: The Political Economy of Cumulative Prices

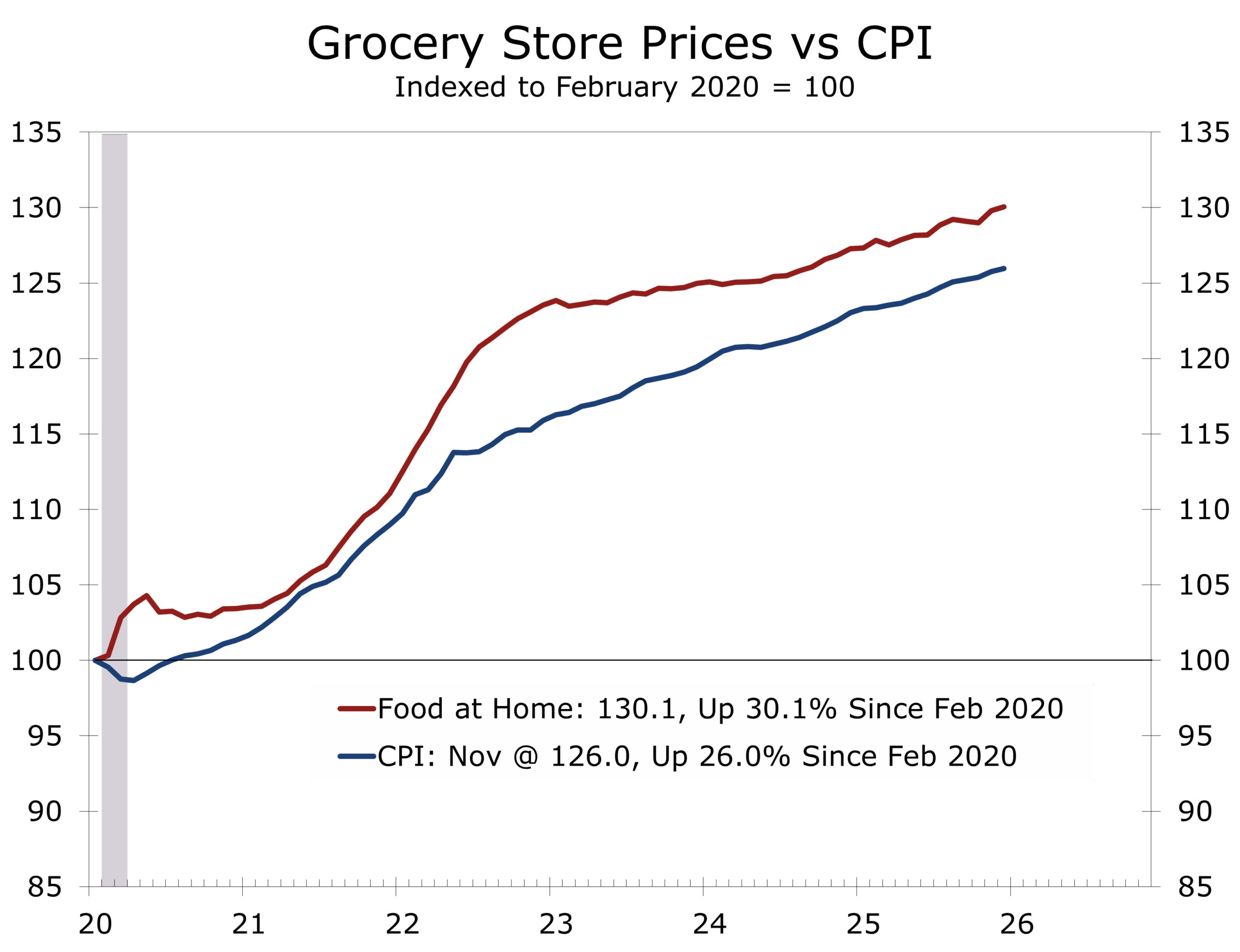

Food prices rose 0.2% in January. On a year-over-year basis, food inflation stands at 2.9%, with food away from home still elevated at 4.0%.

The monthly change, however, understates what consumers feel.

At the grocery store, it is the cumulative price level that matters. Food-at-home prices remain just over 30% higher than they were on the eve of the pandemic. Most of that increase occurred during the post-pandemic inflation surge under President Biden, but consumers benchmark against memory, not momentum.

Cumulative grocery inflation, not monthly changes, shapes consumer psychology.

If grocery prices do not moderate further this year, political pressure will intensify — regardless of when the initial increase occurred.

Structural Boom, Cyclical Softness

Real GDP is expected to run strong this year. But the drivers are structural.

The expansion is being powered by:

- AI infrastructure buildout

- Large pharmaceutical investment tied to GLP-1 therapies

- Reshoring of strategic manufacturing

- Revitalization in civilian aerospace

- Defense rearmament

These are capital-intensive, long-duration investment cycles that are ultimately disinflationary.

The cyclical side of the economy tells a different story. Consumer spending on durables remains soft. Housing activity is constrained by affordability. Capital expenditures outside AI, pharma, aerospace, and defense remain cautious.

The weakness in consumer durables and housing is one of the key factors pulling inflation lower. The weakness in cyclical parts of the economy provides the Fed some room to cut interest rates further but not until headline price measures move closer to their long-range target.

Policy Implications: Disinflation Creates Room

With headline inflation at 2.4%, core at 2.5%, shelter easing, and tariff pressures fading, the inflation constraint on monetary policy has eased materially.

Lower inflation is supportive of additional rate cuts, even with strong headline GDP growth. Structural strength does not eliminate cyclical weakness.

Monetary policy operates with a lag. Lower rates would primarily support housing, consumer durables, and cyclically oriented capital investment — the sectors still feeling the effects of earlier restrictive policy.

At this stage, rate cuts are best understood as insurance rather than stimulus. They would move the federal funds rate back toward neutral, or modestly below it.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 13, 2026

Mark Vitner, Chief Economist

(704) 458-4000