Consumer Confidence Rebounds in July

- Consumer Confidence rose 2.5 points in July to 100.3, driven by a slightly more optimistic view on future economic conditions.

- The Present Situation Index declined 1.7 points to 133.6, reflecting less optimism about the current labor market. The expectations index rose 5.4 points to 78.2.

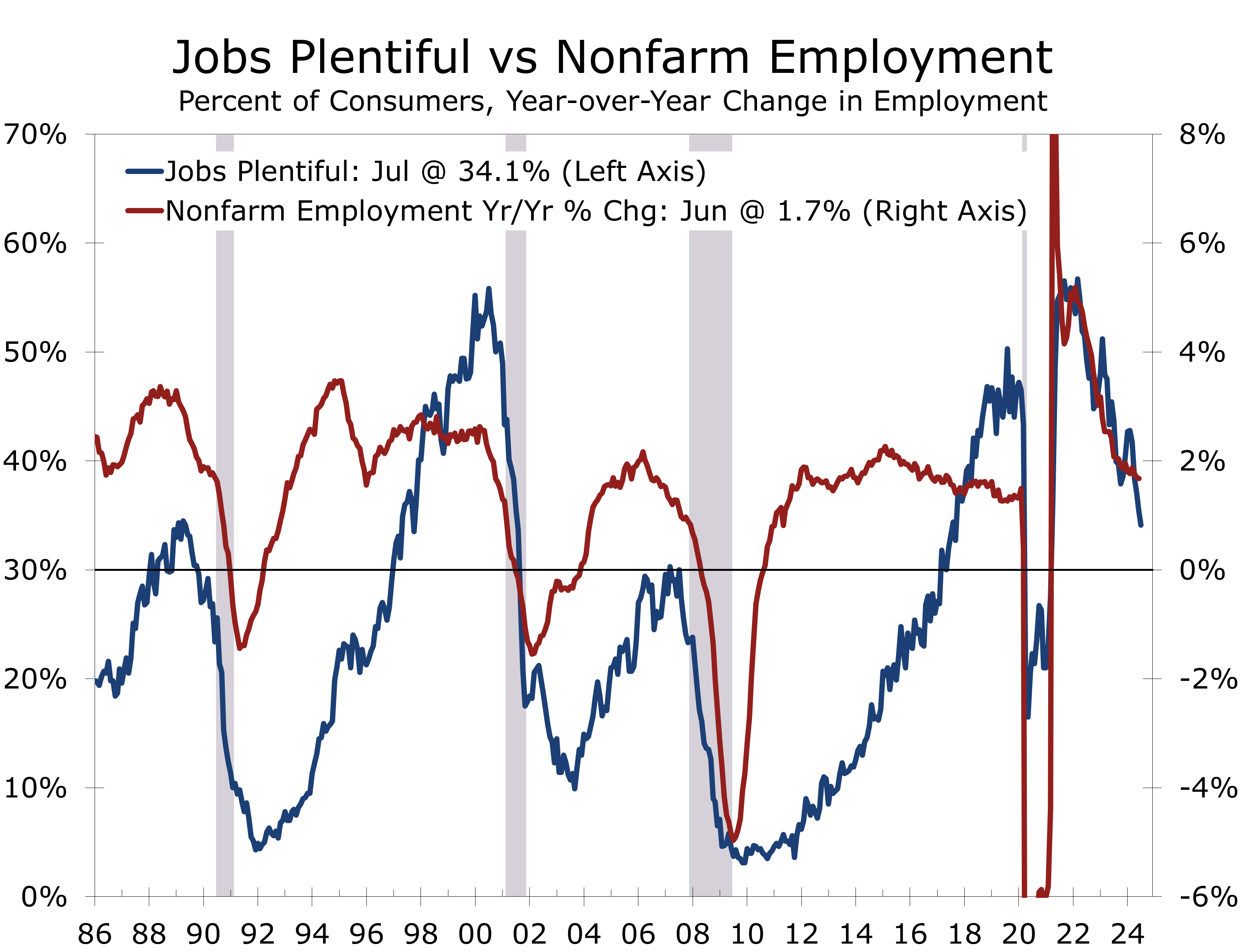

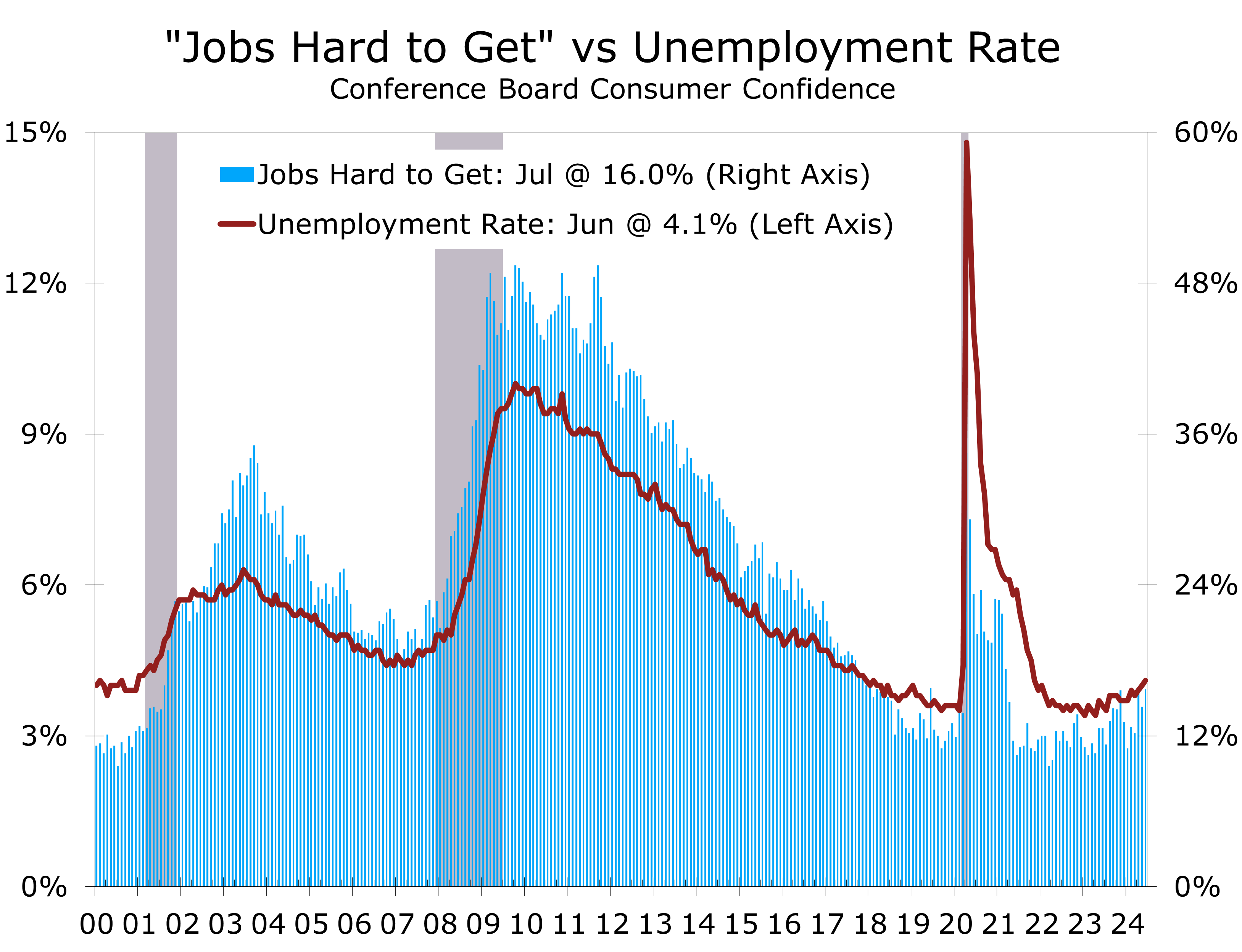

- The labor market indicators in the report offered confirm a cooling job market, fewer consumers see jobs as “plentiful” while more say jobs are “hard to get.”

- Average inflation expectations remained high at 5.4%, as consumers remain frustrated by past increases in food and energy prices.

- Buying plans for homes fell to a 12-year low on a six-month moving average basis.

- The Consumer Confidence report held few surprises. The index has cooled in ways consistent with a soft landing, suggesting job growth will weaken further. Some battle scars from the inflation fight are also evident, with inflation expectations for the next 12 months still well above pre-pandemic levels.

The Conference Board’s Consumer Confidence Index® rose a modest 2.5 points in July, reaching 100.3 (1985=100) from a downwardly revised 97.8 in June. Confidence remains 0.1 point below its reported figure one month ago. The entirety of July’s gain stemmed from consumers’ improved outlook on future economic conditions. Consumers’ assessment of the Present Situation declined by 1.7 points to 133.6 from 135.3, whereas the Expectations Index rose 5.4 points to 78.2 June’s 72.8. Despite this uptick, the expectations index remains below the critical 80 threshold, which often signals an impending recession.

The preliminary results cutoff date was July 22, 2024, occurring one day after President Biden withdrew from the presidential race and nine days following the assassination attempt on former President Trump.

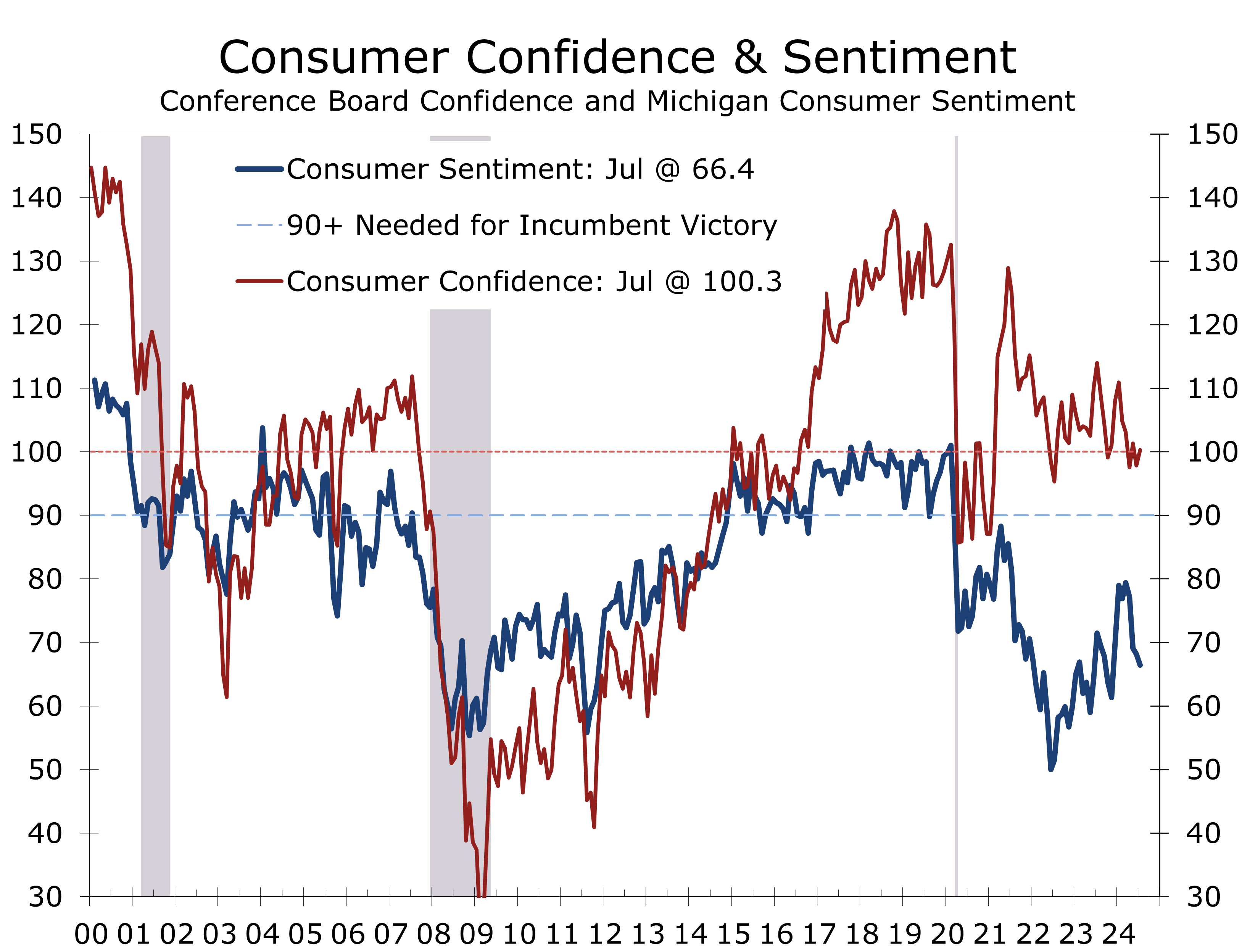

Consumer confidence is hovering near 100, a key level historically necessary for an incumbent party presidential candidate to secure re-election. Moreover, there is a considerable gap between the Conference Board’s Consumer Confidence Index and the University of Michigan’s Consumer Sentiment Index. The Conference Board’s metric places greater emphasis on employment conditions, which remain robust relative to historical norms. The University of Michigan’s survey underscores consumer finances, adversely affected by elevated inflation, particularly for essentials such as food, transportation costs, and housing. The incumbent party has typically lost the White House when Consumer Sentiment is below 90.

The wide gap between consumers’ assessment of current economic conditions and their expectations for conditions six months ahead is narrowing. This narrowing is largely due to a declining share of households who perceive current conditions as favorable. The current conditions index has decreased from a peak of 155.3 in June 2023 to 133.6 currently, marking a 21.7-point drop. This decline reflects the ongoing rebalancing of the labor market, with job openings and hiring slowing, and the unemployment rate rising from 3.5% a year ago to 4.1% in June.

Conversely, the expectations index rose by 5.4 points but remains relatively low at 79.8, which is 9.8 points lower than it was a year ago. An expectations index below 80 typically signals an impending recession. Consistent with this indicator, consumers remain cautious about the economy’s prospects, with 66% expecting a recession in the next 12 months.

An increasing number of consumers feel jobs are less plentiful, indicating job growth is cooling.

The labor market is clearly cooling. The share of consumers who believe jobs are “plentiful” fell by 1.4 points to 34.1% in July, an 8.6-point decline since January. Meanwhile, the percentage who feel jobs are “hard to get” rose by 0.3 points to 16%, a 5-point increase since the start of the year. The labor market differential, the gap between the two, dropped by 1.7 points to 18.1, down 13.6 points since January.

The slight increase in the “jobs hard to get” series aligns with the recent rise in the unemployment rate. Similarly, the decline in the “jobs plentiful” series has preceded the slowdown in nonfarm payroll growth. This ongoing decline supports our below-consensus forecast of 170,000 net new nonfarm payrolls in July. The unemployment rate may inch up to 4.2%.

Inflation expectations have improved this year but remain above their pre-pandemic level.

The Conference Board’s analysis of write in comments indicates that inflation/higher prices, especially for food and groceries, continue to be the primary factors shaping consumers’ economic outlook. These concerns are followed by the US political situation and labor market conditions. Notably, average 12-month inflation expectations remained stable at 5.4% in July, compared to a peak of 7.9% reported in 2022.

Consumer anxiety over higher prices underscores the imperative for the Fed to bring inflation back to its 2% target. While we anticipate the Fed signaling readiness to cut rates in September, their stance may remain hawkish. We project four to five quarter-point cuts this cycle, bringing the funds rate to approximately 4.25%.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

July 30, 2024

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000