Confidence Continues to Slide as Job Security Concerns Increase

-

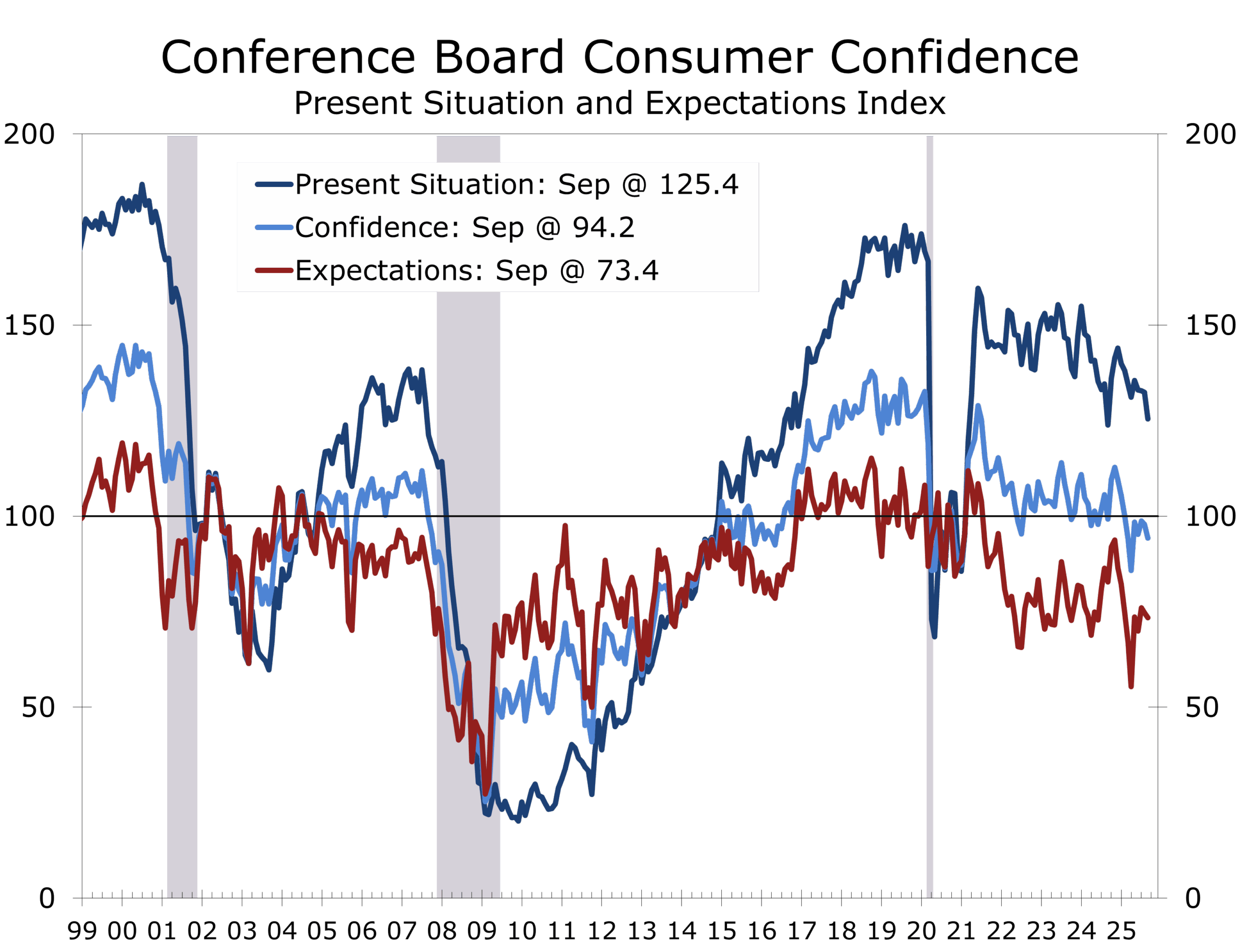

- The Conference Board’s Consumer Confidence Index® slipped 3.6 points in September to 94.2, modestly weaker than expected but still near recent averages.

- The Present Situation Index fell 7.0 points to 125.4, its largest drop in a year, while the Expectations Index eased 1.3 points to 73.4, remaining well below the recession-warning threshold of 80 for an eighth straight month.

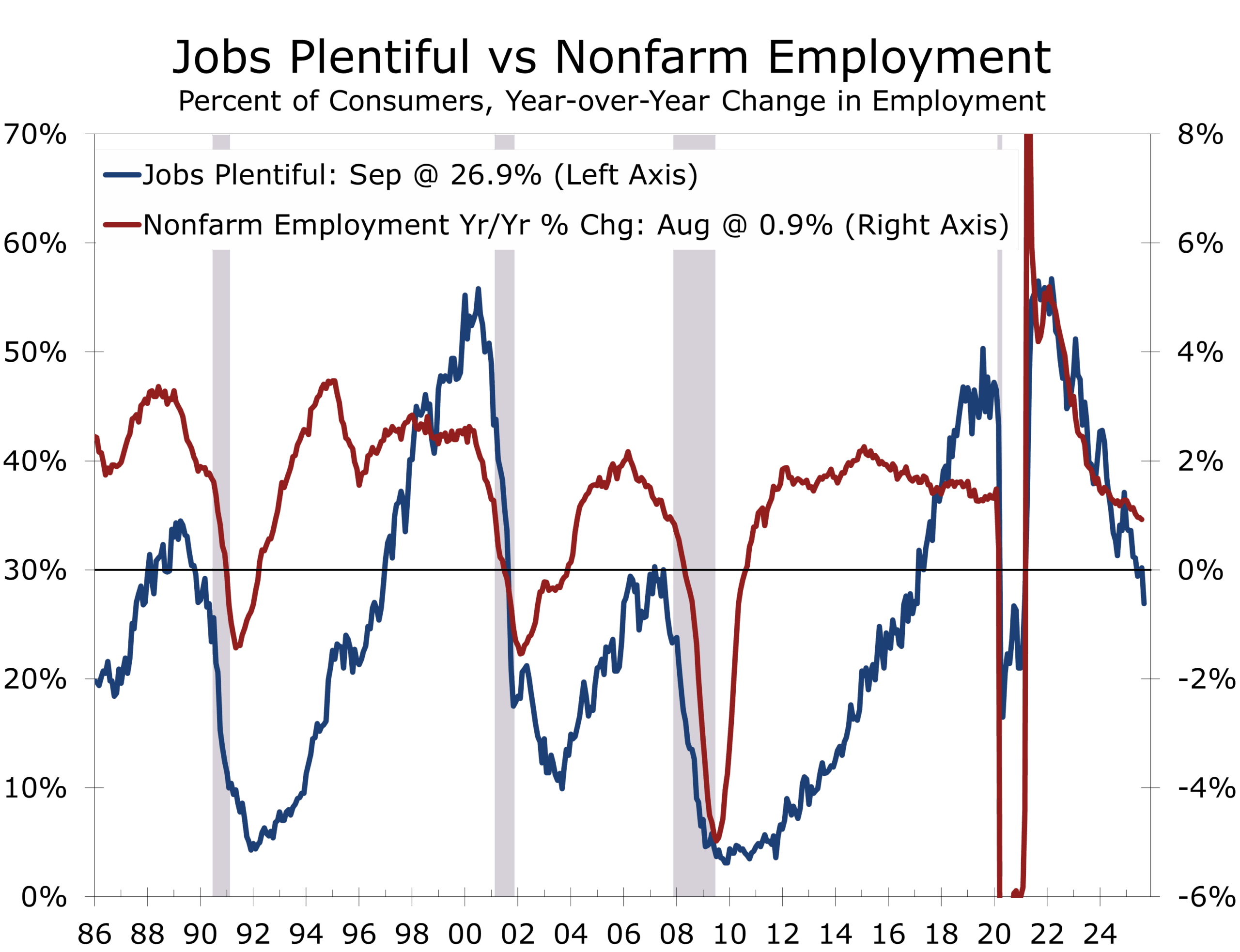

- The labor differential narrowed to 7.8—its lowest level since February 2021—signaling weaker job availability.

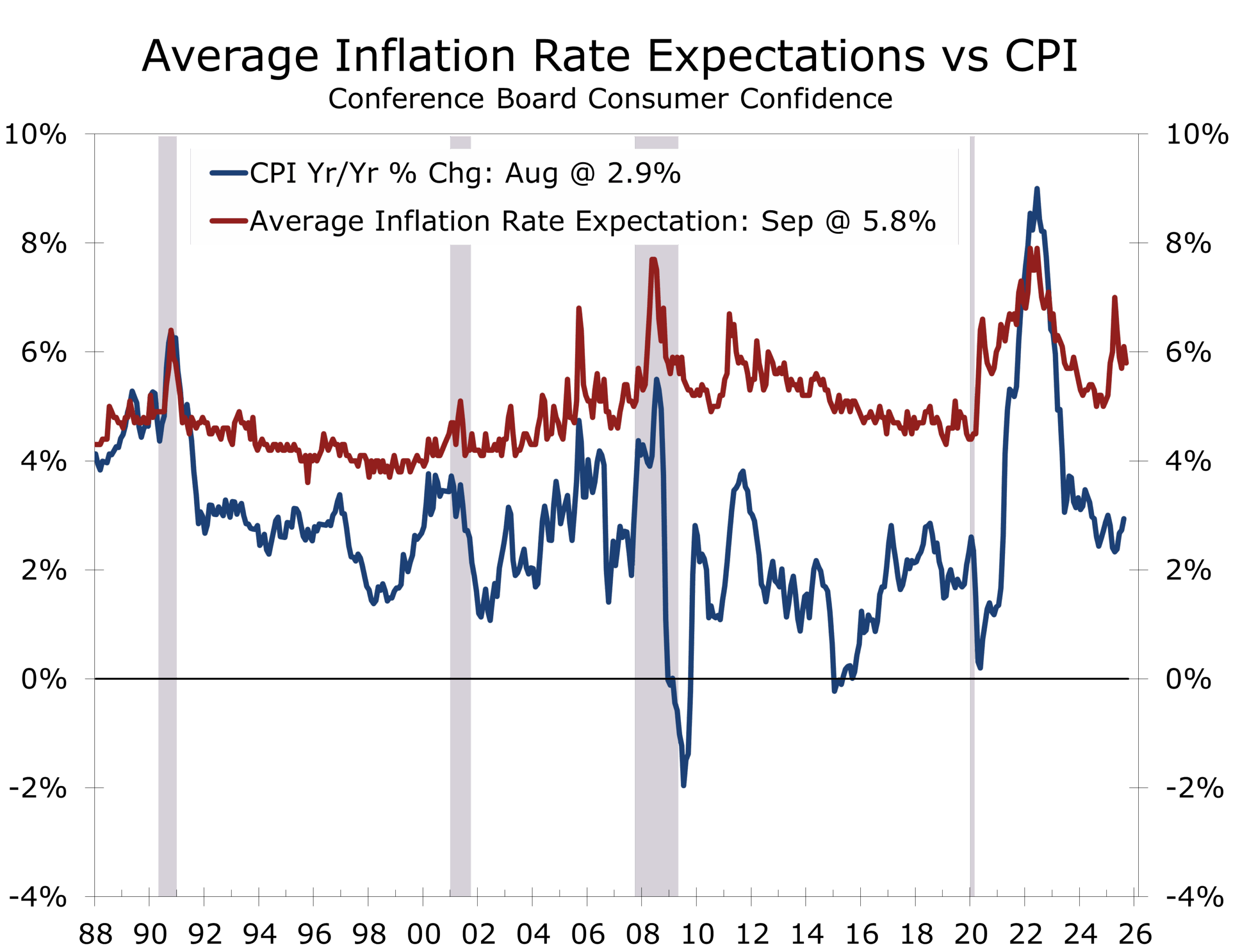

- Inflation expectations edged down to 5.8%, but consumer write-ins showed renewed concern about prices. Mentions of tariffs declined, though they remain associated with price pressures.

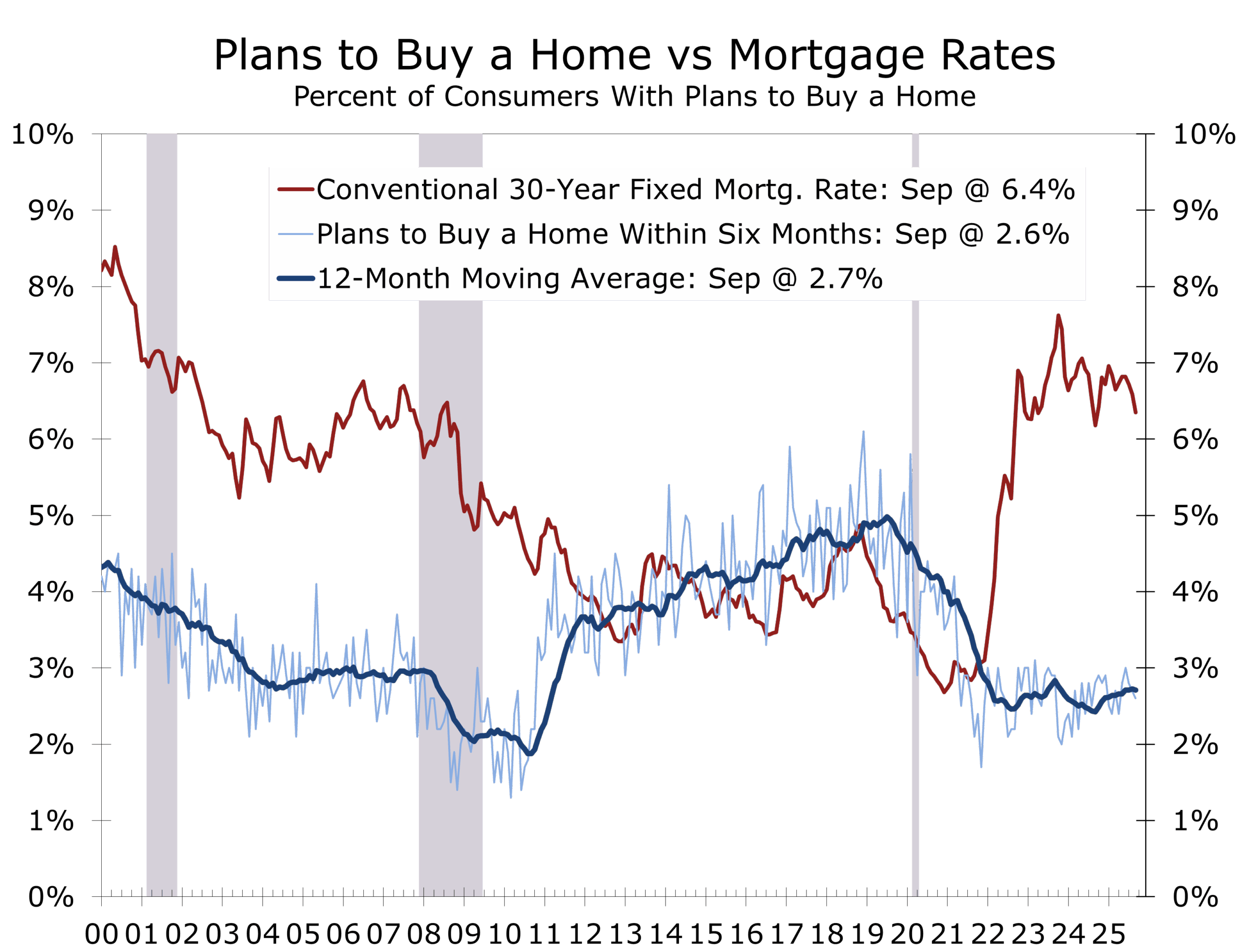

- Spending intentions were mixed: home buying plans hit a four-month high, but car buying and travel-intentions weakened.

Upper-Income Resilience vs Middle-Income Angst

Consumer confidence fell slightly more than expected and the underlying details suggest the expansion remains more fragile than recently upgraded GDP forecasts suggest. The steep decline in the Present Situation Index reflected growing unease about business conditions and job availability. The share of consumers saying jobs are “plentiful” fell to 26.9%, down from 30.2% in August, while 19.1% said jobs are “hard to get.” This pushed the labor market differential down to 7.8, its lowest reading since February 2021.

Traditionally, the labor differential leads the unemployment rate, which has been rising as the differential has fallen. The relationship between the two, however, may be shifting. With fewer foreign workers entering the workforce, slower labor force

two, however, may be shifting. With fewer foreign workers entering the workforce, slower labor force growth could temper the rise in unemployment even as consumers report weaker job availability. The deterioration in the differential still stands as a clear warning that labor market conditions are weaker than the headline employment numbers suggest. The latest JOLTS report reinforced this picture of a “low hiring, low firing” economy—job openings remain plentiful relative to history, but hiring rates have slipped, making it harder for job seekers to gain traction.

Upper-income spending holds on asset gains, while middle-income caution grows.

Consumer spending stayed resilient this summer, with stronger July and August retail sales lifting Q3 GDP forecasts. But the gains were driven mainly by upper-income households benefiting from rising equity and housing wealth.

Middle-income households, by contrast, are showing greater caution. Job security appears to be waning, and more job seekers are finding it harder to land positions in a softer hiring environment. These households also remain more sensitive to inflation, which explains why inflation references reemerged as the top consumer concern in September’s survey.

Middle-income households pull back as job security wanes and inflation fears linger.

Meanwhile, middle-income households in the region’s manufacturing and logistics sectors are retrenching, constrained by weaker hiring pipelines and persistent price pressures on essentials. This divergence echoes national trends but is magnified in regions like the South, where growth has long depended on the persistent in-migration of job seekers. The risk is that confidence erosion at the middle-income level could begin to sap the broader consumer base that has historically underpinned growth across the Southeast.

Inflation expectations provided a small offset, easing to 5.8% from 6.1% in August. Even so, consumers’ write-in comments suggest they are not convinced inflation pressures are truly receding. Tariff mentions declined but remain elevated, a reminder that trade policies continue to shape consumer psychology even as pass-through effects have been surprisingly modest.

Spending intentions remain uneven. Home buying plans climbed to a four-month high as lower mortgage rates lured some buyers back, but auto purchases slipped under the weight of high financing costs. Travel plans weakened further, with international trips leading the decline. The link between sentiment and spending has loosened. Spending is outperforming income growth, however, indicating that wealth is helping sustain spending as job growth slows and worries about employment security increase.

Spending outpaces income growth, sustained by wealth effects as job worries mount.

The September Consumer Confidence report captures a consumer mood that has softened at the margin but is still far from collapsing. Confidence declined slightly more than expected, but the sharper deterioration in the present situation underscores risks around jobs and spending intentions. Inflation anxieties remain sticky, and middle-income households appear more cautious even as upper-income spending supports headline growth. For the Fed, this mix—sliding confidence, a weakening labor backdrop, and persistent price concerns—supports a cautious, gradual approach to rate cuts.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 30, 2025

Mark Vitner, Chief Economist

(704) 458-4000