Confidence Holds Its Ground as Middle East War Pressures Prices and Rebound in Equities Cushions Sentiment

Mark P. Vitner, Chief Economist | mark.vitner@piedmontcrescentcapital.com · April 28, 2026

| Indicator | April 2026 | March 2026 | Change |

|---|---|---|---|

| Consumer Confidence Index | 92.8 | 92.2 | +0.6 |

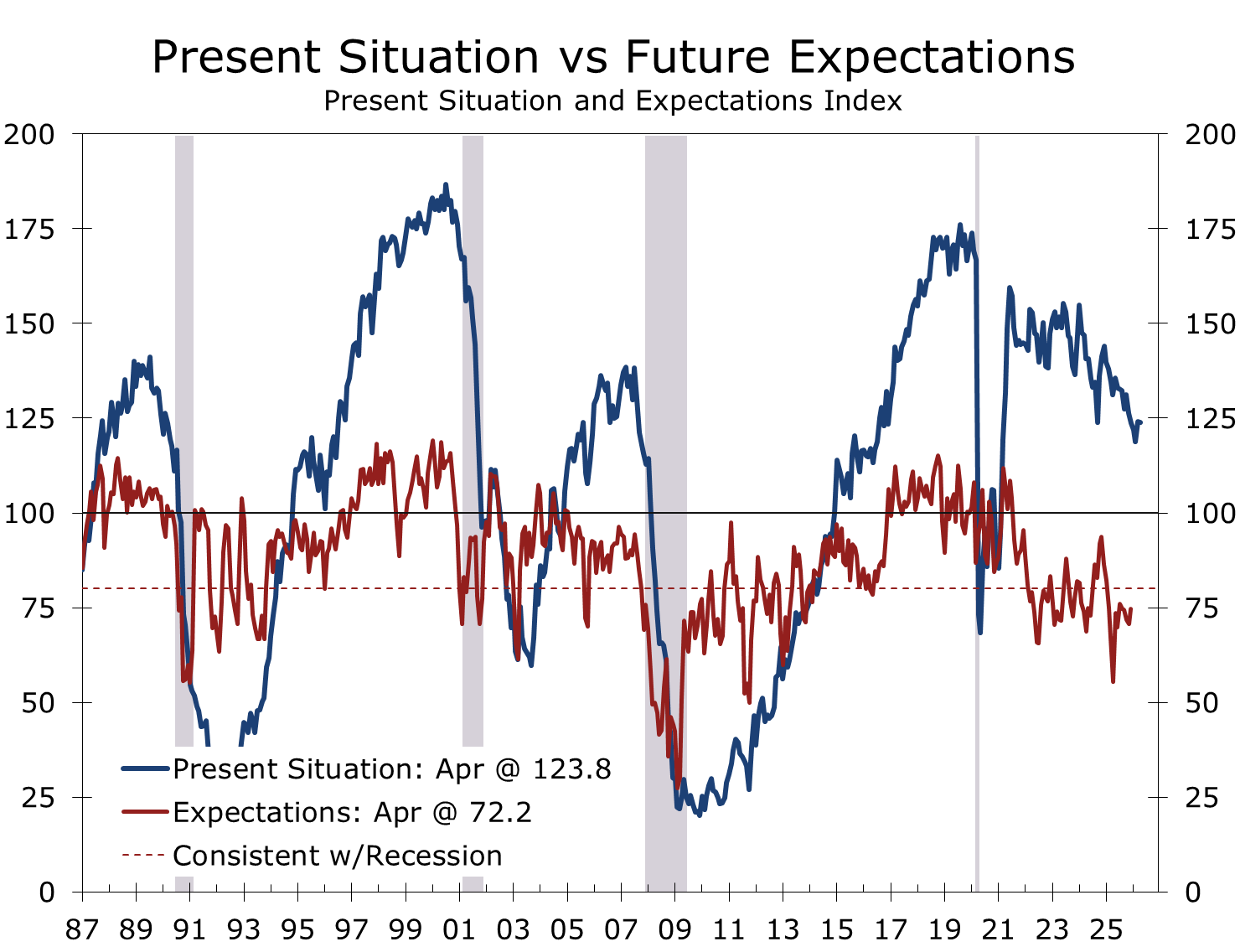

| Present Situation | 123.8 | 124.1 | −0.3 |

| Expectations | 72.2 | 71.0 | +1.2 |

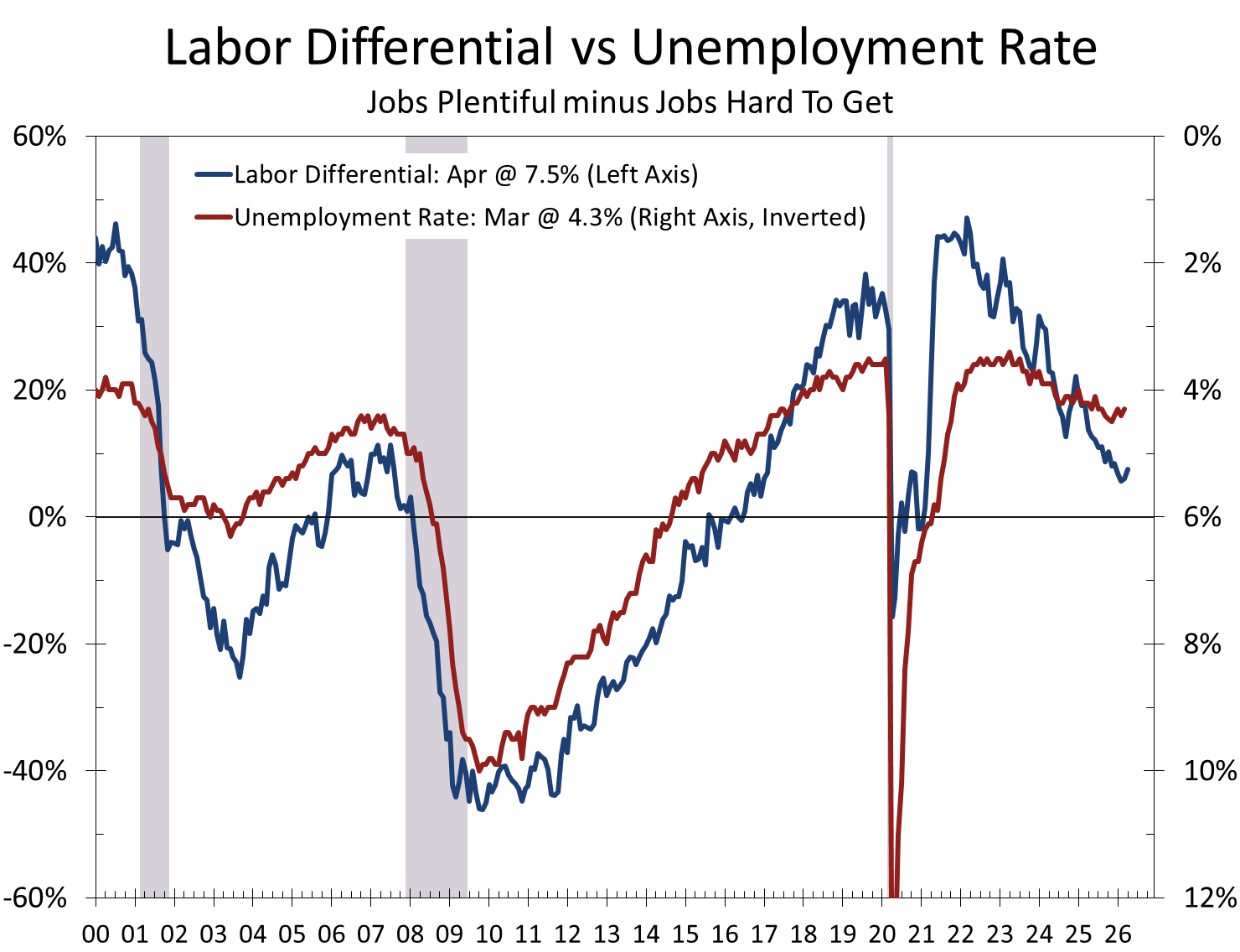

| Labor Market Differential | +7.5% | +6.1% | +1.4 ppt |

| Jobs “Plentiful” | 27.3% | 27.4% | −0.1 ppt |

| Jobs “Hard to Get” | 19.8% | 21.3% | −1.5 ppt |

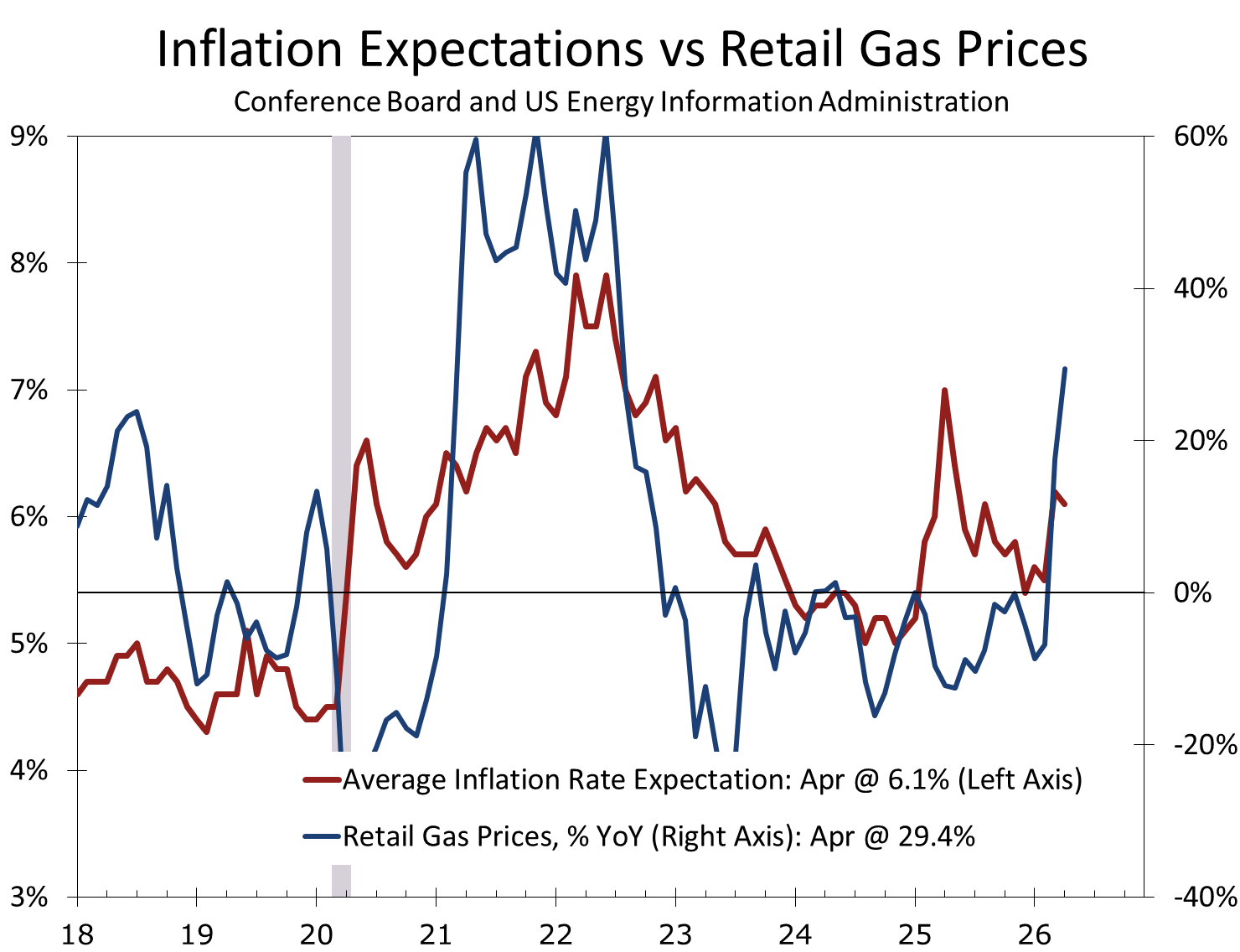

| 12-Mo. Inflation Expectations | 6.1% | 6.2% | −0.1 ppt |

Headline Print

The Conference Board Consumer Confidence Index® rose 0.6 points to 92.8 in April, with March revised up to 92.2 from 91.8 originally reported. The result topped the Bloomberg consensus of 89.0 and represented the third straight monthly gain following the early-2026 trough. The improvement was driven by the forward-looking Expectations Index, which climbed 1.2 points to 72.2, while the Present Situation Index slipped 0.3 points to 123.8 on softer assessments of current business conditions.

Expectations remain below the 80-point recession threshold for the fifteenth consecutive month, but the trajectory has clearly shifted. After bottoming earlier this year amid heightened geopolitical uncertainty, the index has now retraced a meaningful share of its decline. The survey window (April 1–22) captured both the two-week ceasefire that began on April 8 and the equity rebound that followed, and consumers responded in kind. The ceasefire has done more for hope than for hard data, and consumers appear to be reading the situation accurately—willing to mark up forward-looking expectations while keeping their assessment of present conditions anchored.

Confidence has now risen for three straight months, with the labor differential climbing to its highest level since December.

Two Surveys, Two Stories

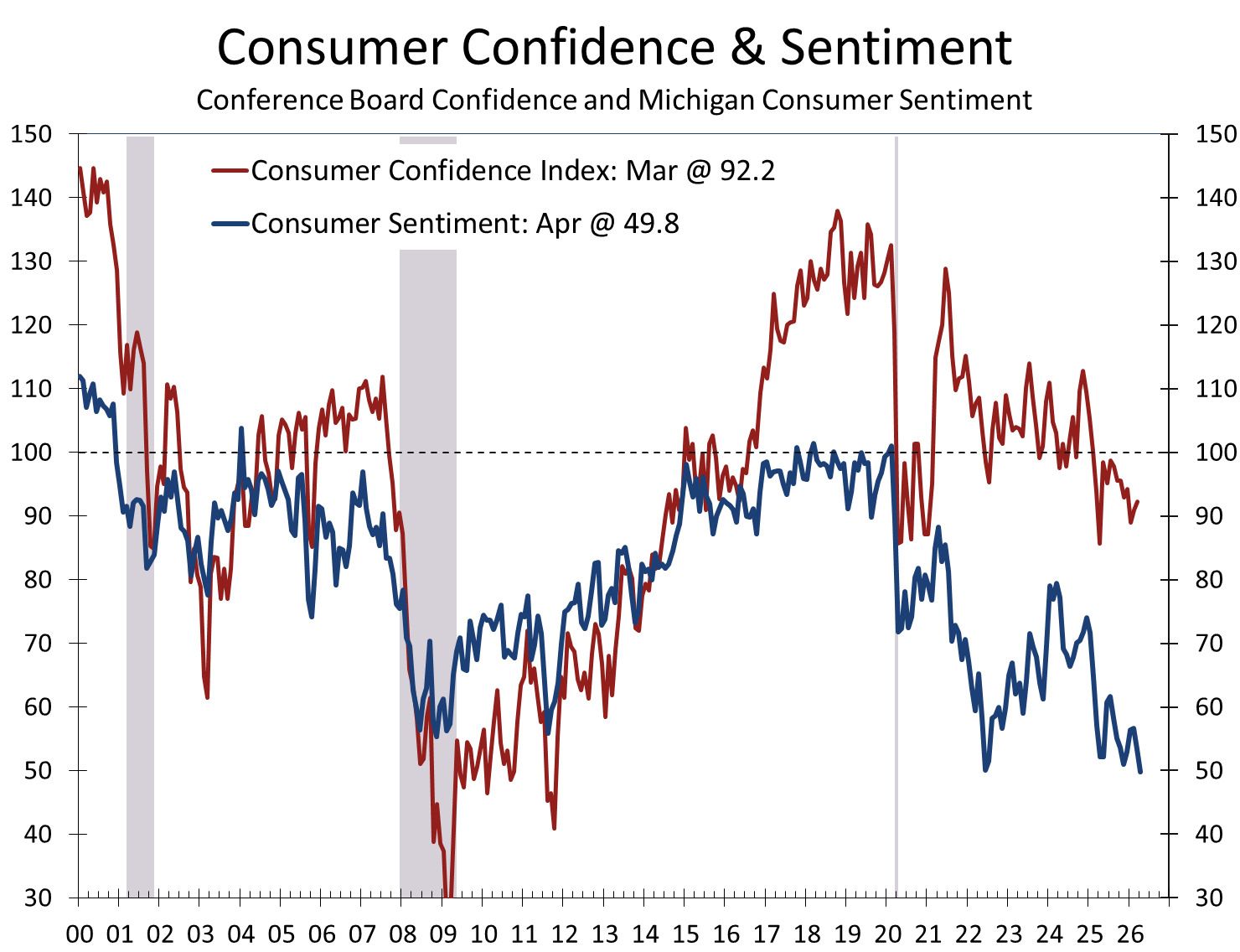

April's Conference Board print stands in stark contrast to the University of Michigan's Survey of Consumers, which fell to 49.8—the lowest reading on record in data going back to 1952, and below the prior 50.0 trough set in June 2022. The divergence is mostly methodological. Michigan leans heavily on inflation expectations and personal finances—both rattled by the surge in gasoline prices, with Michigan's year-ahead inflation expectation jumping from 3.8% to 4.7% in April. The Conference Board weights labor-market conditions more heavily, and labor has been firming. Survey timing played a smaller supporting role: Michigan's preliminary reading of 47.6 was largely completed before the April 7 ceasefire announcement (Hsu noted 98% of those interviews predated it), and although the final reading's interview window extended through April 20 and incorporated a modest post-ceasefire bounce, sentiment still hit a record low. We continue to weight the Conference Board index more heavily for forecasting consumer spending; its labor-market sensitivity has historically tracked actual outlays more reliably than Michigan's inflation-driven swings. The honest read is that consumers are simultaneously alarmed about the price level and reassured by the job market. Both can be true. The spending data will adjudicate.

Labor Market: A Quiet Strengthening

The labor market differential—the share of consumers saying jobs are plentiful minus those saying jobs are hard to get—rose 1.4 points to +7.5%, its highest reading since December 2025. The improvement was driven almost entirely by the “hard to get” share, which fell to 19.8% from 21.3%. The “plentiful” share was essentially flat at 27.3%. With voluntary quits still running below pre-pandemic norms, our read is that workers see fewer attractive outside options—a labor market that is firm at the surface but with diminishing churn underneath.

This is a constructive signal. The labor differential typically moves in step with the unemployment rate, and a rebound here is consistent with a stabilization rather than further deterioration in hiring conditions. Forward-looking labor market views also improved, with 16.1% of consumers expecting more jobs available six months from now (up from 15.4%) and the share expecting fewer jobs falling to 26.9%. Net income expectations turned slightly more positive as well, with the “declining income” cohort dropping to 12.3%.

We continue to expect the unemployment rate to drift modestly higher into mid-year as labor demand softens, but the pace of any rise should be cushioned by slower labor-force growth. Today's report supports that view.

Inflation Expectations: Still Elevated, But Stable

Twelve-month inflation expectations ticked down to 6.1% from 6.2% in March, which had been the highest reading since May 2025. The recent run-up reflects the surge in Brent crude prices that followed the escalation of Middle East hostilities, which has lifted retail gasoline prices to roughly 30% above year-ago levels. Stabilization in pump prices during the April survey window appears to have arrested the upward drift in expectations, though the level remains well above the pre-conflict baseline near 5.5%.

The composition of consumer write-in responses tells the same story. References to prices, oil and gasoline, and the Middle East conflict rose in frequency from March. These remain the dominant household concerns, but their salience appears to have plateaued rather than intensified. The share of consumers expecting interest rates to be higher 12 months from now climbed to nearly 50%, a reflection of the lingering inflation overhang.

Buying Intentions: Selective, Not Defensive

Plans to purchase big-ticket items softened on a month-over-month basis in April, with the share of consumers saying “no” rising relative to “yes” and “maybe” responses. However, the proportion answering “yes” remains comfortably above the other categories, and the more reliable six-month moving averages tell a different story. On that basis, auto-buying plans continued to rise, homebuying intentions for both new and existing units staged a mild recovery, and plans for furniture, appliances, and electronics improved further. Used cars remain the clear preference over new in the auto category, and existing homes—a far larger market—continue to lead new construction.

Services spending plans painted a more cautious picture. Anticipated outlays fell across nearly every category in April, with pet care the lone exception. Restaurants, beauty and personal care, and streaming retained the top spots, but the displacement of personal travel by utilities and healthcare in the top-five future spending list points to a household that is prioritizing the necessary over the discretionary. Domestic travel intentions have largely tracked sideways through the first four months of the year, while foreign travel partially recovered in April after a Q1 collapse.

The pattern is consistent with what we have called “cheap thrills” spending: consumers continue to participate in the economy, but they are increasingly drawn to lower-cost goods and essential services. Energy price spikes have historically prompted trade-down behavior even within higher-margin discretionary categories—beer, soft drinks, snacks—and that channel bears watching as long as pump prices remain elevated. This is a more measured posture than outright retrenchment, and it explains why goods consumption has held up better than many forecasts anticipated even as services growth moderates.

Demographics & Cross-Currents

On a six-month moving average basis, confidence improved among Millennials and Gen Z while continuing to soften among older cohorts. Respondents under 35 remain the most optimistic and those 55 and over the least—a pattern that has held for several months and is largely a function of what the Conference Board survey measures. The CCI weights labor-market conditions heavily, and younger workers have benefited disproportionately from wage growth concentrated at the bottom and middle of the distribution. Older cohorts, by contrast, are more exposed to the variables the index does not weight as heavily: the cumulative inflation hit to the price level, fixed-income returns that have lagged, and the equity volatility earlier this spring. By income, results were mixed but most groups expressed somewhat less optimism on a trend basis.

Confidence rose modestly among Democrats and held steady among Republicans, while Independents pulled back. The dispersion across political affiliations remains wide, and we continue to view the partisan gap as a noise factor that warrants caution when interpreting month-to-month moves in headline confidence.

Recession Perceptions and the Wealth Effect

The share of consumers describing a US recession over the next 12 months as “very likely” rose again in April, while “somewhat likely” and “not likely” responses fell. The cohort believing the US is already in recession edged higher. These measures are not part of the headline index calculation, but worth watching: they have historically led the headline by several months at cyclical inflection points.

Offsetting that caution, the equity rebound during the survey window appears to have provided a meaningful lift to perceived household financial conditions. Expectations for higher stock prices a year from now ticked up. The S&P 500 has recovered fully from its roughly 9% drawdown earlier this spring and pushed to new all-time highs in April, neutralizing the negative wealth effect that had been weighing on high-income household sentiment in the first quarter.

Bottom Line

April's report reinforces a constructive read on the consumer. The third straight monthly gain in headline confidence, the firming labor differential, and the stabilization in inflation expectations all point to a household sector that is absorbing the geopolitical and price shocks of recent months without breaking. The contrast with Michigan's record-low sentiment is best understood as a story about survey timing and methodology, not as evidence the consumer is on the brink.

Risks remain—expectations are still below 80, recession concerns are drifting higher, and energy prices will hinge on developments in the Middle East. But the data in hand suggest a consumer that is cautious rather than capitulating, and an expansion with more durability than the headlines often imply. We continue to expect real consumer spending to slow in 2026 from last year's pace, but to remain solidly in positive territory.