A Bold Start to the Easing Cycle

- The Federal Reserve’s decision to kick off its easing cycle with a larger-than-expected 50bp cut dominated this past week’s economic news.

- Stock prices rallied after processing the Fed’s move, while the yield curve steepened toward a more normal shape.

- This past week’s economic news mostly came in stronger than expected. Retail sales edged 0.1% higher, with the key control group category rising 0.3%.

- Industrial production rebounded 0.9%, reflecting a bounce back in light vehicle assemblies. Housing starts also rebounded, while weekly first-time unemployment claims fell to new lows.

- The Fed’s more aggressive start to the easing cycle likely reflects more concern about slowing job growth rather than confidence inflation has been vanquished. The size of the next move will depend upon the data released between now and the November 7-8 FOMC meeting.

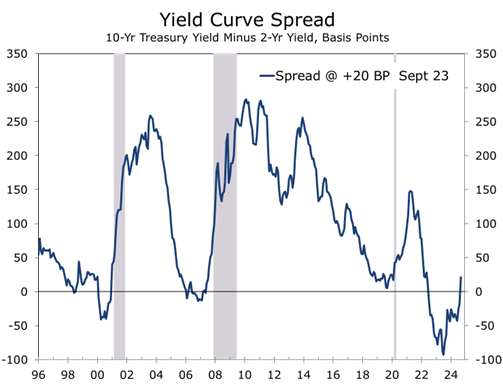

The Federal Reserve surprised the financial markets this week by kicking off its easing cycle with a larger-than-expected 50-basis-point rate cut, dominating the economic headlines. Stock prices rallied in response to the Fed’s move, while the yield curve steepened, beginning its trek toward a more normal slope.

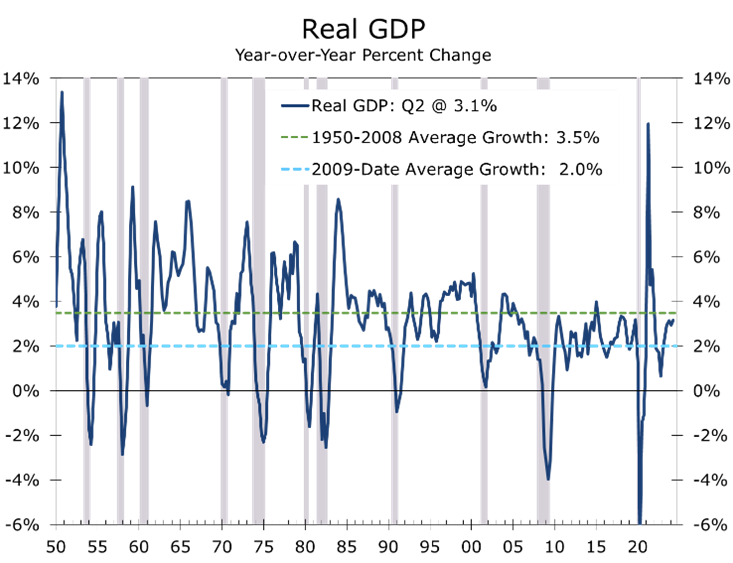

Recent economic data have also exceeded expectations. Retail sales rose 0.1%, while ‘control group’ sales, a key indicator of goods purchases in quarterly GDP, increased 0.3%, signaling strong Q3 consumer spending. Industrial production rebounded by 0.9%, driven by a recovery in light vehicle assemblies, and housing starts bounced back after last month’s weather-related dip. Additionally, weekly initial jobless claims hit new lows. The latest Atlanta Fed GDPNow projects real GDP to rise at a 2.9% annual rate during the current quarter.

Despite these positive figures, the Fed’s aggressive action reflects growing concern about the economy, particularly softening job growth, rather than optimism about cooling inflation. At the press conference following the Fed’s move, Chair Powell noted that if July’s weaker employment data had been available earlier, the Fed might have acted sooner. Currently, wage growth is easing, and inflation is gradually approaching the Fed’s 2% target.

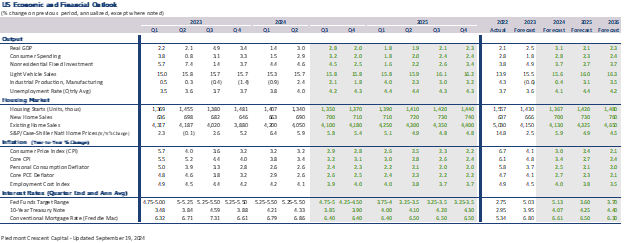

We had anticipated a quarter-point cut in September, as we expect the economy to be in a similar position for the next few FOMC meetings. This raises the risk of disappointing financial markets in the near term. We forecast the Fed will cut the funds rate by a quarter point in both November and December, bringing the year-end rate to 4.38%.

We expect the federal funds rate to be around 3.50% a year from now, indicating five or six more quarter-point cuts. This aligns with the latest Summary of Economic Projections, where 12 of the 19 FOMC participants project the rate will be between 3% and 3.50% by next year’s end. Five participants foresee a rate above 3.50%, with one just over 4%, while two expect it to fall below 3%.

A large majority of FOMC participants see the funds rate falling to between 3% and 3.50%.

Fed Chair Jerome Powell emphasized the word “recalibrate” to explain the Fed’s larger-than-expected rate cut in September. This aligns with two themes we’ve highlighted in the CAVU Compass. The first is Newton’s Law of Motion, which states that an object in motion continues at the same speed and trajectory unless acted upon by an unbalanced force. Here, the object in motion is the labor market, where job growth is slowing, and the unemployment rate is nearing the upper limit of the Fed’s estimate of “full employment.” The unbalanced force is the Fed’s larger-than-expected 50 bp cut in the federal funds rate.

The second theme we have focused on is that the expansion is transitioning beyond the post-pandemic recovery, which was driven by massive fiscal stimulus and unusually loose monetary policy. The effects of these measures have largely faded. The bulk of the stimulus from the CARES Act stimulus is long gone, the surge in EV and microchip plant construction is slowing, and the benefits of low interest rates, which helped strengthen balance sheets, are diminishing.

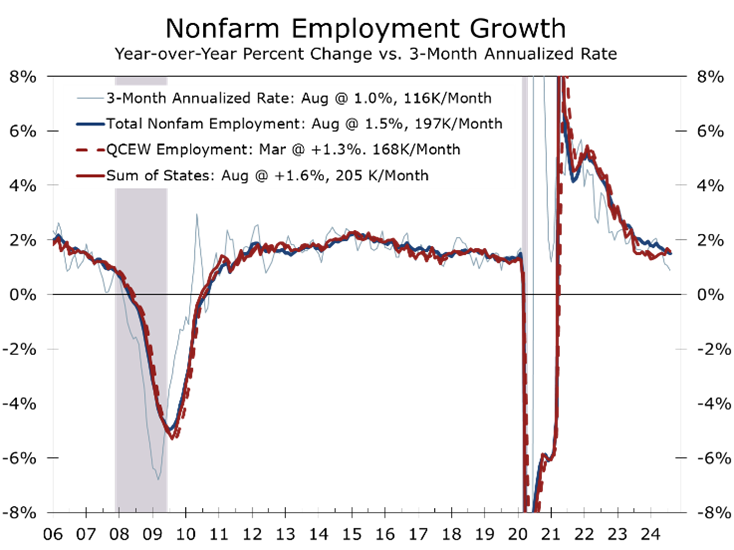

More recently, the impact of the Fed’s aggressive rate hikes has taken a bite out of labor force growth. The toll began to be clear about a year after the Fed initially hiked rates, with the bulk of the impact hitting about 18 months after policy began to tighten. Nonfarm payroll growth has decelerated from 300,000 jobs per month in March 2023 to just 114,000 jobs per month over the past three months. Not only has job growth slowed, but the breadth of job gains has narrowed considerably, with healthcare, the leisure and hospitality sector, and government accounting for a disproportionate share of job gains.

The slowdown in job growth is due to several factors. Higher interest rates have cut sales of new and existing homes and slowed purchases of big-ticket items, including light vehicles, furniture, and appliances. With demand cooling, pricing power has waned, squeezing profit margins and slowing hiring. Fewer industries are also short-staffed today than they were 18 months ago, when they were still recovering from pandemic disruptions. The upcoming election is also likely weighing on hiring, as it introduces an element of uncertainty.

Another point we have raised in previous reports and in client briefings is that the yield curve would begin to steepen once the Fed began to lower interest rates. The larger-than-expected cut accelerated this, but the curve should steepen further. We expect the 10-Year Treasury yield to surpass 4% by early next year and reach 4.30% by the end of 2025, with the 3-Month T-Bill falling to 3.2%. This steeper curve reflects the Fed’s more growth-oriented policy stance and greater patience regarding inflation’s return to its 2% target, along with ongoing concerns about federal deficits.

Despite moving past the post-pandemic phase, the economy still has significant stimulus in place. The Inflation Reduction Act and CHIPS Act will continue supporting above-average capital spending, while the bipartisan infrastructure act boosts public works. State and local governments are well-funded and have many road and water projects underway, adding upside risk to economic growth and interest rates.

One key item to watch is the comprehensive revision of the National Income and Product Accounts, released with the revised Q2 GDP data on September 26. These revisions may slightly lower GDP growth estimates for the past year, currently centered around 3%. Weekly jobless claims and the September jobs numbers will also be closely monitored, with job growth expected to rebound from its recent weak trend.

As for geopolitics, we mentioned that we would get a clearer picture of the U.S. election following the first Trump-Harris debate. Vice President Harris has come out ahead in the wake of that debate, and her victory now looks more likely. Our current read suggests Harris will win a narrow electoral majority, with the GOP regaining control of the Senate and narrowly losing the House. A sweep by either party would likely present an unwelcome surprise to Wall Street and the broader economy. A Trump victory remains possible but would likely require a surprising enthusiastic turnout and help from an exogenous event.

A sweep by either party would likely present an unwelcome surprise, adding to deficit worries.

Overseas, the Middle East is moving closer to a broader war. Israel’s initial success in Southern Lebanon has surprised and devastated Hezbollah’s leadership. The move against Hezbollah is also a clear signal that Israel is winning its battle against Hamas in a more convincing manner than has been reported. Israel is acting now because it feels it is in a stronger position to take aggressive actions while the U.S. is focused on its presidential election. Iran will likely attempt some form of intervention to save its key proxy but has so far been ineffective in combating the more technologically advanced Israeli forces. A broader war in the Middle East would lead to higher energy prices and increased global instability. China and Russia may also seek to establish a larger role in the region, potentially escalating tensions just prior to the U.S. election.

We have slightly lowered our GDP forecast through 2025. We expect real GDP growth to remain near its long-run potential, which we believe conflicts with the FOMC’s interest rate expectations, especially with the economy near full employment. This mismatch supports our view that the yield curve will steepen, reducing the effect of lower short-term rates.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 23, 2024

Mark Vitner, Chief Economist

Piedmont Crescent Capital

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000