Markets Wrestle with Inconsistencies

- Many were quick to label September’s jobs report as a return to a Goldilocks. We feel this complacency is misplaced.

- While stronger growth helps alleviate fears the labor market had cooled off too much, the composition of job gains remains skewed toward just a handful of industries.

- Hours worked also weakened in September despite the big jump in payrolls.

- Last week’s other economic reports were mixed, with the ISM manufacturing data remaining weak and ISM services data showing surprising strength.

- We see third quarter real GDP rising at a 3.1% annual rate.

- The suspension of the dockworkers’ strike comes at a huge cost. Dockworkers are set to receive a 62.5% over the next five years. That ‘settlement’ is already spurring demands for larger wage gains elsewhere.

The markets were relieved to learn that the labor market was not nearly as weak as the July and August employment data had indicated. Employers added 254,000 jobs in September, and job growth for July and August was revised modestly higher. Suddenly, the economy does not look as vulnerable as it did when the Fed opted to kick off its easing cycle with a half-percentage-point cut in the federal funds rate.

The September jobs data are encouraging. Not only did job growth ramp up, but gains were more widespread, with the diffusion index rising to 57.6, the highest since January. While more industries added workers, the bulk of job gains continued to come from just four sectors: leisure & hospitality, health care, government, and construction.

The Household Survey was also quite strong, with employment rising by 430,000, significantly outpacing the 150,000-person increase in the labor force. As a result, the unemployment rate fell from 4.22% to 4.05%. Wages remain under pressure, with average hourly earnings rising by 0.4% to $35.36, marking a 4% year-over-year increase—higher than the Fed’s target amid ongoing strike activity.

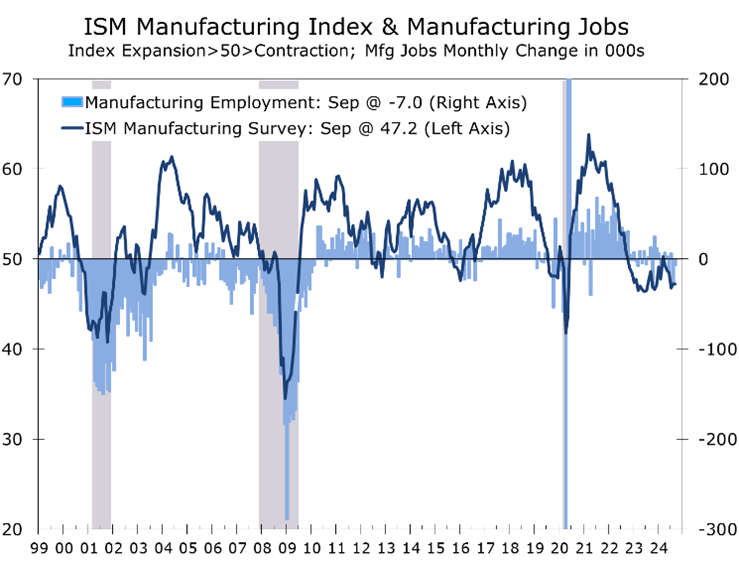

While overall employment conditions improved, manufacturing continues to struggle, with payrolls declining over the past two months and 40,000 jobs lost this year. The Boeing strike, which began in September, will impact October’s data. Weak demand for goods reflects the impact of higher interest rates. The ISM manufacturing index was unchanged at 47.2 in September and has remained below the 50 break-even level for 22 of the last 23 months, signaling ongoing contraction. While the employment index fell, production and new orders rose slightly, though all remained below 50. Manufacturing job losses align with the ISM index on a historical basis.

On a more positive note, the ISM services survey, which includes construction, rose 3.4 points to 54.9. The composition was mixed, the business activity (+6.6 points to 59.9) and new orders (+6.4 points to 59.4) components both increased strongly, driving the overall index higher. The employment component declined by 2.1 points to 48.1, signaling some softness in labor markets for the service sector, which is evident. The prices paid index moved higher, up 2.1 points to 59.4, indicating some inflationary pressures.

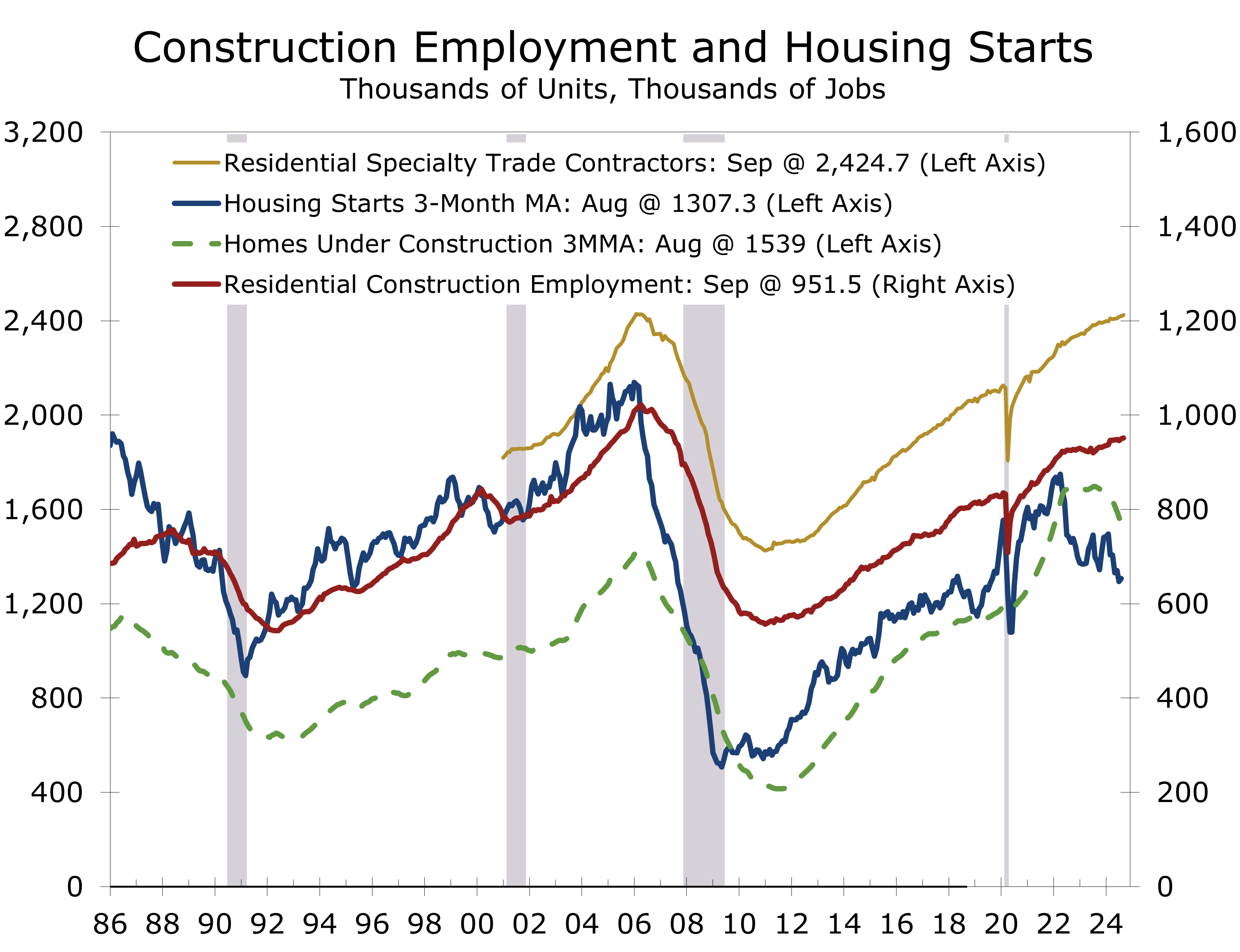

Construction has been a source of strength recently, benefitting from both residential and nonresidential construction. While housing starts have weakened of late, particularly new apartment projects, there is still a great deal of work in the pipeline. Nonresidential continues to benefit from major fiscal initiatives including construction of EV assembly and parts plants, microchip plants and infrastructure improvements. Here too, new projects are slowing but there remains a considerable pipeline of projects underway.

One reason construction employment has held up so well is that there has been an abundance of open positions and hiring has slowed in other industries. Immigration has also helped, with a large number of recent immigrants receiving temporary work permits. This has been particularly helpful in many of the trades, including framing, painting and landscaping.

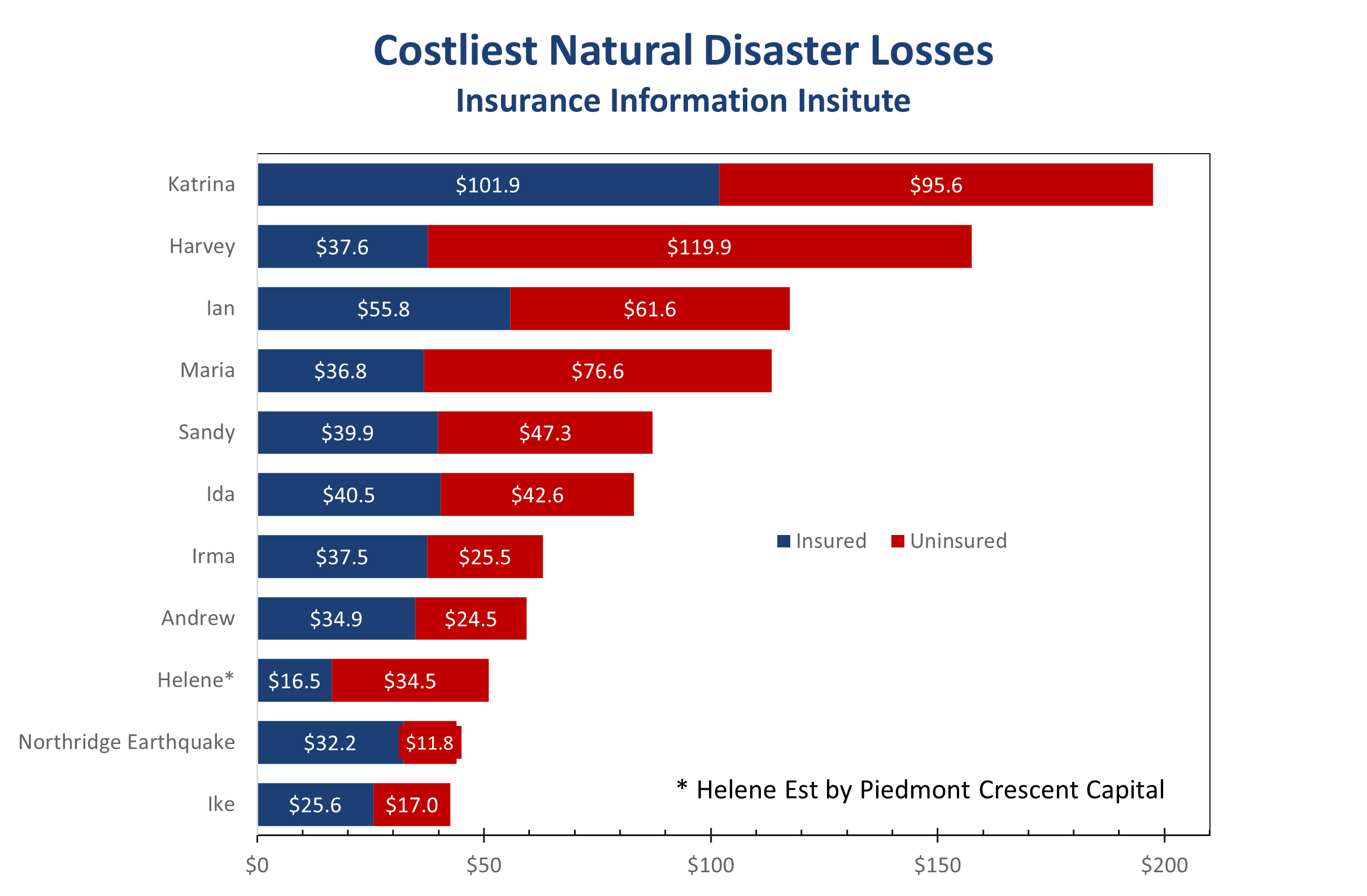

The latest estimates put losses from Hurricane Helene at 230 fatalities and approximately $41 billion in property damage, much of it from uninsured flood damage. The storm impacted Florida’s Big Bend, swept across Georgia from the southwest to the northeast, and hit the western Carolinas, eastern Tennessee, and southwest Virginia.

The greater Asheville area, up to the Tennessee border, was hardest hit by flooding and is expected to face prolonged economic disruption. October is the peak of the tourist season, as visitors flock to see the changing leaves. We estimate that Helene-related closures could reduce October nonfarm payrolls by around 50,000 jobs, primarily in leisure and hospitality, as well as professional services. Construction may see a modest uptick due to cleanup efforts.

Flood damage is difficult to assess, and early estimates are likely conservative. We estimate insured losses at approximately $16.5 billion, mostly from wind, with uninsured losses more than doubling that, reaching $34.5 billion. Recovery from the storm is expected to be slow, particularly in areas hardest hit by flooding.

In the longer term, we expect migration out of the affected areas, as rebuilding efforts will require stricter standards, potentially pricing out many residents. As housing becomes even less affordable, many residents are likely to resettle in major metro areas in the region, particularly Charlotte, Greenville, and Winston-Salem.

October also marks the one-year anniversary of the war between Hamas, Iranian proxies, and Israel. The surprise attack on October 7 caught Israel off guard and marked one of the largest intelligence and operational failures in its history. Not only was Israel dealing with the largest loss of Jewish life since the Holocaust, but ordinary Israelis were concerned about the survival of the Jewish state.

Israel has come a long way over the past year. Its victory over Hamas has defied expectations from virtually all Western governments, particularly the U.S. The recent pivot to targeting Hezbollah has been nothing short of spectacular, resulting in the elimination of much of Hezbollah’s leadership and enabling Israel to make significant gains against its rank-and-file forces while resulting in minimal civilian and Israeli casualties.

Will Israel choose to send a message to the snake or opt to cut off the head of the snake?

Today, it is Iran’s leadership that is concerned about its survival, actively sending messages to other nations to rein Israel in. The question now is how and when Israel will respond to the 180-missile barrage Iran launched at Israel on October 1. There is widespread speculation that Israel will target Iran’s oil production and distribution facilities or possibly their nuclear sites. Israel’s leadership remains tight-lipped.

The critical question for Israel is whether to send a message, as it did in April, and potentially scare off the snake, or to go straight for the head. If they choose the former and fail, Iran will likely push more aggressively to develop nuclear weapons. If they choose the latter, they must succeed, as failure could undo much of what Israel has accomplished so far.

We expect Israel to continue pushing hard into Lebanon and Gaza as the U.S. moves closer to the presidential election. We would be surprised if Israel tipped its hand before acting, given the remarkable success of their surprise beeper and walkie-talkie attacks against Hezbollah, as well as their more direct efforts to eliminate the leaders of Hezbollah and Hamas.

Our final thought this week circles back to where we began. There seems to be growing complacency around the belief that the Federal Reserve has successfully engineered a soft landing, with diminished risks of inflation and a slowdown in job growth or the broader economy. We do not share this view.

Moreover, we are concerned about the inconsistency in both the Fed’s and consensus forecasts, which call for another 150 basis points of cuts in the federal funds rate, while predicting strong economic growth and low unemployment. If growth is that strong, the Fed wouldn’t need to cut rates.

While third-quarter growth is likely to come in around 3%, we expect fourth-quarter growth to slow to less than 2%, as businesses and consumers pull back ahead of the presidential election and the hurricanes cut spending. Additionally, we believe the risk of inflation remaining above the Fed’s target is higher than what the market has priced in. The suspension of the dockworkers’ strike, while a relief, comes at a cost—labor unions are now emboldened, making a resolution to the Boeing strike more difficult.

Our forecast calls for economic growth to slow to just under a 2% pace over the next three quarters. This slowdown should allow the Fed to continue cutting the funds rate down to 3.50%. However, with unemployment remaining low, we expect the yield curve to steepen, making it harder for lower short-term rates to effectively boost economic growth.

The election looks too close to call, but the Harris campaign seems to be steadily losing momentum. A divided government remains the best result from the market’s perspective and still appears to be the most likely outcome. A sweep by either party raises the risk of even larger federal deficits.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.