Highlights of the Week

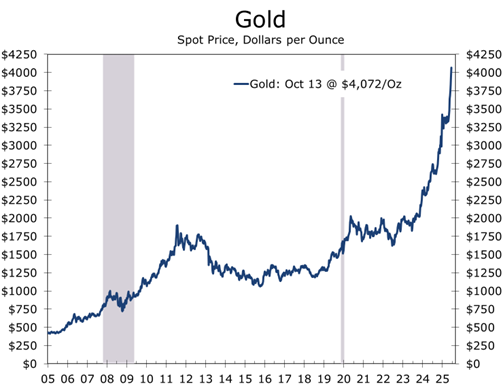

- Gold’s rally evokes a 1970s déjà vu — a mix of inflation anxiety, policy division, and global unease.

- Markets closed the week defensively as trade tensions resurfaced and data visibility dimmed under the government shutdown.

- The Nobel Peace Prize went to Venezuela’s María Corina Machado, sparking celebration abroad and political theater at home.

- A ceasefire took effect in Gaza, expected to return all living hostages and the remains of those who died in captivity — but peace remains elusive.

- Tariff and currency volatility reemerged as global risk drivers, with China’s export curbs and Washington’s 100% tariff threat triggering safe-haven flows into gold and Treasuries.

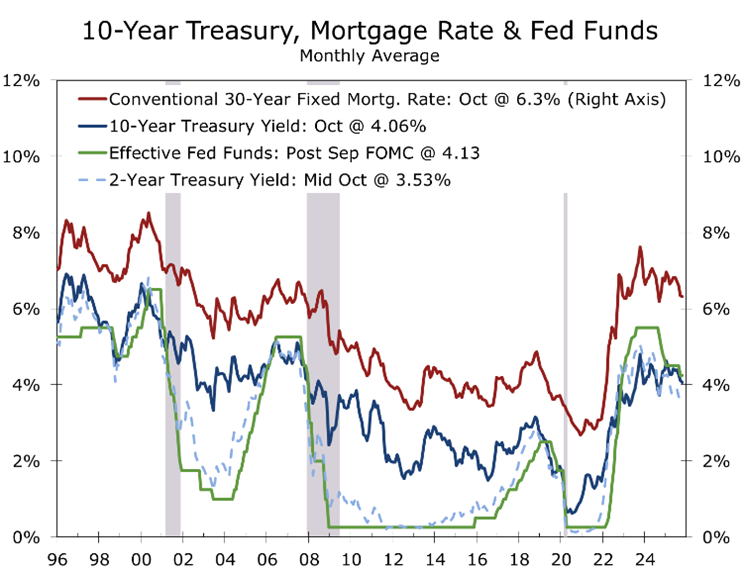

- Bond yields compressed and equity volatility climbed, as investors priced in slower growth, policy uncertainty, and a potential October rate cut.

- Investors appear to be buying insurance against uncertainties: both known and unknown. The Gaza ceasefire is a good first step at bringing some certainty back into play.

Headwinds and Handlebars: Some Vacation Reflections – Somewhere along Italy’s Adriatic coast this past week, I found myself pedaling into a headwind strong enough to feel personal. The road hugged the sea, sunlight glinting off an endless stretch of whitecaps as we made our way back from Santa Maria di Leuca — the southernmost point of the Salento Peninsula, or more simply, the heel of Italy’s boot. Even on the downhill stretches, the wind was so fierce you had to keep pedaling just to make headway. It struck me that markets are doing much the same.

Confidence has become the currency of this cycle — and gold is its barometer.

The resistance traditional assets face — inflation anxiety, political distrust, and weakening confidence in global institutions — are headwinds for growth but tailwinds for gold, crypto, and other safe havens. Progress now depends on the sectors still pedaling hardest — AI, data centers, and infrastructure — whose steady effort keeps the economy moving even when gravity should be taking over.

A few days later, our ride wound inland through Puglia’s ancient olive groves, where gnarled trees — some planted before the discovery of the New World, and capitalism itself — still yield oil as golden as the coins now coveted by investors. Those trees have endured conquests, plagues, and wars, their deep roots and slow reward standing in quiet defiance of today’s jittery markets — driven by the next big thing but weighed down by the next big worry.

Each turn of the pedals brought a reminder of equilibrium: effort met by resistance, progress tempered by patience. Investors are doing much the same — stretching for yield, recycling old assumptions to reconcile a new set of risks, and trying to shape something smooth from systems that refuse to remain still.

.

It is always hard to find time for a long vacation, particularly one that requires careful planning. When we departed, the timing seemed perfect. The weather forecast was ideal, and the U.S. government shutdown meant most data releases would be suspended for the bulk of our trip. The world’s attention was focused on the proposed and now agreed upon ceasefire in the Israel–Gaza conflict. Yet even from afar, it was clear that markets were wrestling with the same question I faced on that windy coastal road — how to keep balance when the terrain keeps changing.

The Week in Markets: A 1970s Show Reboot

Gold stole the show last week, climbing to record highs as investors dusted off a script last performed in the 1970s — when inflation, geopolitics, and trust all seemed to unravel at once. Back then, Americans waited in gas lines by day and watched prices spiral by night as the global financial order wobbled in real time. After Nixon severed the last link to the Gold Standard, gold and silver became the decade’s twin obsessions — safe havens for some, speculative addictions for others.

.

Today’s version stars an overworked Fed, underinformed markets (thanks to the prolonged shutdown), and a global audience binge-watching for clues — wondering whether this time, the ending is different. But the cast of commodities has changed: where oil once defined the economic anxieties of the 1970s, rare earths and high-end semiconductors now occupy center stage, as China’s expanded export controls threaten to weaponize supply chains and extend the trade war far beyond tariffs.

Gold’s latest rally has little to do with inflation — and everything to do with confidence, or the lack thereof. Confidence has become the currency of this cycle. It anchors expectations when data go dark and defines market psychology when the instruments go blank.

Bond yields retreated, particularly in the 2-to-10-year range, as traders extended bets on an October rate cut, now priced around 65%. Treasuries caught a late-week flight-to-safety bid after President Trump threatened a “massive increase” in China tariffs is response to Beijing’s unusually harsh new restrictions on rare earth exports— a reminder that in today’s economy, minerals and microchips have replaced oil as the leverage points of global power.

Israel Under Pressure—and Shifting Global Currents

With no official jobs or inflation data released, markets flew on instruments guided by private signals. Reports from ADP and Challenger released earlier this month show the labor market continuing to lose momentum. High-frequency data suggest this trend continued into mid-October, perhaps amplified slightly by federal payroll cuts. State filings and shutdown-related disruptions point to jobless claims near 235,000 — consistent with a labor market that is cooling gradually, not collapsing.

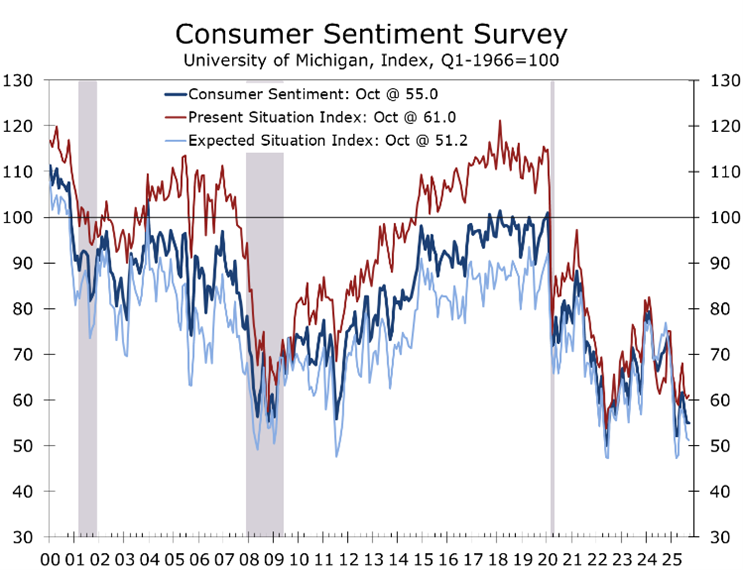

The early read on October consumer sentiment was steady on the surface but softening beneath. The University of Michigan index was virtually unchanged at 55.0 (down from 55.1), but consumers rated now as the worst time to buy durable goods since 2022. Year-ahead inflation expectations slipped modestly to 4.6%, while long-run expectations held at 3.7% — still above the Fed’s comfort zone.

Stocks ended the week lower as tariff headlines erased midweek gains. The S&P 500 fell 1.3%; the Nasdaq 1.8%, led by megacap pullbacks. The 10-year Treasury yield dipped below 4.1%; oil prices fell roughly 3.5%; and Bitcoin hovered near $112,000 — a speculative mirror to the VIX.

For all the talk of gold bugs, the message was broader: when markets doubt the pilots, they reach for parachutes — and last week, they bought a lot of them.

Macro Backdrop: Flying Blind

The economy remains resilient, even with poor visibility. With the government still shuttered, investors have been forced to navigate by intuition and incomplete signals. The picture that emerges is one of an economy that continues to move forward — but increasingly by feel rather than sight.

Private consumption indicators are steady, business investment remains strong in AI and related infrastructure, and housing shows tentative signs of stabilizing. Mortgage demand has rebounded as rates ease toward 6%, and builders are discounting prices to clear a growing inventory of unsold new homes. Job creation is clearly ebbing, however, and the Fed’s “dual mandate” is beginning to split along partisan lines. Inflation expectations have nudged modestly higher — not on data, but on psychology.

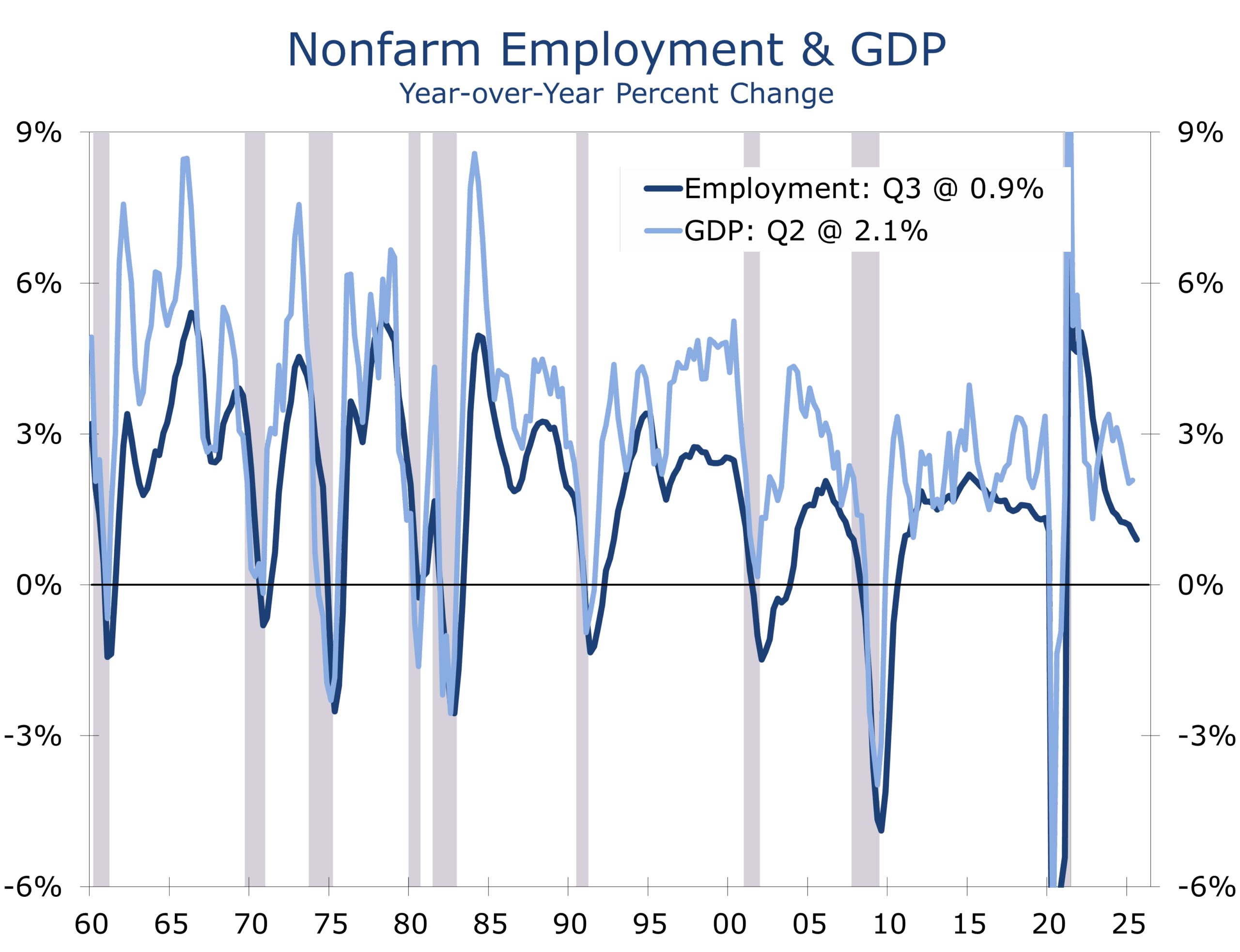

Meanwhile, the shutdown has turned the nation’s data stream into radio static. Economists have become codebreakers, piecing together fragments from Redbook, ADP, and credit-card data to fill the void. Expectations for Q3 GDP growth remain near 3%, but most Q4 forecasts have slipped into the 1.5%–1.8% range (a touch below our own 2.0%) as uncertainty delays spending and hiring decisions. Private indicators — and the federal furloughs that have thinned payrolls — suggest job growth is tepid at best and may already be turning negative. The larger question is how long the expansion can endure with the labor market faltering. History would say not long, but perhaps we are witnessing the rise of a second “new economy.”

.

U.S.–China: Tariffs, Technology, and the New Oil

Trade tensions flared again after Washington threatened to impose 100% tariffs on all Chinese imports — a dramatic escalation aimed at countering Beijing’s newly expanded export controls on rare earth elements and related technologies. Under the new rules, Chinese exporters must obtain government approval if Chinese content accounts for more than 0.1% of a product’s value, with licenses limited to six-month terms and subject to discretionary renewal — signaling that Beijing may selectively target rapidly growing U.S. technology and defense-related firms.

Beijing has already been slow-rolling existing export approvals, effectively tightening supply without a formal ban. These measures mark a shift from tariffs to technological choke points, turning access to critical minerals into a lever of geopolitical power. Washington’s retaliatory tariff threat — coupled with potential export controls on U.S. software and aircraft components — underscores how both sides are now weaponizing their comparative advantages: China’s dominance in critical mineral refining and America’s leadership in innovation and code.

We believe President Trump and President Xi are positioning themselves for negotiations later this year, likely using these threats to shape leverage ahead of potential discussions on the sidelines of the upcoming APEC summit in South Korea. While both sides may delay implementation for several weeks as talks proceed, the episode introduces yet another headwind for a global economy already losing momentum.

It’s a confrontation reminiscent of the 1970s energy shocks. Then, oil linked geopolitics to inflation and power; today, that role belongs to rare earths and semiconductors. Supply chains have become the new battle lines of national security, and markets — once buffered by globalization — now move in rhythm with each strategic announcement from Washington or Beijing.

Europe and Asia: Fragile Mandates, Fading Margins of Error

Political turbulence in France and Japan added fresh layers of uncertainty. In Paris, President Emmanuel Macron reappointed Sébastien Lecornu as prime minister after a destabilizing resignation. The reshuffle underscores Macron’s eroding authority in a divided parliament, where fiscal reform has stalled amid budget battles and social unrest. With borrowing costs rising, France’s paralysis threatens to widen OAT-Bund spreads and rekindle talk of a “two-speed Europe.”

In Tokyo, the collapse of Japan’s ruling coalition after Komeito’s withdrawal left Prime Minister Sanae Takaichi struggling to form a majority. The yen’s slide to multi-decade lows reflects doubts about the BOJ’s willingness to exit ultra-loose policy. Inflation has stabilized near 2%, but wage growth remains weak, and fiscal expansion tied to defense and energy subsidies has blurred the line between monetary and fiscal policy.

In both nations, credibility — not capacity — is the constraint. France faces pressure to enforce fiscal discipline without unrest; Japan, to defend the yen without reigniting deflation. The erosion of confidence in long-ruling parties has become a global motif — one that helps explain why gold and cryptocurrencies continue to climb.

The Nobel Peace Prize: Symbolism in a Cynical Age

The 2025 Nobel Peace Prize was awarded to María Corina Machado, the Venezuelan opposition leader long barred from public office by Nicolás Maduro’s regime. The committee cited her “unwavering advocacy for peaceful democratic transition.”

Machado dedicated the award to “the people of Venezuela — and to those who stood with us,” a clear nod to Donald Trump’s diplomatic pressure on Caracas. The move sparked admiration abroad and outrage at home, turning a humanitarian prize into a political lightning rod.

Nominations for the prize were due on January 31 — just eleven days after President Trump took office — far too early to reflect his later diplomatic achievements, including the breakthrough agreement between Israel and Hamas.

Internationally, the award was celebrated as a moral statement — democracy over détente — but in the United States it reopened partisan wounds. Some critics called it a “snub” to Trump, while others praised the committee’s independence. Like so many peace prizes, this one said more about the state of the world than about peace itself: it celebrated courage but reminded us how rare peace has become.

The Week Ahead

- U.S. Data: The shutdown’s continuation means limited new information, though private trackers for retail sales and jobless claims will be closely watched. The NFIB Small Business Optimism Survey (Tuesday) will be key for clues on supply chain strain and inflation pressures.

- Fed Watch: Markets will parse speeches from Waller and Bowman, as well as Wednesday’s Beige Book, for signals on whether October remains “live” or if a cut is now a virtual certainty.

- Geopolitics: All eyes on the Gaza truce — if it holds, oil could retreat; if it fails, risk spreads widen again.

- Earnings: Banks kick off reporting season — providing stress test results for credit conditions and consumer sentiment.

Closing Thoughts: The Road Ahead

On the final day of the ride, coasting downhill toward Monopoli, the wind finally shifted at my back. The Adriatic shimmered in the evening light, and for the first time in days the climb felt worth it. It was that same afternoon the trade deal with China came off the rails — Beijing tightening exports of critical materials and magnets, Washington retaliating with threats of 100% tariffs. The headwinds that had eased along the coast were rising again in the markets, unseen but unmistakable.

Progress in policy, like cycling through crosswinds, rarely comes with momentum alone. It demands endurance — the ability to keep pace when the path tilts against you and the signals ahead blur. Gold’s gleam this month reflects less fear of inflation than a loss of faith: in policymaking, in coordination, and in the systems meant to anchor both.

Like those ancient olive trees rooted in the rocky soil of Puglia, investors who hold their ground through seasons of strain tend to outlast the storm. The road ahead will twist and rise again — it always does — but those who shift gears with purpose rather than panic will find that even the steepest ascent offers a broader view from the summit.

Concluding Thoughts: The Penalties from Hell

Vacations have a way of inviting reflection — especially when surrounded by inspiring architecture, landscapes, and art. We have switched from biking to touring — and from one coast to another. On our first day in Sorrento, we toured an exhibition of Joan Miró, whose work was as colorful as it was thematic across the decades of his long and illustrious career.

Israel’s long war with Hamas brings to mind Miró’s Les Pénalités de l’Enfer — “The Penalties of Hell” — a phrase that captures both the fury and the necessity of this drawn-out conflict. The title originated in Miró’s early 1970s collaboration with poet Robert Desnos, where chaos, color, and anguish collided on the page. Miró’s vision was an artistic outcry against cruelty and constraint; Israel’s version is tragically literal — a campaign of force aimed at dismantling an organization that glorified death and desecrated innocence. Each, in its own way, represents a struggle to make sense of evil through expression — whether on canvas or in combat.

The parallels with 1973 extend beyond the calendar. Then, the Yom Kippur War triggered the Arab oil embargo and unleashed the inflationary spiral that defined the decade. Today’s conflict unfolds amid a different kind of shock — less about oil, more about trust and technology — dividing the world once again into blocs aligned with the U.S. and Europe on one side, and Russia, China, North Korea, and Iran on the other. Yet this time, the arc may prove more hopeful. The Abraham Accords have opened a path toward normalization between Israel and its Arab neighbors — a peace built not on illusion, but on mutual interest: trade, security, and shared resistance to extremism.

The 1970s ended in disillusionment and disorder. This decade could still close in redefinition and renewal. The “penalties from hell,” both as art and as policy, remind us that order often emerges only after the most violent ruptures. What Miró rendered in abstraction, Israel now lives in reality — a confrontation with darkness that tests whether civilization still has the will to defend itself.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 13, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000