Highlights of the Week

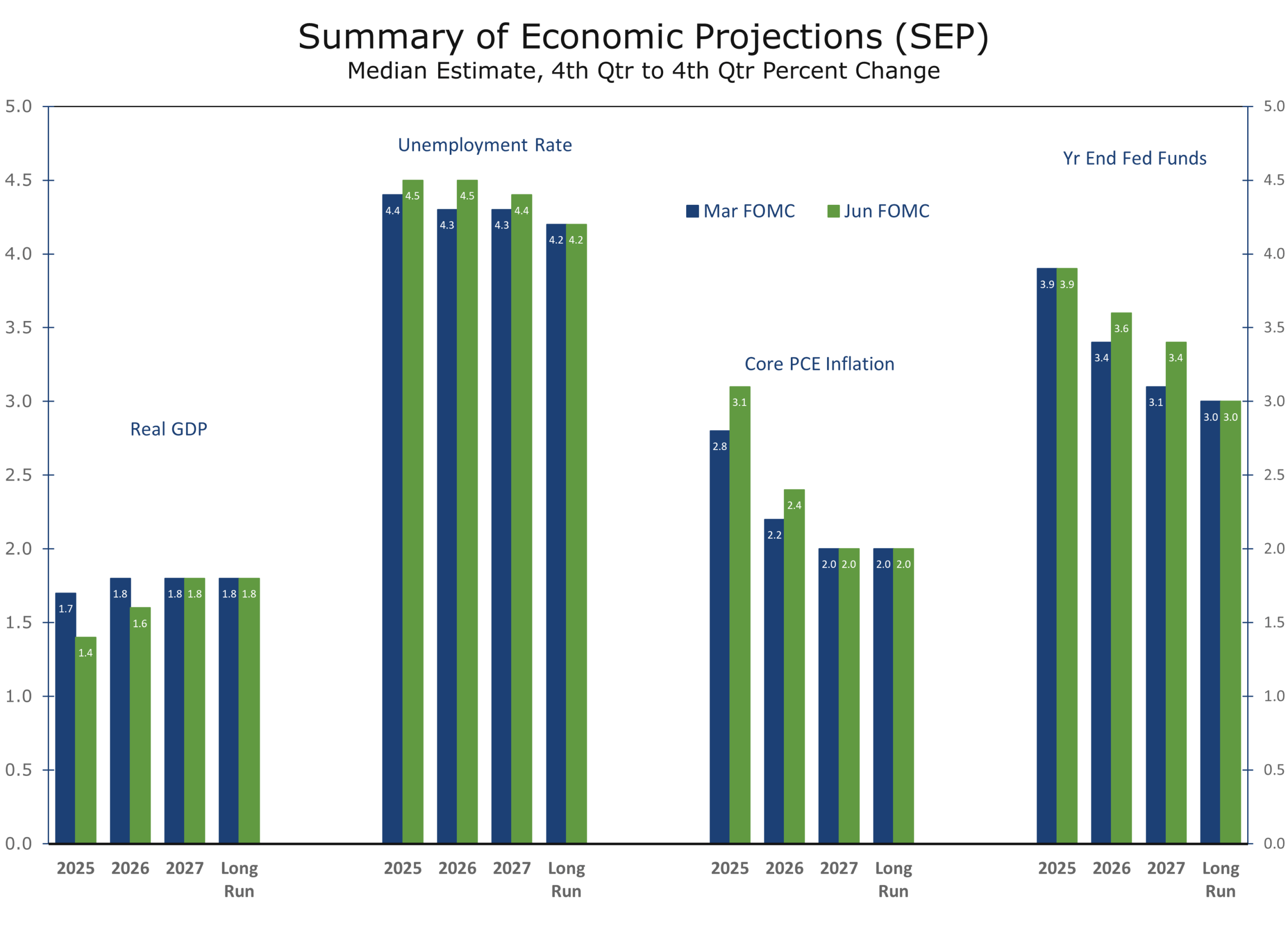

- The Fed is poised to cut rates this week, but Powell’s tone and the next two inflation prints will determine whether it’s the start of a string of three or more successive cuts, or a more drawn out data-dependent process.

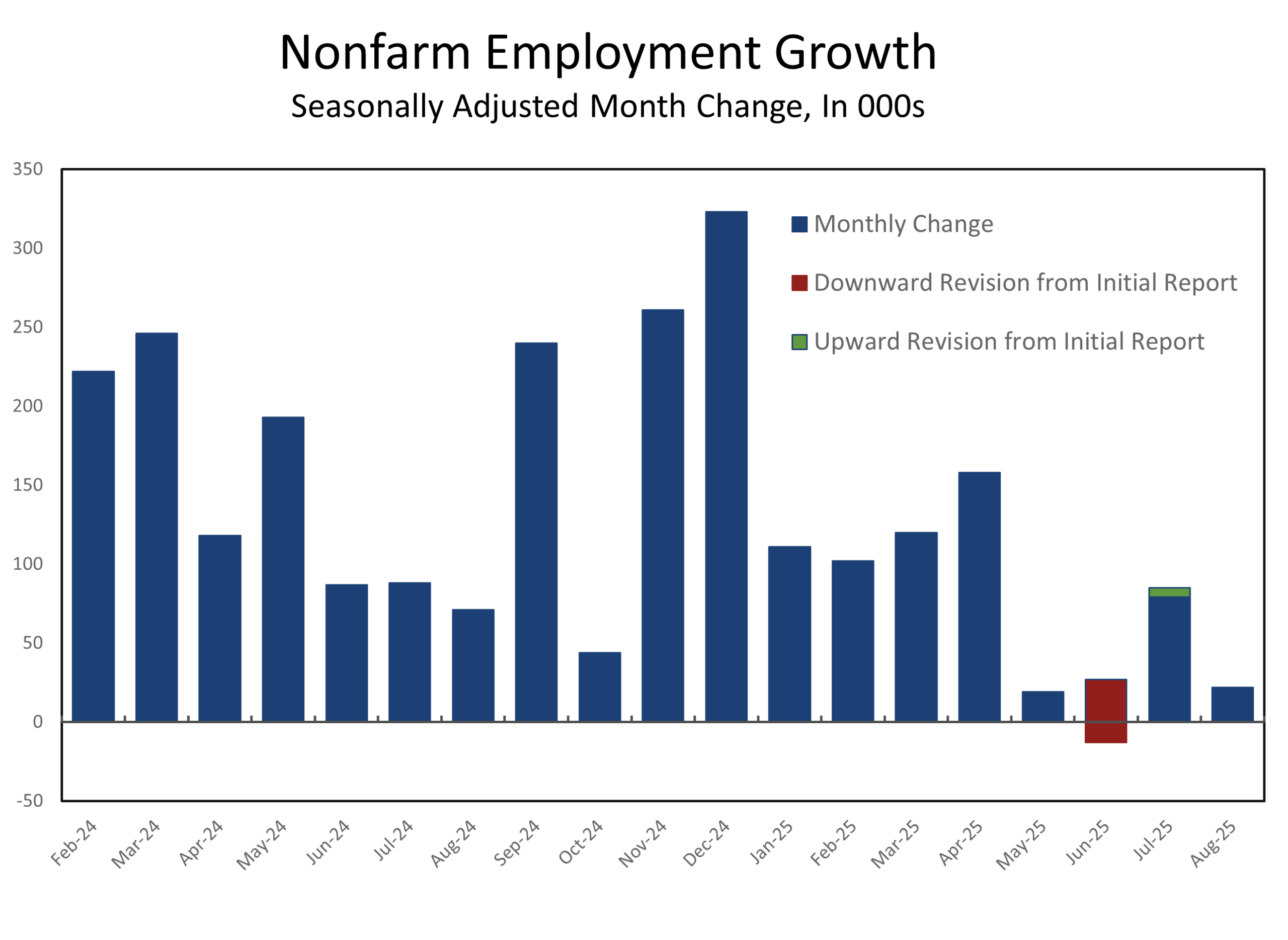

- QCEW revisions revealed that job growth has been much weaker than reported, suggesting underlying job growth is now running at around 25K per month and leaving little margin for error.

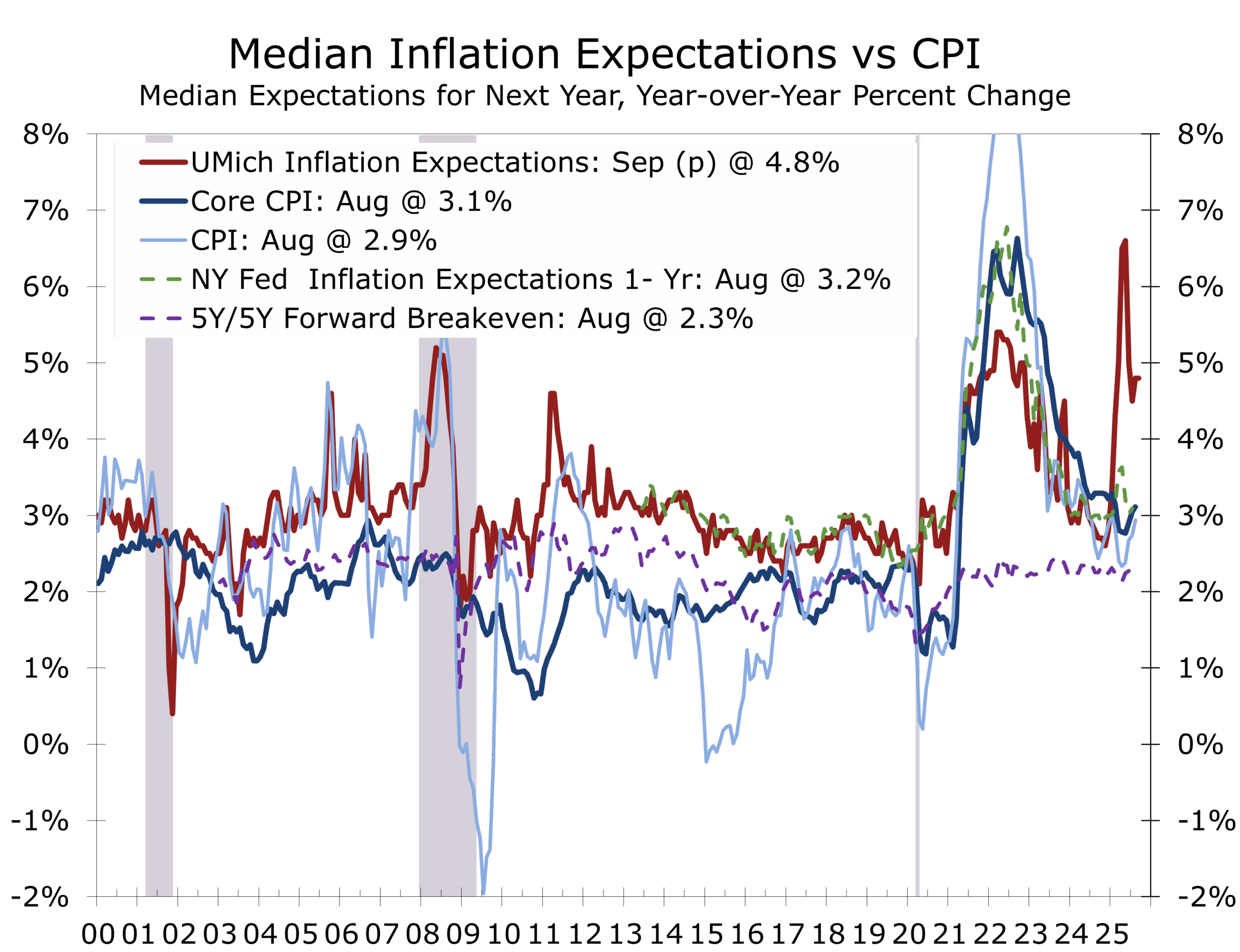

- Inflation reports show tariff effects in goods but no broad overheating, while long-term expectations remain well anchored.

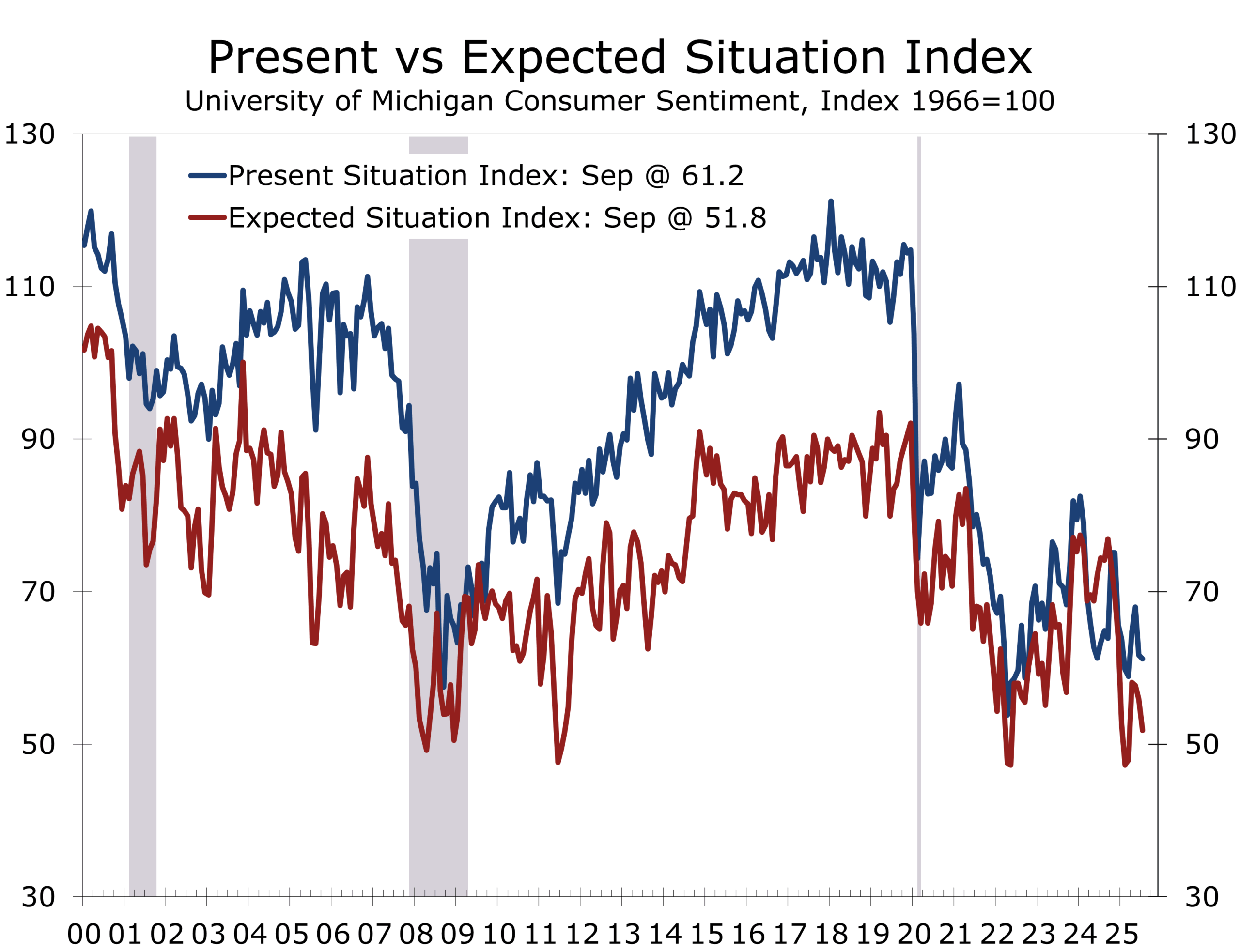

- Consumer sentiment fell more than expected in September, with households increasingly concerned about jobs and tariffs.

- Housing is plateauing, with inventories of completed homes weighing on new construction and affordability still the key constraints.

- Geopolitical tensions are rising: Russia intensifies strikes, Israel extends operations—including an attempted decapitation strike on Hamas leadership in Qatar—and Venezuela continue to provoke Guyana and the U.S. Navy. Domestically, the assassination of Charlie Kirk injects fresh volatility into U.S. politics.

- Cross-asset positioning favors duration and steepeners, with gold and EM credit benefiting from weaker dollar dynamics and selective upside emerging in Chinese internet equities.

Markets in Limbo

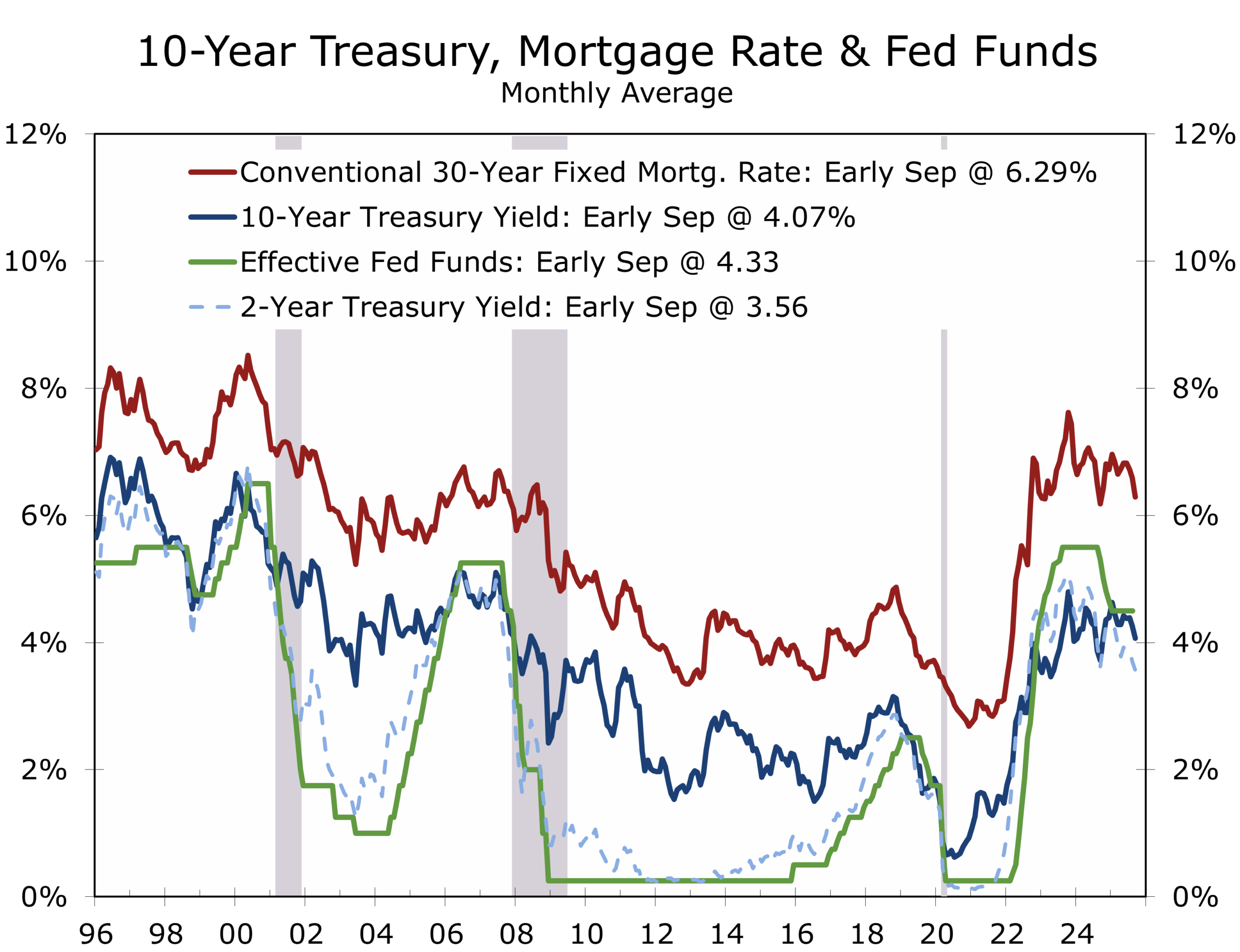

Markets begin the week in a holding pattern—defensive but orderly. The Treasury curve continues to steepen, with short-end yields anchored by expectations of Fed easing while the long end wrestles with heavy supply and elevated geopolitical risk premia. Equities remain near record highs, supported by resilient earnings, though valuations leave little margin for error. Credit spreads are tight, and agency MBS spreads narrowed further on dovish repricing, with larger bank demand likely to re-emerge as liquidity improves into October. Positioning remains tilted toward duration and steepeners, a measured hedge as policy, inflation, and geopolitics intersect.

The Fed can accomplish more by doing less—cut rates but avoid overcommitting to a rapid pace.

Countering the weakening labor market has become the Fed’s overriding objective and will remain so until growth re-accelerates or inflation rises beyond the expected temporary bump from tariffs. The challenge now is communication. The Fed can accomplish more by doing less—anchoring expectations without overpromising on cuts.

.

Labor Market — QCEW Rewrites the Narrative

August’s payroll gain of just 22,000 was troubling on its own, but the real story came from the BLS’s preliminary benchmark revision incorporating QCEW data. The revision cut 911,000 jobs from payrolls between April 2024 and March 2025—the largest downward adjustment since at least 2000—halving average monthly gains to 71,000. Job growth has slowed even further since then, averaging only 41,000 per month from April through August.

QCEW revision: 911,000 jobs cut from April 2024–March 2025 payrolls

The revisions were concentrated in leisure and hospitality, professional and business services, manufacturing, and trade, while education, healthcare, and government employment were little changed. The unemployment rate rose to 4.3% in August, and broader slack measures suggest even greater weakness. The jobless rate would likely be at least half a percentage point higher were it not for the outflow of foreign-born workers since the start of the year, which has reduced measured labor supply.

The QCEW confirms that the labor market has cooled sharply, particularly among smaller firms, and leaves the Fed with little choice but to pivot its focus squarely toward the downside risks to employment embedded in its dual mandate.

Inflation — Tariffs Bite, but Expectations Stay Anchored

August’s inflation reports showed tariffs feeding into goods prices but offered little evidence of broad overheating. Headline CPI rose 0.4% (2.9% year-on-year) and core CPI increased 0.3% (3.1% year-on-year). Goods prices firmed on higher import costs, while services inflation held steady near 3.6%. Producer prices were softer, with headline PPI down 0.1% and core measures pointing to margin compression rather than pass-through to households, following unusually large gains in July. Supply chains remain fluid, delivery times stable, and wage growth is slowing as labor demand weakens.

The greater risk for policymakers is not current inflation but expectations, which is why the Fed must get its messaging right. Short-term tariff effects could unsettle psychology, but the latest surveys suggest stability. The New York Fed’s Survey of Consumer Expectations showed one-year expectations ticking up to 3.2%, while the three-year (3.0%) and five-year (2.9%) horizons held steady—providing Chair Powell with cover to pivot toward labor support at Jackson Hole. Anchored long-term expectations distinguish today’s environment from 2021–22, when inflation psychology unmoored and forced aggressive rate hikes.

Still, fragility is evident. Consumers view the labor market as the weakest since the NY Fed series began in 2013, and more now expect unemployment to rise over the next 12 months. That shift implies rising precautionary saving, softer spending, and an economy leaning further into disinflation. The Fed has room to ease, but the runway is short—and a geopolitical shock could close it quickly.

Consumer Sentiment — Softer and Splintered

The University of Michigan’s preliminary September reading fell to 55.4, with both current conditions and expectations deteriorating. Long-term inflation expectations edged up to 3.9%, underscoring how tariff worries weigh heavily on household psychology. Nearly 60% of respondents mentioned tariffs unprompted, highlighting the growing salience of trade policy. The sharpest declines were among lower-income households, who bear the brunt of higher costs and have not shared in equity market gains.

Tariffs are weighing on sentiment. Nearly 60% of households mention tariffs unprompted.

While sentiment surveys have been less reliable since the pandemic, the directional signal is clear: spending resilience is fading and households are bracing for a less certain labor market and slower growth. Consumption has already pulled back, most notably among middle- and lower-income households, but it has not shut down. Spending has bent, not broken—but the cracks are now spreading up the income curve.

Housing — Plateau, Not Rebound

Housing remains stuck in neutral. Rising inventories of completed homes are weighing on builders, while affordability remains the key constraint. Mortgage rates have fallen to the low 6s and should provide some relief but are not enough to spark a broad recovery. Builders remain disciplined with incentives and cycle-time management. Without rates dropping below 6%, a strong rebound is unlikely. A drop below 6% would likely require more economic weakness, which would also sideline potential home buyers, leaving the sector in a plateau rather than recovery. Housing is no longer the swing factor—it is the stalemate sector.

Geopolitics & U.S. Political Risk — Polarization Adds to Policy Risk

Global tensions remain elevated. Russia’s intensified strikes in Ukraine, including drones intercepted over Poland, underscore how easily the conflict could spill into NATO territory. In the Middle East, Israel’s attempted decapitation strike on Hamas leadership in Qatar signals its intent to pursue Hamas globally but risks undermining one of the few viable diplomatic channels. Meanwhile, the U.S. Navy’s strike on another suspected drug-running vessel off Venezuela highlights Washington’s growing footprint in the Caribbean, where tensions over Guyana’s oil-rich Essequibo region persist.

Israel–Hamas: Attempted strike in Qatar highlights conflict crossing borders

In Asia, trade negotiations between the U.S. and China have taken on new urgency. The latest talks suggest a tentative framework that would reduce tariff escalation in exchange for greater Chinese purchases of U.S. agricultural and energy products. Markets have read this as a modest sign of stabilization in an otherwise adversarial relationship. At the same time, the apparent deal to restructure TikTok’s U.S. operations—with American investors and technology partners taking a controlling stake—underscores how trade policy and technology security have become inseparable. While these developments reduce near-term uncertainty, they highlight a longer-term reality: U.S.–China competition is shifting from tariffs toward technology, data, and capital flows.

Domestically, the assassination of Charlie Kirk has deepened partisan divides and injected fresh volatility into U.S. politics. The tragedy has galvanized fundraising, hardened rhetoric, and intensified debates over free speech, extremism, and the role of social media. It also underscores how digital platforms have become both an economic flashpoint and a political accelerant. Against this backdrop, polarization could easily spill into fiscal negotiations. With the September 30 fiscal year-end deadline approaching, Congress must pass appropriations or a continuing resolution to keep the government funded. The atmosphere in Washington is combustible. While some Republicans appear willing to use the threat of a shutdown as leverage, Democrats may be less inclined to risk a lapse in funding at a time when demonstrations could quickly turn ugly.

For markets, the concern is not simply a shutdown itself but the perception of dysfunction and unrest that could accompany it. Political volatility feeds into fiscal uncertainty, raises the term premium in Treasurys, and complicates the Fed’s already narrow policy runway at a time when external shocks remain elevated. If unrest takes hold, adversaries may sense an opening—politics, not policy, could become the next real shock for markets.

Global Bond Markets — Three Stories, One Theme

Global bond markets are moving along diverging paths. In the United States, Treasury yields continue to steepen as Fed easing expectations anchor the front end while heavy fiscal supply and political risk push the long end higher. Europe faces the opposite challenge: weak demand and disinflation are pulling Bund yields lower, and the effect is spilling into CE3 bonds—the sovereign markets of the Czech Republic, Poland, and Hungary—which typically track Bunds with a spread premium and are now flattening as growth momentum fades. In Asia, government bonds remain anchored by policy: Japanese yields are capped by the Bank of Japan’s cautious stance, while Chinese bonds benefit from persistent deflationary pressure and restrained stimulus.

Europe/CE3: Bund yields drifting lower, CE3 curves flattening

The common thread across regions is that fiscal dynamics, not just monetary policy, are increasingly driving yields. The global bond market is no longer telling one story—it is telling three, and each points to a world where politics and policy carry more weight than growth.

.

Looking Ahead

- Tuesday – September 16: Retail Sales are expected to rise modestly, with core retail sales up 0.2%. Import Prices will likely rise 0.3%. Industrial Production is expect to decline modestly on milder weather, with manufacturing output down 0.1%.

- Wednesday – September 17: Housing Starts expected to trend lower, with both single- and multifamily activity cooling. The FOMC is expected to cut the federal funds rate by 25bp; Powell’s tone and dot plot will shape expectations for further easing.

- Thursday – September 18: Initial Unemployment Claims should pull back from last week’s spike. The Philadelphia Fed Manufacturing Index expected to improve slightly from 0.3 to low positive territory.

Final Thoughts

The QCEW revisions reveal a labor market weaker than anyone expected, while inflation remains contained and expectations anchored. That combination gives the Fed the runway to cut this week, even if tariff effects keep the data noisy. But with consumer sentiment fading, housing stalling, and both international and domestic political risks intensifying, the path forward looks narrower. The soft landing is still possible—but the margin for error is shrinking fast.

The Margin for Error in Politics is Also Shrinking

The Vietnam War-era song One Tin Soldier — more commonly known as the theme from the early 1970s movie Billy Jack — tells of a people who destroyed their neighbors for a treasure, only to discover that the treasure was not gold or silver, but a simple message: Peace on earth.

Recast for today, that treasure is freedom of speech. It is the foundation of our civic life — the ability to exchange ideas, to challenge one another, and to do so without fear.

Charlie Kirk’s assassination shows what happens when violence replaces dialogue. Silencing a person does not silence their ideas. Instead, it erodes the very treasure that sustains a free society.

As a society we should honor Charlie’s memory not only by mourning, but by recommitting ourselves to the defense of open discourse. Freedom of speech is the treasure we must protect. That means resisting the temptation to weaponize words like fascist, racist, or Nazi simply to discredit others. It means choosing honest debate over slander, dialogue over division, and civility over violence.

If freedom is treasure, then protecting the conversation itself is how we preserve it.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 15, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000