Highlights of the Week

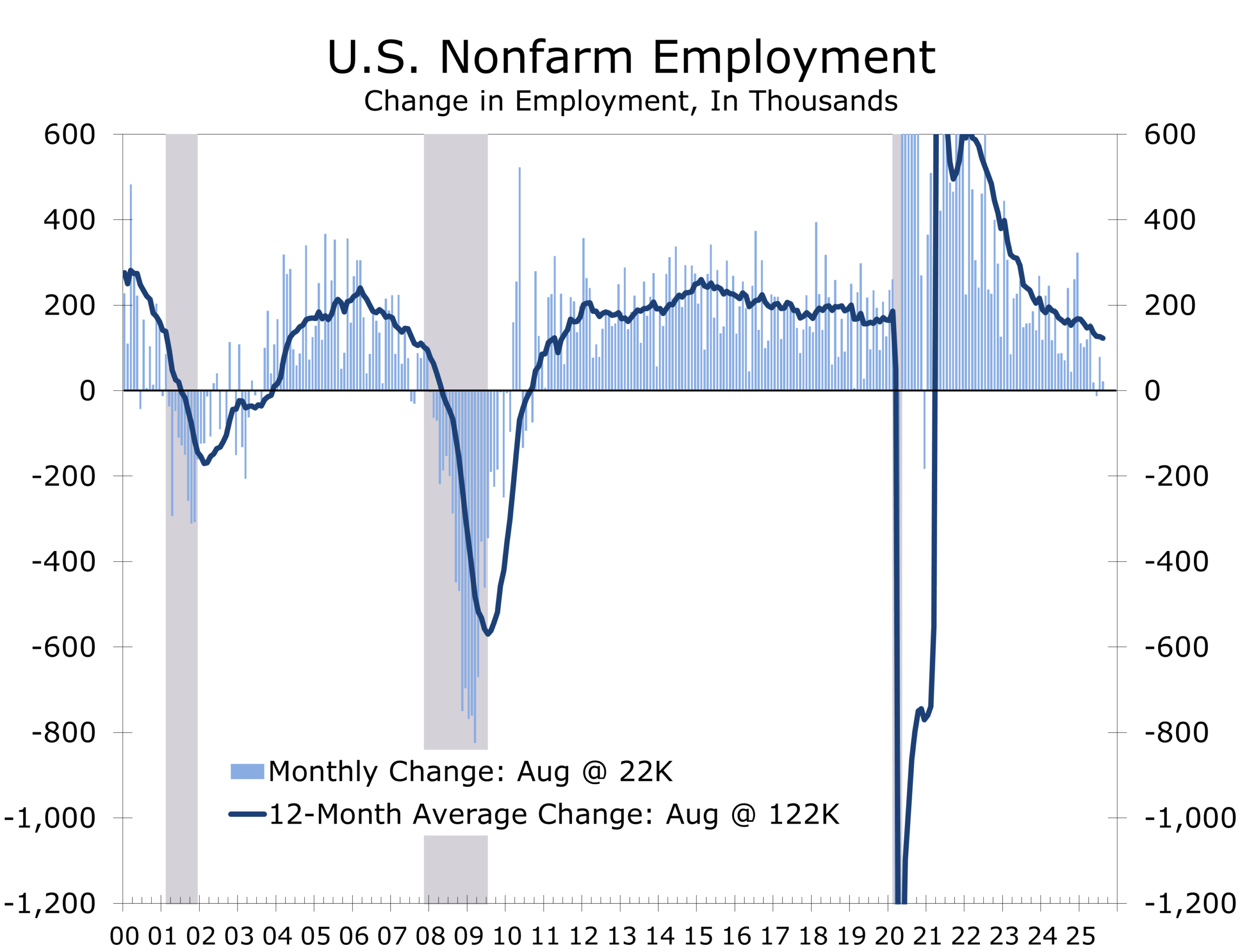

- August nonfarm payrolls rose just 22,000, with downward revisions pulling the three-month average to 29,000, well below the pace needed to stabilize unemployment.

- Unemployment rate climbs to 4.3%, its highest level since late 2021.

- Markets pivot sharply: Treasury yields plunged and mortgage rates fell nearly 30 bps as traders priced in three Fed rate cuts by year-end, starting September 17.

- Global long rates surge, reflecting concerns over sovereign debt and fiscal sustainability.

- Tariffs weigh on confidence, not prices: ISM surveys and the Beige Book report hiring freezes, delayed investment, and fragile demand with only modest inflation pass-through to end consumers.

- OPEC+ signals October production increases, putting downward pressure on oil prices despite supply disruptions elsewhere.

- Geopolitical flashpoints escalate: Russia intensifies strikes on Ukraine, Japan’s PM resigns, and U.S.–Korea relations are strained following an unusually large Hyundai-site immigration raid.

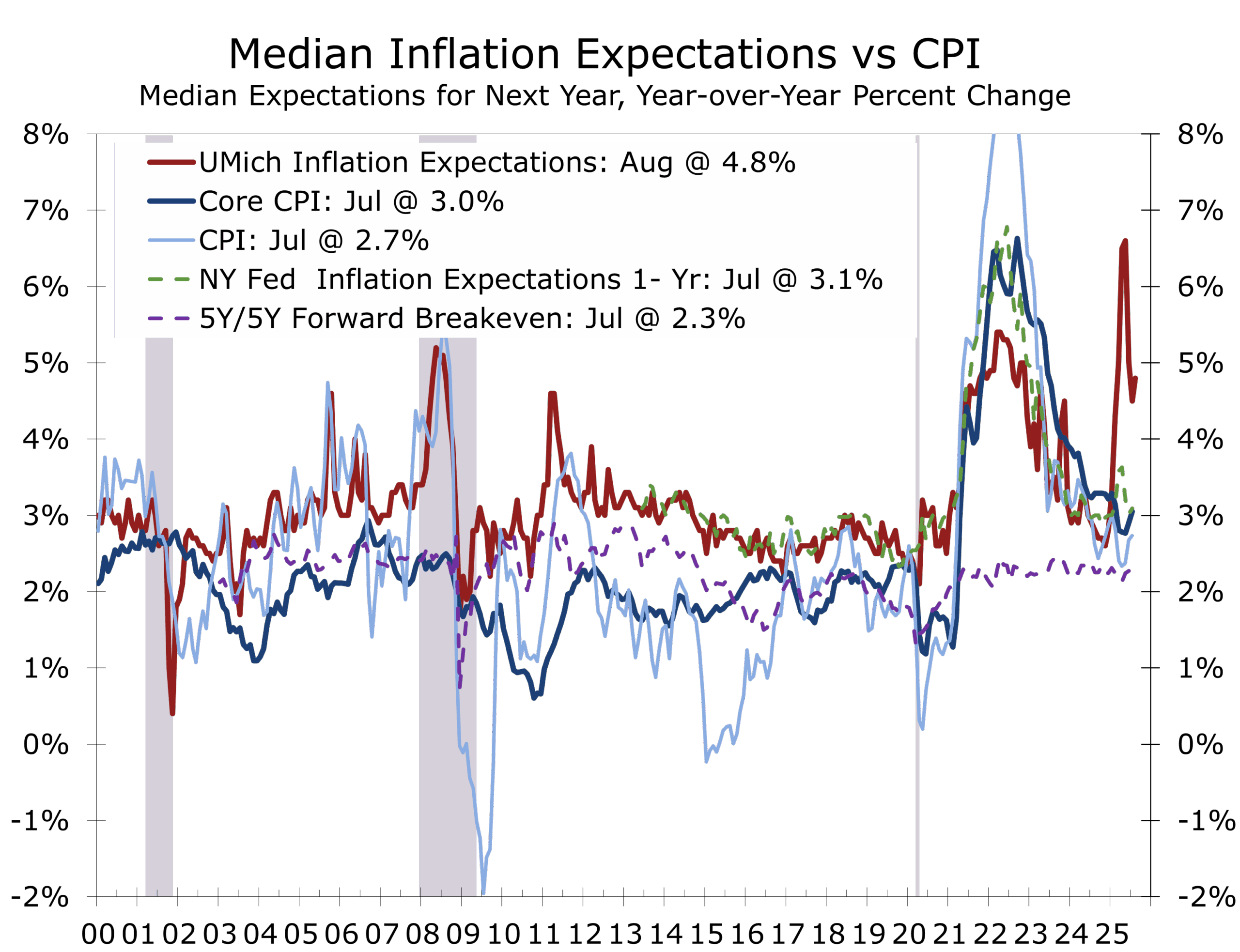

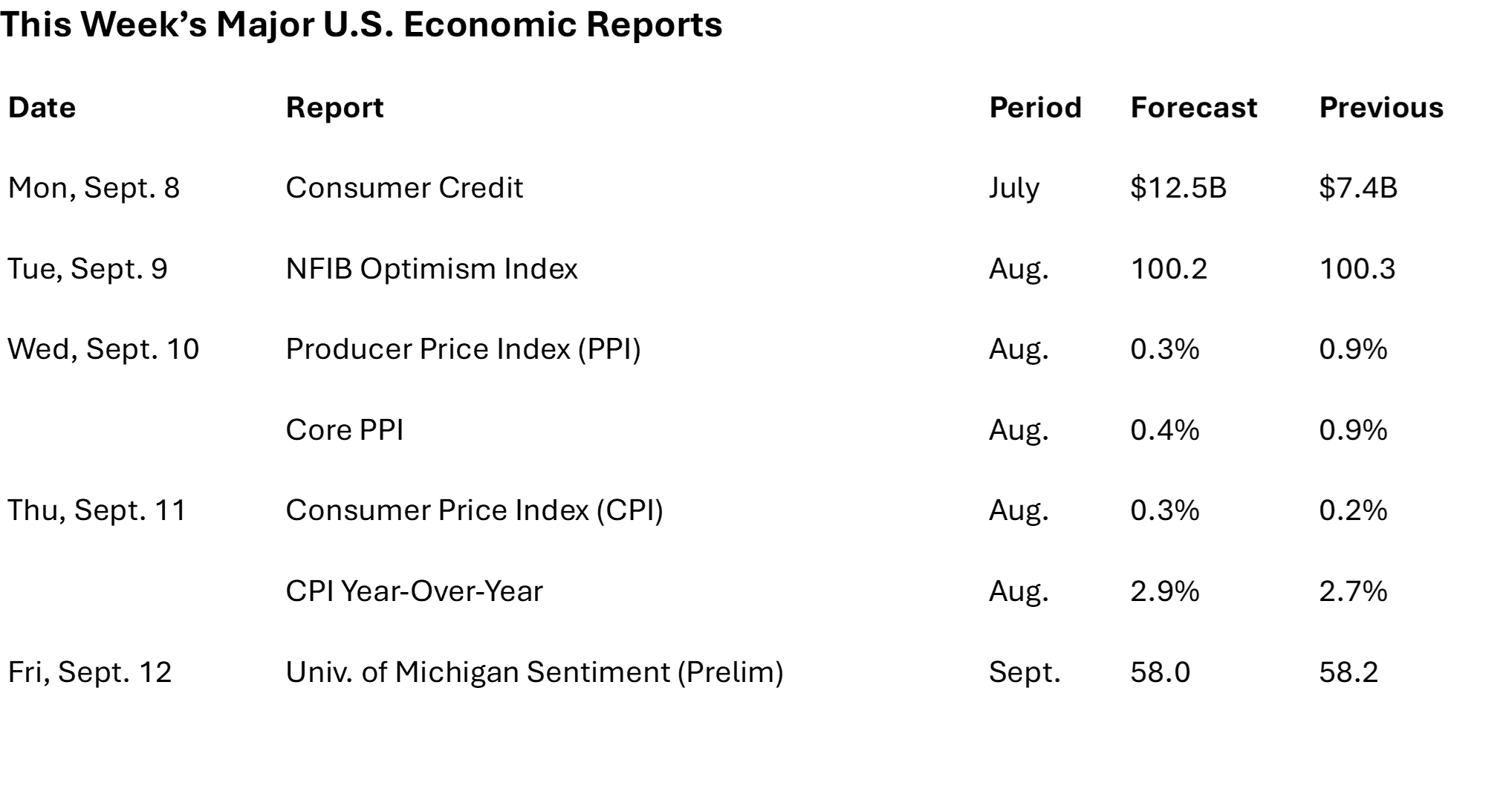

- Key week ahead: CPI (Thursday) will dominate, alongside PPI and NFIB Small Business Optimism data, as markets gauge whether muted inflation trends persist amid slowing growth.

The Fed Waited. Growth Didn’t.

For much of the summer, Federal Reserve officials maintained they had time to wait and see how tariffs would play out. The assumption was that higher trade barriers would eventually lift inflation, giving the Fed a reason to delay or moderate rate cuts.

The August jobs report upended that narrative. Instead of igniting inflation, tariffs have chilled hiring and business activity. Nonfarm payrolls rose by just 22,000 in August, while prior months were revised lower. Over the past three months, job growth has averaged only 29,000 per month—well below the roughly 50,000 needed to keep the unemployment rate steady.

Healthcare and social assistance provided nearly all the job gains. Manufacturing shed 12,000 jobs, including a 15,000 decline in transportation equipment tied to strikes. Temporary help, wholesale trade, and mining also contracted, the latter reflecting a pullback in energy exploration.

Inflation never surged as feared. Instead, tariffs brought hiring to a standstill

The unemployment rate climbed to 4.3%, its highest level since late 2021, while long-term unemployment jumped to 1.9 million, or 25.7% of overall unemployment—a share rarely seen outside recessions. Wage growth slowed to 3.7% year-over-year, and average hours worked were flat at 34.2.

We have long contended that the QCEW data, due out September 9, will show job growth has been significantly overstated—our base case is by around 45,000 jobs a month. Adjusted for this, true job growth since April—which has averaged just 41,000 jobs per month—may have been flat to negative.

The Fed is now staring at a labor market that has shifted from “balanced” to fragile, with stagnation overtaking overheating as the dominant risk.

Tariffs: Confidence Killer, Not Inflation Driver

Tariffs are now acting as a tax on business confidence, not a source of runaway inflation.

The ISM manufacturing index held at 47.2 in August, marking six consecutive months of contraction. Negative tariff commentary outnumbered positive anecdotes two to one, signaling weak sentiment.

The ISM services index rose to 52.0, but much of the improvement came from front-loading orders ahead of October tariff hikes—a temporary boost that is unlikely to last.

The Fed’s Beige Book echoed these findings, citing hiring freezes, delayed capital spending, and fragile consumer demand. NFIB surveys confirm small businesses face rising input costs but possess only limited pricing power, squeezing margins without generating significant inflation.

Tariffs have proven to be more of a tax on business confidence than consumers

Only 13% of consumer spending directly falls on tariffed goods. The broader drag comes from uncertainty, which slows hiring and investment across industries.

Housing and Construction: Diverging Paths

Construction spending fell 0.1% in July, marking the third consecutive monthly decline and leaving total outlays nearly 3% below year-ago levels.

- Private nonresidential spending weakened sharply, with declines in manufacturing, commercial, and even data center projects.

- Public infrastructure offered a modest offset but remains insufficient to stabilize the sector.

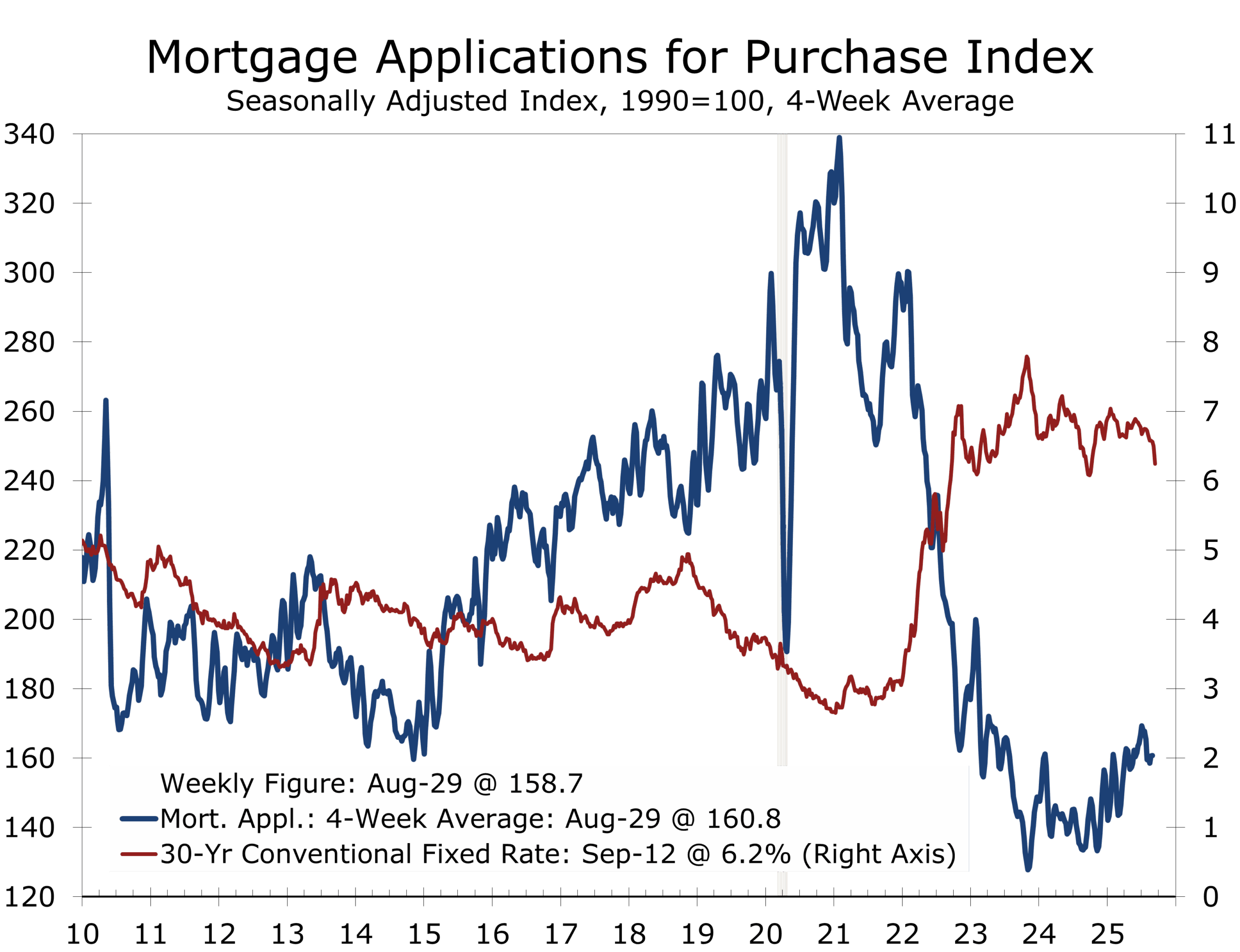

Mortgage rates’ sharpest weekly drop in a year could revive fall home buying

The surprise came from housing. Mortgage rates dropped nearly 30 bps after the jobs report, the steepest weekly decline in over a year. This sudden easing could stabilize homebuyer demand heading into the fall. If sustained, housing—one of the largest economic drivers—may become one of the first sectors to turn the corner even as broader conditions remain soft.

.

Markets: Diverging Yield Dynamics

Treasury yields fell sharply following the weak jobs report as traders priced in three Fed rate cuts by year-end, starting September 17. The two-year yield slid below 3.5%, while MBS spreads narrowed to their tightest since early 2022.

At the same time, global long-term yields surged, with 30-year bonds in the U.S., Europe, and Japan selling off even as front-end rates declined. This divergence reflects rising concerns over sovereign debt sustainability. Governments are ramping up defense and infrastructure spending while avoiding unpopular tax hikes or entitlement reforms. Markets increasingly sense a fiscal reckoning is inevitable—though not imminent—allowing the drop in short- and intermediate-term yields.

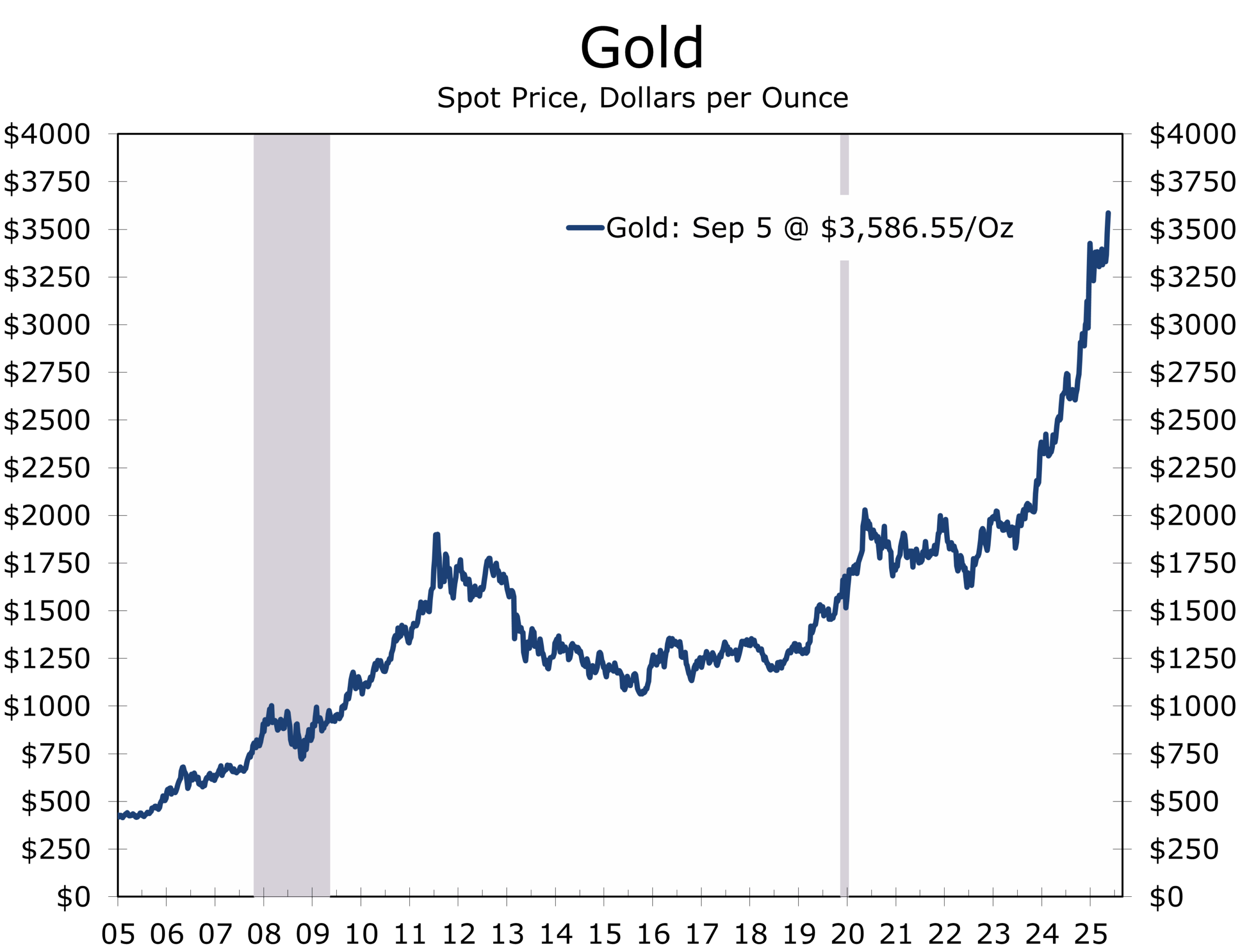

Adding to the crosscurrents, gold prices briefly soared above $3,600/oz, a record high. This reflects heightened demand for safe havens amid weakening labor data, geopolitical turbulence, and waning confidence in sovereign debt markets. Institutional investors are moving decisively into gold as confidence in long-term government papers erode.

Gold surges past $3,600 as sovereign debt fears mount

For now, corporate balance sheets remain strong, and credit spreads tight. But if growth slows further, elevated long-term yields could magnify financial instability—particularly in housing, commercial real estate, and maturing corporate debt.

Geopolitical Shifts Intensify

Global tensions escalated sharply last week, underscoring how geopolitical risk is now structurally embedded in markets.

The Beijing military parade attended by Xi Jinping, Vladimir Putin, and Kim Jong Un was a direct counterpoint to the Oval Office gathering of Western leaders following the Alaska summit. This symbolic alignment underscored the deepening rift between rival global blocs.

Russia and China’s intentions are clear: weaken Western resolve and fracture alliances. India’s presence highlighted its swing-state diplomacy, leveraging ambiguity to extract favorable trade and security terms. The key takeaway: China under Xi cannot be trusted, and would act toward Taiwan or other neighbors with the same aggression Russia has shown in Ukraine.

Xi, Putin, and Kim challenge Western unity while Russia escalates strikes

Russia launched its most intense wave of strikes on Ukraine in months, targeting energy infrastructure, ports, and logistics hubs. These attacks aim to exploit political transitions and fiscal constraints in the West, raising the costs of NATO’s continued support.

Western nations are responding by ramping up defense spending and tightening alliances. Europe, Japan, and non-aligned Asian nations are accelerating one-sided trade agreements with the U.S. to secure their positions.

Markets are reacting in real time. Gold’s rally is not merely a reflection of rate expectations but a barometer of systemic fear, signaling investors’ preparation for a world with greater instability and fewer safe havens.

Japan added to global instability with the sudden resignation of Prime Minister Shigeru Ishiba, sending the yen lower and JGB yields higher as markets anticipate looser policy under his successor.

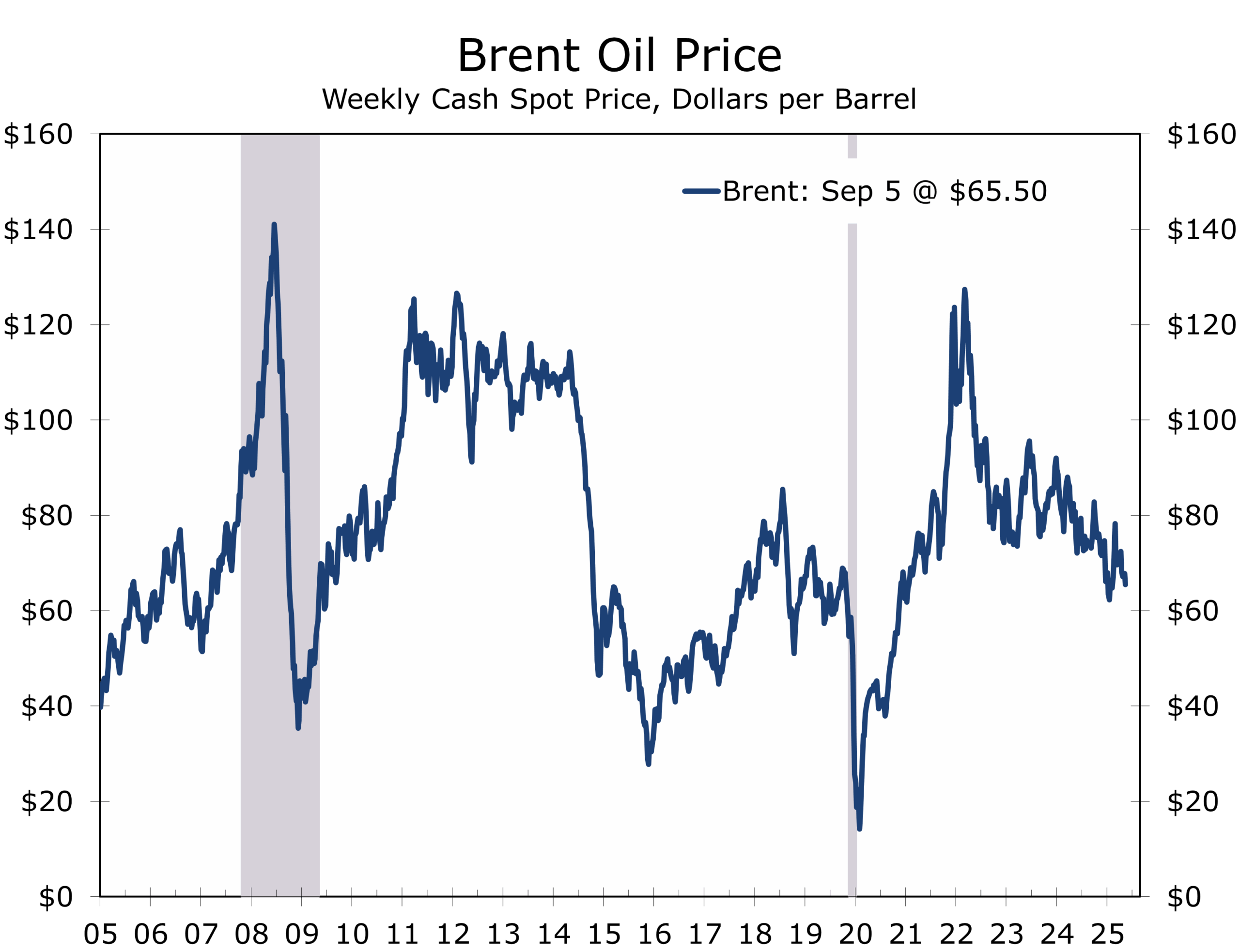

OPEC+ fueled further volatility by signaling a modest October production increase (+130k to +350k barrels/day). Brent crude slipped to $66/barrel, but risks remain tilted toward renewed price swings as geopolitical conflicts evolve.

Closer to home, U.S.–Korea relations were rattled by an immigration raid at Hyundai’s Georgia site, disrupting EV and battery facility construction. Korean officials expressed concern about regulatory clarity, especially as Korean firms remain among the largest foreign investors in the Southeast.

Looking Ahead

The coming week features a light but critical economic calendar, with Thursday’s CPI report in sharp focus. CPI is expected to rise 0.3% for both headline and core measures, with y/y headline at 2.9% and core steady at 3.1%.

A steady CPI reading would cement expectations for a September 17 Fed cut, while a hotter print could disrupt markets temporarily and shift expectations to a slower, every-other-meeting pace of cuts. The latter seems more plausible to us, as we feel price measures are likely to capture more of the impact of rising tariffs in coming months. The Fed may actually be able to accomplish more by doing less.

Bottom Line

The Fed waited for inflation to re-emerge before cutting rates. Instead, growth slowed, unemployment climbed, and tariffs chilled confidence without sparking significant price pressures.

The sharp drop in mortgage rates shows how quickly financial conditions can shift when markets anticipate Fed action. Housing may stabilize sooner than other sectors, but manufacturing and business investment remain fragile.

Globally, Russia’s escalation, Japan’s political vacuum, and OPEC+ decisions highlight a world where geopolitical risks are permanently embedded in markets. These forces are now visible in higher long-term yields, a stronger bid for safe havens, and persistent volatility in energy prices.

Clarity—not just action—is the Fed’s most valuable tool

Unless this week’s inflation data fundamentally alters the narrative, a September rate cut is virtually certain. The Fed’s greater challenge will be providing clarity to navigate a world of slowing growth, rising geopolitical risk, and fragile investor confidence.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 7, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000