Trade Winds Shift: Q2 Growth Prospects Surge on Import Collapse

Highlights of the Week

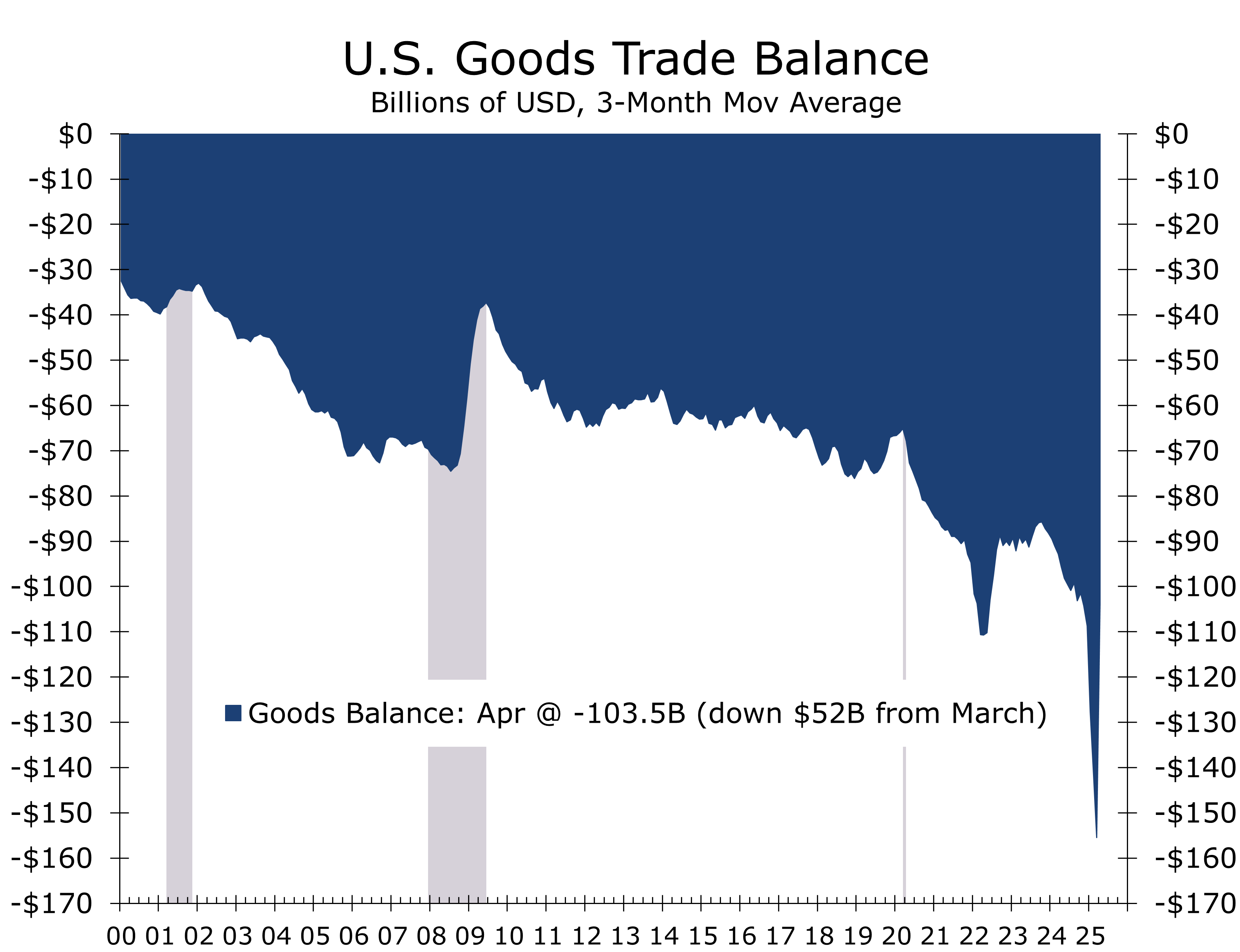

- The U.S. trade deficit was nearly halved in April as imports collapsed, turning net trade into a major tailwind for Q2 GDP. The Atlanta Fed’s GDPNow model surged in response.

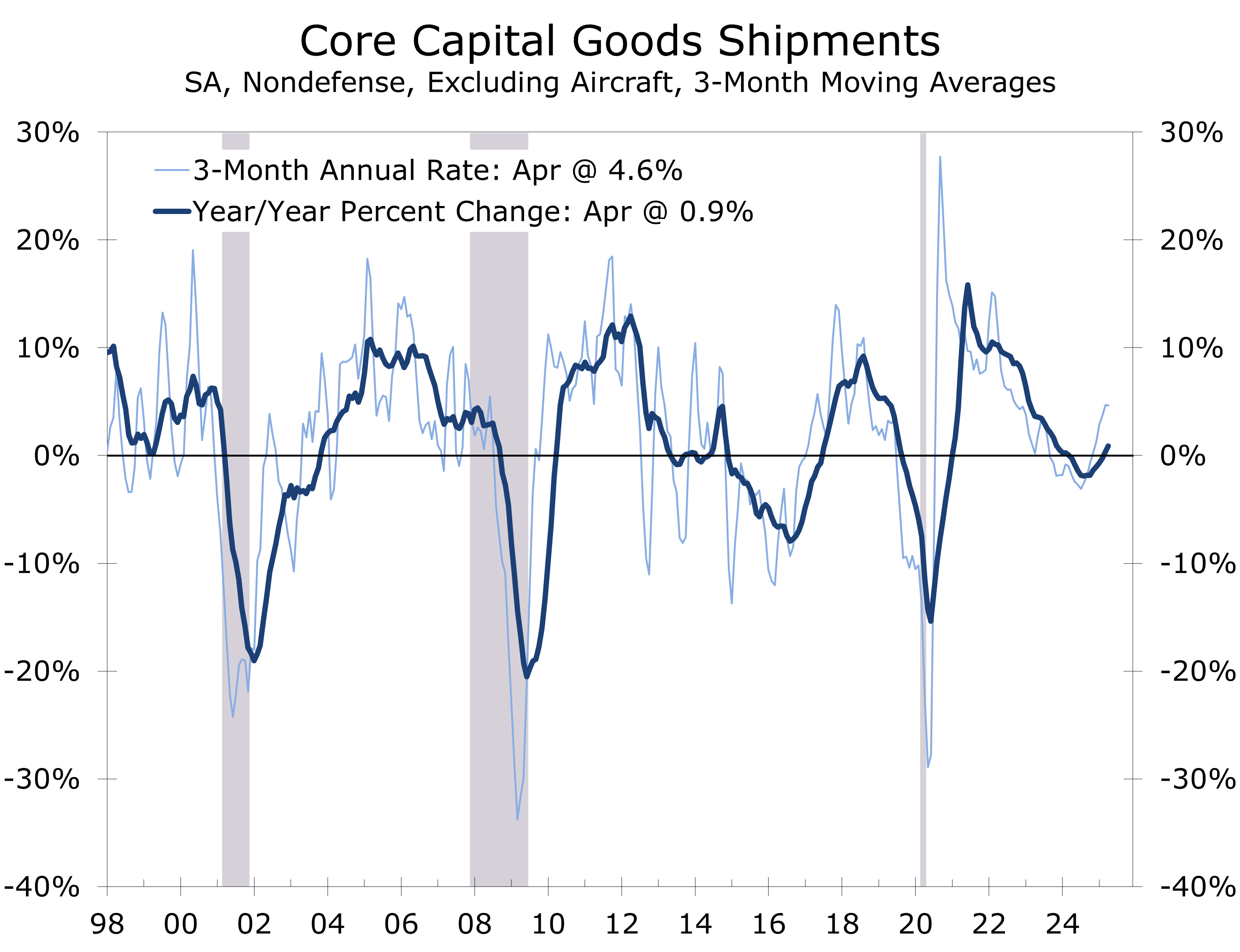

- Durable goods orders fell 6.3% in April due to a sharp drop in commercial aircraft bookings, while core orders and shipments showed modest resilience.

- Q1 GDP was revised slightly upward to a -0.2% contraction, but underlying private domestic demand was revised lower.

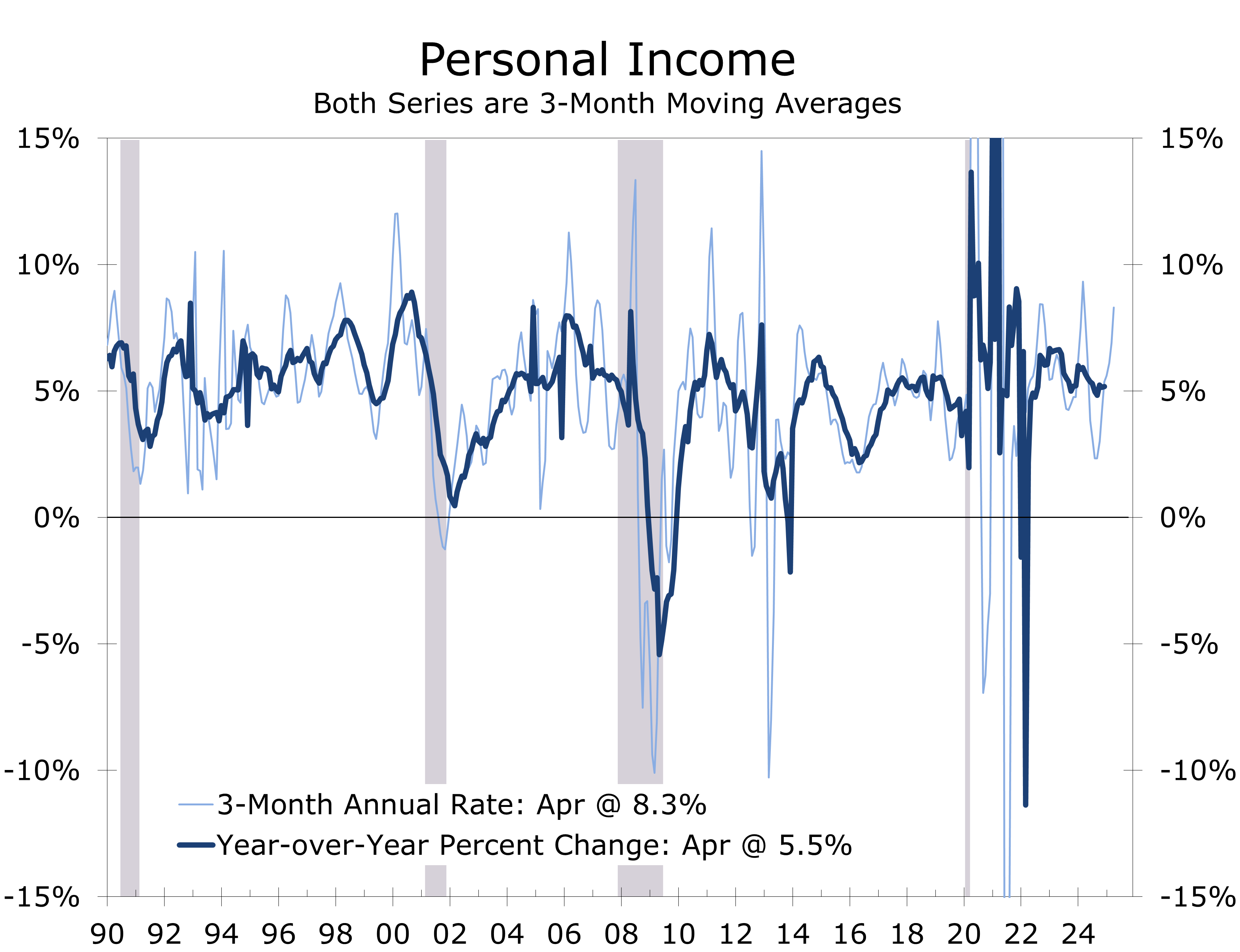

- Personal income jumped 0.8% in April, lifted by solid wage growth and retroactive Social Security payments; consumption rose a modest 0.2%.

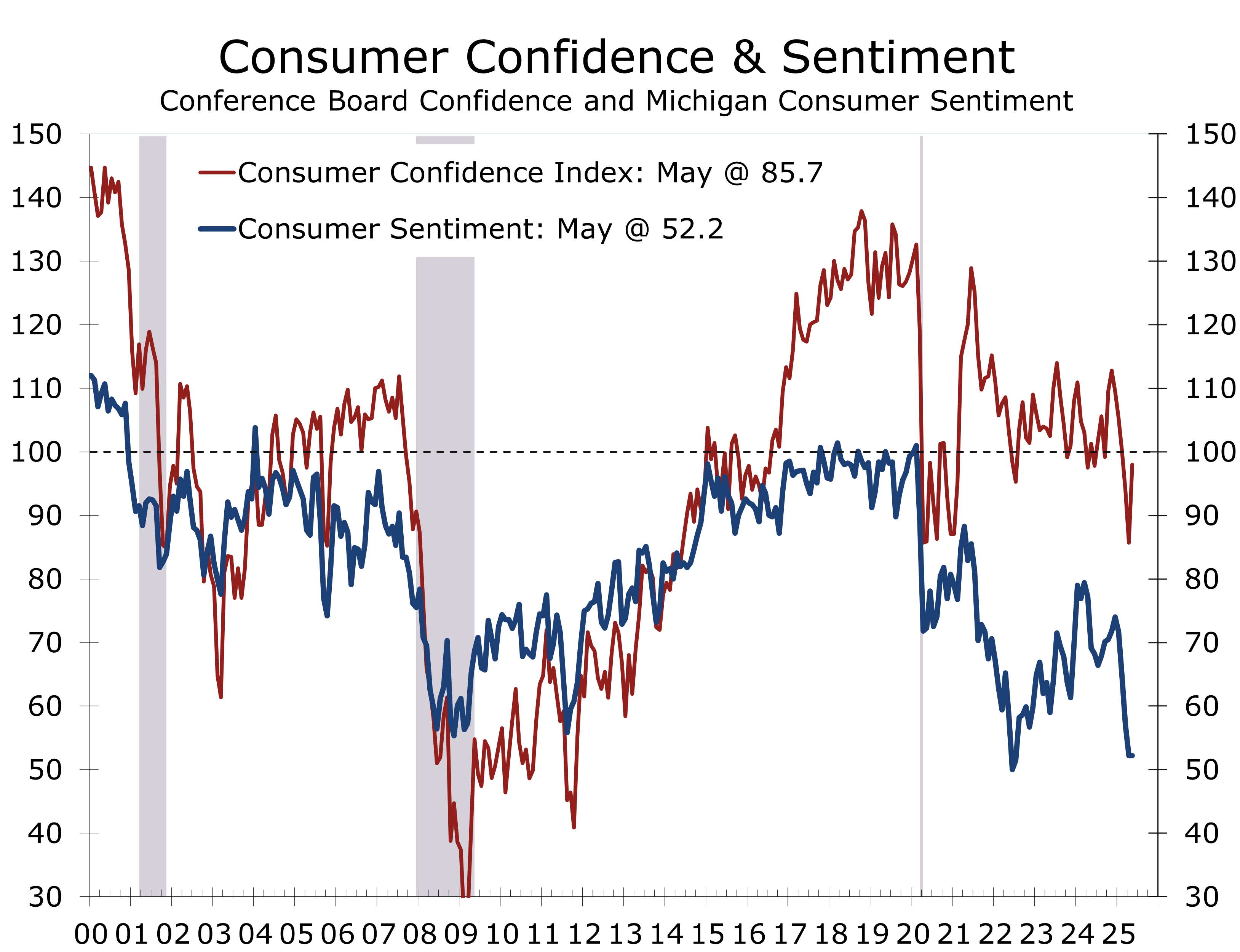

- Consumer confidence rebounded sharply in May, while consumer sentiment improved only modestly and remains historically low.

- Labor market signals continue to soften: the labor differential narrowed for a fifth month and continuing jobless claims hit their highest level since November 2021.

- Russia unleased another brutal attack on Ukraine and is threatening more decisive action, prompting Trump to issue a harsh denunciation of Putin.

- The Fed remains in wait-and-see mode amid sticky inflation and rising employment risks. The markets appear set for a December rate cut but we feel the Fed will move sooner.

Markets Digest Crosscurrents in Trade and Growth

Consumers, businesses and the financial markets continue to grapple with a multitude of macroeconomic and geopolitical crosscurrents. Tariffs and higher interest rates remain the top concern, but there is a growing realization that Trump’s tariffs are designed to bring about trade deals, promote national security and help reshore key parts of the manufacturing sector rather than to severely restrict trade. The extension of the timeline to reach a deal with the European Union is a prime example, as is the President’s post on Truth Social bemoaning China’s unwillingness to comply with the terms of the most recent trade truce. The talk rattled the markets late Friday, as Trump said he was readying new remedies.

The trade deficit appears to be swinging back from its first quarter plunge, boosting Q2 GDP.

New court rulings are adding complexity but not reversing the trade trajectory. On May 28, the U.S. Court of International Trade ruled that several of the administration’s “Liberation Day” tariffs imposed under the International Emergency Economic Powers Act (IEEPA) were invalid. The Trump Administration has already appealed the decision and was granted a temporary stay, allowing the tariffs to remain in effect for now. Legal experts expect the Supreme Court to ultimately hear the case and likely affirm most of the president’s authority under existing national security-based trade statutes. The tariffs most at risk are the reciprocal tariffs applied to U.S. allies, rather than those targeting strategic rivals such as China. Even if the appeals court upholds the lower court’s decision, the president retains other statutory pathways—such as Section 301 and broader national security provisions—to reimpose similar trade barriers. We expect trade negotiations to continue at their recent pace and look for some deals to be announced in coming weeks.

Earlier tariff announcements and efforts to stay ahead of anticipated trade barriers have disrupted recent economic data and are likely to continue doing so into the current quarter. The impact was particularly evident in the April durable goods report. Headline orders plunged 6.3%, largely reflecting a reversal in commercial aircraft bookings, which had surged in March. Commercial aircraft orders are expected to rebound in the coming months following President Trump’s visit to the Middle East and a blockbuster order from Qatar Airways. Excluding transportation equipment, durable goods orders rose 0.2%, indicating some underlying resilience. Orders for nondefense capital goods excluding aircraft—a key proxy for business fixed investment—declined 1.3%, and core shipments edged down 0.1%. These declines follow stronger results in March, as firms pulled forward activity ahead of tariff announcements.

Consumer confidence surged in May, reflecting relief from the partial but significant rollback of earlier tariff hikes on China and a better understanding of how trade policy is likely to evolve. The Conference Board’s Consumer Confidence Index rose 12.3 points to 98.0 in May. Consumers’ assessment of current economic conditions improved modestly, but the expectations component—which tends to influence actual consumer behavior more directly—posted a more substantial rebound. Sentiment was buoyed by equity market gains and a more optimistic outlook for income growth and stock prices. Inflation expectations eased for the first time since late 2024, but labor market perceptions softened slightly, with the labor market differential edging lower. While fears of a recession have subsided, they remain elevated, and policy volatility will likely keep confidence readings choppy in the months ahead.

With tariffs top of mind, businesses have slowed hiring, making it difficult to land a new job.

The Conference Board’s labor market differential —the difference between the share of consumers stating jobs are plentiful versus those saying jobs are hard to get—narrowed in May, falling 0.6 points to 13.2. This marks the fifth consecutive monthly decline and likely signals a further slowdown in hiring. Businesses have become more cautious amid volatility in policy announcements and market swings, contributing to reduced job postings.

While hiring has clearly slowed, layoffs do not appear to have materially increased. Weekly unemployment claims continue to show that initial claims remain historically low, but continuing claims have been trending higher. As of late May, continuing claims reached 1.91 million—the highest level since November 2021—suggesting that job seekers are having a harder time finding new employment. This trend suggests growing friction in labor re-entry, possibly reflecting mismatches in skill sets or simply a reduced hiring appetite in rate-sensitive sectors. Unemployment claims have risen a bit more in the greater Washington D.C. area, reflecting substantial public sector job cuts.

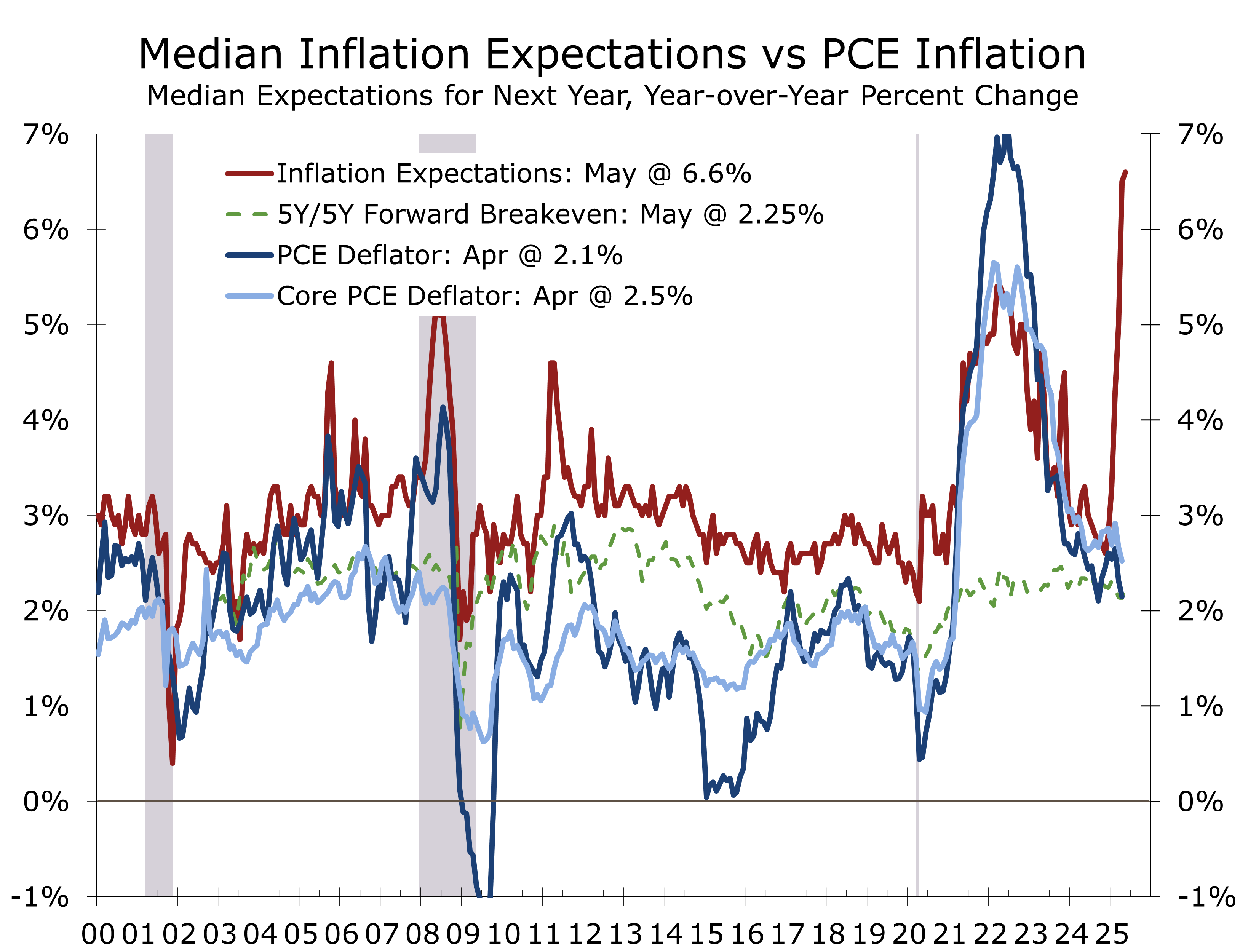

The Conference Board’s results were more pronounced than those released by the University of Michigan on Friday. Consumer Sentiment was revised up only slightly to 52.2 from its early-month preliminary reading. While the revision ended a four-month streak of declines, sentiment remains historically low, and Consumer Sentiment is much further below its historic norms than Consumer Confidence is. The details of the report were more positive, however. Year-ahead inflation expectations were revised down to 6.6%, and long-run expectations fell to 4.2%—the first drop since December 2024. Consumers were more optimistic about future personal finances and buying conditions for big-ticket items, which suggest consumer spending should remain resilient.

Personal income growth has been stellar so far this year, supporting consumer spending.

Personal income rose 0.8% in April, beating expectations and reflecting strength across wages and salaries and a significant boost from government transfers, particularly retroactive Social Security payments under the Social Security Fairness Act. Upward revisions to prior months’ data lifted the year-to-date trajectory: on a three-month moving average basis (3MMA), personal income is up 5.5% from last year, while wages and salaries are up 4.2%. Real disposable (after-tax) income rose 0.7% in April alone and is up 1.7% year-to-year, on a 3MMA basis.

Personal consumption rose a modest 0.2% in April, with all of the increase coming from services. Spending on goods fell slightly, driven by declines in durable categories like motor vehicles and recreational equipment, reflecting a partial reversal of March’s front-loading ahead of potential tariffs. Spending on services, particularly restaurant dining, rose solidly during the month. Consumer spending is up a solid 5.5% year-to-year. Given easing inflation expectations and the rebound in equity markets, we suspect spending regained some momentum in May.

The U.S. goods deficit was nearly halved in April, plunging from $162.3 billion to $87.6 billion, as imports dropped by $68.4 billion—the steepest monthly decline in recent memory. The reversal reflects the unwinding of front-loaded purchases in Q1, collapsing arbitrage in gold flows, and a near standstill in Chinese imports following tariff hikes that temporarily pushed duties above 100%. The sharp import retrenchment—especially in pharmaceuticals, gold, and consumer goods—flipped net trade from a major Q1 drag to a sizable Q2 tailwind. The Atlanta Fed’s GDPNow tracker surged in response, suggesting trade alone may add more than two percentage points to Q2 GDP.

Although net exports are now boosting headline growth, the gains are unlikely to persist into the second half of the year. While some duties have been reduced, uncertainty surrounding future trade deals, retaliatory measures, and procedural constraints continues to cloud the outlook. For now, collapsing imports are alleviating recession fears prompted by the historic widening in the trade gap during the first quarter.

Both the overall and core PCE Deflator—the Fed’s preferred inflation measure—rose 0.1% in April. Inflation is still running well below consumer expectations, which have been hyped by tariff fears.

The May FOMC minutes reiterated that policymakers remain in wait-and-see mode. Although inflation has softened at the margin, the Fed is keenly aware that tariff-induced price pressures may re-emerge. Meanwhile, signs of a softer labor market and a strong dollar are providing room to hold policy steady.

The Fed continues to place a great deal of emphasis on the role inflation expectations play in containing inflation. The recent spike in inflation expectations in the consumer confidence surveys has gotten the Fed’s attention, although more reliable measures, such as the 5-year forward breakeven inflation rate and the New York Fed’s consumer survey, do not suggest expectations have deteriorated nearly as much.

The markets appear set that the Fed will remain on hold until December. We suspect the Fed is leaning toward an earlier rate cut, possibly late this summer but certainly sometime this fall. We feel labor market conditions are weaker than the nonfarm data have indicated and eventually that reality will be reflected in the data.

Treasury yields have been unusually volatile. Supply concerns and fiscal uncertainty continue to exert upward pressure on term premiums. The 30-year Treasury briefly rose above 5%, while the 10-Year Note rose above 4.50%, in the aftermath of the Moody’s downgrade and House Reconciliation Bill, which front loads stimulus and pushing budget savings in the out years. Yields peaked following last week’s disappointing 20-Year Treasury auction but have been trending lower ever since. Auctions have also been well bid, including a stellar 7-year Treasury auction this week. Investors appear to be positioning for growth to slow later this year, which aligns with our forecast.

China remains Russia’s economic lifeline but is playing hardball on energy and tech. For Moscow, a ceasefire could lock in territorial gains and stabilize the economy. For Trump, brokering one offers foreign policy clout, a potential market tailwind, and a way to lower NATO tensions.

The war has cost Russia $1.3 trillion, over 100,000 lives, and lasting economic damage. Quiet talks suggest Ukraine’s NATO bid is off the table, and neutrality is assumed. But some affiliation with Western Europe also seems inevitable. We had earlier pondered whether Ukraine could attain some sort of observer status within NATO, allowing for cross training with NATO members but no NATO bases on Ukrainian soil. That prospect seems more remote today. Even a formal peace remains distant, but a tactical ceasefire is increasingly likely.

Europe Pushes Back on Populism

Despite forecasts of a hard-right surge, Europe’s center held. Romania elected pro-European Nicușor Dan over nationalist George Simion. Portugal’s center-right outpaced the far right Chega party in parliamentary elections, which gained seats but not much clout. And Poland’s liberal candidate secured a run-off spot against his nationalist rival.

Looking Ahead: June 2-6, 2025

The May employment report will headline another busy week of economic reports. We are projecting a middle-of-the-road 145,000-job gain but are also looking for an 0.1 point uptick in the unemployment rate. The labor data can be unusually volatile in May due to the timing of school year end. With hiring slowing, the seasonals could overcompensate, yielding a much weaker number than expected.

- Monday: ISM Manufacturing Index (May) – is expected to remain in expansionary territory and may surprise to the upside due to lengthening delivery times.

- Tuesday: Factory Orders (April) – look for a decline following weak headline durable goods report.

- Wednesday: ISM Services Index (May) – expected to show modest growth; employment and price indexes in focus.

- Thursday: Jobless Claims – overall claims remain low but continuing claims have been rising and are currently at multi-year highs.

- Friday: Nonfarm Payrolls (May) – we are projecting a 145,000-job rise in nonfarm payrolls; unemployment rate is expected to inch higher to 4.3%.

Market participants will also monitor revisions to productivity and labor costs, plus any policy commentary from Fed speakers. The Fed’s Beige Book will also be released on Wednesday and will be closely reviewed for any fallout from tariffs and changes in consumer behavior.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

May 23, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000