Highlights of the Week

- The Fed executed a perfectly timed A‑Team maneuver — ensuring the CPI report dropped ahead of the October FOMC — giving policymakers just enough cover to cut rates while long‑term yields stayed anchored near 4%.

- Growth continues, but the margin for error is narrow: Flash PMIs point to steady expansion, with much of the economy’s strength concentrated in asset appreciation, AI infrastructure, aerospace, and affluent‑driven services.

- The expansion is bifurcated: higher‑income households continue to spend as asset prices surge; middle‑ and lower‑income families face higher living costs, slowing job growth, and eroding affordability.

- Lower rates are stabilizing housing: existing‑home sales have firmed just over 4.0M units, inventories are rising, and price growth is cooling — a sign of renewed activity without reigniting shelter inflation.

- Markets are firmer today on headlines that Washington and Beijing have a framework to pause the threatened 100% tariffs and rare‑earths export curbs — relief is real, durability TBD.

- Trump’s Southeast Asia swing has raised hopes of a near‑term tariff truce — but the geopolitical road remains headline‑sensitive and volatile.

- With Powell’s plan working, the October cut remains the base case — but Mr. T’s driving leaves everyone wary of unexpected twists and turns.

The Setup — CPI Gets the Spotlight

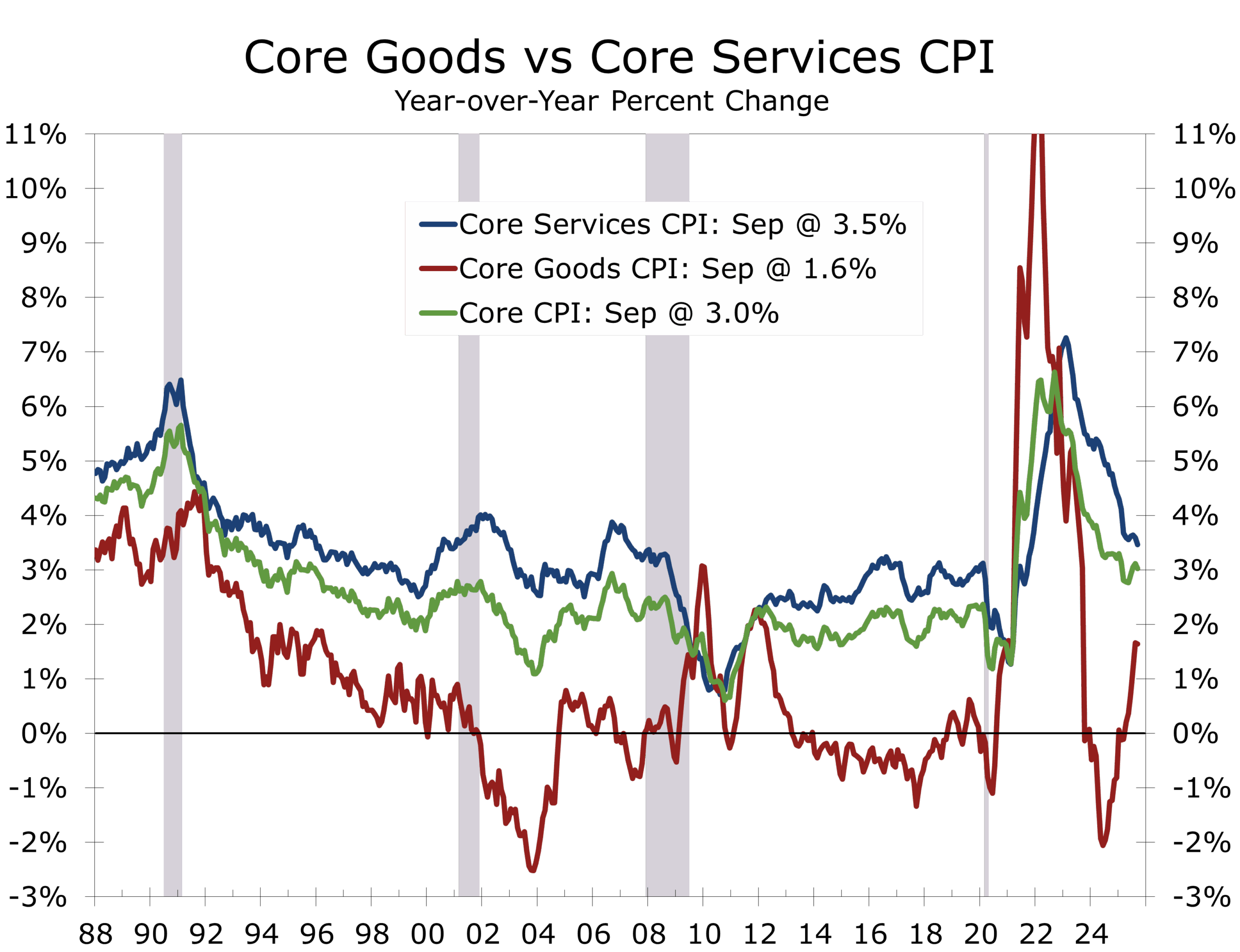

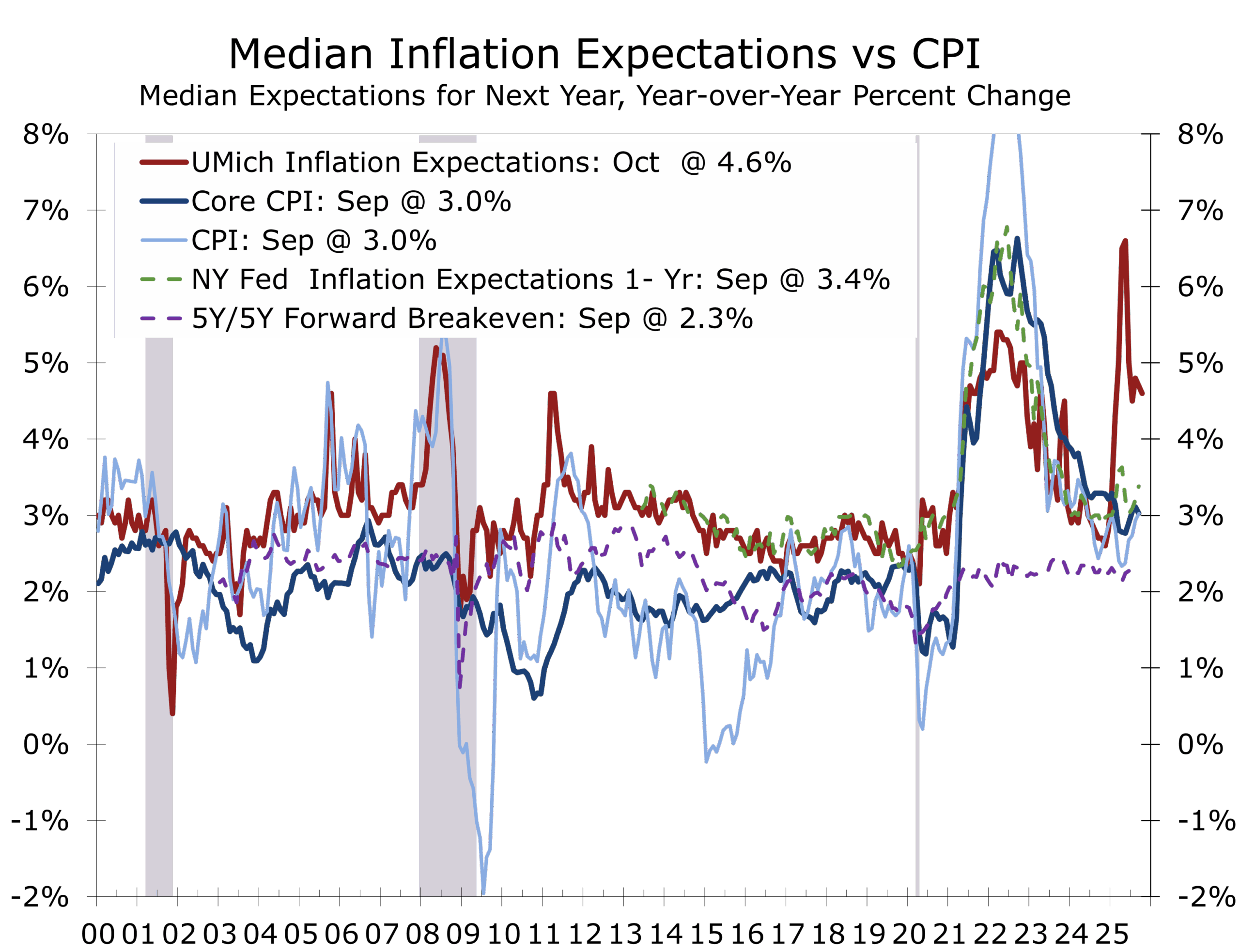

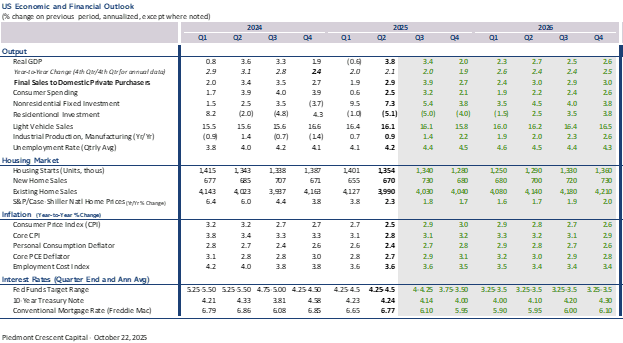

September CPI came in cooler than expected, reinforcing disinflationary pressures and giving the Fed just enough visibility to continue easing without losing credibility. Headline CPI rose 0.3% m/m (3.0% y/y), down from 0.4% in August, while core printed softer at 0.2% m/m (3.0% y/y). Core goods inflation held at 1.5% y/y, and core services eased to 3.5% from 3.6% — confirming that tariffs (not demand) remain the primary inflation driver.

Inflation may be lagging, but leading indicators continue pointing lower. Private sector price gauges and survey data have clearly rolled over. Supplier delivery times remain stable, eliminating fears of a 2021-style relapse. The weaker labor market also suggests core services prices will moderate further.

The softer CPI report allows continued measured easing, while keeping long rates anchored.

The Mission — Gradual Easing to Support the Labor Market

The Fed’s mission has evolved: it now seeks to maintain disinflation progress while carefully cushioning a weakening labor market. With underlying inflation easing and signs of job market fragility emerging, policymakers have started cutting rates to prevent a downturn from spiraling into weaker consumer spending.

The ongoing federal shutdown amplifies these risks by clouding economic visibility, so the Fed must proceed with caution—not only to support jobs and growth, but also to maintain the confidence of bond markets and avoid fueling renewed volatility.

Recent layoff announcements underscore the stakes:

- Tech giants continue trimming staff tied to non-AI business units.

- Several major retailers have announced headquarters and distribution-center cutbacks, perhaps counting on a productivity boost from new technology investments.

- Transportation and logistics firms are consolidating as goods demand cools.

These cuts remain measured — but confidence-sensitive. A small slip could cascade.

The ongoing federal government shutdown adds another layer of risk. With paychecks now likely delayed, millions of workers — including contractors with minimal savings buffers — will be forced to pull back on spending. That drag will widen if the shutdown lingers into the holiday season.

.

S&P Global’s October Flash PMIs confirmed a pickup in business activity, with the Composite Output Index rising to 54.8 from 53.9—the highest since July and signaling the strongest pace of growth in several months. Services led the expansion with a reading of 55.2, while manufacturing improved to 52.2 but continued to lag, hampered by weak exports and rising inventories.

The data also highlight modest overall job gains, with services adding positions and manufacturing still shedding jobs, as firms express caution over policy and tariff risks. Business confidence remains subdued, but lower interest rates and resilient domestic demand are supporting continued solid, if uneven, momentum into Q4.

The Fed is easing just enough to keep the van rolling, but everyone can feel the suspension tightening as the road gets bumpier and risks multiply from layoffs and the federal government shutdown. The soft patch helps the Fed, by further anchoring long-term rates. Just like the A-Team, businesses are improvising under pressure, patching together solutions and aiming to stay ahead of each new obstacle that pops up.

The Two‑Tier Economy — A Bifurcated Expansion

From inside the van, the ride feels smooth. Outside, road conditions vary considerably depending on which lane you are in.

Upper‑income households benefit from record‑high asset values and healthy discretionary spending. Wealth effects keep upscale services buoyant, especially in leisure, travel, and experiential activities.

Asset owners are celebrating the ride. Wage earners are gripping the armrests.

Middle‑ and lower‑income households remain under strain — slowing job gains, persistent price pressures, and housing affordability hurdles. Consumer sentiment remains fragile.

This bifurcation supports growth and disinflation — but it’s a knife‑edge. If the bottom weakens further, the mission shifts from landing the van to rescuing it.

Trade & Geopolitics — The Road Gets Bumpy

Risk tone brightened as Washington and Beijing reached a provisional framework pausing threatened 100% tariffs and rare-earths export curbs—pending Trump–Xi leader sign-off later this week. President Trump said he expects to “come away with a deal,” with China delaying export bans and boosting U.S. soybean purchases—tactically easing AI supply-chain stress and trimming term-premium risk.

Trump’s multi-stop ASEAN tour, with Treasury Secretary Bessent and Secretary of State Rubio, is choreographed to lock the arrangement before the Trump–Xi summit. Markets rightly view this as a truce, not a treaty. Export controls remain active tools, holstered rather than removed.

Canada felt the other end of the stick: Trump announced a fresh 10% tariff on Canadian goods in retaliation for an Ontario advertisement he believed misrepresented Ronald Reagan’s views on tariffs, particularly as the speech was given while he himself was implementing tariffs. He labeled the ad a “hostile act,” abruptly ending ongoing trade talks and injecting fresh tension into North American supply chains. Ottawa’s response remains measured for now—as it quietly deepens ties with Asia.

Argentina delivered a political jolt with Liberty Advances, President Javier Milei’s party, securing 41% of the vote in midterm elections—an endorsement of his free-market reforms and fiscal consolidation efforts. The U.S. has reportedly offered expanded financial backstops if Milei’s reforms remain on track—complementing the newly announced $20B swap line and increased U.S. beef import target. Market takeaway: reform momentum is real, and external liquidity risks are easing. This is a positive for Argentina, Latin America as a whole and the U.S. Beef imports may provide some modest price relief.

Geopolitically, the road may have straightened—but potholes remain in plain sight. And as markets have learned repeatedly this year, I pity the fool who gets on the wrong side of Mr. T.

Financial Markets & Rates — Keep the Roof Panels Secure – Markets continue to trade the Fed’s script: controlled disinflation paired with gradual easing favors long duration and curve steepeners. Equities rallied on the CPI release because a clean glide path reduces valuation risk.

Shutdown dynamics add a twist: delayed paychecks risk a sharper pullback in discretionary spending, which would increase expectations for further cuts — a development likely to reinforce the downward bias in long-term yields.

Industrial commodities remain subdued as global PMIs point toward slower momentum ahead. The S&P Global US composite PMI rose to 54.8 from 53.9, supported more by services than manufacturing. Output and new orders improved, while employment was mixed, rising in services and falling in manufacturing. Base metals and energy will likely underperform in this environment.

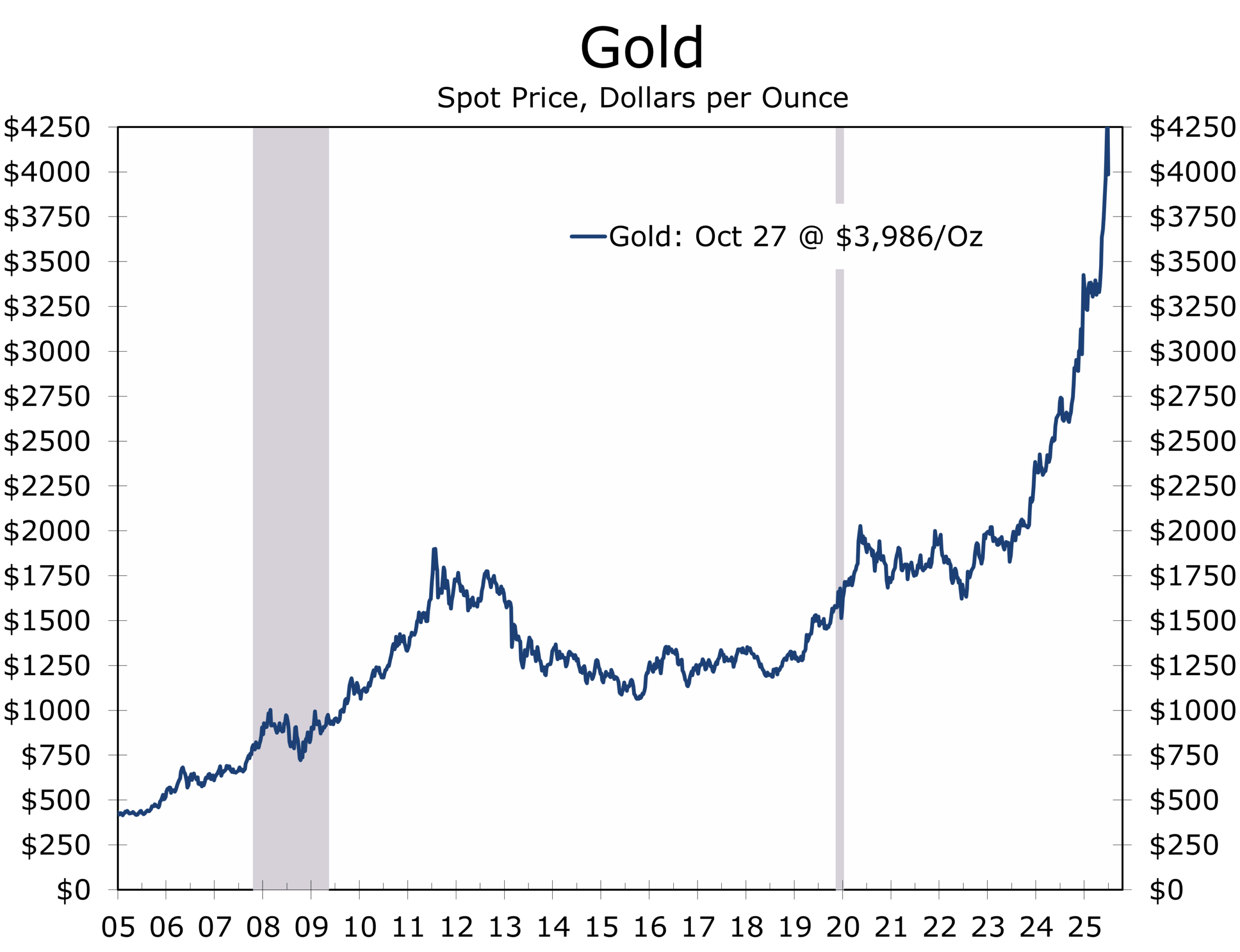

Gold’s recent correction appears to be more technical, rather than thesis changing. The world economy and global monetary framework are rapidly evolving. Central bank buying remains relentless — a secular force supporting the metal as insurance against fiat instability and geopolitical recoil.

As long as Powell keeps the A-Team on message — and Mr. T refrains from yanking the wheel — the van should stay on the road and the term premium contained.

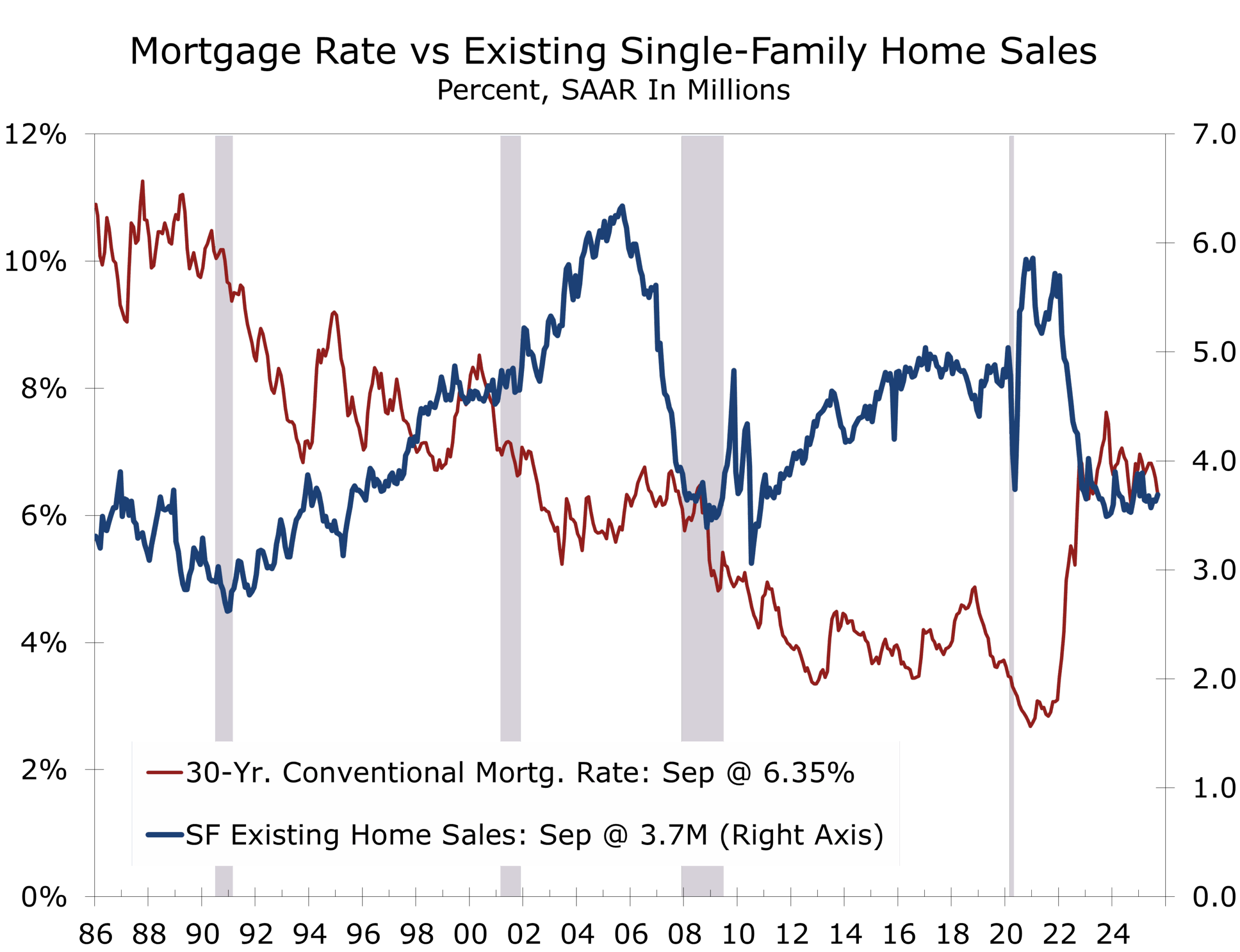

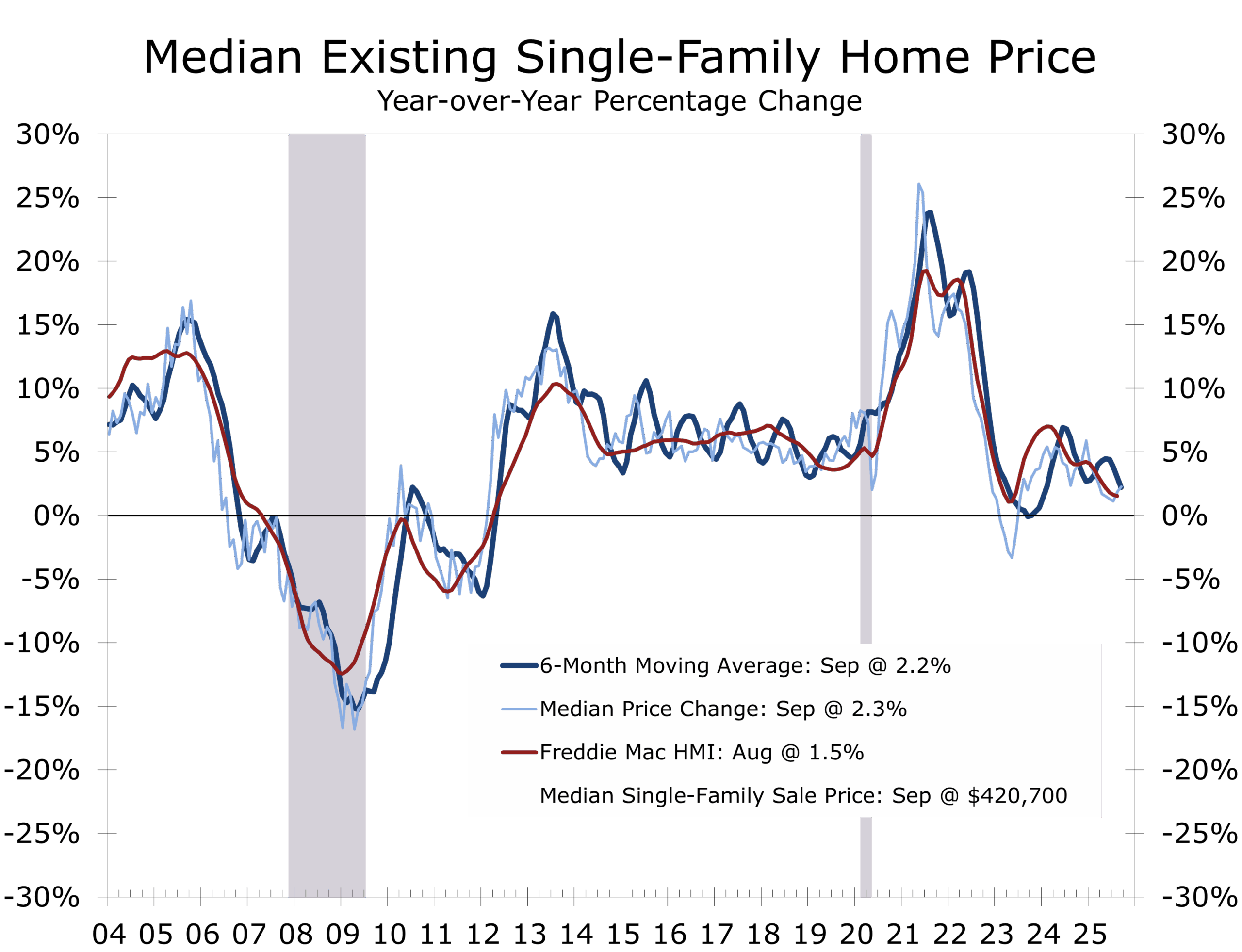

Housing & Business Signals — Checkpoints Along the Route – Housing is stabilizing — with lower mortgage rates coaxing more listings and buyers back into the market. Unlike the federal government, Realtors are still working. The National Association of Realtors reported last week that existing home sales ticked up to 4.06 million units in September (seasonally adjusted annual rate), marking the strongest pace in several months. Inventories continue to rise, with supply is up to 4.6 months, while median prices are increasing only in the low single digits (+2.1% y/y at $415,200).

From a structural viewpoint, this is significant. More listings improve choices for buyers, while moderate price growth reduces affordability pressure — but the market is still far from overheating. The inventory uptick plus stable sales pace suggests a rebalancing rather than a rebound. Lower mortgage rates and improving affordability are clearly lifting activity, yet first-time buyer share remains constrained, and many homeowners remain locked into their current homes, which have sub-4% mortgages.

Builders, brokers, and remodelers may finally get a smoother stretch of road, thanks to the pickup in listings and turnover rather than the chaotic spike-and-crash of the past couple of years.

The moderation in housing price appreciation pairs well with the disinflation trend elsewhere — reducing shelter’s risk to the CPI.

Because the market is not overheating, the Federal Reserve has room to cut short-term rates without triggering a new wave of housing-fueled inflation.

In short: housing is shifting into a steady-state recovery, rather than a boom. Upper-income homeowners continue to benefit from equity gains, while first-time and middle-income buyers are finding incremental relief on affordability metrics — neither boom nor bust, but a slow ascent.

Landing the Van — The Fed’s Escape Route

One more cut in December remains realistic — but is still conditional.

Key risks remain: Tariffs could return, leading to a jolt in term premium and sending yields higher. Housing could ramp back up and boost shelter inflation, halting the disinflation trend. Geopolitics could flare up, leading to supply chain disruptions and energy spikes.

Our base case: Growth moderates toward 2.0%, headline inflation holds firm at around 3% through year end but softens a touch on an underlying basis, implying moderating top-line inflation in 2026. Long yields hover around 4% but rise modestly as the economic picture improves next year.

If Powell keeps the A‑Team on script, the plan will come together nicely. If Mr. T stomps on the accelerator and yanks the wheel in a different direction, the outcome could become less certain.

The Week Ahead

We will miss a number of high-impact economic data releases this week due to the government shutdown, including critical reports on durable goods, trade, Q3 GDP, and PCE inflation. Despite the uncertainty, consensus and private forecasts anticipate:

- Consumer confidence, home prices, and private sector estimates of first time unemployment claims will all likely draw more scrutiny amidst mixed signals from labor market data and recent PMI gains.

- We look for another 25bp cut in the federal funds rate target at the October FOMC, with a third cut in December still expected barring surprises. We will also look for more insight into when the Fed will end quantitative tightening.

- Q3 GDP growth tracking near 3.4% annualized, propelled by resilient personal consumption, AI-driven capital spending but tempered somewhat by weak residential investment and export.

- Earnings: Checking in on the Mag-7 — Microsoft, Apple, Alphabet, Amazon and Meta and all report earnings this week. The markets will not only focus on earnings and revenue trends but also capital spending and other clues about the buildout of AI.

Time to bring out a cigar?

The plan has come together — for now. CPI delivered on cue, markets bought the story, and the van moved forward. Colonel John ‘Hannibal’ Smith can bring out the cigar, but it would be wise not to light it just yet. With Mr. T driving, no one is relaxing. Stability is a moving target — and the Fed knows one wrong turn can rewrite the story.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

October 27, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000