Highlights of the Week

- The Government shutdown appears likely to end as a bipartisan Senate vote approaches; market uncertainty may ease.

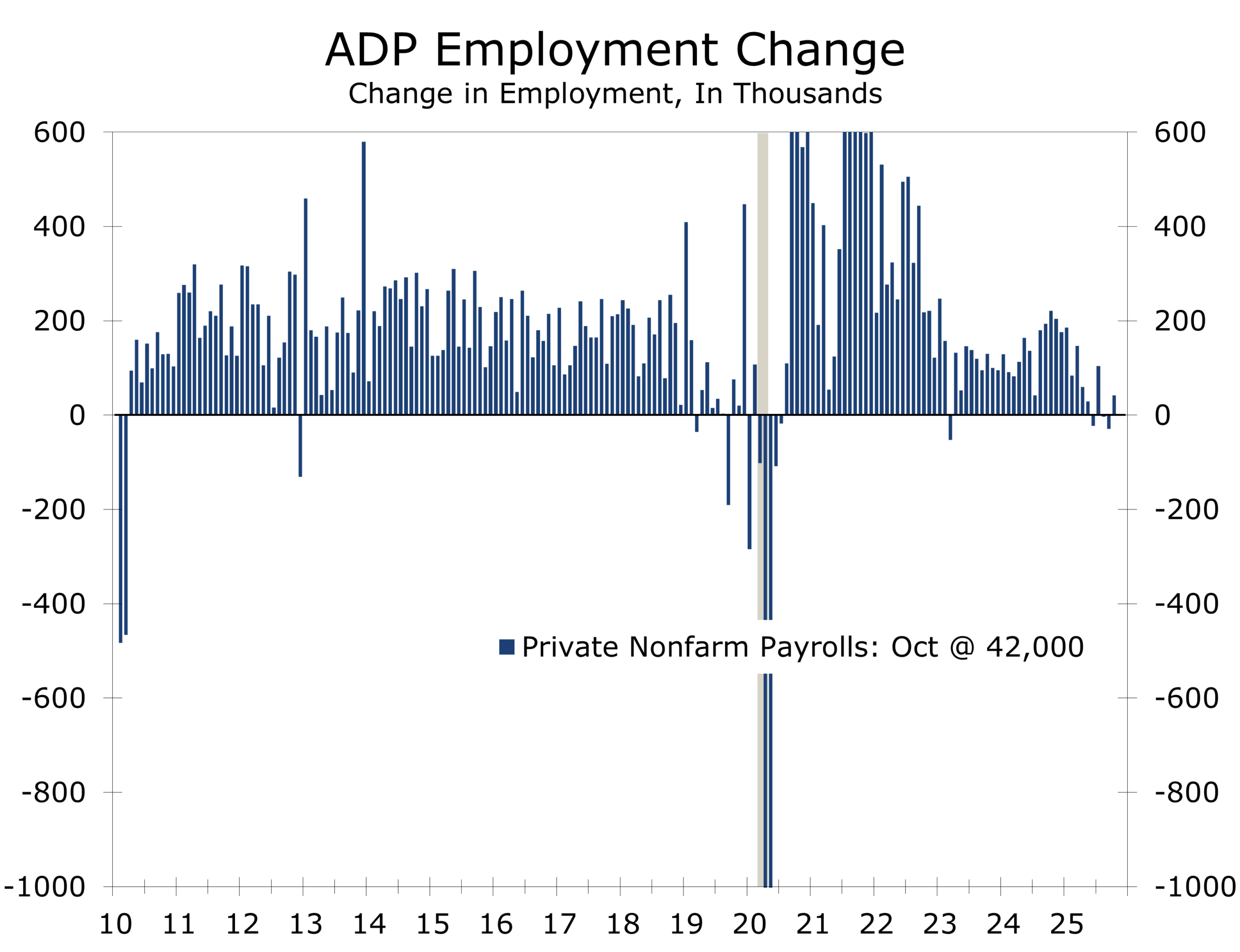

- Private payrolls rose 42,000 in October per ADP, while Challenger layoffs surged 183% from September and jobless claims held near 228,000.

- The data reinforce a picture of a cooling but not collapsing labor market—one where hiring slows, layoffs rise selectively, and firms sustain output through productivity gains rather than adding staff. We may be entering a “jobless expansion”.

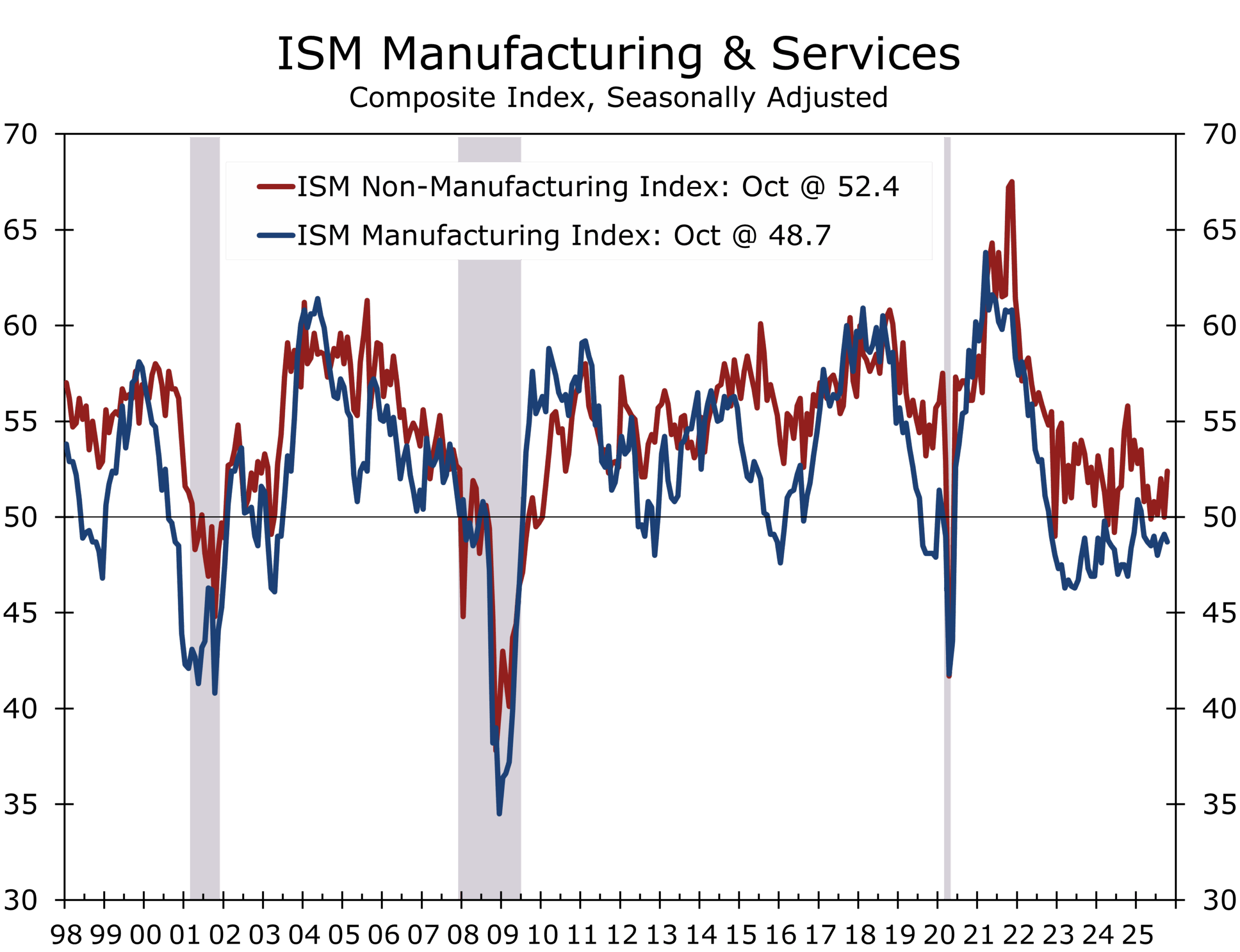

- ISM Services rebounded while manufacturing remains mired in

- Fed officials remain divided as data blackout clouds the December policy decision.

- Stocks suffered their sharpest weekly loss since April; yields remain steady near 4 percent.

- Off-year U.S. elections deepened fiscal gridlock, while Russia escalated winter strikes on Ukraine’s power grid and Israel expanded operations against Hezbollah. Local politics—from New York to Beirut—are now reverberating globally, shaping fiscal policy, supply risk, and energy markets more than central banks.

U.S. ECONOMY & FINANCIAL MARKETS

This week’s commentary assesses the macro and policy landscape, focusing on persistent fiscal uncertainty, labor market bifurcation, and global flashpoints impacting risk assets and corporate strategy. As the government shutdown extends to historic length, prospects for a resolution are improving, with a pivotal Senate vote scheduled Sunday evening and Democrats signaling willingness to support a deal to reopen the government. Macro data visibility remains diminished, creating tactical challenges for allocators and policymakers.

An apparent resolution of the government shutdown appears to be in the works.

The longest government shutdown on record is finally moving toward a resolution. The Senate advanced a bipartisan funding bill on Sunday by a 60–40 vote, clearing the key procedural hurdle to reopen the government. The measure—backed by eight Democrats—would fund most federal agencies through late January and provide retroactive pay to furloughed workers. Negotiations continue over health-care subsidies and longer-term spending caps. The CBO estimates the shutdown has already shaved 1–2 percentage points off Q4 GDP, or roughly $14 billion. A final Senate vote is expected early this week, potentially allowing agencies to resume operations and easing mounting economic strains.

While discussions remain fluid and no deal is finalized until the vote is taken, the mood in Washington has shifted and a breakthrough appears increasingly likely—potentially ending weeks of fiscal drag and market volatility.

Federal contractors and air-traffic controllers remain unpaid, forcing the FAA to cut flight schedules at major hubs. Beyond the fiscal drag, the shutdown has created a data fog for the Federal Reserve just weeks before its December policy meeting. Key inflation and labor reports have been delayed, leaving policymakers to navigate without their usual instruments and relying on private data, experience and instincts.

Labor Market: Cooling, Not Collapsing

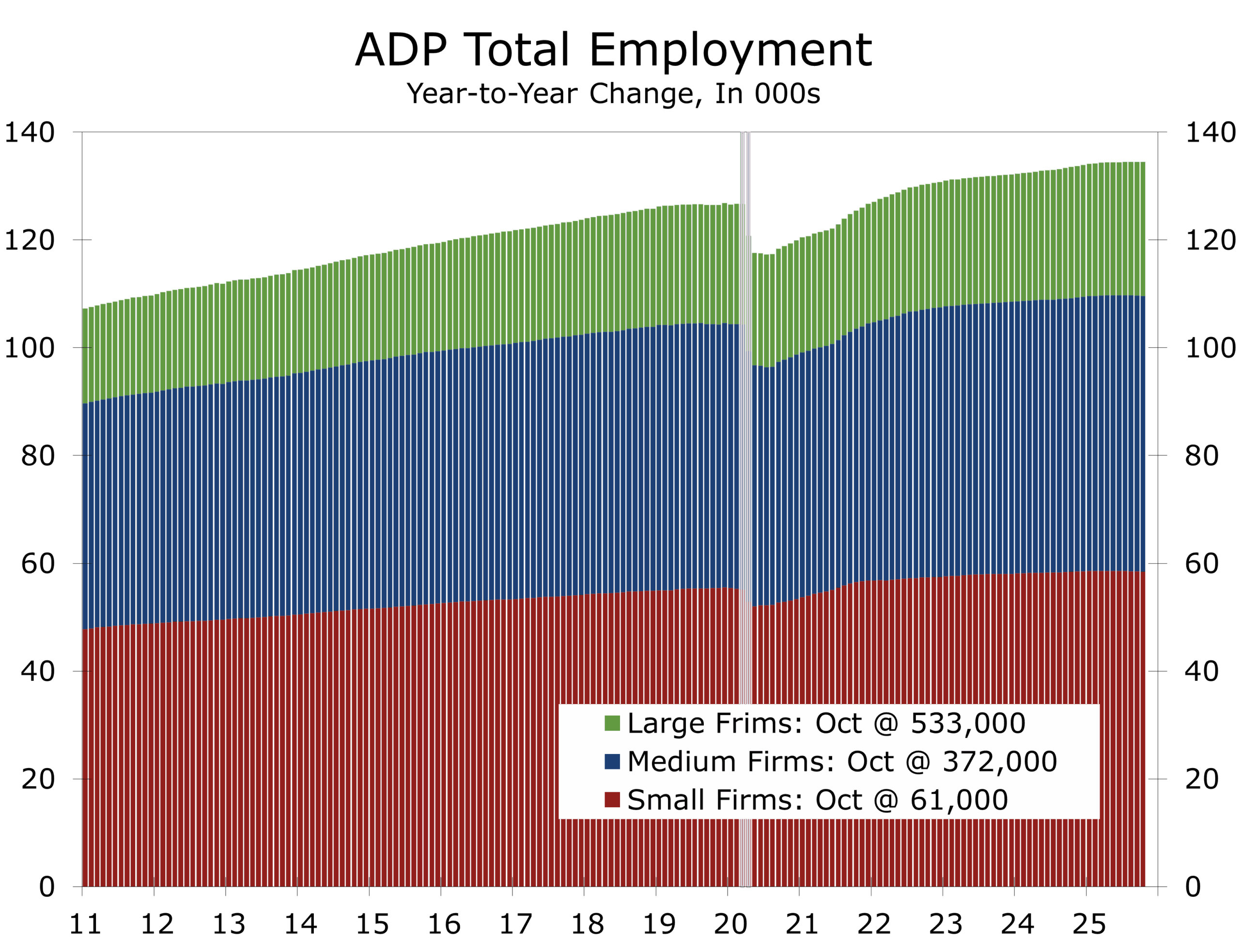

The October ADP report showed a modest 42,000 private-payroll gain—a rebound from two months of declines but well below the pre-pandemic trend. Hiring remains concentrated in healthcare, hospitality and travel-related services while professional and information industries continue to shed jobs. Small and medium sized firms have cut payrolls in five of the past six months, while large companies continue to add staff.

Depictions of a low-hire, low-firm environment may be slightly optimistic; recent data may be overstating net job growth. Productivity gains and AI-driven efficiencies are enabling firms to sustain output with fewer hires. The primary risk is not mass layoffs, but a prolonged period of stagnant hiring and more intense debate over inequality.

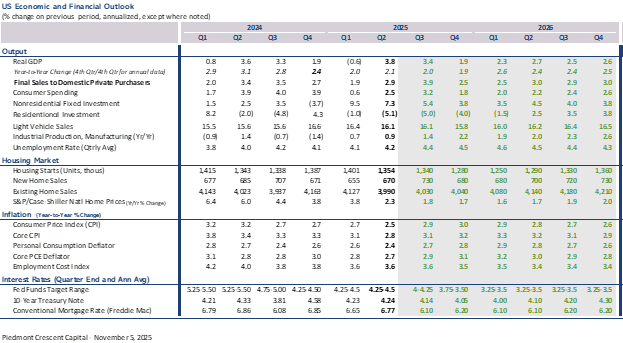

Real GDP is estimated to have risen at a 3.4 percent annual rate during Q3, while nonfarm payrolls averaged just 45,000 per month in July and August. Productivity growth is strong, but labor-force participation is slipping as attractive job opportunities become scarce, immigration slows, and policy uncertainty rises. The threshold for job growth to keep unemployment stable has fallen to roughly 45,000 per month, implying GDP can grow without meaningful job creation.

While layoff announcements spiked in October, state-level unemployment insurance filings do not reflect a generalized uptick. State-level jobless claims remain subdued at around 228,000 per week, consistent with a labor market that is cooling but not cracking. Layoff announcements typically take months to translate into job losses.

The gig economy, meanwhile, provides displaced workers opportunities to generate income while searching for a new position, reducing the impact on headline unemployment statistics.

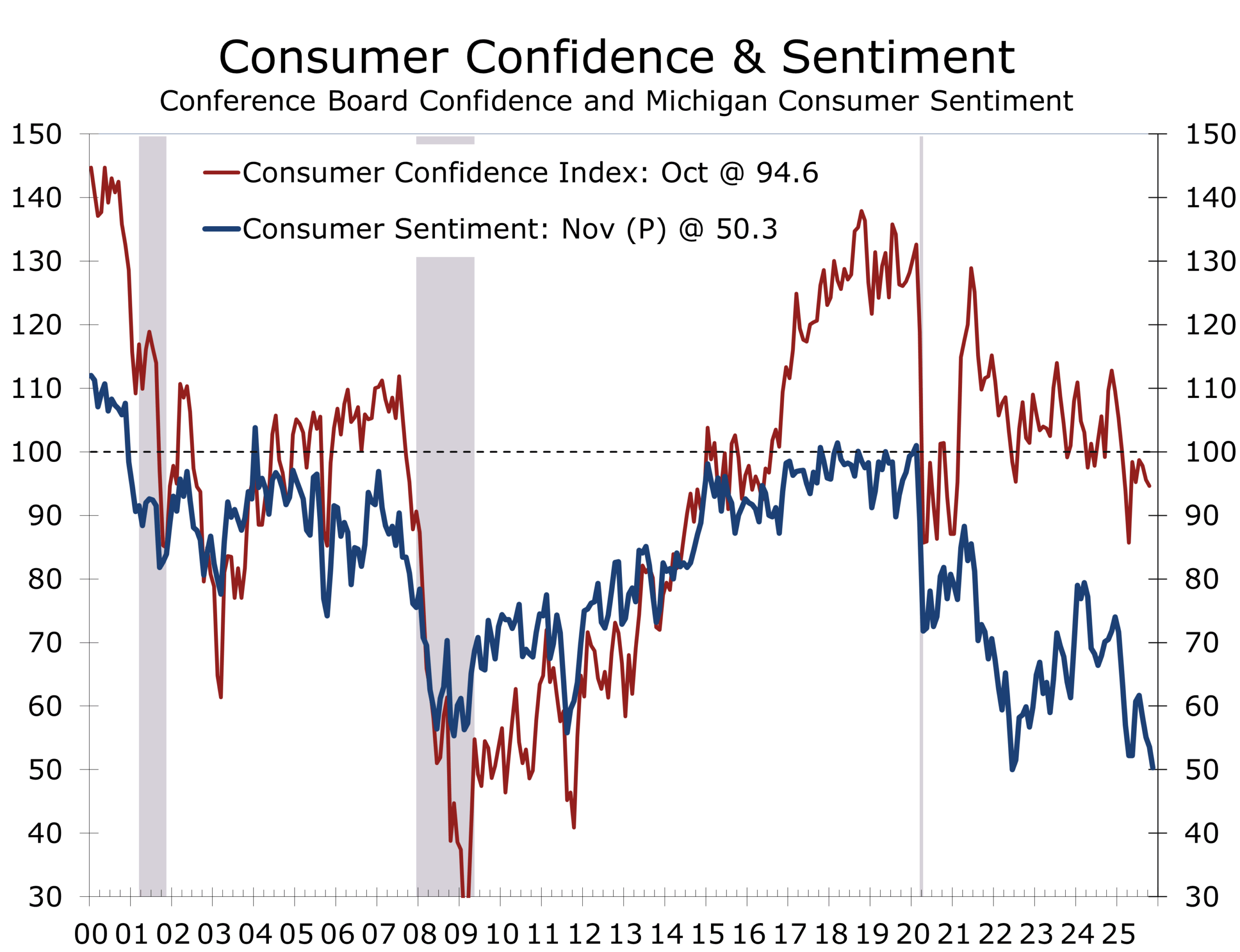

Consumer Mood Sours

Consumer sentiment fell sharply in early November. The University of Michigan Index dropped 3.3 points to 50.3, the lowest since 2022. The decline reflects growing pessimism after the off-year elections and a deepening divide over the government shutdown. Inflation expectations remain elevated at 4.7 percent for one year and 3.6 percent over five to ten years. Notably, gasoline prices—normally inversely correlated with sentiment—fell in late October and early November.

Wealth effects sustain overall spending, even as confidence and credit use sag.

Despite weaker sentiment, the link between confidence and spending remains loose. Wealthier households, buoyed by strong equity holdings, continue to spend, while middle- and lower-income consumers face tighter credit and shrinking real incomes. Consumer credit rose $13.1 billion in September, driven primarily by student and auto loans. Revolving credit remains negative year over year, underscoring the uneven consumer base and the growing bifurcation of the U.S. household sector.

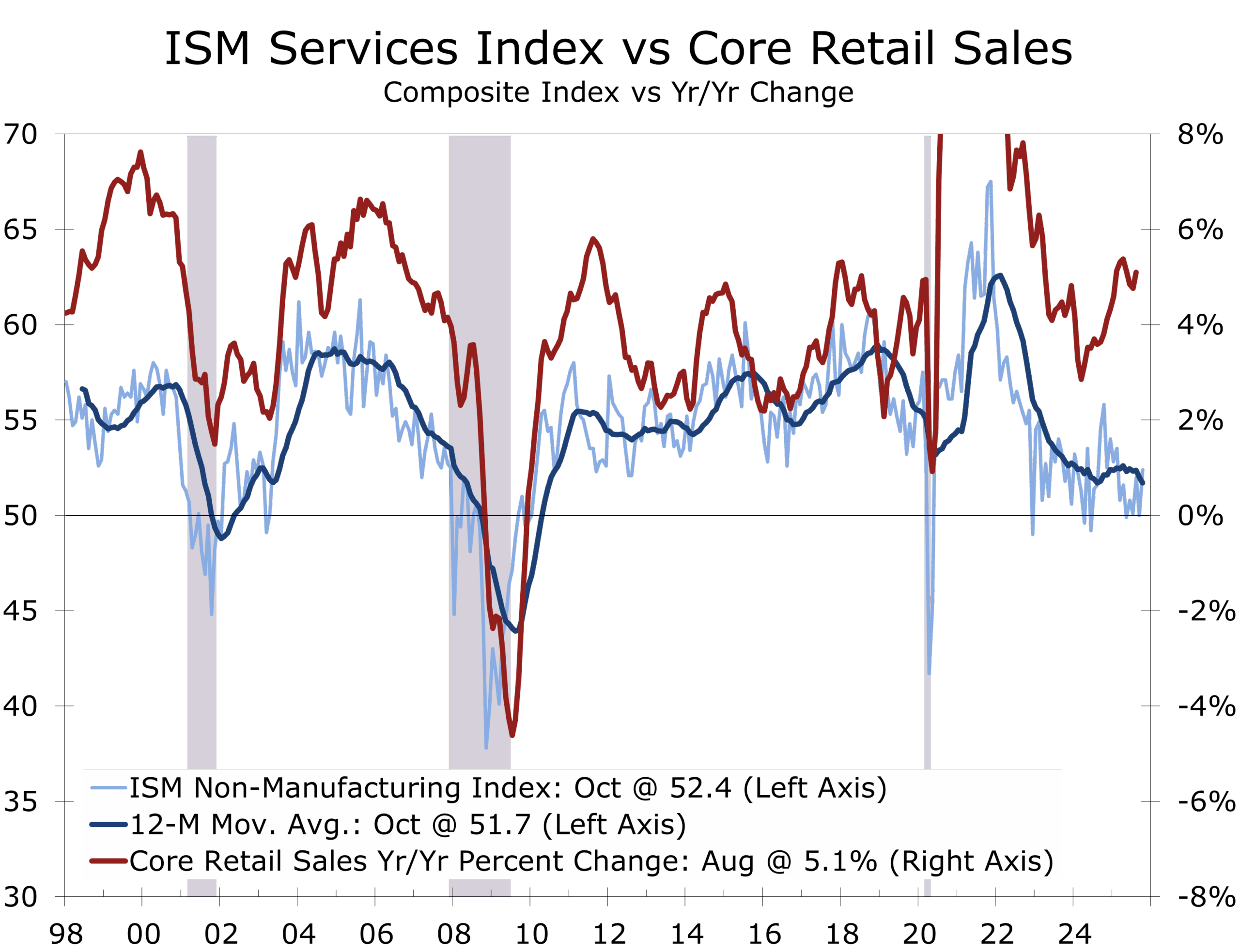

Manufacturing Still Contracting, Services Rebound

The October ISM Manufacturing Index improved modestly but remained in contraction at 48.7, its fourteenth straight month below 50. Production and new orders are still contracting, as manufacturers trim inventories. ISM Services rebounded to 52.4, driven by business activity and new orders, even as employment stayed soft. The Prices Paid Index rose to 70.0, its highest in nearly three years—a reminder that inflation pressures remain entrenched in services.

The economy appears stuck between resilient services and slowing manufacturing.

The mid-December FOMC meeting remains live, with futures markets assigning a 72 percent probability of a 25-basis-point cut. The December meeting resembles a “booth review” in football—a rate cut is the call on the field, and policymakers will need decisive evidence to overturn it, which would unsettle markets, businesses, and consumers.

With official data frozen, the Fed must weigh a softening labor market against potential inflationary effects from tariff pass-throughs. While inflation expectations have firmed, underlying measures continue to moderate. Rents are likely to remain soft through mid-2026. The jobs and hiring outlook has weakened more than expected, keeping risks weighted toward the employment side of the Fed’s mandate.

Markets: Stocks Snap Streak, Bonds Hold Ground

The stock market endured its worst week since April. The S&P 500 fell 1.8 percent, the Nasdaq lost 2.8 percent, and the Russell 2000 declined 2 percent. Selling was broad, led by technology and consumer discretionary sectors, as weak manufacturing data and mounting policy uncertainty weighed on investor sentiment. Stretched valuations in AI-related names and the worsening government shutdown contributed to a long-anticipated pullback.

Treasuries rallied sharply mid-week before yields retraced. The 10-year ended near 4.10 percent and the 2-year at 3.56 percent. Credit spreads widened modestly, and rate volatility remained high as investors moved into quality.

Gold remains around $4,100 per ounce, near its all-time high, supported by safe-haven demand and growing conviction the Fed will cut rates further. Brent crude slipped toward $64 per barrel, the lowest since early spring, after OPEC+ paused production increases amid softening global demand indicators.

Tariffs and the Court

The Supreme Court’s review of Trump-era tariffs may reshape inflation and trade dynamics. Oral arguments last week revealed most justices are skeptical of presidential authority under IEEPA to impose tariffs without Congressional approval.

Prediction markets now place the odds of the Court upholding IEEPA tariffs at 30 percent, down from 40 percent pre-argument. A decision is expected in December or January, with a closely split result probable. Our take is that the Court will rule the president overstepped, but the Administration could shift tariffs under other statutes or preserve international agreements.

Refunds to U.S. importers will likely be less than originally remitted, with payments delayed and requiring legal follow-up. The net deflationary impact may emerge gradually, via lower import costs and modest relief to corporate margins.

Alternative tariff authorities include:

- Section 122 of the Trade Act of 1974—temporary tariffs up to 15 percent

- Section 301 of the Trade Act—retaliatory tariffs for unfair trade practices

- Section 232 of the Trade Expansion Act of 1962—tariffs on national security grounds

A ruling invalidating tariffs would slightly reduce near-term inflation risk, offering some cushion for policymakers heading into 2026. Renewed use of alternative authorities could reintroduce friction, sustaining supply chain and price volatility. The decision, expected late this year or early 2026, will add another twist to the Fed’s calculus.

Geopolitics: Off-Year Elections and Global Flashpoints

Off-year elections injected more volatility into Washington’s fiscal environment. Democrats gained ground in several key states, underscoring voter frustration with living costs, affordability, and the shutdown. The results strengthen Democrats’ negotiating position in the budget impasse, increasing pressure on House Republicans to act before the economic fallout widens.

Zohran Mamdani’s upset win in New York City on a platform of rent stabilization, transit breaks, and progressive taxation sent shockwaves, prompting immediate White House response—even threats to withhold funding. The federal-local confrontation highlights tangible risks for businesses tied to contracts, infrastructure, or transit systems.

The broader political takeaway is voter fatigue with dysfunction and an emphasis on affordability and stability over ideology. Markets have noticed: the sell-off in equities and rally in Treasuries reflect the view that fiscal disarray, not inflation, is the principal near-term risk.

Russia and Ukraine

Russia’s winter offensive intensified, launching the largest strike on Ukrainian energy infrastructure since the 2022 invasion.

- 458 drones and 45 missiles struck 25 sites across four regions.

- National generating capacity temporarily dropped to zero; outages of up to 12 hours daily in Kyiv

- Civilian casualties rose; Zelenskyy appealed to allies for more Patriot air defense systems

Sanctions waivers for Hungary and continued energy purchases further strain Ukraine’s resilience. Markets remain insulated so far, with energy prices subdued. But escalation risks remain if supply disruptions resurface.

Israel, Hezbollah, and Gaza

Conflict along Israel’s northern border flared, with strikes on Hezbollah in southern Lebanon targeting elite Radwan forces. Disarmament under UN Resolution 1701 remains critical but unfulfilled, complicating prospects for lasting peace. Lebanese and Israeli experts emphasize that failure to disarm Hezbollah undercuts incentives for Hamas and impedes regional stability.

The U.S. Treasury has sanctioned Hezbollah facilitators for funneling funds from Iran. Lebanon’s economic stability now hinges in part on progress toward disarmament.

Meanwhile, Gaza remains volatile. Hezbollah’s claim of success in resistance strategy and inter-group connectivity heighten the risk of north-south escalation. For markets, the status quo is baked in, but any misstep could quickly revive regional risk premiums across energy and defense assets.

OPEC+ and Energy Politics

OPEC+ opted to hold output increases through March 2026, raising only 137,000 barrels per day in December. Weak demand—especially in Asia—drives the decision. Oil prices reflect the freeze, with Brent crude in the low-$65 range and WTI at $61–62. The cartel’s strategy favors stability over spikes, aligning with fiscal stress and rising inventories.

Other Global Flashpoints:

- China: The Fifteenth Five-Year Plan signals more regulation over stimulus, weighing on equities.

- Iran: Intensified uranium enrichment sets the stage for future negotiations.

- Taiwan/Pacific: U.S. naval patrols continue, but risk of confrontation remains muted.

Strategy Watch: For CFOs and Treasurers

- Liquidity and Funding: Volatility in equities and steady Treasury yields present an opportunity to term out short-term debt before year-end. Curve remains slightly upward-sloping; locking in spreads provides insurance ahead of potential rate cuts.

- Cash and Investment Policy: Money-market yields have eased to 3.8–3.9 percent. Ladder Treasury bills and short-duration agencies to preserve liquidity and reduce reinvestment risk.

- Credit and Counterparty Risk: Spreads have widened modestly but remain tight by historical standards. Reassess supplier and customer credit exposure, especially for small or trade-exposed counterparties.

- FX and Commodities: Unwind euro hedges partially; maintain yen protection and update commodity-linked hedges for current price levels.

- Capital Spending and Planning: Expect slower Q4 cash flow, reflecting delayed federal contract payments. Maintain caution on discretionary capex until visibility improves in later this year and in early 2026.

The Week Ahead: November 10–16

Key indicators will remain limited by delayed federal releases. Focus on NFIB small business optimism, Fed speeches, weekly jobless claims, and pre-meeting remarks from Atlanta Fed President Bostic and Kansas City’s Schmid for insight into the Fed’s December outlook.

The economy is expected to post 3.4 percent real GDP growth for Q3 and to slow to just under 2 percent in Q4, with momentum increasingly reliant on consumer services and exports as hiring and credit conditions tighten.

Markets begin the week on a firmer footing. The 10-year Treasury yield jump back up to 4.15 percent on optimism that the government shutdown is nearing resolution before settling back in at 4.10. Equities look set to rebound, and the dollar remains mixed, reflecting improved fiscal sentiment but ongoing uncertainty about the Fed’s next move.

For CFOs, treasurers, and other decision makers: liquidity first, duration second, discipline always. Use near-term optimism around a fiscal resolution to lock in funding and reassess exposures—while remembering that the underlying structural issues remain unsettled.

The economy is still moving forward, but the composition of growth is shifting. Productivity, not payrolls, is now driving the expansion. The Fed faces a complex policy decision on a short timetable, and markets and business leaders are adjusting to a slower, leaner phase of growth.

In this environment, balance-sheet discipline and liquidity flexibility are the best tools—and staying opportunistic will be the edge as the market recalibrates around the next policy turn.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

November 10, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000