Highlights of the Week

- The U.S.-EU trade deal narrowly avoided escalation, codifying 15% tariffs on most EU exports. The move buys time—but not a final settlement—in a broader trade realignment aimed squarely at China.

- Strategic cooperation is being reframed as large-scale foreign investment in U.S. infrastructure, energy, and defense supply chains—much of it backed by federal loan guarantees.

- Durable goods orders slipped less than expected, but core capital goods fell for the third straight month, pointing to softening investment amid tariff uncertainty.

- New and existing home sales both disappointed in June, and housing inventories are building—especially at the higher end—constraining momentum for construction and consumption. The weakened state of housing is a macroeconomic concern.

- Labor market data remain mixed: initial claims edged down, but continuing claims are trending higher, suggesting fewer re-hires and weaker hiring momentum.

- Escalating conflicts Israel-Gaza and at the Thai-Cambodian border briefly rattled markets, though cease-fires and trade-linked diplomacy have helped reduce near-term geopolitical risk.

- Markets now expect the Fed to tee up a September rate cut. This week’s data onslaught—including payrolls, inflation, ISM, and the FOMC decision—will help determine the timing and magnitude of the next move.

Driving Toward China

President Trump was not merely playing through at his Scottish golf resort last week—he was laying down the contours of a new trade regime. The U.S.-EU deal announced Sunday sidesteps a tariff spike just before the August 1 deadline, setting a 15% baseline tariff on most EU exports, including autos. That is a gentler swing than the 25% some had feared, but it still embeds lasting friction into the U.S.-Europe trade relationship.

Trump is not just negotiating trade—he is improving the lie ahead of the next big shot.

The bigger game remains China. As we noted in The CAVU Compass, Trump’s approach to trade diplomacy is less about bilateral wins and more about setting the global lie ahead of a final showdown. By locking in terms with allies—Japan, Vietnam, Indonesia, and now the EU—Trump is creating a global framework designed to isolate Beijing and force its hand on critical minerals, semiconductors, and intellectual property enforcement. China is currently engaged in talks ahead of the August 1 deadline and is widely expected to strike a deal.

The structure of Trump’s trade deals is evolving into a new form of strategic cooperation—not simply tariff relief, but access to U.S. markets in exchange for meaningful investment in American infrastructure and industrial capacity. The message is clear: allies may keep their trading lanes open if they help America re-industrialize. Countries are buying into the strategy as the most effective way to manage China’s rise. There is broad recognition that the United States must remain a credible counterweight to a more assertive China.

That help increasingly takes the form of large capital commitments—many of them supported by U.S. loan guarantees—to fund energy infrastructure, logistics, and defense supply chains. A prime example is the push to unlock vast reserves of natural gas in northern Alaska. Multiple bilateral discussions with Japan and South Korea have centered on financing export terminals, pipelines, and processing hubs to bring Alaskan LNG to Asia. Similar arrangements are in discussion for critical mineral processing, semiconductor packaging, and submarine cable networks. Energy is also a key pillar of the EU deal and is intended to reduce dependence on Russian natural gas.

This is industrial policy at global scale. The new model is part trade deal, part energy alliance, and part security compact. It redefines globalization as conditional access—with terms enforced not just by tariffs, but by capital flows and strategic alignment. Tariffs are likely to settle in at a 15% base rate on all imports to the United States, lower rates on U.S. exports, and higher rates on strategic sectors such as steel, aluminum, semiconductors, and electric vehicles. Investment pledges—largely structured as loans or loan guarantees—allow the administration to claim that most of the long-term financial benefit remains in the United States. Interest payments are not profits.

Both the Japan and EU deals were par fours—difficult, but straightforward plays from the fairway. The China deal, however, is shaping up to be a long par five—narrow, uphill, and fraught with hazards. The outcome will define not just the trade balance, but the structure of the global economy for decades to come.

Trade and the Treasury Market: Sand Traps Ahead

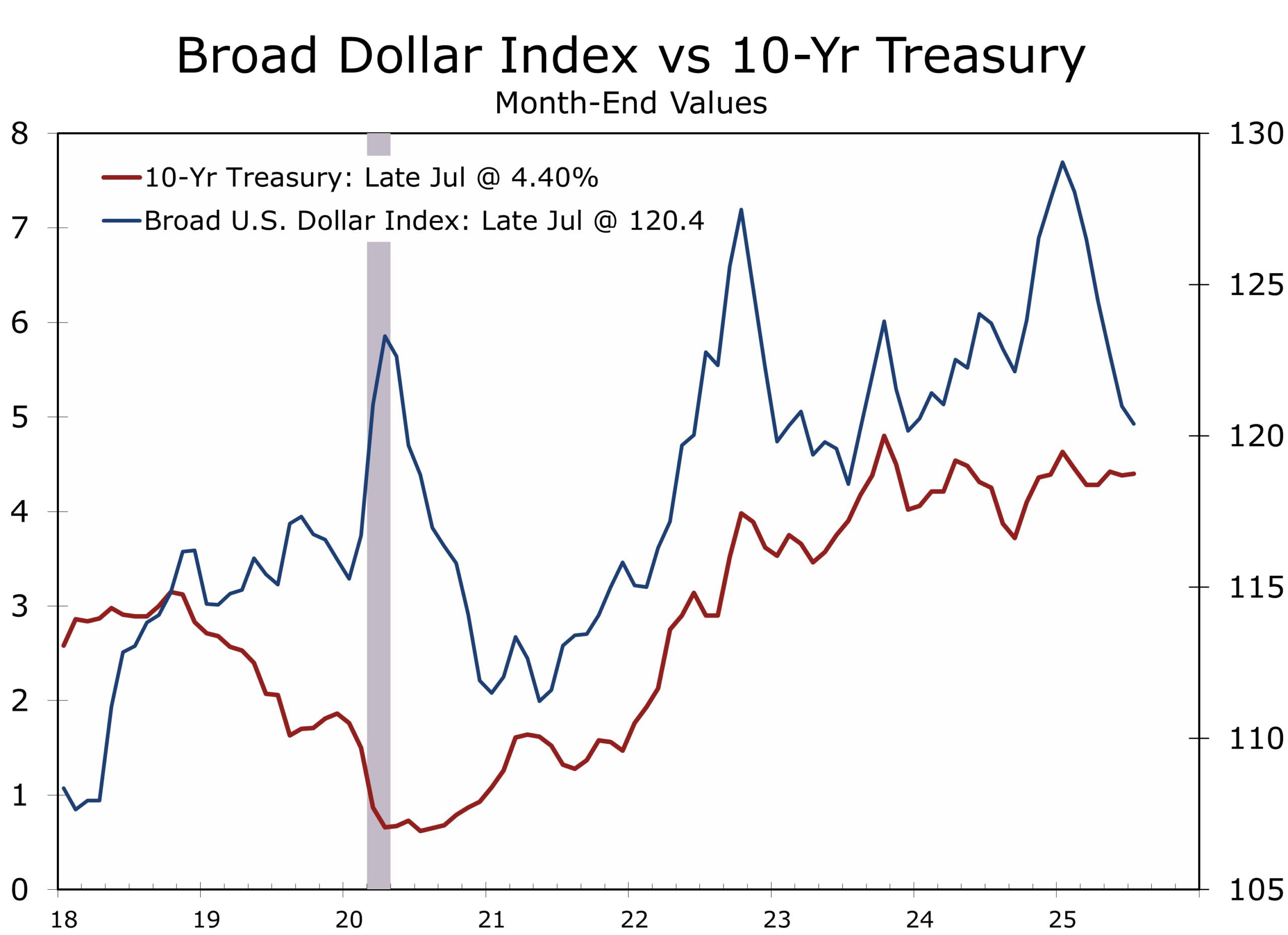

Markets greeted the EU trade deal with cautious optimism. Treasury yields initially moved higher overnight as risk sentiment improved, but the rally quickly faded. The long end of the curve remains vulnerable to supply concerns and lingering inflation risks, with the 10-year note briefly testing support near 4.5%. While the deal provided a modest lift to the dollar, the broader trend remains downward as the Fed edges closer to a dovish pivot and the terms of trade continue to deteriorate.

The U.S. remains the cleanest scorecard in the clubhouse—and likely to remain so.

Tariff revenues are climbing, but so are investor concerns about policy unpredictability and inflation passthrough. The flurry of recent trade agreements has reduced—but not eliminated—uncertainty. The dollar’s recent weakening reflects this shift, as global investors begin to question how long the U.S. can remain the cleanest scorecard in the clubhouse.

We remain confident that the dollar will hold its status as the world’s reserve currency for the foreseeable future. While increased foreign direct investment may require producers abroad to export more to the U.S. to finance those flows, the investment itself—and the economic growth it spurs—will ultimately boost returns on dollar-denominated assets. We expect near-term softness but anticipate dollar strength to return within 18 to 24 months.

Housing Loses Momentum

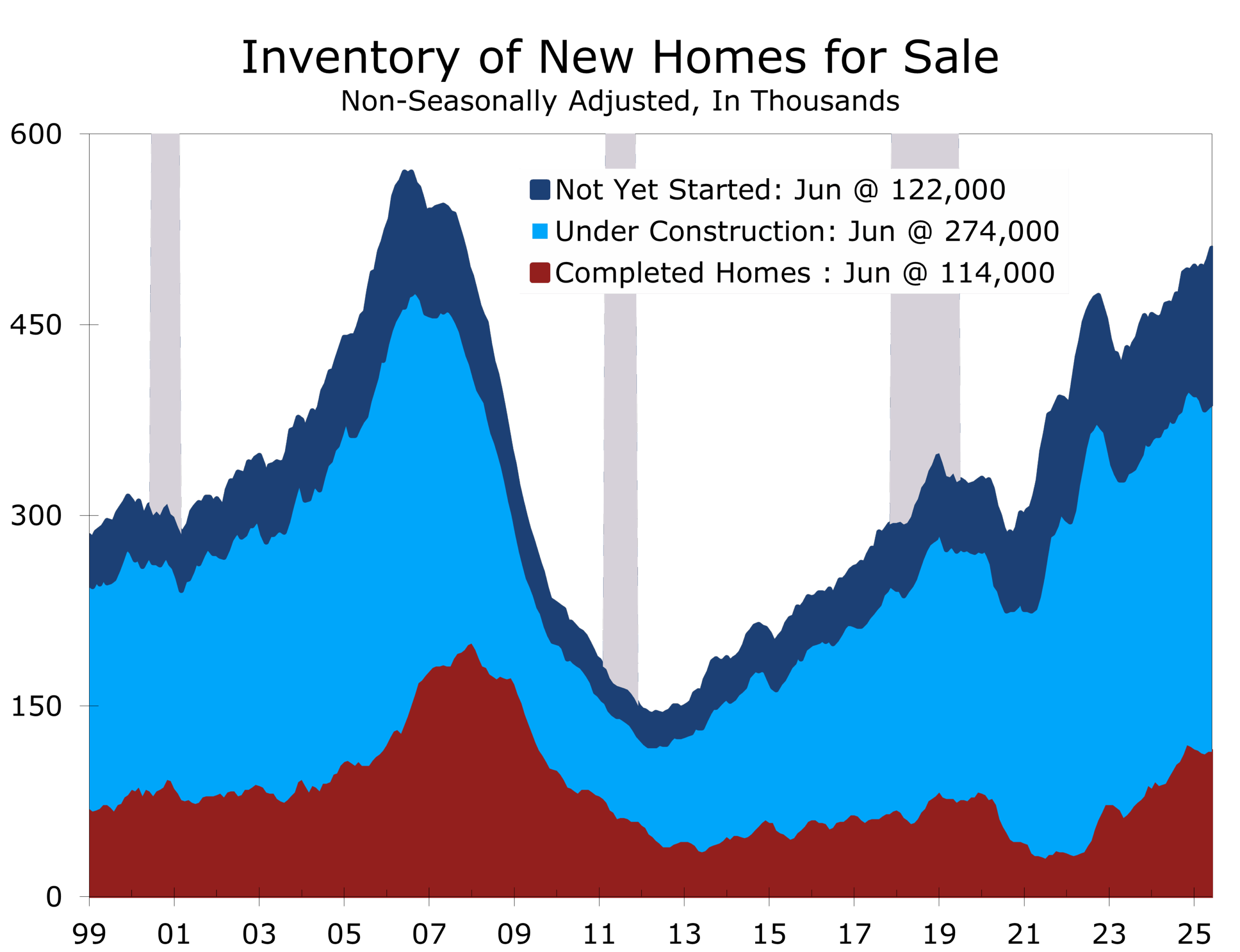

June’s existing home sales fell 2.7% to a 3.93 million annual pace, nearing post-GFC lows. The median existing home price climbed to a record $435,300, but that higher median price reflects a lack of inventory at the low end, not resurgent demand. Supply remains more than adequate at the upper end of the market. New home sales edged up just 0.6% to a 627,000 pace and are down 6.6% from a year ago. Builders are leaning on incentives and price cuts to sustain sales, but inventories of completed new homes continue to climb—now at their highest level since 2009. A substantial backlog of homes under construction also persists.

Single-family permits have declined for four straight months, underscoring increased caution among builders. Higher-end inventory is accumulating, while first-time buyers remain constrained by affordability challenges and high mortgage rates. We expect sidelined buyers to return as rates move closer to 6%, but a sustained recovery is unlikely until the labor market stabilizes. New hiring and job switching have both slowed sharply over the past year, reducing mobility for both renters and homeowners.

Business Investment: Chipping Away

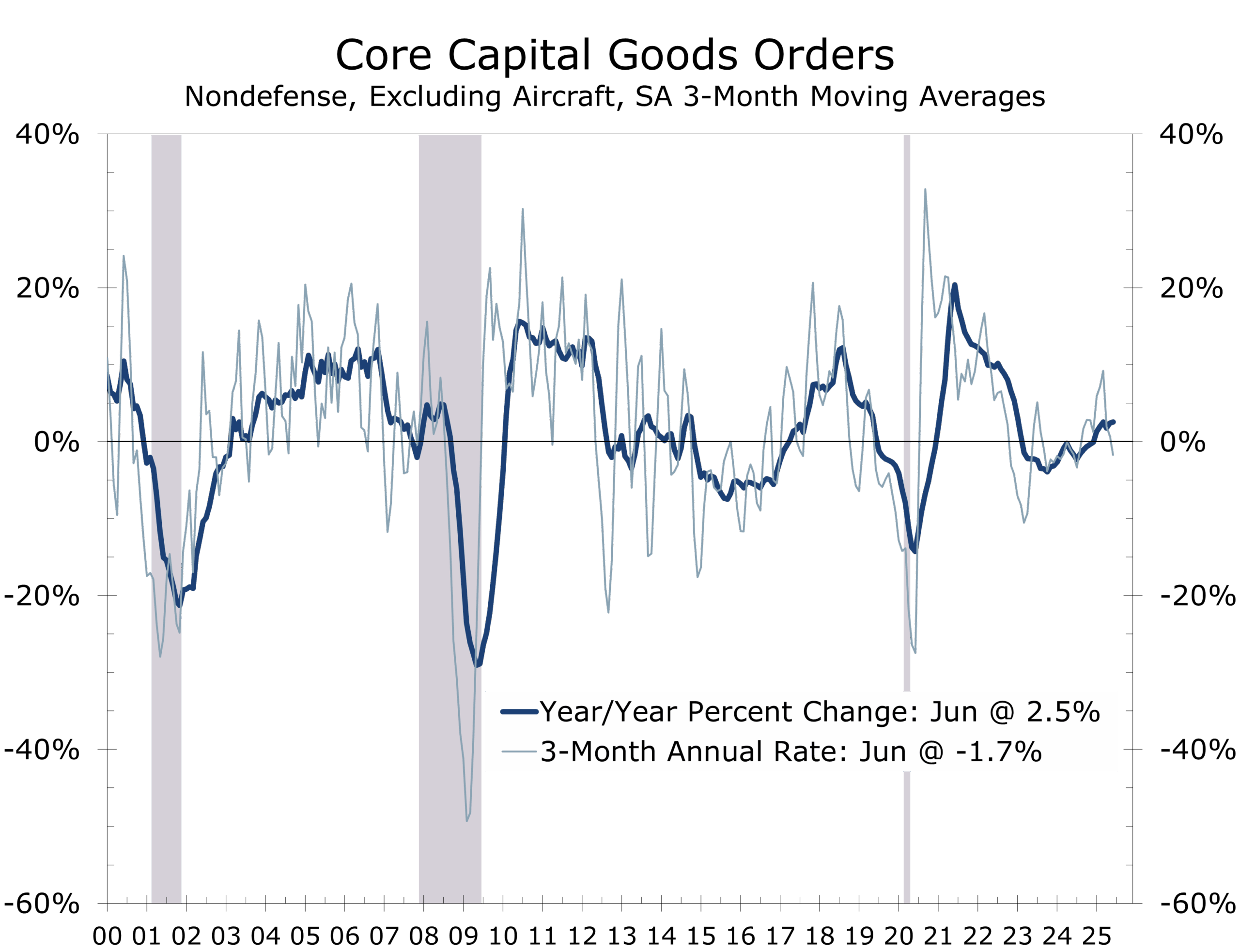

Durable goods orders fell 9.3% in June, which was less than expected and only partially reversed the prior month’s 16.5% spike driven by a surge in commercial aircraft orders. Capital goods orders excluding aircraft and defense fell a larger-than-expected 0.7%, marking the third consecutive monthly decline and pulling the measure back into negative territory for the quarter. Business equipment shipments also slipped, suggesting that Q2 business investment will be soft following a strong Q1.

Policy uncertainty is clearly weighing on capital spending. Trade deals—especially provisions requiring reshoring to receive tariff relief—may eventually support investment, but in the short term they are raising costs and clouding visibility. Until the fairway clears, expect firms to play it safe and lay up.

Labor: No Longer Pin-Seeking

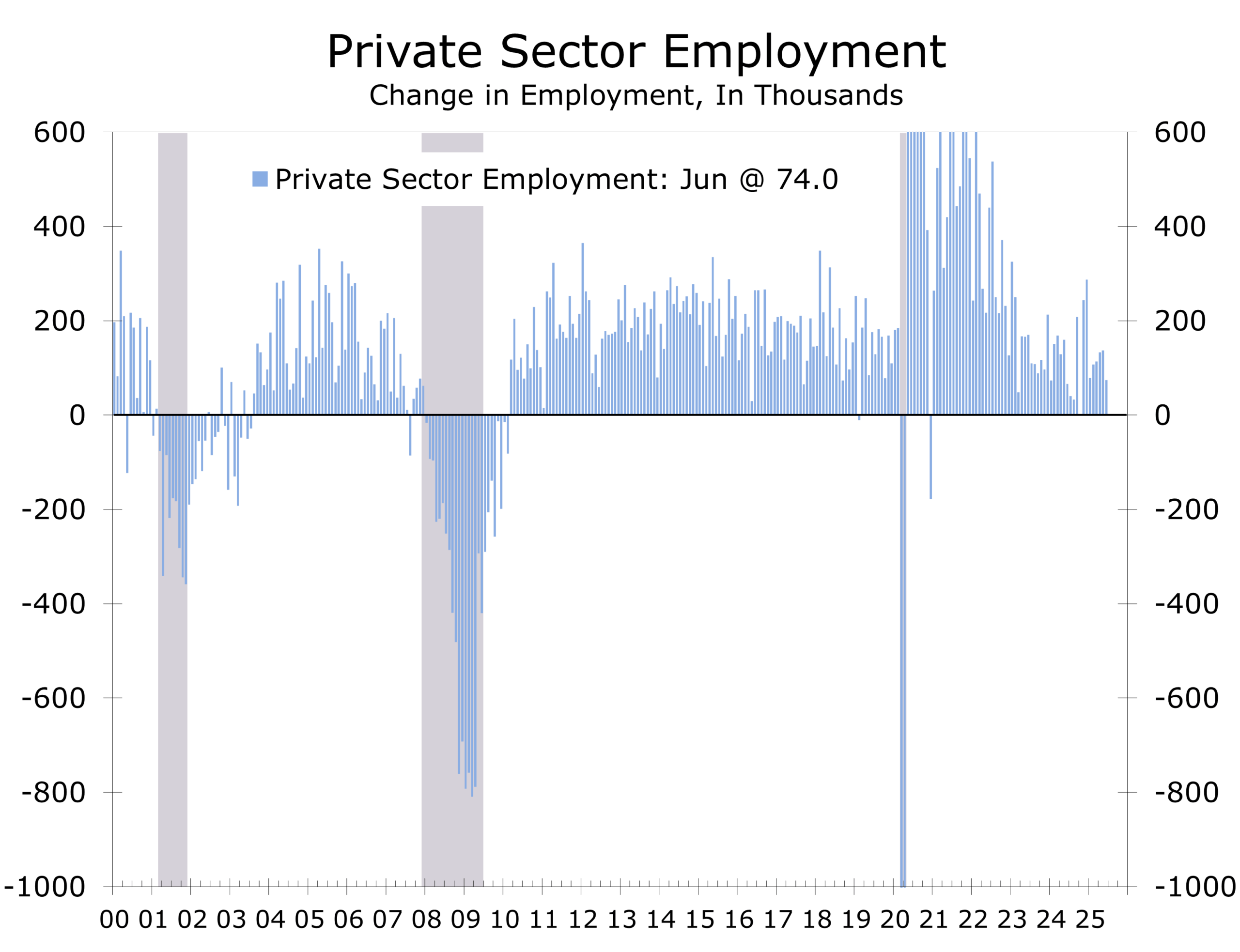

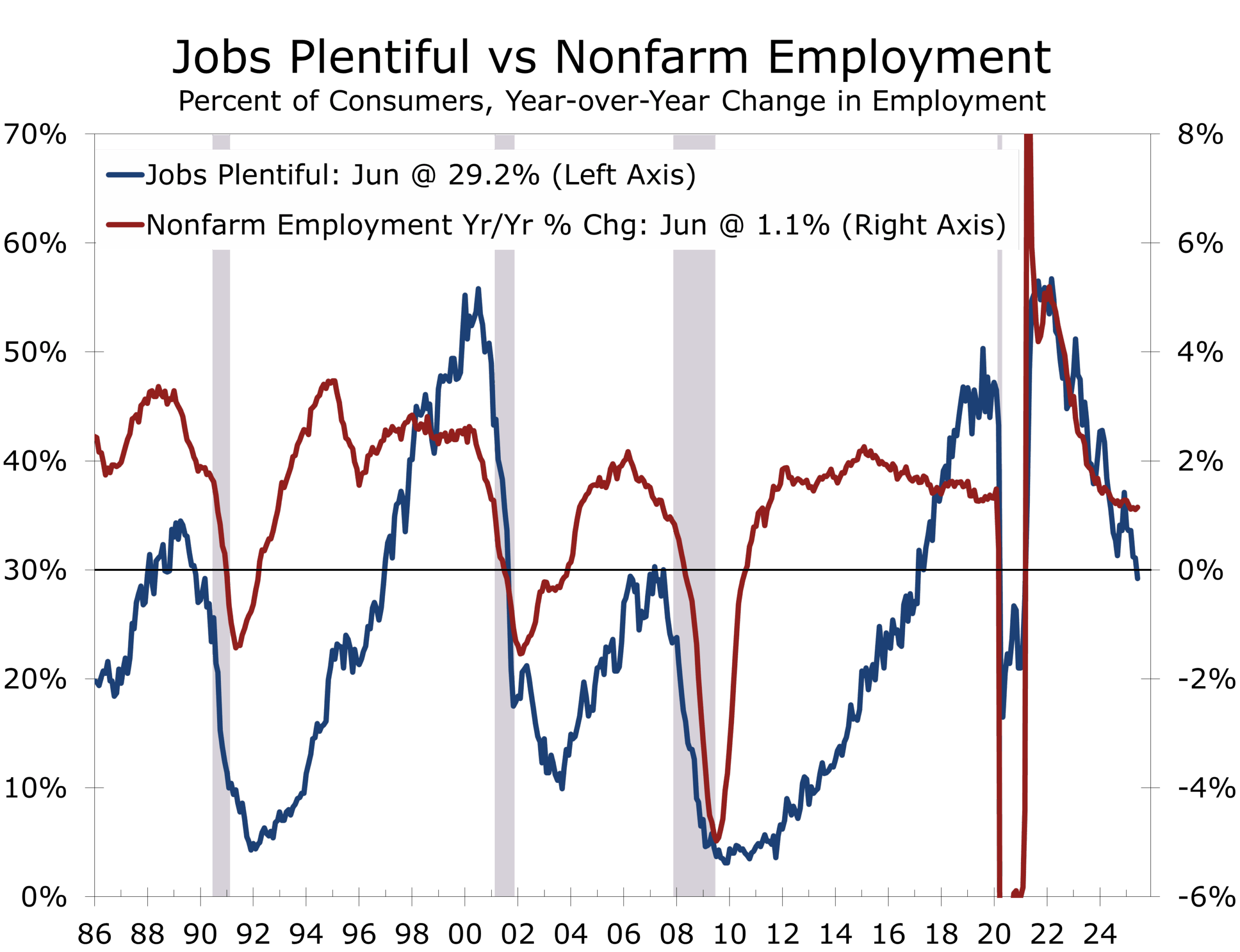

Initial jobless claims fell to 215,000—better than expected—but continued claims edged higher to 1.96 million. The divergence suggests a labor market in transition: layoffs remain low, but hiring is slowing. Quits are down, long-term unemployment is ticking up, and recent federal layoffs—enabled by a Supreme Court ruling that curbed agency protections—are beginning to register in the data. AI adoption may also be dampening hiring in the near term, even as it boosts productivity over time. In June, private employers added just 74,000 jobs, and a separate report from ADP showed private sector headcount declining by 33,000.

The recent softness in labor market data is unlikely to trigger a panic rate cut, but it does strengthen the dovish case. Wage growth has moderated, and if the July jobs report shows sub-trend gains or an uptick in the unemployment rate, momentum could shift more decisively toward easing. The unemployment rate, however, may remain artificially low in the near term due to tighter immigration enforcement and an accelerating wave of Baby Boomer retirements.

We are looking for a soft July payroll print this Friday, with nonfarm payrolls rising by just 95,000 jobs. The unemployment rate should edge higher to 4.2%.

Geopolitics: Pressure Points, Limited Market Reaction

Two geopolitical flashpoints dominated headlines last week but left financial markets largely unmoved.

In the Middle East, renewed rocket fire from Hamas prompted fresh Israeli airstrikes in Gaza, escalating a conflict already marked by deep humanitarian strain. Civilian casualties are rising, and critical infrastructure in Gaza remains decimated. U.S. and regional mediators—including Egypt and Qatar—are pushing to restart talks, though the prospects for a durable cease-fire remain slim. Washington has urged Israeli restraint, citing risks to regional energy flows and the fragile stability underpinning the Abraham Accords.

Hamas continues to pursue a strategy aimed at maximizing civilian casualties and leveraging global media to generate sympathy abroad. The group’s stated objective—the eradication of Israel—stands in stark contrast to the portrayal in many widely circulated images, including two this weekend that were factually misleading. One featured a child with cerebral palsy, falsely presented as a typical Gaza victim; the other showed a child receiving long-term medical care in Italy for unrelated reasons.

Israel has consistently found itself on the defensive in the global PR war, with critical coverage emerging before it even responds to attacks. That dynamic has prompted Israel to take more assertive steps to deliver aid, including parachuting in humanitarian supplies—provided by other governments—via IDF aircraft. There is no viable resolution to the conflict that allows Hamas to remain in power, and the longer Hamas holds control, the more the people of Gaza are likely to suffer. That view is not unique to Israel; it is shared by several Arab governments in the region.

In Southeast Asia, Thailand and Cambodia agreed to an unconditional cease-fire after five days of deadly clashes along their contested border. The conflict, rooted in a century-old dispute over ancient temple sites, displaced more than 300,000 civilians and claimed at least 35 lives—mostly noncombatants. A breakthrough came after President Trump made a cease-fire a precondition for further trade talks, threatening a 36% reciprocal tariff on Thai and Cambodian exports. The deal was brokered in Kuala Lumpur by Malaysian Prime Minister Anwar Ibrahim, with quiet support from both U.S. and Chinese officials.

Despite the use of drones, naval assets, and heavy weaponry, markets barely reacted. Risk assets held steady, oil prices remained stable, and Treasury yields stayed within recent ranges.

The muted response reflects a familiar pattern: unless geopolitical shocks directly threaten global supply chains or major energy corridors, markets are inclined to look through them. Still, the growing use of trade tools to influence regional conflict outcomes is a trend worth watching—particularly as tariff diplomacy increasingly doubles as security policy.

The Turn: Tight Lies and Tighter Margins

This week will tell us a lot—about where the economy stands, where it’s headed, and how much room the Fed has to maneuver.

Wednesday’s FOMC meeting will anchor the week, with Powell expected to strike a more cautious tone. Thursday brings the June PCE inflation report and the Employment Cost Index. Friday delivers the July payrolls report, ISM manufacturing data, and consumer sentiment.

Markets are also watching trade. August 1 marks the formal implementation date for the new tariff regime. Last-minute exemptions are still possible, but the direction is set: more trade friction, more policy uncertainty, and greater reliance on industrial strategy over free trade.

On the earnings front, over 150 S&P 500 firms will report—including Apple, Amazon, Microsoft, and Meta. Corporate commentary on hiring, pricing, and investment will provide critical insight into how companies are adjusting to higher costs and slower demand.

The Fed may be nearing a rate cut, but this is no easy putt. The economic recovery remains intact—but vulnerable. Tariff policy is distorting inflation signals, business investment is fading, and the labor market is losing altitude. With each deal struck, the stakes grow higher for the U.S.-China endgame—and the global fairway narrows.

This Week’s Scorecard: Key Data on the Tee

Tuesday, July 29 – Opening Shots

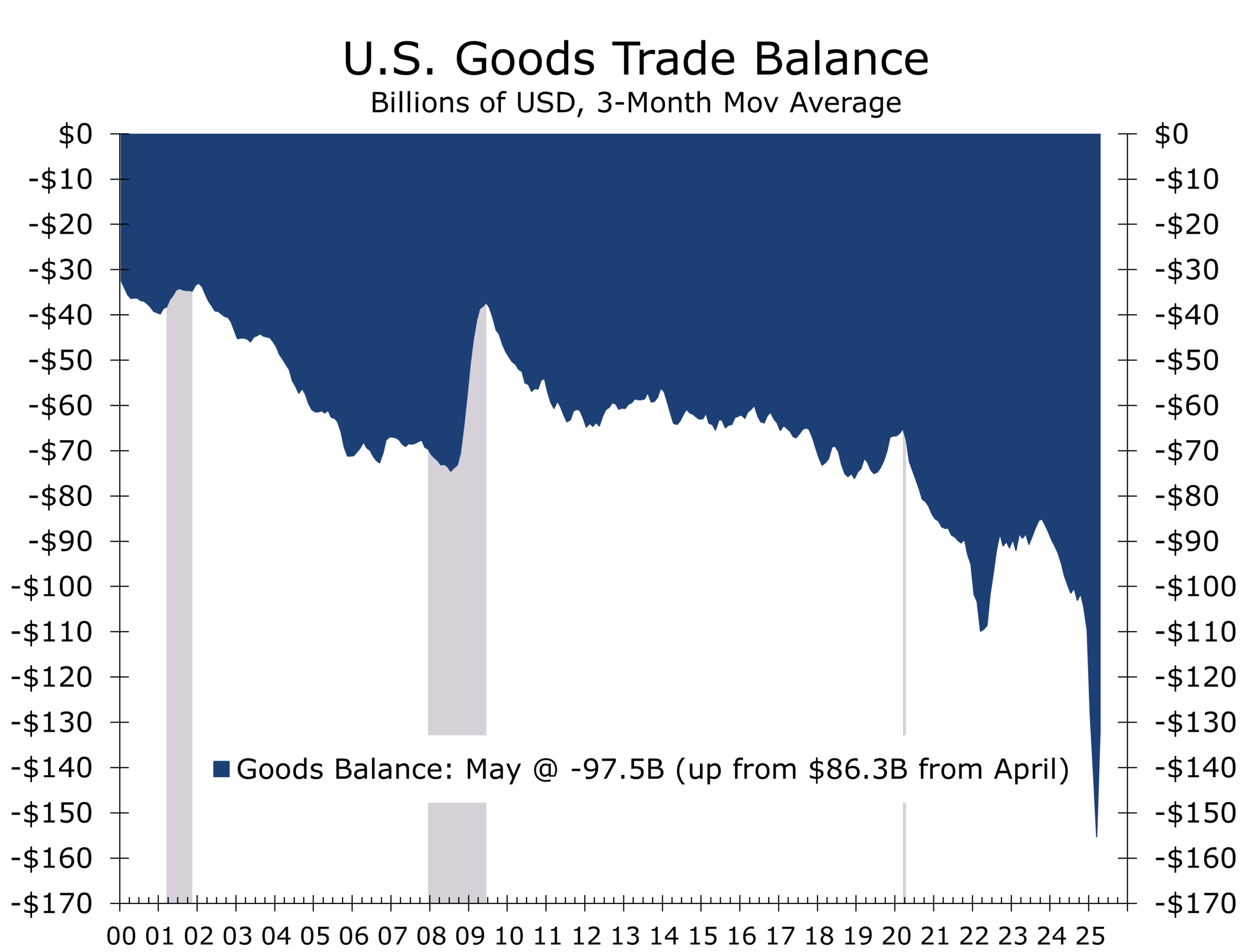

- Advance Goods Trade Balance (June)

Expect a widening deficit as exports slow and pre-tariff imports remain elevated. - Wholesale Inventories (June, preliminary)

Inventories likely dipped slightly, playing it safe from the rough. A larger drop would cause forecasters to scale back Q2 GDP estimates. - FHFA House Price Index (May)

Continued declines expected as sellers adjust to tighter conditions. - S&P Case-Shiller Home Price Index (May)

Price softness is deepening, particularly in Florida and Texas, with more markets joining the slide. - JOLTS (June)

Openings likely declined again; many remain posted but unfilled. The quits rate is the one to watch. - Consumer Confidence (July)

A modest rebound is expected, helped by easing tariff concerns and steadier market conditions—though labor market nerves could hold sentiment back.

Wednesday, July 30 – The Mid-Round Turn

- ADP Employment Change (July)

Following last month’s miss-hit, expect a partial recovery—about +55,000—plus possible revisions. - Q2 Advance GDP

Forecasted at +2.6%, powered by net exports and moderate consumption. Atlanta Fed GDPNow is tracking at 2.4%. - Pending Home Sales (June)

A slight gain is likely, supported by lower mortgage rates and a small lift in purchase applications. - 2:00 PM – FOMC Statement

- 2:30 PM – Chair Powell Press Conference

Thursday, July 31 – Staying in the Fairway

- Employment Cost Index (Q2)

Expected to rise 0.8%, with annual wage growth easing to 3.5%. A slight fade from earlier strength. - Personal Income & Spending (June)

Income +0.3%, spending +0.2%. Core and headline PCE expected at +0.3%, though a softer read is possible on core.

Friday, August 1 – A Crucial Approach

- Nonfarm Payrolls (July)

Job growth is expected to slow to +90,000, with the unemployment rate ticking up to 4.2%. Hiring restraint and seasonality are in play. - ISM Manufacturing Index (July)

Still under par at just below 50. Defense and tech are driving modest strength, while construction and consumer sectors struggle. - Construction Spending (June)

Residential and commercial weakness continues, though infrastructure may provide a lift from the sand trap. - University of Michigan Consumer Sentiment (July, final)

Sentiment should edge higher with steadier inflation expectations and market gains—but survey polarization remains a hazard.

Final Putt: A Narrow Fairway Ahead

As the Fed eyes the back nine, the course ahead grows more complex. This is not merely the halfway point—it is the start of a tougher stretch where precision matters, hazards multiply, and the margin for error narrows. How we navigate this stretch won’t just determine the score this round—it will shape the course we play going forward.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

June 28, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000