Highlights of the Week

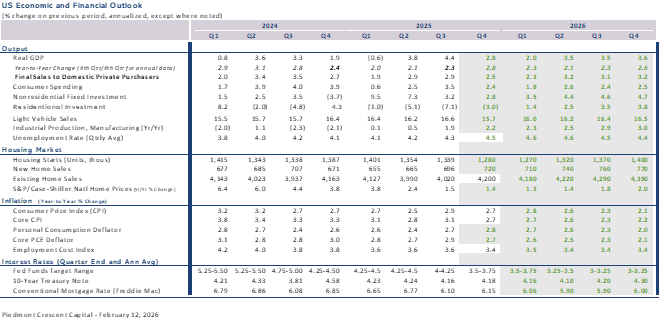

- January CPI cooled to 2.4% headline and 2.5% core year-over-year, broadly in line, with leading components pointing to further moderation into the second half of 2026.

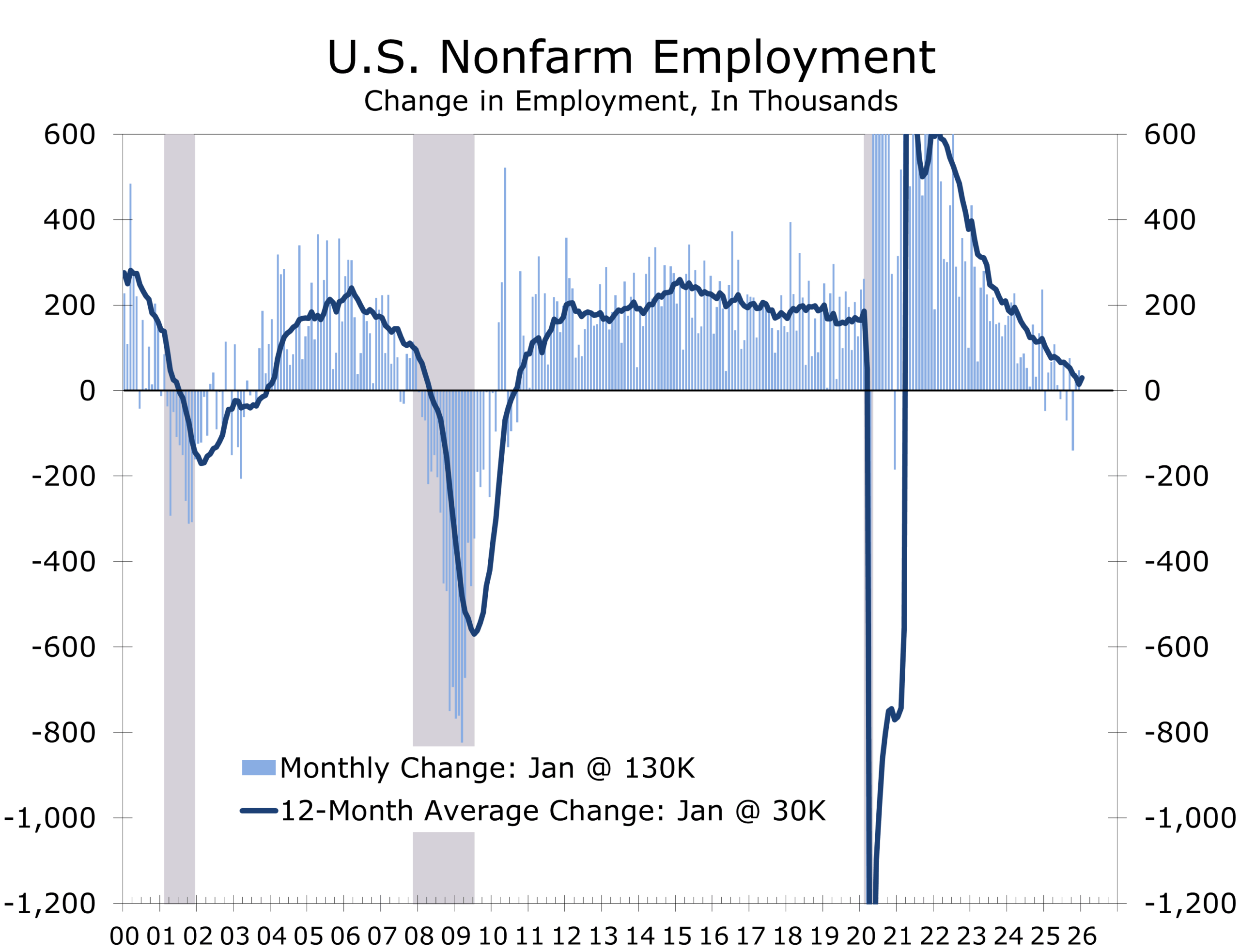

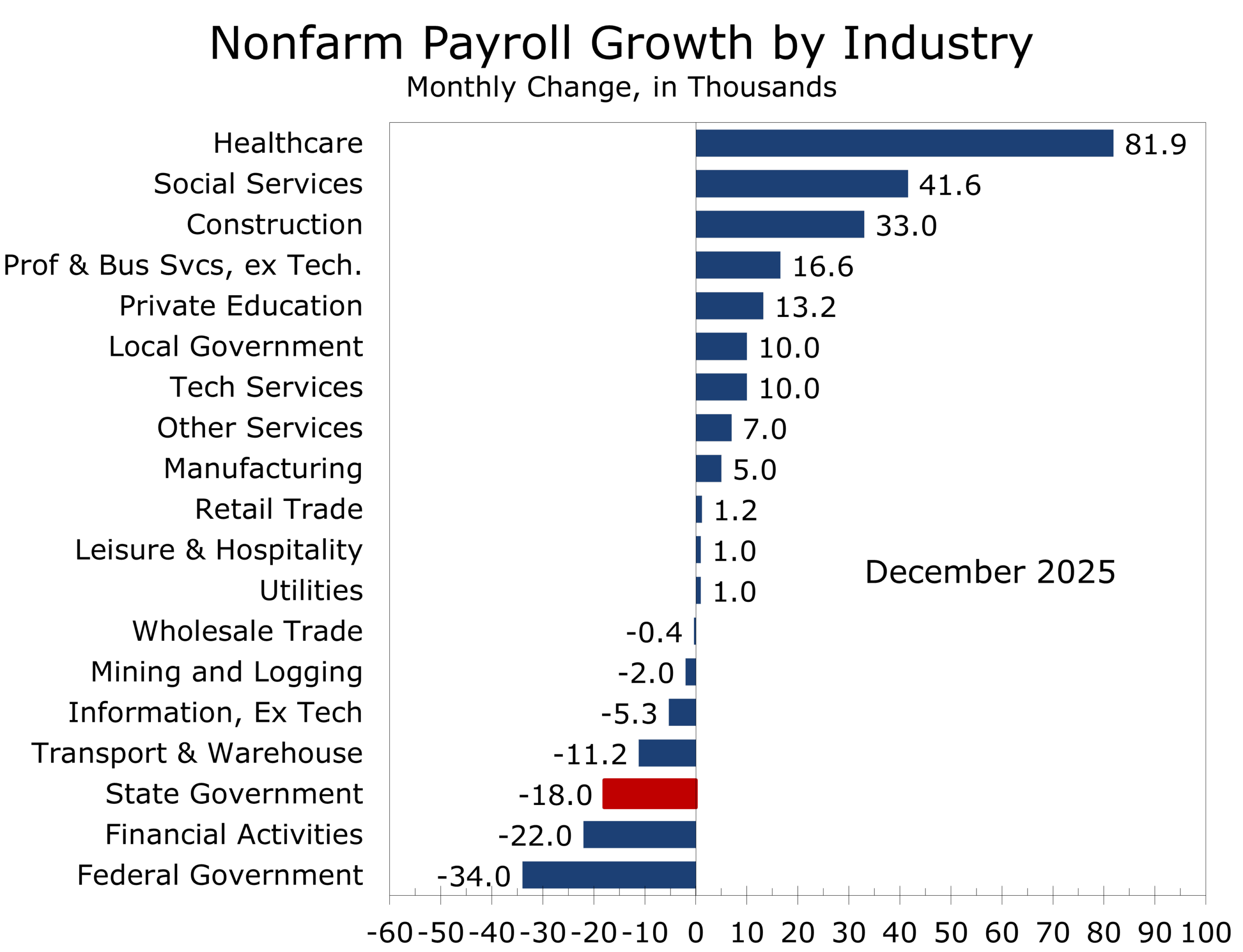

- Payrolls rose 130,000 in January, nearly double what we believe the underlying pace is. Private payrolls rose an even larger 172,000.

- Retail sales and housing softened but largely reflect weather distortions and payback from earlier strength rather than structural retrenchment.

- Markets are recalibrating from “limitless AI” to selective productivity gains, while Fed cut odds remain volatile but not urgent.

- Geopolitics is now a structural input into capital allocation, not merely a tail risk.

Stabilization, Green Shoots and a Lower Bar

The past week delivered textbook Goldilocks data (firmer employment, moderating inflation, and no visible credit stress), yet equities sagged and Treasury yields fell to multi-month lows. The divergence owes more to positioning and narrative fatigue than to macro deterioration.

Read in isolation, the employment report signals stabilization, not slowdown. January’s stronger-than-expected gains and annual revisions suggest the labor market is stabilizing earlier than anticipated. While job growth remained heavily concentrated in healthcare and social services, the overall diffusion index has stayed above 50 for three consecutive months, and the manufacturing diffusion index returned above 50, consistent with the recent upside in the ISM manufacturing survey.

One month does not make a trend. Should cyclical segments continue to rebound, we would revise our underlying job-growth estimate higher, from approximately 65,000 per month currently to approximately 75,000 in the first half of the year and potentially 90,000 in the second half. Manufacturing payrolls recorded their first gain in 14 months in January. Sustaining that improvement will require modest labor-supply relief, likely from some easing of immigration enforcement (as we expect) and higher participation among younger workers.

The labor market no longer needs 150,000 jobs a month to hold the unemployment rate stable. It needs between 50,000 and 75,000, and January easily cleared that bar.

The bottom line is that the breakeven pace of job growth has declined from a year ago. That lowers the threshold for maintaining a steady unemployment rate, but it also means the Fed may have less room to cut rates aggressively. We still expect easing later this year, but likely not to the extent or duration currently priced by markets.

A Cyclical Rebound vs AI-Related Compression

January’s 130,000 payroll gain, powered by a 172,000 rise in private-sector jobs, cleared a far lower bar than in prior cycles. With working-age population growth curtailed by demographics and reduced immigration, January’s job growth pulled the unemployment rate dipped to 4.3%, as new and re-entrants were absorbed. Other early cyclical green shoots were also evident: manufacturing added 5,000 jobs, temporary help services stabilized, average hours worked rose, and the unemployment rate.

Yet breadth remains strikingly narrow. Healthcare and social assistance drove approximately 95% of total gains (approximately 124,000 jobs), with most other sectors flat or negative. Ongoing heavy capital investment in AI infrastructure, advanced manufacturing, reshoring, and grid modernization continues to drive output while adding relatively few workers. AI adoption is directly displacing some labor demand without widespread layoffs, further compressing the sustainable pace of hiring.

The labor market is stabilizing, not broadly reaccelerating. Modest cyclical improvement is emerging atop a structural, productivity-driven foundation, but limited breadth and persistent AI-related restraint point to only modest upside. Downside risks to labor demand have eased while the potential for a cyclical rebound has increased.

Disinflation Broadens

January’s CPI report reinforces the disinflation trend. Headline inflation eased to 2.4 percent year over year and core inflation held at 2.5 percent. Energy prices declined during the month, helping suppress the headline figure, while shelter rose just 0.2 percent and continues to trend lower on a year-over-year basis.

Core goods inflation remains contained, with most tariff pass-through effects now behind us. Services inflation is still firmer than the Fed would prefer, but the breadth of pressure is narrowing. Inflation is no longer broad based. It is concentrated and gradually converging toward target.

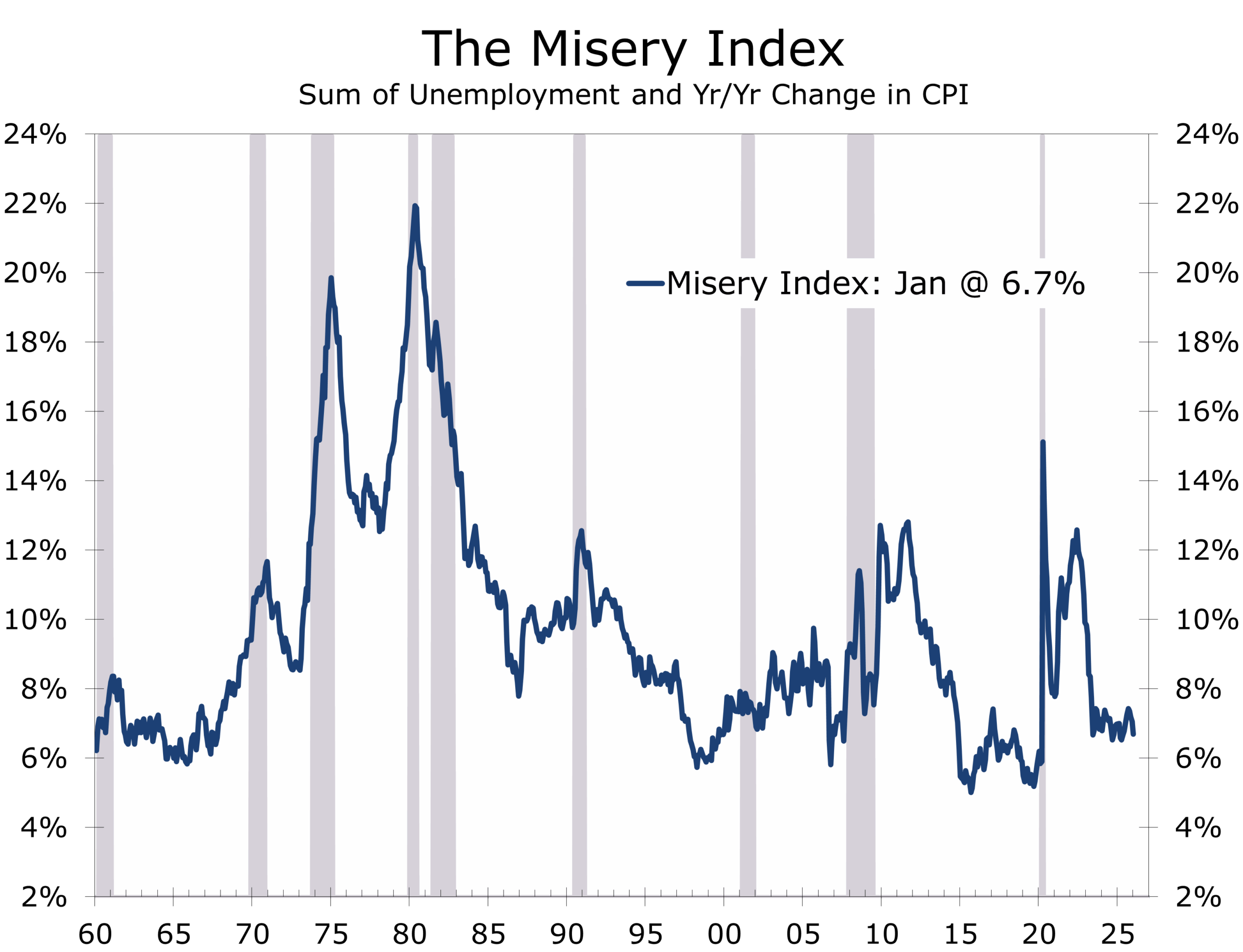

The Misery Index, defined as the unemployment rate plus inflation, has now fallen below where it stood when President Trump took office. Lower inflation and a stable labor market have materially reduced overall economic strain.

This gives the Federal Reserve flexibility, but not urgency. Rate cuts before mid-year would likely require clearer evidence of further disinflation. For now, policy remains positioned to hold steady throughout the first half of the year, with easing possible later if trends continue.

If sustained, the improved economic backdrop could begin to reshape expectations heading into the midterm elections. Sentiment tends to lag the data, but better fundamentals eventually matter.

Consumer and Housing: Weather, Not Weakness

Consumer spending softened at the start of the year, but the weakness appears more short-term oriented. Overall retail sales were flat in December and core retail sales fell 0.1%. Even after the cooldown, holiday retail sales turned in a solid performance, rising 3.7%. December’s drop reflects payback effects from earlier strength and harsh winter weather weighing on activity. Final demand remains supported by steady employment and easing inflation, limiting downside.

This looks like weather distortion and seasonal payback, not a demand pullback.

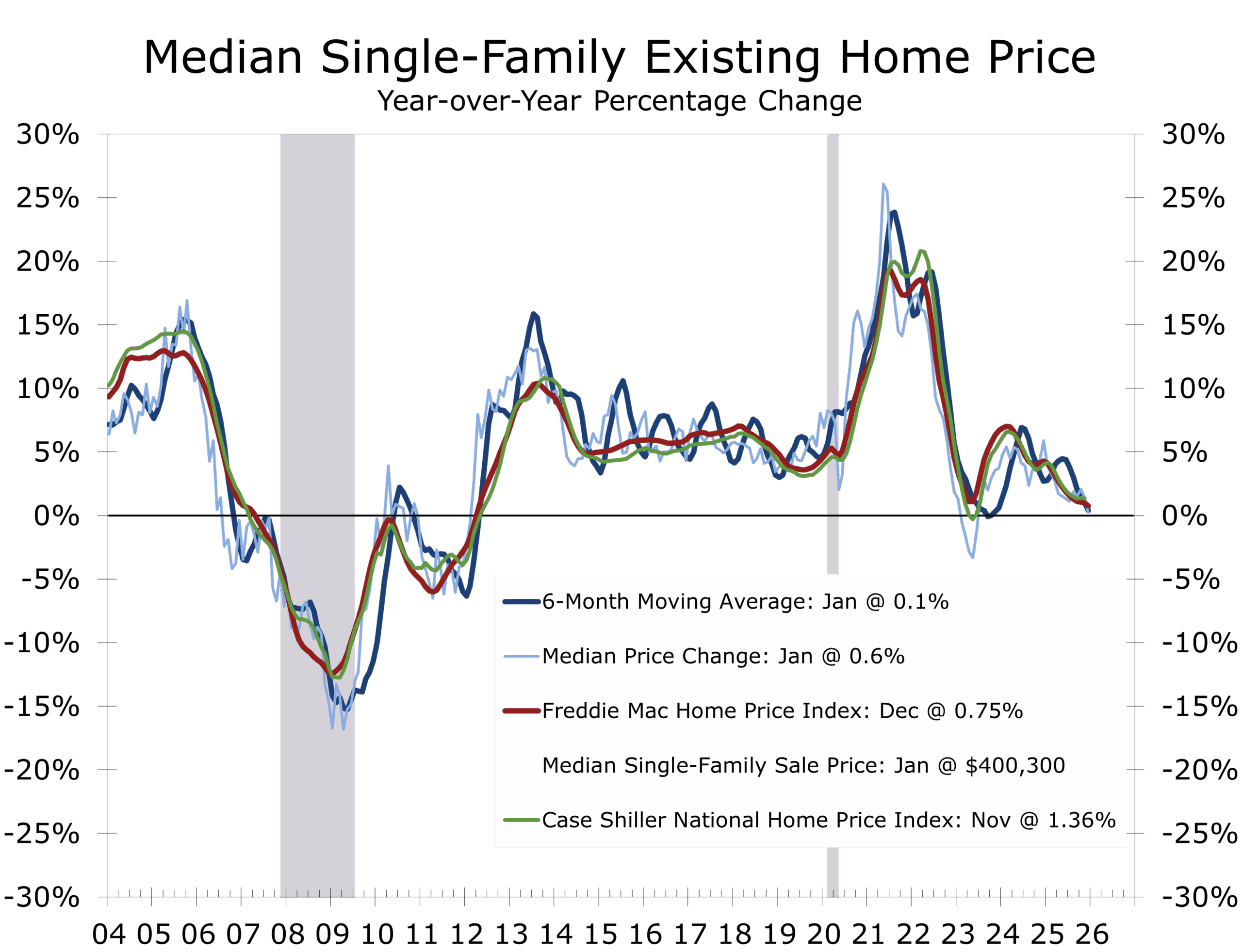

Housing activity also started 2026 on a weak note. Existing home sales fell 8.4 percent in January to a 3.91 million annual pace, well below expectations, with prior months revised lower. Harsh winter weather likely contributed to the decline, and tight inventories compounded the slowdown. For-sale supply slipped again in January and remains constrained, though inventory typically improves heading into spring.

Median home prices fell 2 percent and are up just 0.9 percent over the past year. As mortgage rates ease and labor markets stabilize, sales should gradually climb back. We are looking for a solid spring selling season and look for housing to add to economic growth in the second half of 2026.

Markets: Narrative Reset

Strong jobs plus softer inflation would normally lift equities and steepen yield curves. Instead, stocks weakened and Treasury yields declined. Recent volatility reflects a shift in market narrative more than deteriorating fundamentals. Despite encouraging jobs and inflation prints, investors are cautious about AI’s disruptive potential, with headline tech and broader indexes struggling to trend higher amid sector rotation and valuation pressures.

Markets are shifting from “limitless AI” to “measured productivity,” and the transition is inherently volatile.

Narrative fatigue has replaced 2025’s “limitless AI” optimism with a more selective “measured productivity” stance, as market participants debate which industries will benefit or be disrupted. At the same time, tighter labor supply driven by slower immigration and aging demographics is lowering the breakeven pace of job growth, complicating the narrative about job destruction.

Funding Windows in a Range-Bound Rate Environment

With the Fed likely on hold in the first half and easing only probable in the second half, funding costs remain range-bound but elevated. Upside labor surprises could push front-end yields higher and flatten the curve again, while downside surprises could pull rates lower and create opportunities to lock in low rates. We expect to see some payback for January’s outsized gain. The true underlying pace of job growth will likely be reflected in the average for the first three months of the year.

If disinflation continues and labor stabilizes near breakeven, the Fed gains room to normalize policy without crisis. But if job openings continue to fall and AI adoption accelerates hiring restraint, the downside risks to growth could climb quickly. In that event, credit spreads would likely widen.

Locking in duration opportunistically remains prudent. Hedge labor and commodity inputs where possible. Monitor openings and hiring rates more than payroll headlines, as lower turnover is a major factor restraining hiring.

Source: National Association of Realtors, Freddie Mac and S&P Cotality

The Piedmont Perspective – A Conflict of Visions: Munich 2026 and the Limits of Design

The Munich Security Conference made clear that geopolitics is no longer episodic volatility or a distant tail risk. It has become a structural input into markets.

In his classic work A Conflict of Visions, economist and philosopher Thomas Sowell contrasted two fundamental worldviews: the “unconstrained” vision, which holds that institutions, markets, and goodwill can gradually reshape incentives and diminish the role of hard power, and the “constrained” vision, which emphasizes enduring limits and trade-offs. Europe’s post-Cold War approach largely reflected the unconstrained vision. Russia’s invasion of Ukraine shattered that assumption, exposing not a lack of resolve but a profound shortfall in capacity: energy dependence, depleted munitions stockpiles, and atrophied defense-industrial bases built on decades of underinvestment.

Energy policy had quietly become security policy. Ambitious climate goals accelerated the retirement of coal and nuclear capacity before alternatives were secured, leaving Russian natural gas as the primary bridge fuel. When the bridge was cut, trade-offs could no longer be deferred: higher costs, weakened competitiveness, and constrained strategic options arrived all at once.

.

For investors, this is not abstract philosophy. Rising defense budgets are reshaping industrial policy across Europe. Energy diversification and reshoring are rewiring supply chains. Sustained fiscal commitments to security are influencing real yields, currency dynamics, and capital allocation.

Geopolitics has moved from tail risk to a key balance-sheet variable.

Durable strategy demands both aspiration and constraint. Markets ultimately reward capacity and production, not intentions or rhetoric.

Parting Thoughts

The macro backdrop remains constructive. Inflation is easing. Labor is stabilizing near a lower breakeven threshold. Housing appears to be bottoming. Business investment remains firm.

The risks sit in two places: labor demand erosion from AI or declining job openings, and market volatility driven by shifting narratives rather than fundamentals.

The signal remains steady. The sentiment is shifting. And the first green shoots of stabilization are visible—but still tentative and fragile.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

February 16, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000