Highlights of the Week

- Economic Data Recap: Industrial production rose on autos and defense while import prices climbed on dollar weakness and firmer global goods prices; sentiment weakened. These signals point to slowing growth with lingering inflation risk.

- Retail Sales: Three straight months of gains put Q3 consumption growth on track north of 2%, providing upside risk to our Q3 GDP forecast. Stronger spending may complicate the Fed’s easing path.

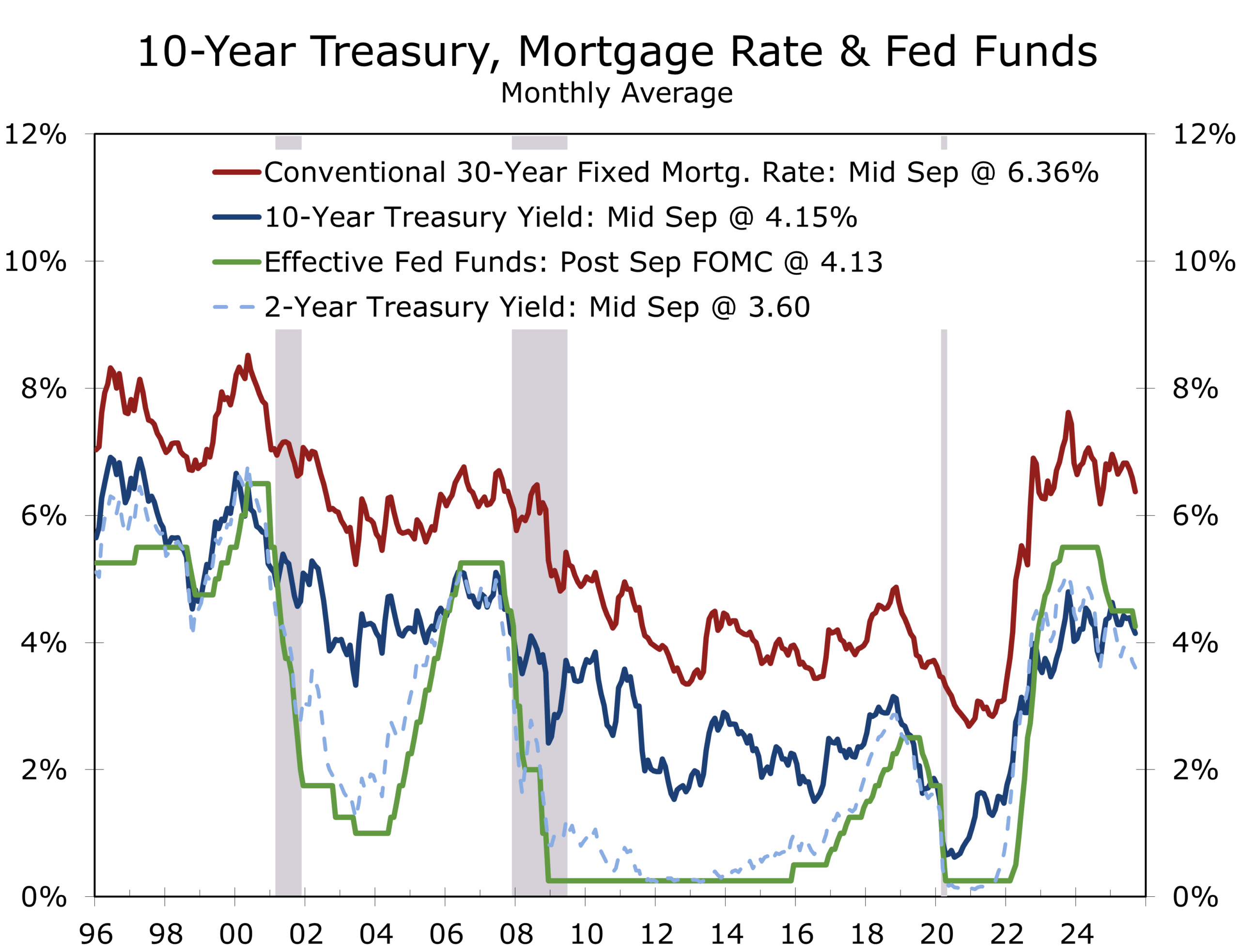

- Markets: Yields eased, the dollar firmed, equities pressed higher. Markets are betting on further Fed easing.

- Fed Policy: The Fed cut rates 25bps last week and signaled more easing ahead. Our view: the Fed can accomplish more by doing less—cutting less than markets expect while anchoring confidence.

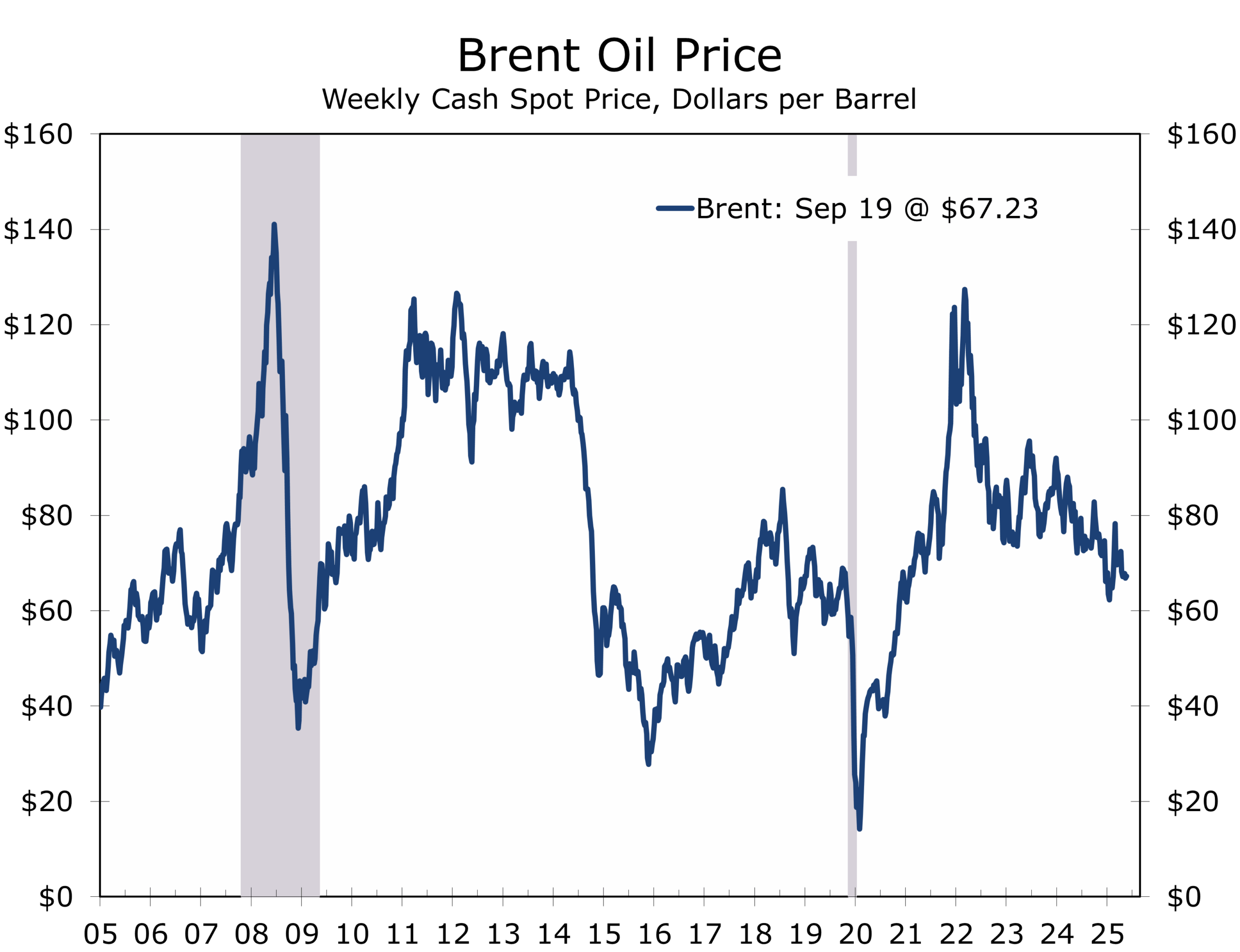

- Energy & Commodities: Brent crude remains capped near $66; gold and precious metals are firming on safe-haven demand and a softer dollar. FX markets show waning U.S. growth premium as investors rotate toward higher-yielding EM currencies.

- UN General Assembly: Fractures on Gaza, Ukraine, and climate finance highlight weak multilateral consensus. The pullback in U.S. leadership has left a void, making solutions to pressing global problems harder to achieve.

- Israel–Qatar Strike: The strike continues to resonate throughout the Middle East, expanding the conflict’s footprint, complicating Gulf unity, and raising energy security risks.

- This Week: New Home Sales on Wednesday, Q2 GDP (third estimate) Thursday; Personal Income & Outlays and the PCE deflators Friday, along with final September Consumer Sentiment.

- Trump’s Tuesday UN General Assembly Address: Will be closely watched for signals of tariff escalation and NATO burden-sharing. Trump’s rhetoric comes amid a leadership vacuum, and markets are weighing whether the U.S. is reasserting leverage or stepping further away from consensus-building

Economic & Market Recap

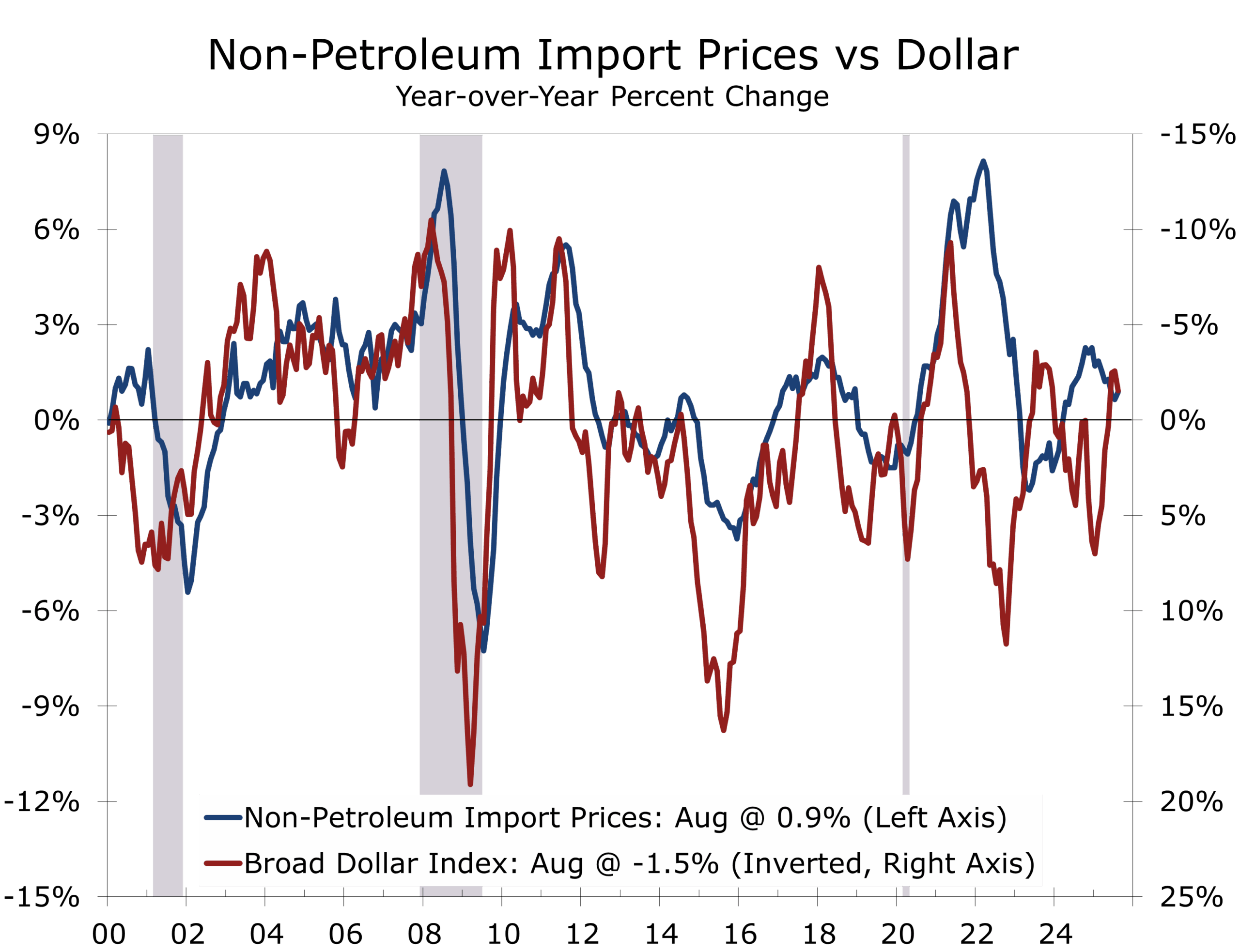

The past week’s data underscored the combination of resilient production and stubborn cost pressures. Industrial production jumped, thanks largely to auto output, underscoring that U.S. manufacturing is not collapsing under high rates. Import prices edged higher, reflecting dollar weakness and firmer global goods prices. While tariffs remain an important policy risk, they do not directly feed into the import price index, which measures values before duties are applied. The upward move nonetheless signals that a softer dollar could complicate the disinflation narrative. Consumer sentiment slipped in early September—households see risks in the job market and are less confident about income growth.

The Fed is being asked to ease policy in an environment that is not fully benign. Growth is slowing, but exchange-rate effects and global price pressures are limiting the pace of disinflation. That explains why Treasury yields fell, the dollar strengthened, and equities still found room to rally—markets are betting that the Fed has room to cut, but the path will likely not be as smooth as implied by the Summary of Economic Projections median points.

Retail Sales: A Stronger Consumer Pulse

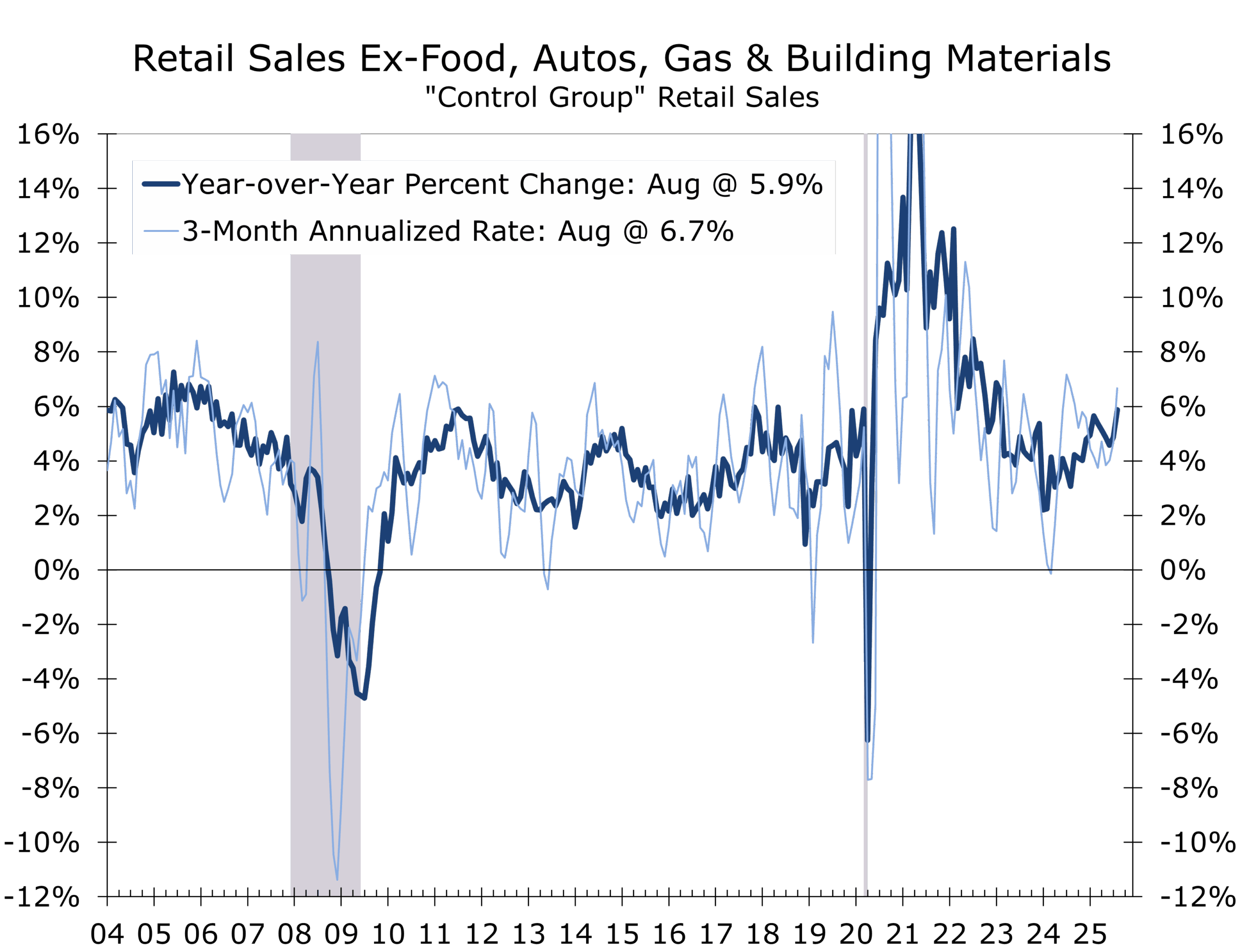

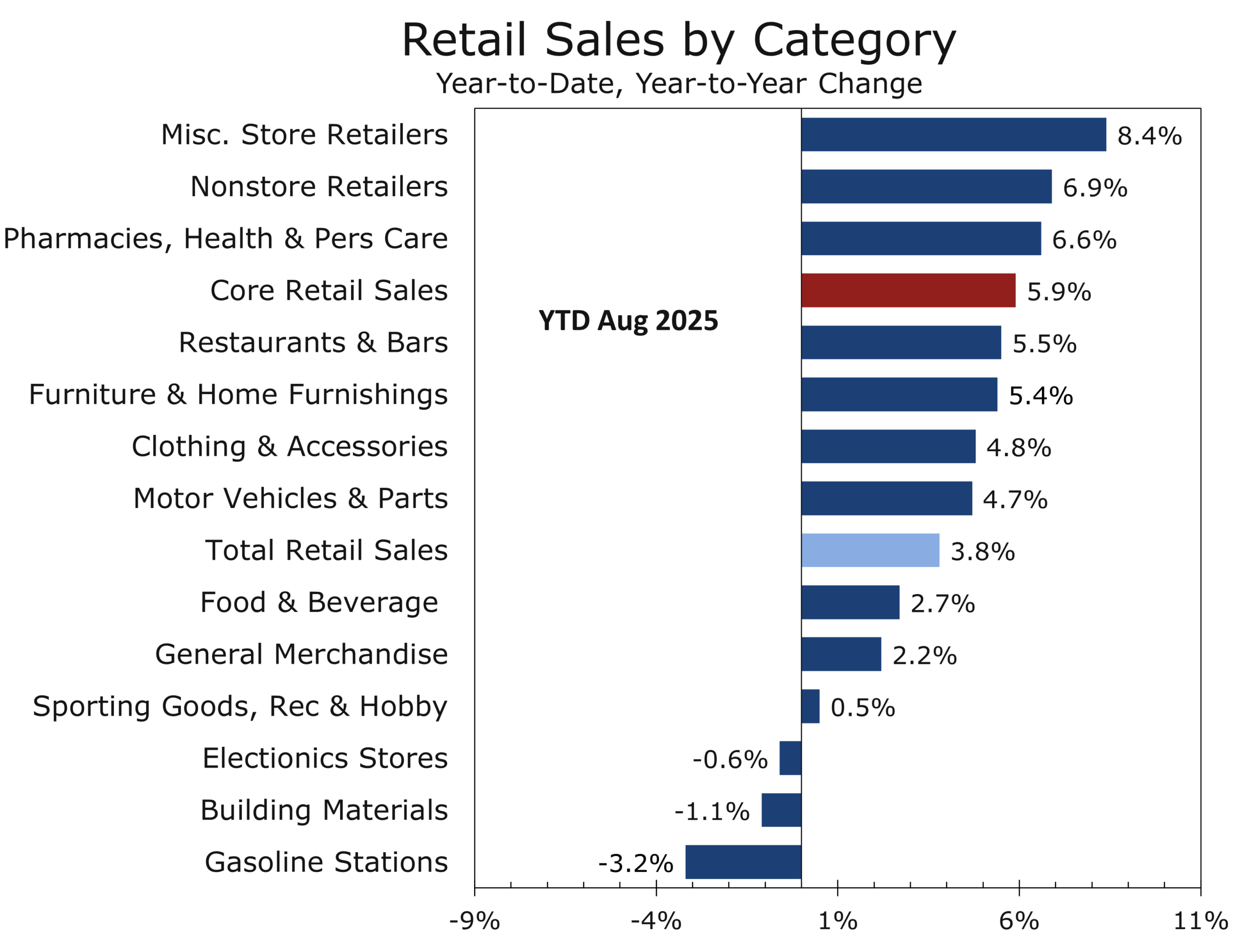

August retail sales surprised to the upside, with headline sales rising 0.6% and core control sales up 0.7%, both well above expectations. July was revised higher to a 0.5% gain, following June’s outsized 0.9% increase—underscoring that momentum has carried through the summer. Gains were broad-based: motor vehicles and gasoline each rose 0.5%, while non-store retailers led with a 2% jump. Clothing sales advanced 1%, signaling a strong back-to-school season and offering a positive precursor to holiday spending. Real core retail sales likely climbed 0.5% in August and are running at a robust 5.5% pace on a three-month annualized basis.

The recent string of buoyant retail sales reports provide upside risk to Q3 GDP forecasts.

This resilience has important implications for the broader economy. Consumption had been a soft spot earlier this year, weighed down by weaker discretionary categories and fading sentiment. Three straight months of gains, however, suggest spending has rebounded more quickly than expected from the midyear slowdown. Consumers may also be making up for purchases deferred in the spring, when the economy appeared more fragile.

The stronger retail sales data also provide upside risk to Q3 GDP. While part of the recent strength reflects higher goods prices as tariffs and import costs filter through, real spending is still advancing. The rebound in discretionary categories such as dining and recreation highlights that higher-income households—who account for the bulk of spending—remain in solid shape, even as lower-income households face pressure from a softening labor market and higher living costs.

For the Fed, the message is nuanced. The resilience of consumer spending will bolster confidence that growth is holding up even as labor market conditions cool, reinforcing the case for a gradual approach to easing to support the labor market. At the same time, stronger demand complicates the disinflation narrative, particularly if robust consumption sustains pricing power in services. Markets may need to temper expectations for the pace of rate cuts if activity data continue to surprise to the upside.

This is another reason why the Fed may accomplish more by doing less—signaling support while avoiding the risk of fueling demand that is already proving resilient.

Accomplishing More by Doing Less

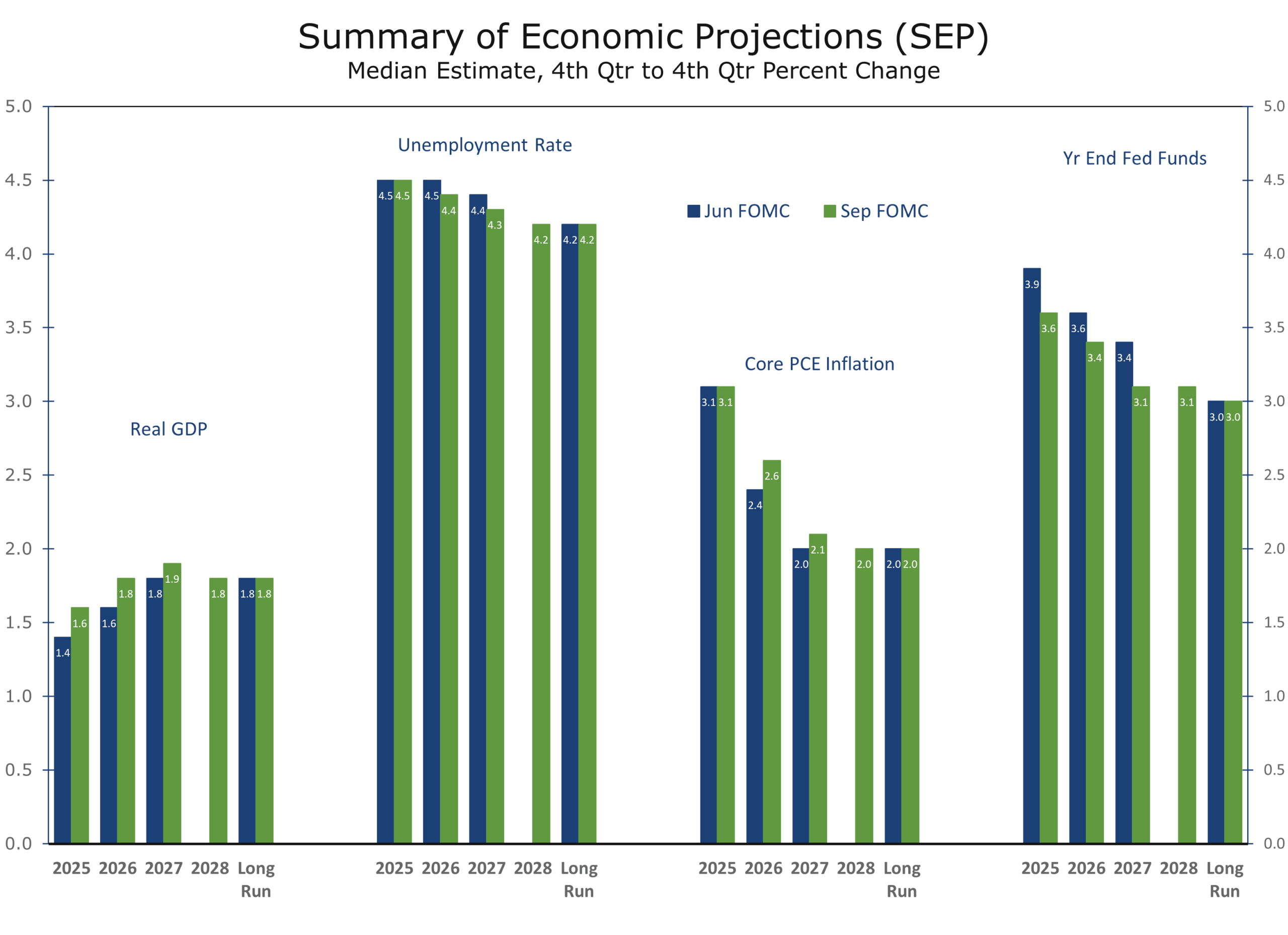

The Fed cut the funds rate by 25 basis points last week, lowering the range to 4.00–4.25%. Chair Powell described the move as a “risk management cut,” stressing that downside risks to the labor market had risen and that the Fed did not want conditions to weaken further. The statement added dovish language that echoed September 2024, when the Fed delivered the first in a series of three cuts. Markets took this as a signal that additional easing is likely, with October and December both in play.

Yet the so-called “dots” tell a more complicated story. While the median projection implied three cuts this year, the distribution was scattered, particularly for 2026 and beyond. This wide dispersion highlights the lack of consensus inside the Committee and underscores the danger of markets pricing in too aggressive a path.

Dots are scattered—the financial markets risk overestimating the path of cuts.

Our view is that the Fed may be able to accomplish more by doing less. Signaling a long series of cuts risks pushing long-term yields higher rather than lower, particularly if investors perceive the Fed is leaning into political winds at a time when headline inflation is rising. A steadier approach—cutting less than the market expects, while reaffirming the Fed’s dual mandate—would anchor confidence in both bond and currency markets.

Looking further out, lower interest rates should allow conditions to firm later this year and into early 2026, bolstering home sales and sales of light vehicles and other big-ticket items. This improvement should broaden as uncertainty surrounding trade and immigration policy subsides, supporting a more durable recovery. Futures positioning already reflects heightened conflict between speculators and hedgers, which suggests volatility will remain high. But if the Fed avoids over-committing, it can preserve credibility while still fostering a recovery that builds momentum into 2026. Moreover, postponements of projects in the aftermath of Liberation Day are increasingly coming back on track, producing a tail wind capex in 2026.

Energy, Commodities, and Exchange Rates

Brent crude remains capped near $67, weighed down by OPEC+ supply adjustments and weak demand. The muted risk premium suggests markets are not yet pricing in broader contagion from Middle East conflict, though Israel’s strike in Qatar could quickly elevate LNG risks given Doha’s pivotal role in global exports.

The dollar has eased following the Fed’s “risk management” cut, as narrowing rate differentials encourage flows into higher-yielding emerging market currencies. The euro has traded with surprising resilience, occasionally acting as a quasi-safe haven, while the yen remains under pressure from Japan’s leadership transition but should stabilize once political uncertainty clears.

The broader backdrop is the U.S.–China trade standoff. Tariffs remain disruptive, but sanctions are now a realistic risk, threatening to fracture global supply chains within a year. Asia’s advanced economies are most exposed, but U.S. reliance on Taiwanese semiconductors highlights domestic vulnerability. This underscores the importance of industrial policy, such as the government’s Intel stake, to mitigate supply chain risk while ensuring taxpayers capture part of the upside. A deal on the U.S. operations of Tik Tok also appears to be close.

UN General Assembly

The UN General Assembly showed how fractured global governance has become. Calls for a Gaza ceasefire, pleas for reconstruction, Ukraine funding, and climate finance all vied for attention—but little consensus emerged. The pullback in U.S. leadership has created a void, leaving a vacuum where solutions to the world’s most pressing problems once had an anchor. Without Washington pushing for compromise, competing blocs are left to pursue narrower interests, and the space for consensus has narrowed considerably.

The pullback in U.S. leadership has left a void that President Trump may address in his speech.

Markets rely on institutions like the UN General Assembly to reduce uncertainty. When consensus breaks down, geopolitical risk premia rise. Investors should expect policy to be set more by ad hoc alliances and bilateral deals than by broad-based agreements, with volatility in trade, sanctions, and aid flows likely to persist.

Israel–Qatar Strike Fallout

Israel’s targeted strike on Hamas leadership in Qatar is not just a tactical event—it expands the geographic footprint of the conflict. Qatar has served as a key intermediary in ceasefire talks and hosts vital U.S. military bases. Whether the strike eliminated senior Hamas figures remains uncertain, but it has already opened the door to greater international criticism of Israel.

The strike comes at a moment when a growing number of countries are moving to formally recognize a Palestinian state. That momentum underscores Israel’s increasing diplomatic isolation, complicating U.S. efforts to manage alliances across Europe, the Gulf, and the developing world. Recognition does not alter the battlefield in Gaza, but it shifts the diplomatic balance, making it harder to build consensus around ceasefire terms or postwar reconstruction.

For investors, the risks extend well beyond the conflict zone. The strike raises the probability of heightened energy price volatility, weaker OPEC+ cohesion, and greater uncertainty in Middle East capital flows. It is a reminder that the war’s economic consequences are not confined to Gaza and that shifting diplomatic alignments could keep geopolitical risk premia elevated across energy and currency markets.

Trump’s UN General Assembly Address Preview

Former President Trump is expected to deliver a muscular address on Tuesday, emphasizing tariffs, NATO burden-sharing, and America’s leverage in global trade. His return to the UN General Assembly stage comes at a moment when the pullback in U.S. leadership has already created a void, leaving international institutions struggling to find consensus on Gaza, Ukraine, and climate finance.

Markets will be parsing not only the words but the direction of policy. Any hint of renewed tariff escalation could unsettle equities, strengthen the dollar, and pressure global risk assets. Stronger calls for NATO contributions could shift defense spending patterns in Europe, with implications for transatlantic capital flows. Trump’s rhetoric will be read as either an attempt to reassert U.S. leverage or as a further sign that Washington is less interested in leading through multilateral consensus. Either way, investors should be prepared for volatility emanating directly from the podium.

Outlook for the Week

This week brings data that will directly influence the Fed’s October meeting.

- Wednesday: The Census Bureau reports on new home sales for August, which may show some benefit from modestly lower mortgage rates. Mortgage rates have since fallen sharply, which should lift mortgage applications in the MBA report—a good sign for sales in coming months.

- Thursday: Advance durable goods orders for August will be reported along with the Commerce Department’s third estimate of Q2 GDP and revised corporate profits. Initial unemployment claims will also be released.

- Friday: The August Personal Income and Outlays report, including the PCE deflators, followed later by the final September University of Michigan Consumer Sentiment survey.

A softer PCE print would strengthen the case for another rate cut, but the Fed will be cautious not to overpromise. The risks of miscommunication are high—if markets expect too aggressive a path, yields could paradoxically rise, undermining the very easing the Fed seeks

Final Thought: Industrial Policy at a Crossroads

The government’s non-voting stake in Intel, recently boosted by Nvidia’s $5 billion investment, marks a notable shift in U.S. industrial policy. Unlike past subsidies, this approach allows taxpayers to share in the upside of strategic investments while avoiding the potential conflicts of day-to-day operational control.

The model seeks to align national security goals with free-market incentives. It channels public resources into critical sectors like semiconductors but does so with transparency and without crowding out private capital. Federal assistance to private industry is nothing new, nor is capturing upside. The Treasury’s investments in major financial institutions during the Global Financial Crisis yielded substantial profits, while support for automakers produced net losses. The Nvidia–Intel deal takes the framework further: private capital is following public commitments, creating scale and momentum in a sector central to U.S. competitiveness.

Still, the risks cannot be ignored. Politicization, distorted competition, and challenges in unwinding government stakes are real concerns. The discipline of markets must not be replaced by the discipline of politics.

From a free-market perspective, the Intel stake represents a pragmatic middle path—using non-voting shares to avoid heavy-handed intervention while ensuring taxpayers benefit when strategic bets succeed. If applied only in sectors where genuine market failures exist, this model could enhance U.S. competitiveness without abandoning the principles of open markets.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

September 22, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000