Shifting Tides: Slower Growth, Mounting Risks

Highlights of the Week

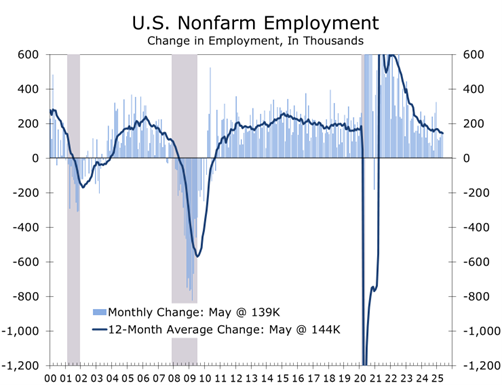

- May payrolls rose a moderate 139,000 and were revised lower by 95,000 for prior months.

- Labor force participation and prime-age employment ratios both declined.

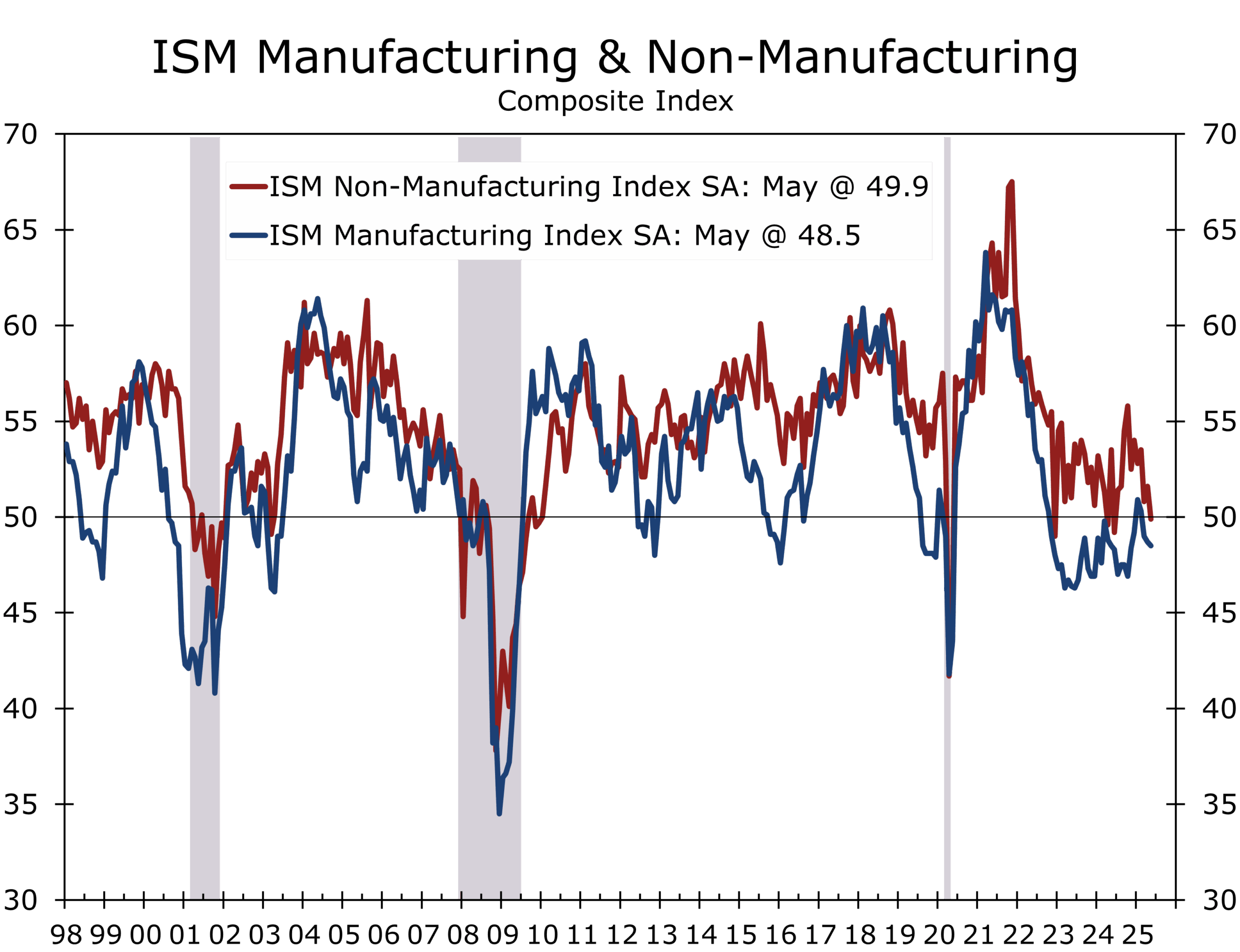

- ISM manufacturing and services indexes slipped into contraction territory.

- Imports collapsed in April, temporarily boosting Q2 GDP estimates.

- Romania swings right, Australia

- Vehicle sales fell sharply in May, signaling post-front-loading fatigue.

- Initial jobless claims climbed to the highest level since October.

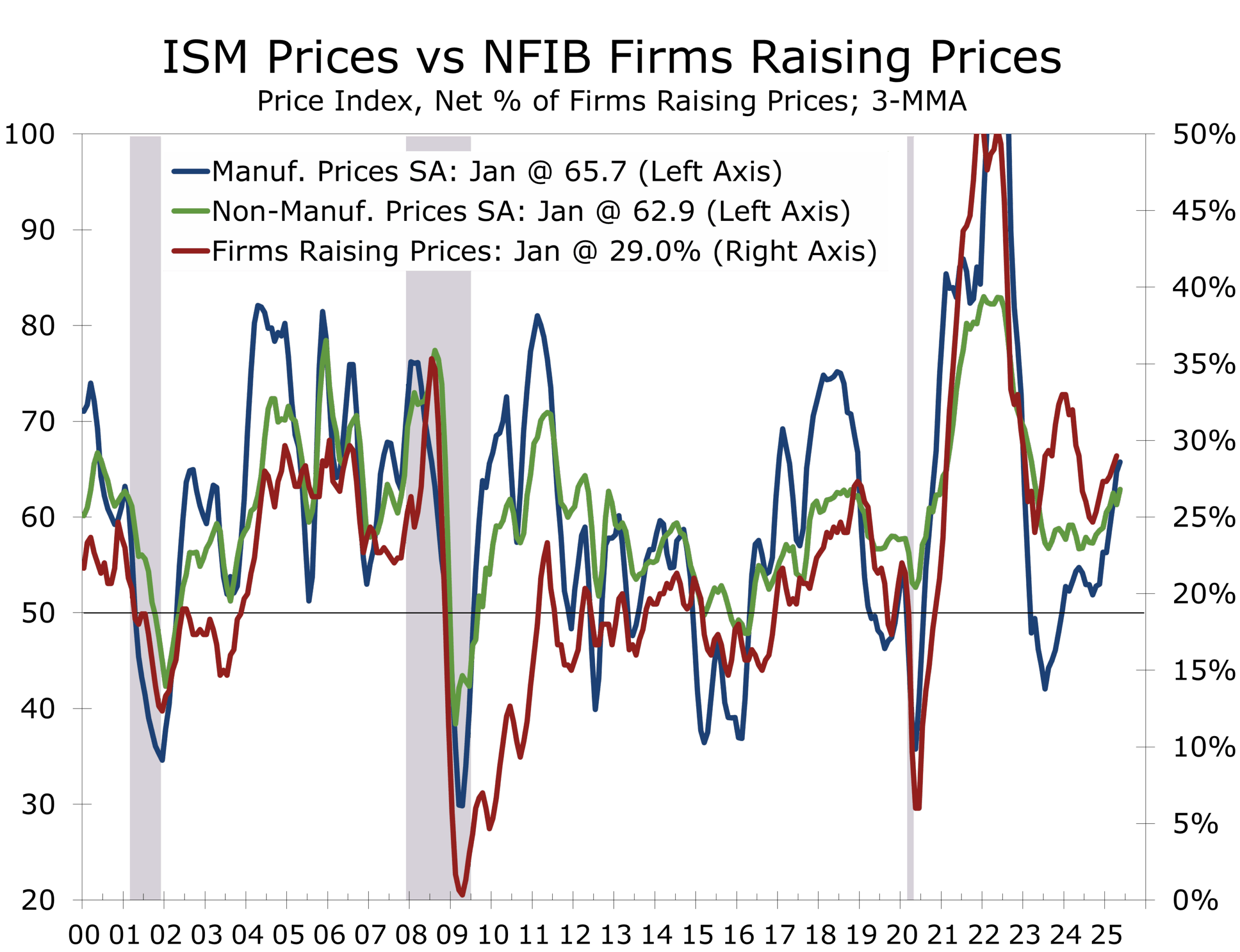

- Tariffs are increasingly driving cost pressures, disrupting orders, and clouding visibility, paralyzing decision making.

- Ukraine’s deep strike into Russian territory altered the strategic balance.

- Markets continue to price in a September rate cut despite continued Fed caution.

The May employment report showed the labor market is losing momentum and raised hopes that the Fed will cut rates a little sooner and by a little more than was expected earlier. Nonfarm payrolls rose by 139,000 in May—slightly below the 12-month average—and downward revisions shaved 95,000 jobs off the previous March and April estimates. Job growth remains concentrated in a narrow range of industries, with health care and hospitality accounting for the bulk of job gains.

Federal payrolls tumbled by 22,000 in May and are down 59,000 year to date. That is a sharp contrast with expectations, particularly given that court rulings have paused formal layoffs. The pullback is driven by attrition and an ongoing hiring freeze, as well as some catch up in the data for jobs cut earlier. We look for larger declines in federal payrolls during the second half of this year, as agencies do not replace retiring staff.

Real private domestic sales offer a clearer view of underlying economic momentum.

While the unemployment rate was unchanged, the household survey was weaker than that headline would suggest. The labor force participation rate fell 0.2 points, and the employment-population ratio fell 0.3 points. Prime-age participation also slipped, suggesting some job seekers may have left the work force. Tightening immigration is also likely playing a role. The employment data are volatile, but the weakening trend is becoming harder to dismiss. Jobless claims have climbed in recent weeks, and the four-week moving average now stands at its highest level since October.

Tariffs Are Increasing Costs and Reducing Demand

Tariff-related distortions continue to ripple through the economy, obscuring signals and intensifying uncertainty across supply chains. The April trade report revealed a collapse in goods imports—the sharpest monthly decline since the pandemic—with particularly steep drops in pharmaceuticals, gold, and motor vehicles. Imports from China alone have fallen 40% year to date, in response to tariff rates that exceeded 100% in April before being modestly scaled back. That dramatic import pullback sharply reduced the U.S. trade deficit, providing a temporary lift to Q2 GDP through a narrower trade deficit. The Atlanta Fed GDPNow forecast for Q2 is currently at 3.8%. The underlying details tell a less encouraging story: final sales to private domestic purchasers have softened, and investment in equipment and structures is losing momentum.

Businesses are increasingly absorbing cost pressures at the margin, wary of passing along price increases in a political environment where “inflation” remains a flashpoint. With tariff-related costs mounting, particularly in sectors reliant on imported components or finished goods, many firms are turning inward to preserve margins. That means spending cuts, headcount reductions, and deferred investment. The most immediate response has come in the form of hiring freezes, reduced hours, and selective layoffs, as noted in the latest Beige Book and ISM surveys.

Retailers and manufacturers are reporting narrower margins and declining order volumes. The reluctance to raise prices stems less from competition than from consumer resistance, political scrutiny, and the risk of drawing unwanted attention—potentially even a presidential callout. With inflation expectations rising and actual inflation slowing, businesses are caught between rising input costs and softening demand, with no straightforward way to pass costs along.

The strain is particularly evident in durable goods. Light vehicle sales fell to a 15.6 million-unit annualized pace in May, down from 17.3 million in April and 17.8 million in March, as the tariff-driven front-loading of demand faded. Inventories are tightening, replacement costs are climbing, and with higher payments and fewer incentives, consumers are pulling back. Even areas that had been showing some resilience, like home furnishings and appliances, are now seeing volumes decline. That slowdown is likely to deepen this summer, especially in discretionary sectors.

Firms that once had pricing power are now shifting to a more defensive stance, prioritizing cost control over growth. Business confidence is retreating broadly—more sharply than at any time since the pandemic—with tariff uncertainty front and center. Unless there’s movement on trade policy or the budget negotiations, capital spending and hiring are likely to slow further in the months ahead.

A Strategic Shift in Ukraine Raises the Stakes

Kyiv’s long-range drone strikes on Russian airbases—dubbed Operation Spiderweb—may mark a pivotal moment in both the war and global security. The successful targeting of up to 41 high-value aircraft, including nuclear-capable bombers and early-warning systems, stands as one of the most significant asymmetric attacks in modern warfare. The damage—potentially over $7 billion—was notable, but the message was louder: Ukraine now has the capacity to strike deep into Russian territory using low-cost, domestically produced technology. The rapid follow-on strike on the Kerch Bridge only reinforced that message.

Ukraine’s surprising and effective strikes deep into Russia are a potential game changer.

These surprising and effective attacks are a potential game changer. For Russia, they reveal alarming vulnerabilities in its air defense and raise doubts about second-strike credibility, escalating the risk of retaliation. For global observers, they highlight the growing threat posed by scalable, decentralized warfare technologies—whether deployed by states or non-state actors. Markets have largely shrugged off the news, treating it as isolated, but that complacency may not last. Ukraine’s increasing tactical reach, combined with Russia’s declining strategic depth, suggests the conflict is entering a more volatile phase with greater tail risks.

The timing of the strikes was no accident. They came just before a new round of talks in Istanbul, signaling Kyiv’s stronger bargaining position. Though the talks produced little, Moscow’s decision to attend—just 48 hours after a major strategic blow—suggests it may be reassessing the cost of a prolonged war. Still, the path forward is fraught. If Putin sees his credibility eroding, the risk of sharp escalation—from large-scale retaliation to symbolic tactical strikes—will rise. Policymakers and investors should not underestimate the instability that could follow if the Kremlin feels boxed in.

Foreign exchange markets remain volatile amid diverging central bank policies and shifting capital flows. The dollar has softened notably in 2025, reversing much of its post-election rally, though it remains supported by interest rate differentials and safe-haven demand. Softer U.S. data and rising fiscal concerns have capped its upside and increased upside and downside risks. The euro has gained modestly as the ECB eases cautiously, while the yen remains under pressure from persistent yield gaps, despite growing intervention risks.

Looking Ahead: The Signal Is Shifting

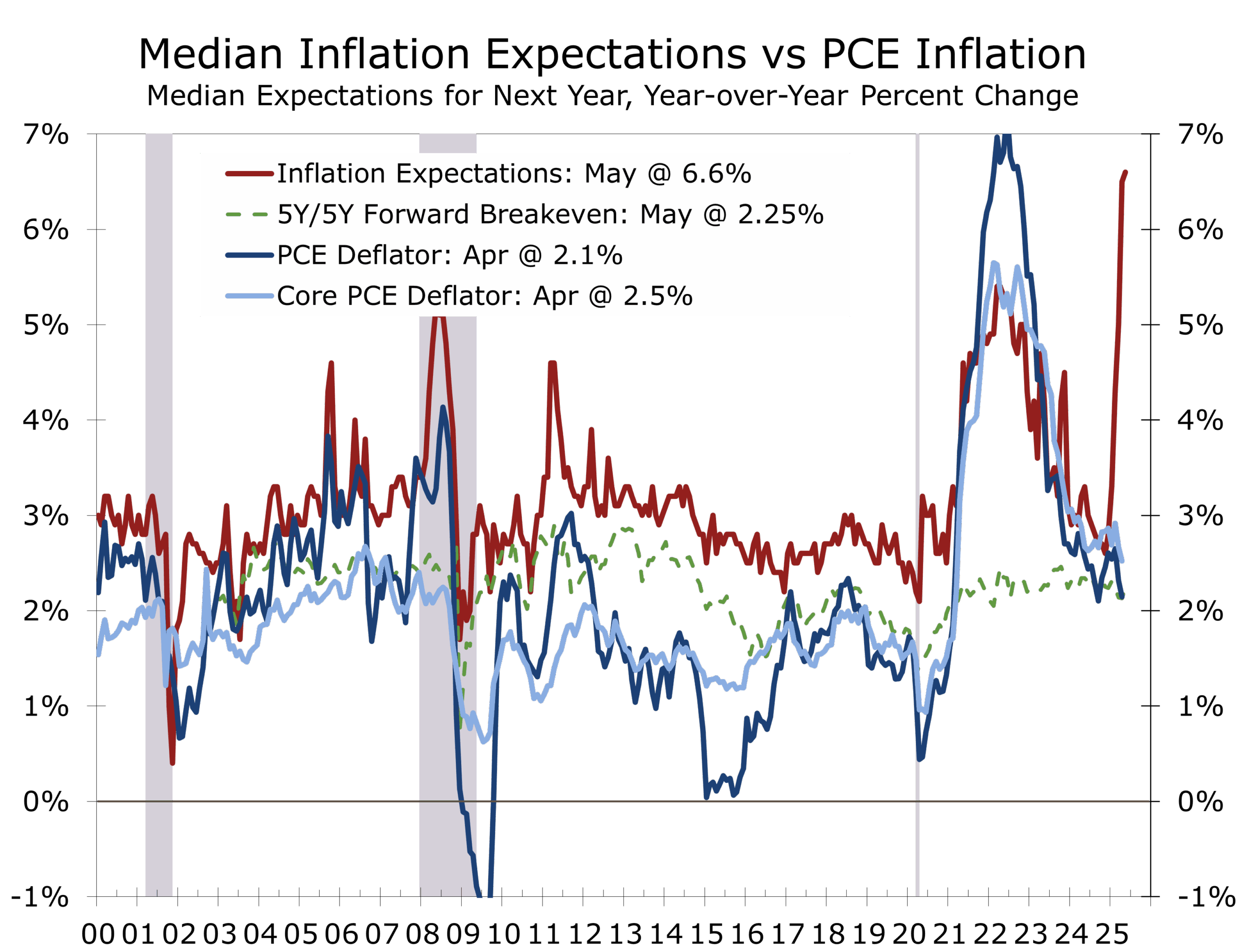

Markets remain focused on inflation and monetary policy. With PCE inflation drifting lower and job growth softening, investors are pricing in a September rate cut. But the Fed has given no signal nor hinted what would trigger that signal. Policymakers remain in wait-and-see mode, watching how tariffs impact inflation expectations and supply chains.

The next round of data will be critical. The May CPI and PPI reports are due Wednesday and Thursday, followed by preliminary consumer sentiment on Friday. We expect the CPI to rise modestly but watch for signs of a further slowdown in shelter inflation and consumer durables. Also look for slight dip in inflation expectations and look what small business owners say about rising costs and their ability to pass them on.

The Week Ahead:

- Monday: Wholesale Inventories (April)

- Tuesday: NFIB Small Business Optimism (May)

- Wednesday: CPI (May), FOMC Rate Decision & Press Conference

- Thursday: Jobless Claims, PPI (May)

- Friday: University of Michigan Consumer Sentiment (June, prelim)

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

June 8, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000