Highlights of the Week

- Q3 GDP printed a robust 4.3% annualized pace, driven by strong consumer spending and AI-related investment.

- The labor market looks stable on the surface, with initial claims at 214k, but lower turnover and cautious hiring point to a more nuanced backdrop.

- Markets are pricing a gradual Fed easing cycle following the recent 25bp cut to 3.5%–3.75%, with CME data signaling a slow-and-steady approach.

- Silver and gold shone brightly, like a familiar holiday tune, highlighting a shift toward hard asset hedging amid supply concerns and expectations of rate cuts.

- Geopolitical tensions remain front and center, with developments in Ukraine, the Middle East, and Taiwan underscoring a world that is anything but quiet

- 2025 is ending the way many past years have: optimism in the tape, anxiety in the headlines, and history reminding us that “quiet” is usually just a comma, not a period.

Gold, Growth, and a Job-Light Economy

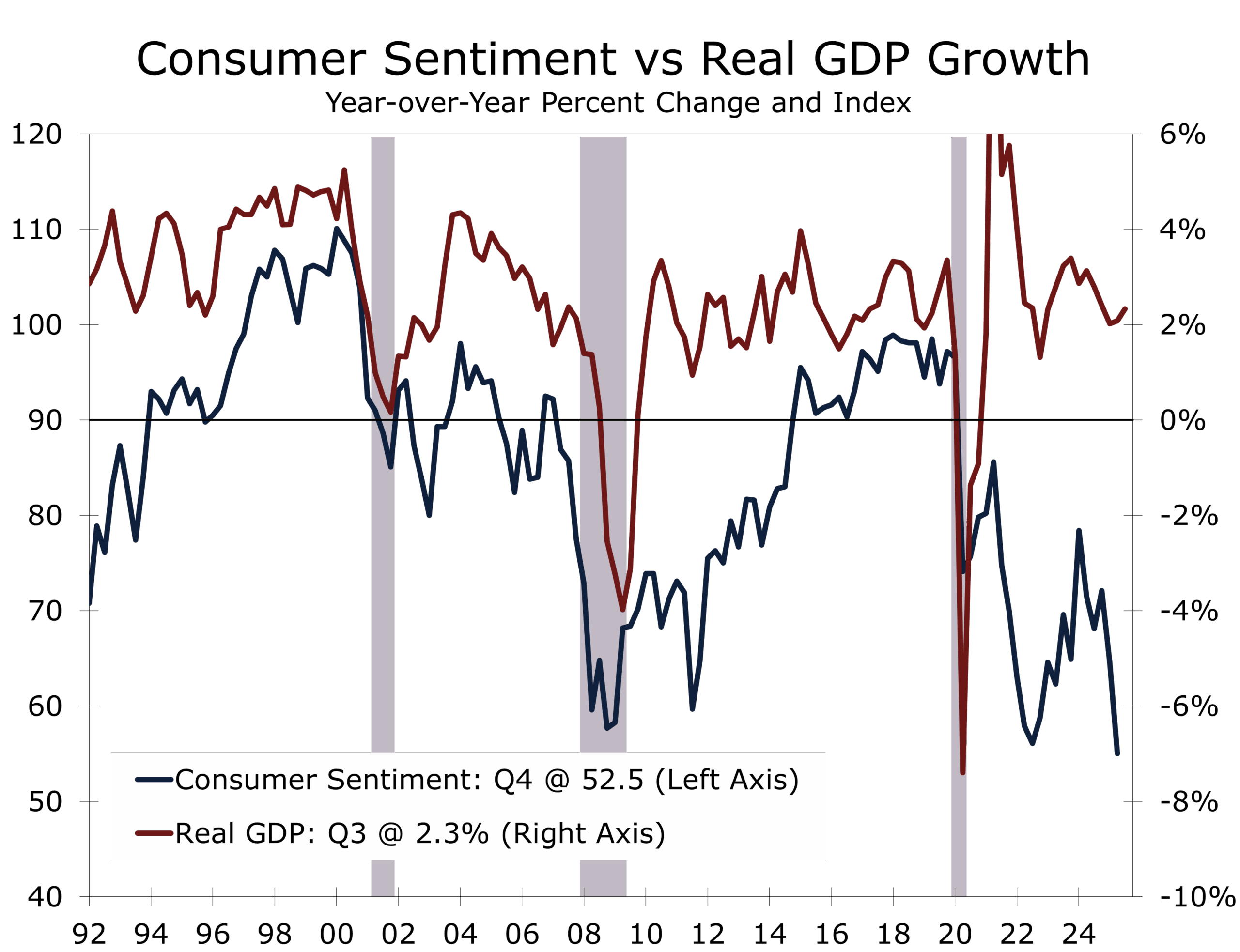

The final full week of 2025 delivered a familiar late-cycle paradox. The macro data still reads like an economy with plenty of altitude, with Q3 real GDP coming in at 4.3% annualized and up 2.3% over the past year, with growth powered by solid consumer spending and an AI-driven investment surge tied to reshoring and technology buildouts. Yet confidence data tells a different story. The economy increasingly feels like one experiencing vertigo.

Things appear to be spinning around the periphery. Consumer confidence fell again in December, with households citing employment and income concerns alongside the usual worries about inflation and politics. The message is not that the expansion is ending. Rather, progress is becoming harder to feel in real time. That disconnect is a defining feature of this job-light, capex-heavy cycle and shows up repeatedly in headlines about how difficult it remains for new entrants and re-entrants to secure employment.

The economy is growing, but the labor market is no longer the messenger.

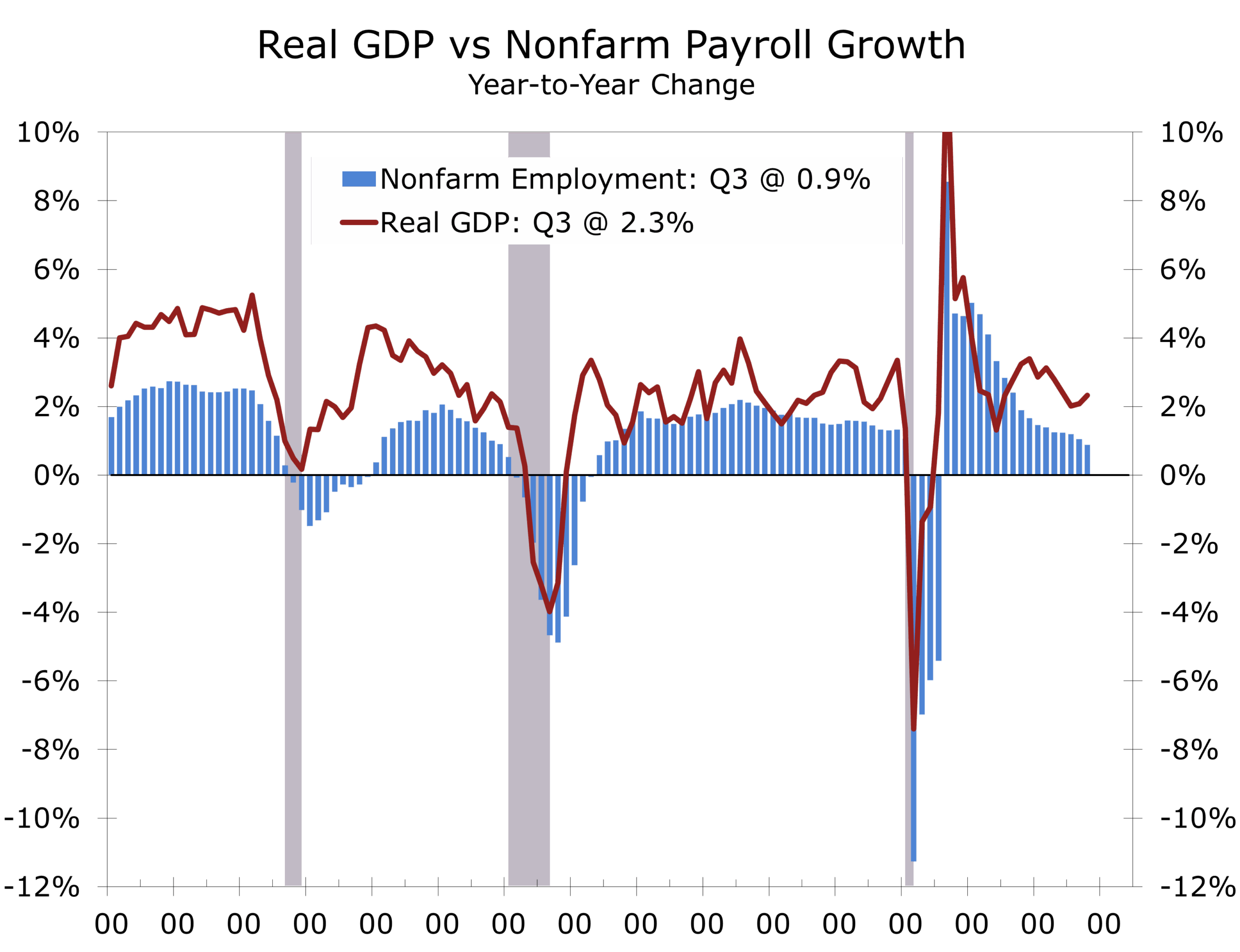

Under the hood, the labor market is still behaving, at least in the narrow sense that matters for recession risks. Initial jobless claims fell to 214k in the latest week, a historically low level inconsistent with broad-based layoffs. But the labor picture is more nuanced. Turnover remains exceptionally low. With fewer workers voluntarily quitting, firms are hiring less aggressively. Layer in the effects of AI adoption, earlier over-hiring, and lingering reluctance to trim payrolls after the pandemic, and the result is a labor market that looks calm on the surface while quietly adjusting to a more cautious, lower-churn footing.

Labor market uncertainty remains one of the largest open questions for the economy and the 2026 outlook. Revised employment data due early next year are expected to show that job growth slowed sharply in late 2025 and may have briefly turned negative. That would be unusual for an expanding economy. Historically, even modest employment declines have tended to coincide with the onset of recession.

Not every hiring slowdown signals a recession. This job-light expansion appears to be by design.

This cycle may be different, which remains the most dangerous phrase in forecasting. Productivity gains, capital investment, and deliberate talent retention are playing a larger role than broad-based hiring. Rather than an expansion riding a wave of payroll growth, today’s economy is advancing with leaner workforces and stronger productivity, a possible sequel to the “New Economy” dynamics of the late 1990s. Growth is being powered less by headcount and more by automation, efficiency, and strategic staffing, including retaining experienced workers, selectively outsourcing, and relying more heavily on contract and temporary labor.

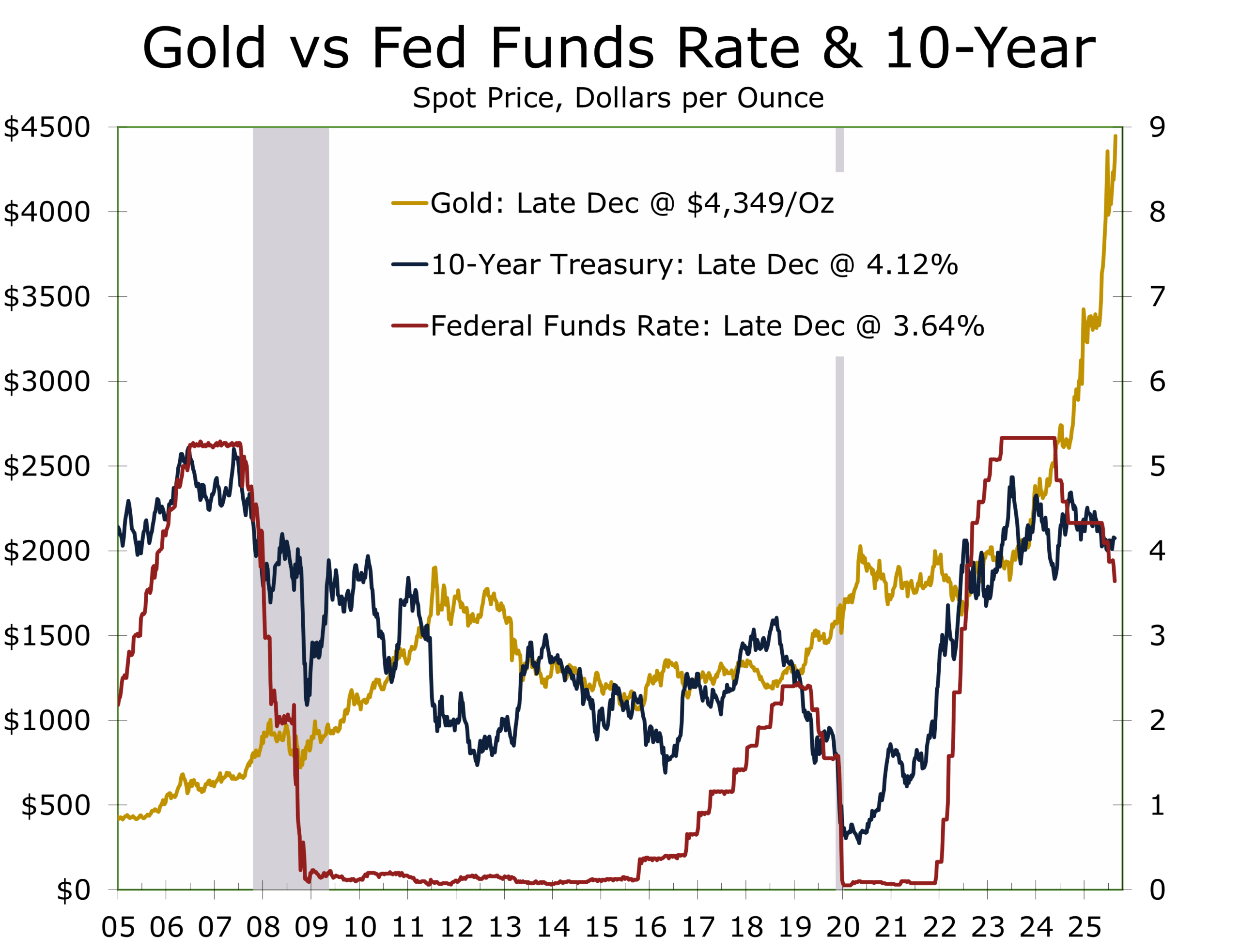

Markets appear to be reading from the same script. Risk assets are closing the year on a firm note, but the more revealing signals came from hedges rather than headlines. A weaker dollar and a renewed bid for precious metals, specifically silver and gold, echo a familiar holiday refrain from Rudolph the Red-Nosed Reindeer that is now hard to get out of my head. These moves suggest investors are positioning for a sequel economy defined less by labor abundance and more by real constraints, including power availability, debt capacity, and the ability to absorb and deploy rapid gains in artificial intelligence.

Markets are hedging constraints, missing data points, and policy uncertainty—not contraction.

Part of the move reflects rate-cut expectations and renewed questions about Federal Reserve independence. It also points to growing recognition that the industrial economy is colliding with bottlenecks in electrification-era inputs. Data center and power projects are crowding out other industrial projects at the margin. The tape is not signaling a crisis. Instead, it is quietly pricing a regime shift toward hard assets, supply security, and resilience premia in an economy running more on efficiency than expansion. One encouraging signal has been the recent strength in transportation stocks, which may be hinting at an end to the long-running freight recession.

Recent Developments: Signals Beneath the Noise

That resilience theme extends beyond economics into geopolitics. Ukraine is moving toward a negotiation framework, with a revised 20-point peace proposal reportedly under discussion with President Trump, even as the hardest questions around territorial concessions and security guarantees remain unresolved. In the Middle East, Trump and Netanyahu are preparing talks on the next phase of a Gaza plan, though the ceasefire architecture remains fragile, particularly following recent comments from Iranian leadership and the apparent launch of three satellites.

In Asia, China’s largest-ever drills around Taiwan served as a reminder that geopolitical tail risks are no longer confined to the margins. They are part of the main distribution. Trump’s more aggressive posture toward Venezuela and recent arms commitments to Taiwan may also be contributing to Beijing’s willingness to apply pressure on the island.

Looking Ahead

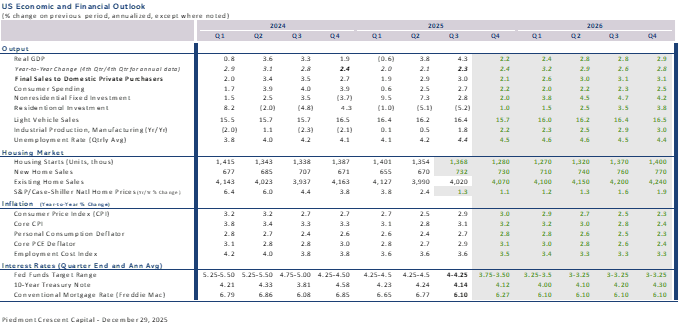

As we turn the page to the first week of the new year, attention will shift back to fresh economic data. The ISM manufacturing index, December’s employment report, and updated readings on consumer sentiment will help set the tone for how 2026 begins.

Before that, the coming week features a lighter calendar, offering a brief pause to recharge and, perhaps, watch a bit more football. Key releases include the FOMC minutes from the December 9–10 meeting on Tuesday, weekly jobless claims on Wednesday, and global and U.S. PMI indices from S&P on Friday. As always, we will be watching for evidence that reinforces or challenges the soft-landing narrative and tests whether the Fed’s cautious easing path remains appropriate. Our preference would be for cuts at alternating meetings, extending the easing cycle without materially lowering the terminal rate.

For now, the economy appears to be staying on script, marked by cautious optimism, an affinity for gold, and a world that never quite sits still.

As we close out 2025, we want to thank our readers and clients for the continued engagement and dialogue. We wish you a healthy, prosperous, and thoughtful New Year, and we look forward to navigating 2026 together.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

December 29, 2025

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000