Highlights of the Week

- The expansion remains intact but is navigating a materially narrower channel as the Iran shock evolves from event to constraint.

- Markets have repriced toward policy-constraining inflation, not a classic growth scare.

- The Fed is on hold and the bar to easing this year has risen meaningfully.

- The labor market remains stable on the surface but fragile underneath.

- The energy shock is broadening into a multi-channel supply disruption beyond oil, encompassing chemicals, fertilizer and key industrial materials.

- The apparent pause in the escalation of the Iran conflict appears credible, though fragile, with recent developments suggesting at least a temporary halt to planned strikes and tentative movement toward negotiations. This pause may open the door to a Venezuela-style outcome, where sustained pressure redirects an ongoing conflict toward a negotiated equilibrium, even as U.S. forces and assets continue to build in the region.

Unknown Unknowns in Narrower Water

The past week marked a decisive turn in the cycle. What began as a central-bank-dominated narrative has been overtaken by energy, geopolitics, and the reintroduction of constraints. The Federal Reserve may still set the policy rate, but it is no longer setting the tone. That role now belongs to geopolitics, where oil flows and shipping lanes are only part of the equation, and where markets are increasingly forced to price the harder-to-quantify variables, namely President Trump’s often opaque strategic calculus and the uncertain present and future leadership of Iran.

Three weeks into the Iran shock, markets have stopped reacting and started repricing. The distinction matters. Initial reactions tend to overshoot and reverse, particularly on Fridays and Mondays. Repricing embeds. Oil, the dollar, equity markets, and Treasury yields are no longer moving independently. They are moving as a system, and that system is signaling something unambiguous: the path forward for policy has narrowed.

“There are known knowns…there are known unknowns…but there are also unknown unknowns—the ones we don’t know we don’t know.” — Donald Rumsfield

This is increasingly a market defined by what Donald Rumsfeld once called the “unknown unknowns,” where the greatest risks are not the ones investors can model, but the ones they cannot yet fully see.

This is not a classic risk-off environment. It is something more nuanced and more challenging. Markets are not primarily pricing a collapse in growth. They are pricing a constraint on policy. Oil has risen enough to lift near-term inflation expectations, but not enough to immediately crush demand. Yields have moved higher, not lower. The dollar has firmed. Even gold has struggled to behave like a traditional haven, reflecting higher real rates rather than panic. Taken together, this is the signature of a stagflation scare in its early, more subtle phase. The first casualty is not growth, but flexibility, meaning the ability of policymakers to ease, of markets to rally on weaker data, and of households and businesses to absorb higher costs without cutting back somewhere.

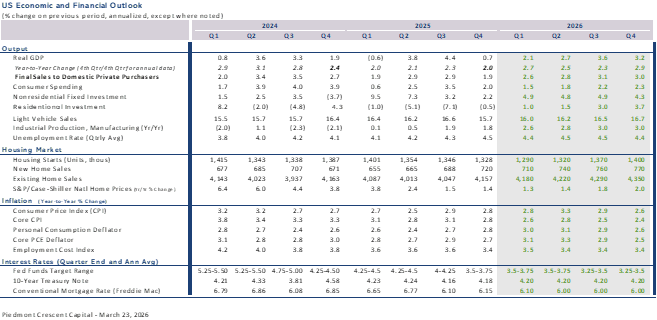

The Federal Reserve finds itself in a familiar but unenviable position. It held rates steady at its March meeting and emphasized uncertainty tied to developments in the Middle East. The tone was more cautious than dovish or hawkish. Policymakers explicitly acknowledged the risk that higher oil prices could feed into inflation expectations, even as the labor market shows signs of softening beneath the surface. The result is a policy stance that is neither tightening nor easing but rather waiting for more information. In this instance, “Wait and see” is less of a placeholder and more of a strategy for now. The futures market does not see another cut until the middle of 2027.

History offers a useful frame for understanding the moment, and it is not a comfortable one. The current posture sits somewhere between Chamberlain’s “peace for our time” and Kennedy’s pledge to pay any price and bear any burden in defense of strategic interests. An early capitulation, or TACO moment, would carry series long-term negative implications for the security of the Middle East, Asia and U.S. homeland. The decision to pay any price and bear any burden comes down to U.S. taxpayers picking up the tab for stakes and burdens than impact much of the world and energy-dependent Europe in particular.

This puts the situation somewhere in the middle defined by caution but shadowed by the risk of escalation. Policymakers are attempting to avoid overreaction while recognizing that underreaction carries its own costs. There is also, still at the far edge of the distribution, the possibility of something closer to a Venezuela-style outcome, where the current conflict is redirected, under sustained external pressure, toward a negotiated equilibrium rather than further escalation. That framework aligns with President Trump’s stated objective of bringing Iran’s enriched uranium under control and establishing joint oversight of the Strait of Hormuz, a solution that would seek to convert military leverage into a new geopolitical arrangement.

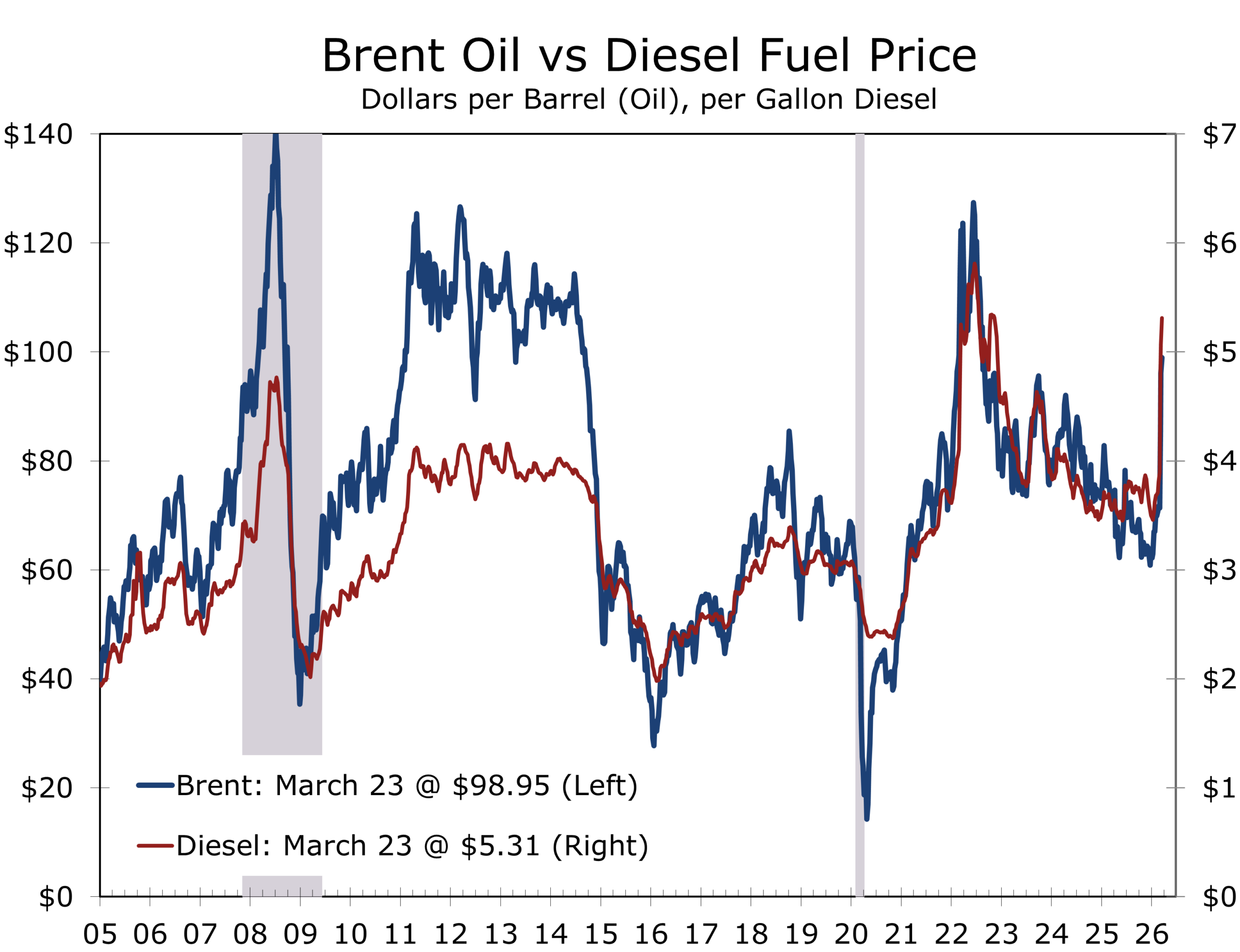

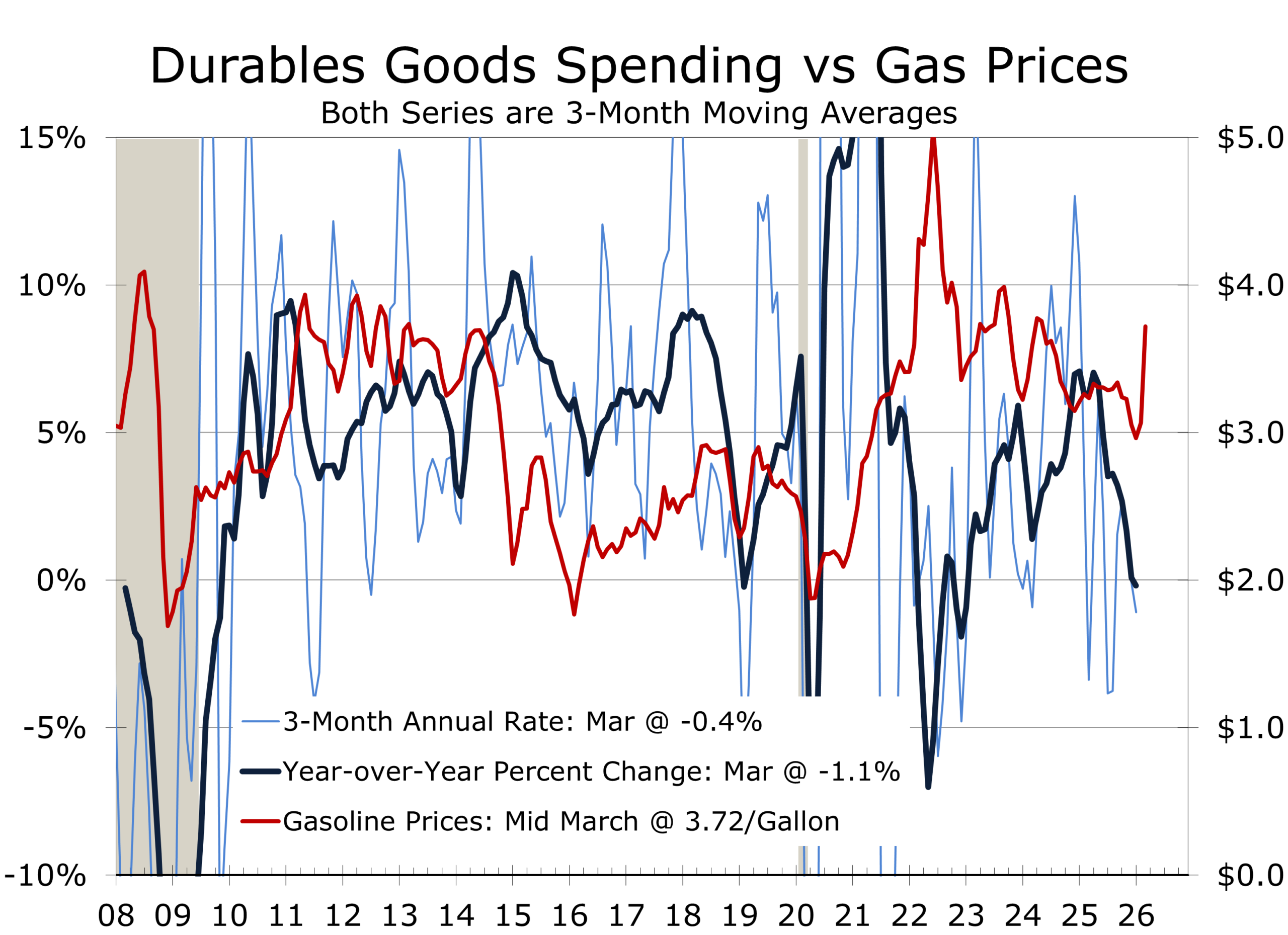

For now, the energy shock is doing what energy shocks typically do. It is acting like a tax on the global economy. Higher gasoline and diesel prices are already eroding purchasing power, particularly for lower-income households, while also raising costs across transportation, logistics, and production. Airlines, railroads and trucking firms are already making hard choices to control cost. The more important development, however, is that the shock is broadening. This is no longer just about oil and diesel fuel. Fertilizer, liquefied natural gas, industrial gases, and shipping costs are all being drawn into disturbance. When supply shocks move beyond a single commodity and into the wider production network, they tend to persist longer and prove more difficult to unwind, particularly if fears of shortages and higher prices become embedded in decision-making.

The labor market, at least on the surface, continues to hold. Initial jobless claims remain low, and layoffs are contained. Yet the underlying dynamics are less reassuring. Hiring has slowed materially, and much of the apparent stability reflects a lack of firing and reduced voluntary turnover rather than resilient demand. This “no-hire, fewer-quits, no-fire” equilibrium is consistent with a productivity-driven expansion, where firms are producing more with fewer workers, supported by capital investment and technological gains. With turnover down by roughly one-third from its prior norm, businesses not only need to hire fewer workers but also spend less on training and onboarding, while benefiting from a more experienced workforce. This is an equilibrium that can shift quickly, however, if demand weakens further.

Housing offers a similar story. Earlier in the year, lower mortgage rates provided a modest lift, raising hopes that the sector might stabilize. That window now appears to be closing. Rising Treasury yields have pushed mortgage rates higher again, affordability remains stretched, and inventories are beginning to build. Housing does not need to lead the expansion, but it does need to find a floor. For now, higher rates are delaying that process. As a result, residential investment is likely to remain a modest drag on growth in the near term rather than the source of support seen in prior cycles.

Globally, the constraint is more pronounced. Europe remains particularly exposed due to its reliance on imported energy and a more fragile industrial base. Central banks are responding accordingly. The ECB has shifted in a more hawkish direction, the Bank of England is warning of renewed inflation pressures, and even in Japan the tone is beginning to change. The common thread is clear: higher energy prices are limiting the ability of central banks to support growth.

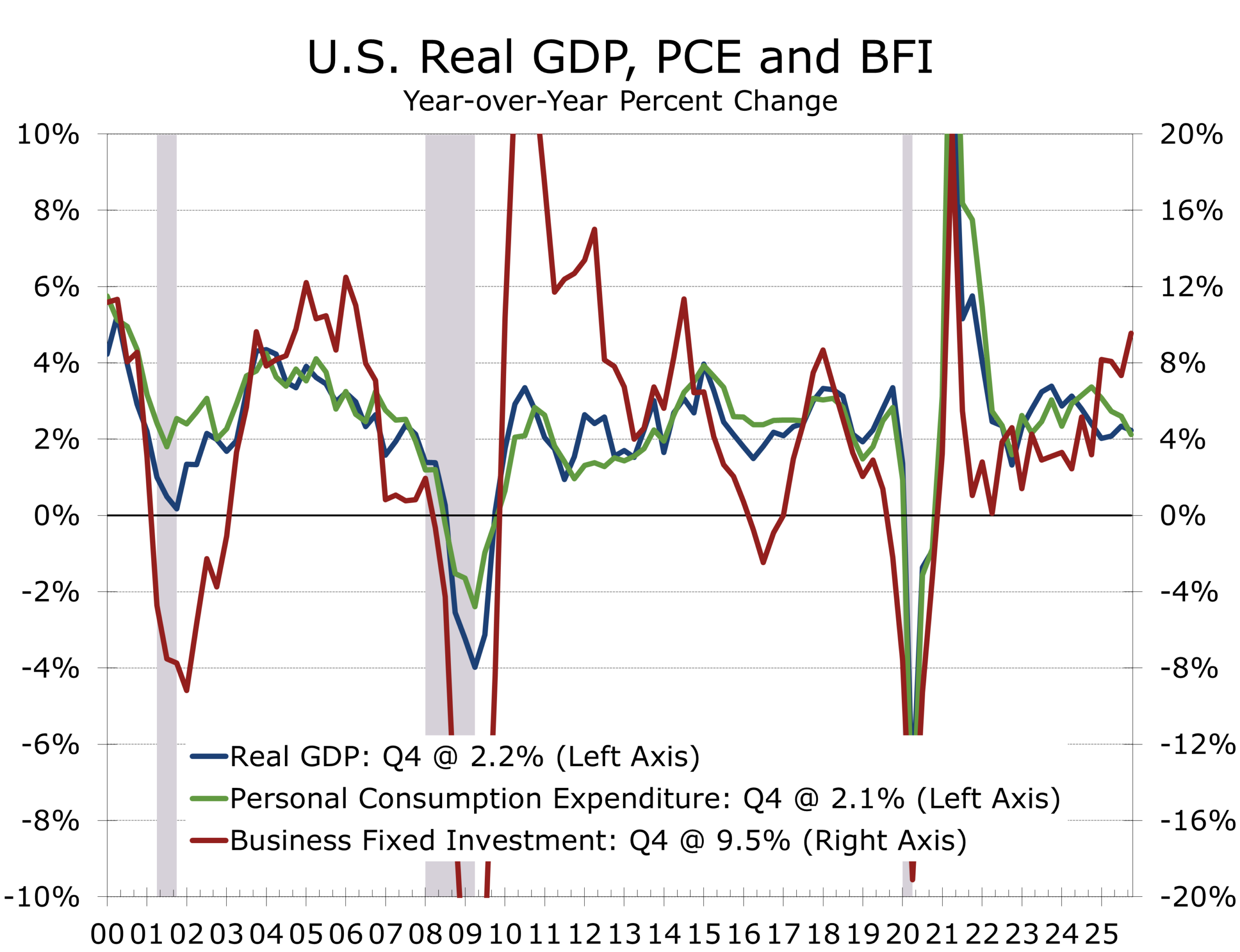

This tension between sustaining growth and preventing a supply shock from evolving into broader inflation is now the defining feature of the cycle. The broader framework we have outlined in recent months still holds. This remains a capital-led expansion, driven by infrastructure, reshoring, and artificial intelligence. Productivity gains are real and continue to support output, but they are unevenly distributed. Capital spending can remain firm, supported by long lead times and strategic investment decisions, even as consumer spending becomes more volatile. The result is a two-speed economy, where strength at the top coexists with increasing strain at the household level.

Looking Ahead

Looking ahead, the usual calendar of economic data matters, but it is no longer the primary driver. Productivity, consumer sentiment, and inflation expectations will provide important signals, but markets are taking their cues from a different set of variables. Oil prices, the dollar, long-term yields, equity market breadth, and inflation expectations measures now form the core dashboard. These are the indicators that will determine whether the current shock stabilizes, intensifies, or begins to fade.

The range of outcomes is relatively clear. A de-escalation in the Middle East would allow oil prices to stabilize, financial conditions to ease, and the Federal Reserve to regain some flexibility. A prolonged disruption would keep inflation elevated and growth below trend, forcing policymakers to remain cautious for longer. A further escalation, particularly one that damages energy infrastructure or meaningfully impairs shipping through the Strait of Hormuz for an extended period, would force difficult trade-offs for businesses and policymakers and further narrow the margin for error.

For all the disruption stemming from the Iran crisis, the expansion is still underway. The underlying structure remains intact. Jobless claims are low, capital investment is firm, and productivity gains continue to support output. But the environment has changed. The system is more sensitive, and the buffer provided by stable energy prices, easing inflation, and improving financial conditions has diminished.

The global economy is still moving forward. It is simply doing so in shallower water, with less room to maneuver, more complex trade-offs, and a policy cushion that is thinning by the week.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

March 23, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000