Highlights of the Week

- Policy risk, not economic data, set the market tone, even as growth, spending, and labor indicators remained constructive.

- Gold and silver crossed psychological thresholds as hedges against policy and institutional uncertainty, with positioning amplifying the move in silver.

- Japan delivered the most consequential signal in global rates markets, as a selloff in super-long JGBs helped reprice term premia worldwide.

- Corporate behavior is shifting toward certainty, with more firms choosing to lock in funding rather than wait for calmer markets.

- The week ahead is light on data but heavy on policy signaling, increasing the risk that headlines overpower fundamentals.

- Greenland marks a shift from strategic ambiguity to permanent U.S. access, achieved through alignment rather than acquisition.

Policy Shock as the Primary Catalyst

This was a week in which geopolitics, rather than macroeconomic data, set the market’s tone. The Greenland episode—tariff threats deployed as leverage and then partially walked back—was notable less for its substance than for its speed. Markets reacted to each development the way they once reacted to payrolls or inflation surprises.

Risk assets sold off, Treasury yields rose, and the dollar softened before partial relief emerged as tensions eased. The pattern itself has become familiar. What stood out was how quickly correlations shifted. At several points, equities and long-duration bonds declined together, a reminder that policy shocks can overwhelm the traditional diversification playbook.

For CFOs and treasurers, the implication is straightforward. Policy posture has become a first-order macro variable. When it changes abruptly, markets adjust through the term premium rather than through growth expectations.

The Data Beneath the Noise

Lost in the headline churn was a reasonably constructive set of economic releases from the holiday-shortened week. The data reinforced a tension that has been building for months: the economy continues to expand, even as markets behave as though the margin for error has narrowed.

When geopolitics outpace the economic data, term premia tend to adjust.

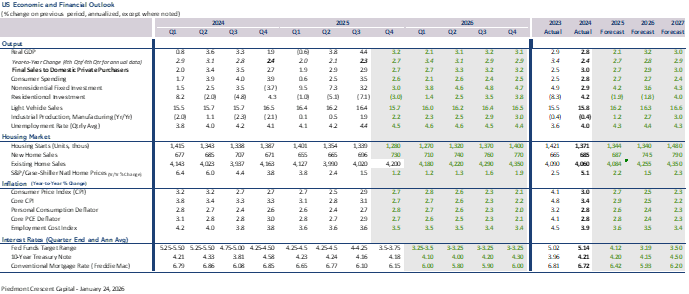

Growth and GDP

Revised GDP figures confirmed that the economy entered year-end with solid momentum. Prior-quarter growth was revised higher, and forward-looking indicators continue to point to above-trend activity. The Atlanta Fed’s GDPNow estimate for Q4 remains elevated, at +5.4%, suggesting growth has not meaningfully rolled over, which is perplexing given the weaker nonfarm payroll data.

Personal Income, Spending, and PCE Deflators

Personal income growth was modest but steady, while consumer spending posted another firm monthly gain. Households continue to spend, though without much enthusiasm. PCE inflation came in broadly as expected, with headline and core measures still above target but no longer accelerating. From a policy perspective, the data argue for patience rather than urgency.

Labor Markets

Initial unemployment claims edged higher but remain near historically low levels. The labor market continues to exhibit a low-hire, low-fire pattern: hiring has slowed, but layoffs remain contained.

That combination presents a familiar puzzle. Payroll growth has softened in a way that would typically be associated with a slowdown, yet layoffs show no sign of accelerating. Historically, that mix is inconsistent with recession.

The economy is not flashing red. Markets are reacting to governance risk, not growth risk.

Consumer Sentiment

The University of Michigan sentiment index improved modestly, but from depressed levels. Consumers are less pessimistic than late last year, though far from confident. The message aligns with the spending data. Households are coping, but also sulking about continued high, albeit no longer rapidly rising, prices for key necessities.

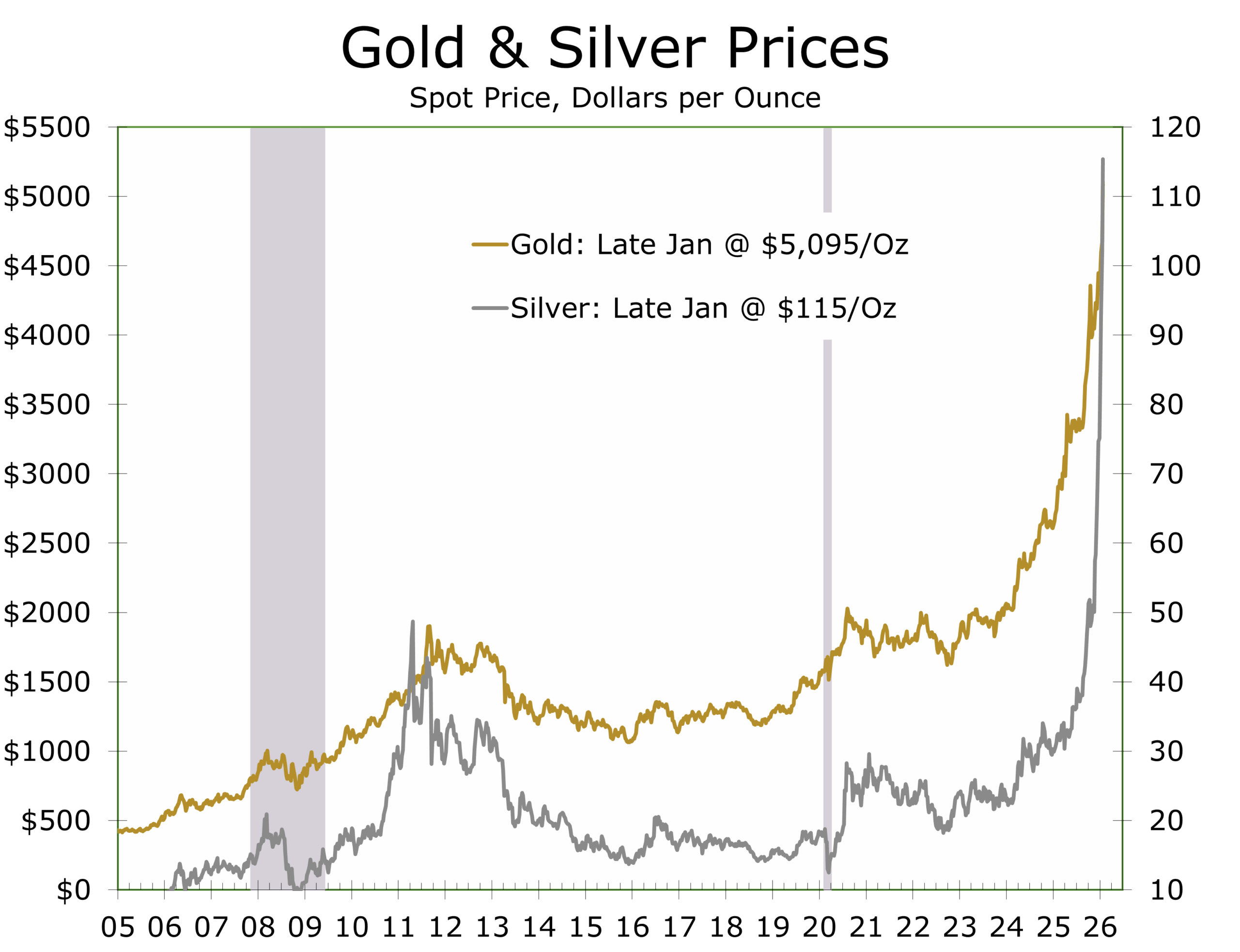

Gold, Silver, and the Price of Uncertainty

Precious metals delivered the clearest emotional signal of the week. Gold surged to within striking distance of $5,000 per ounce, while silver moved decisively through $100. These were not incremental moves. They were threshold events.

Gold behaves like insurance. Silver behaves like insurance—with leverage and air pockets.

The character of the rally matters. Gold’s advance increasingly resembles a hedge against policy uncertainty and institutional credibility, reinforced by central-bank accumulation and private-sector demand for assets without counterparty risk. This looks less like an inflation trade and more like a confidence trade.

Silver told a slightly different story. Alongside the macro narrative, its smaller and more volatile market structure amplified momentum. Crowded positioning and forced short covering likely accelerated the move once key technical levels gave way. That does not negate the signal, but it does make silver a higher-beta expression of the same underlying concern.

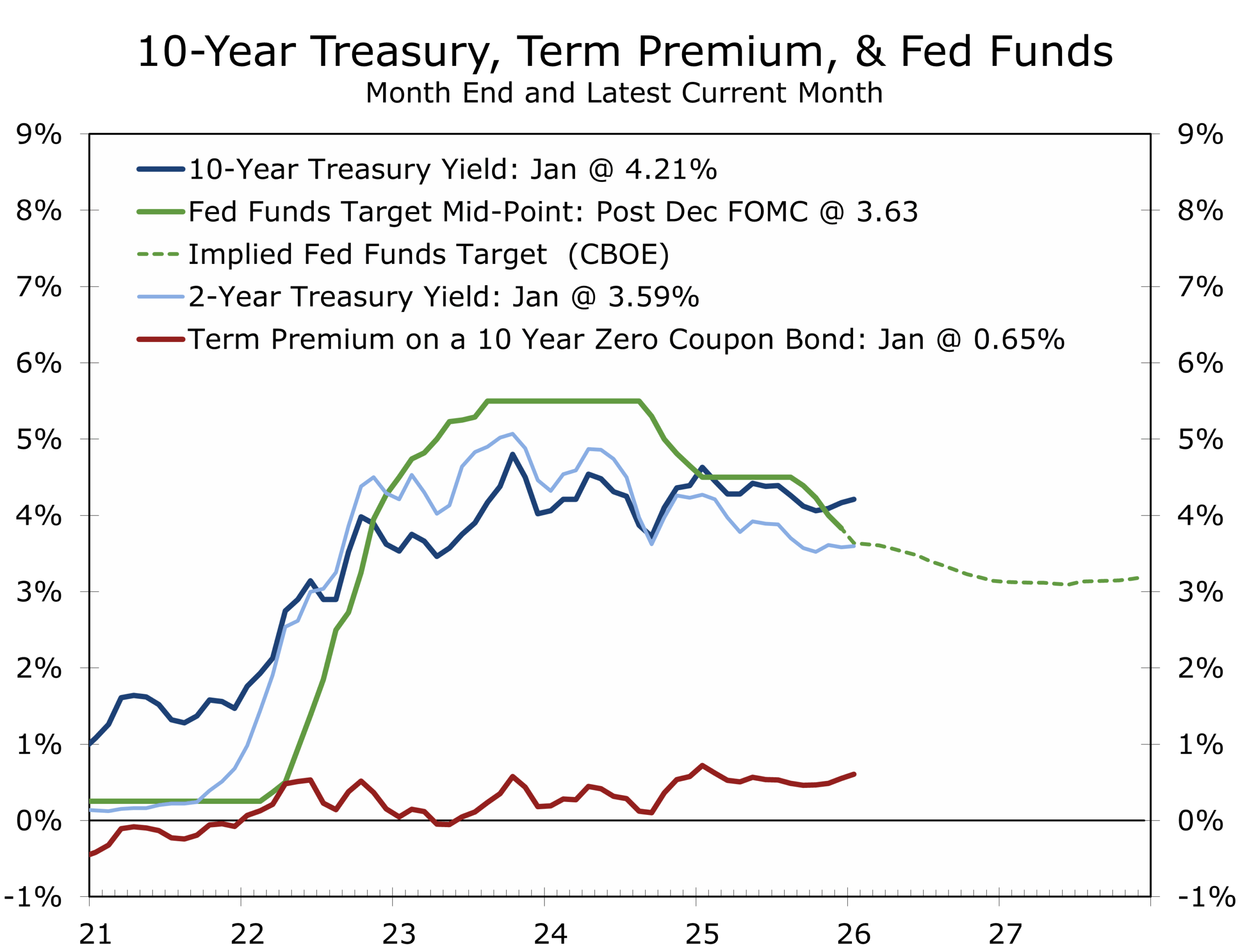

Japan and the Return of Global Term Premium

This past week’s most underappreciated development came from Tokyo. Japanese government bonds, long the anchor of global duration markets, experienced a sharp selloff. Yields on 30- and 40-year JGBs rose to levels that would have seemed implausible just a few years ago.

The implications were immediate. As Japan’s super-long yields moved higher, global investors were forced to reassess what long-dated “risk-free” assets should yield elsewhere. U.S. Treasuries felt the pressure, particularly at the long end, with the curve steepening even as risk sentiment deteriorated.

This was not a warning about U.S. credit quality. It was a reminder that the global supply of patient, price-insensitive buyers of long-dated sovereign debt is not infinite. When Japan’s anchor slips, term premia become more mobile everywhere.

Japan did not cause U.S. yields to rise. It did, however, raise the global hurdle for duration.

For treasury teams, this matters. Long Treasuries remain liquid and credit-safe, but they are no longer immune to flow-driven volatility.

Certainty Is the New Optionality

Against this backdrop, corporate behavior is changing. Firms are increasingly refinancing earlier and locking in rates rather than waiting for a cleaner window. This is not panic. It is a rational response to a market in which policy headlines can move the curve more than a quarter’s worth of economic data.

In a volatile policy regime, the cheapest debt is not always the best debt.

Notably, this shift is occurring even as the economic backdrop remains constructive. GDP growth is solid, layoffs are limited, and real-time growth estimates remain elevated. The move toward certainty reflects volatility management, not recession anxiety.

Energy and the Cost of Reliability

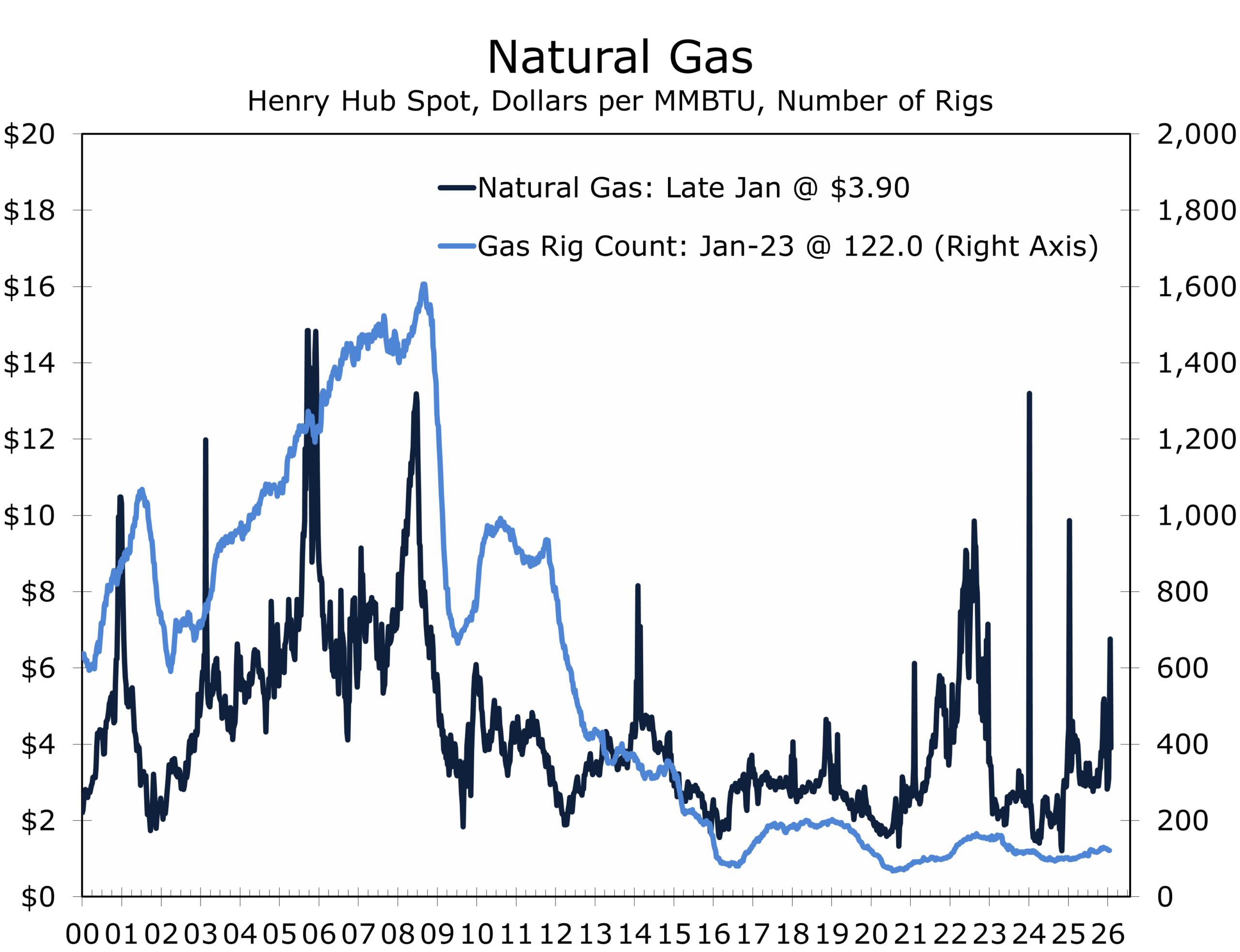

Energy markets offered a parallel reminder that volatility is no longer theoretical. Natural gas prices surged as extreme winter weather drove a sharp increase in heating demand, disrupted production, and stressed regional power grids, pushing wholesale electricity prices to extraordinary levels in parts of the country. The speed of the move, rather than its magnitude, caught many participants off guard. While the spot price has jumped to nearly $7 MMBtu the March futures are well under $4 MMBtu.

For energy-intensive firms, the issue was less about price than about continuity. Energy risk now includes availability and operational resilience, not just cost. That reality increasingly pulls treasury, operations, procurement, and capital planning into the same risk-management conversation.

Energy risk is shifting from price volatility to reliability risk.

What Comes Next for Natural Gas

Looking ahead, the balance of evidence suggests that the recent spike in natural gas prices is likely to prove acute rather than prolonged. As temperatures normalize, production recovers, and storage draws moderate, spot prices should retrace some of their gains. However, the episode reinforces a more structural shift: U.S. gas markets are now tightly linked to global conditions through LNG exports, leaving prices more exposed to weather shocks, infrastructure constraints, and geopolitical spillovers than in prior cycles.

For corporate buyers, this new environment argues less for betting on price reversals and more for planning around volatility as a recurring feature rather than a tail risk. The world is full of surprises, and the weather is just the latest one to assert itself.

The Week Ahead: Data Quiet, Policy Not so Much

The coming week is light on market-moving data but heavy on policy signaling.

When the data are quiet, that makes room for policy noise to get louder.

The January FOMC meeting is expected to result in no change in policy rates; the focus will be on language, particularly whether the Committee acknowledges that policy uncertainty and geopolitical risk are tightening financial conditions at the margin. Durable goods orders and jobless claims should confirm ongoing expansion rather than alter the outlook. With fundamentals broadly stable, markets remain vulnerable to headline-driven volatility. On the policy front, the fatal shooting of a Minneapolis resident by federal immigration agents has intensified partisan opposition to the Department of Homeland Security funding bill, with Senate Democrats vowing to oppose the measure absent substantive reforms—raising the prospect of a partial government shutdown as early as the end of this week and injecting a new political risk premium into markets.

With fundamentals broadly stable, markets remain vulnerable to headline-driven volatility. As the Greenland episode demonstrated, policy signaling now moves prices faster than most scheduled releases.

What This Past Week Taught Us

This was a week about confidence rather than cycles. The data continues to describe an economy that is expanding and cooling gradually, not one on the brink of recession. Markets, however, are pricing governance risk, policy uncertainty, and global term-premium dynamics with increasing urgency.

Gold and silver reflected that shift first. Japan’s bond market translated it into rates. Corporate treasurers are responding by paying for certainty. In that sense, the most important signal of the week did not come from a data release. It came from behavior.

Piedmont Perspective: Trump, Greenland, and the Panama Canal Lesson America Forgot

Donald Trump’s interest in acquiring Greenland was widely dismissed as diplomatic theater. In reality, it reflected a strategic lesson drawn from recent history: strategic vacuums do not remain empty.

The Panama Canal is the cautionary precedent. The U.S. handover in 1999 was framed as a diplomatic success, yet it created space for China to embed itself economically at one of the world’s most important trade chokepoints. Influence shifted quietly, not through force, but through capital. Formal sovereignty did not prevent strategic displacement.

Greenland marks a shift from strategic ambiguity to permanent U.S. access.

Greenland presents a similar dynamic in a colder geography. It anchors the GIUK Gap, hosts critical U.S. missile and space infrastructure, and holds significant mineral resources. China has tested the perimeter through mining proposals, infrastructure bids, and research activity, all framed as commercial engagement rather than strategic intent.

The Apparent U.S.–Greenland Understanding

While no formal treaty or transfer of sovereignty has been announced, markets and allied governments appear to be interpreting recent developments as a de-facto strategic alignment. The United States retains and expands its permanent military footprint, secures priority influence over infrastructure and foreign commercial access, and positions U.S. and allied firms as preferred partners in future critical-mineral development. Greenland remains sovereign, but strategic ambiguity has been sharply reduced.

Ownership has been replaced by permanence. Purchase has been replaced by control.

Trump’s Greenland Gambit was not about real estate. It was about preventing a repeat of Panama. In an era of renewed great-power competition, geography still matters, and drift rarely favors the incumbent power.

A longer standalone version of this Piedmont Perspective is available on our website.

Disclaimer: This publication has been prepared for informational purposes only and is not intended as a recommendation offer or solicitation with respect to the purchase or sale of any security or other financial product nor does it constitute investment advice.

January 26, 2026

Mark Vitner, Chief Economist

mark.vitner@piedmontcrescentcapital.com

(704) 458-4000